|

市場調査レポート

商品コード

1683990

インドの殺菌剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの殺菌剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 169 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

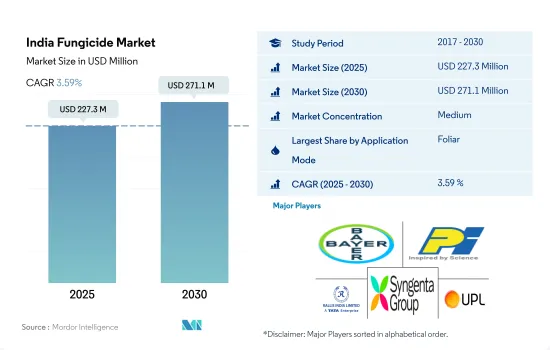

インドの殺菌剤市場規模は2025年に2億2,730万米ドルと推定され、2030年には2億7,110万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは3.59%で成長する見込みです。

真菌性病害の増加により、様々な散布方法での殺菌剤の需要が高まっています。

- 殺菌剤は、特定の要件や病害に応じて、さまざまな方法で散布することができます。これらの方法には、化学的散布、葉面散布、燻蒸、種子・土壌治療などが含まれます。これらの多様な散布方法は、条件に応じて様々な作物に殺菌剤を効果的に散布する上で重要な役割を果たしています。

- 2022年には、葉面散布が殺菌剤散布セグメントを支配し、60.9%の最大市場シェアを占めました。この方法は、葉上の病原体を直接標的にすることで葉面真菌病に対する効率的な保護を提供するため、非常に好まれました。葉面散布は、殺菌剤の植物組織への迅速な浸透・吸収を促進し、真菌病原体に対する効果的な作用を保証します。

- 殺菌剤種子処理は、植物発生の初期段階で真菌感染と闘うために広く使用されています。これらの治療は、種子の周囲に保護バリアを提供し、種子の腐敗、苗立枯病、湿害、根腐れなどの様々な病害を効果的に予防します。2022年のインドの殺菌剤市場において、殺菌剤種子処理剤セグメントは13.8%の市場シェアを占めました。

- 穀物・穀類生産者は、これらの作物が害虫の影響を受けやすいことから、作物のステージや害虫の発生状況に応じて、あらゆる散布方法を栽培に取り入れています。これらの作物では葉面殺虫剤散布が主に採用されています。

- 散布方法の選択は、特定の対象病害、作物の種類、病期、設備の有無など様々な要因に影響されます。殺菌剤市場は予測期間中にCAGR 3.9%を記録すると予想されます。

インドの殺菌剤市場動向

気候の変化と病害圧力の上昇が殺菌剤の消費を促進する見込み

- インドは、殺菌剤を含む作物保護化学物質の重要な消費国です。同国の農業セクターは規模が大きく、多様な種類の作物が栽培されているため、殺菌剤の需要が大きいです。真菌病は農産物の生産高と品質を著しく低下させ、かなりの損失をもたらします。殺菌剤は様々な病気の予防と管理に不可欠であり、農業生産の健全性と生産性を維持します。2022年、インドにおける殺菌剤の1ヘクタール当たりの消費量は101.5g/haでした。

- インドは作物の多様性が高く、米や小麦のような主食作物から綿花、果物、野菜のような換金作物に至るまで、多様な病害が発生しています。さび病、疫病、べと病、腐敗病は、これらの作物に対する菌類病害の壊滅的な影響の一例です。こうしたリスクを軽減し作物を守るため、インドの農家は殺菌剤を病害管理戦略の重要なツールとして利用しています。

- インドでは農業慣行の変化と食糧需要の増加により、作付面積が増加しています。農家は作付けを頻繁に繰り返したり、毎年作付けサイクルを増やしたりしています。このような作付集約化は、真菌性病害を含む病害発生のリスクの増大につながり、その結果、殺菌剤の必要性が高まる。インドにおける1ヘクタール当たりの殺菌剤消費量は、2017年から2022年にかけて5.0%増加しました。

- インド政府は、殺菌剤などの作物保護化学物質の使用を奨励するために、いくつかの計画やプログラムを策定してきました。政府は、補助金、普及サービス、研修プログラムを通じて、病害管理に殺菌剤を利用するよう農家に働きかけています。

気候変動が真菌の生存力や感染力、宿主の感受性を変化させ、新たな病害の発生につながります。

- 真菌病は重要な作物にとって大きな脅威です。真菌病原菌はインドの様々な作物で大きな収量損失をもたらしています。穀物では収量制限要因として知られています。インドにおける真菌感染による作物収量の減少は、年間約500万トンに上ると考えられています。

- Mancozebは広範囲の接触殺菌剤で、トウモロコシ、コメ、コムギ、野菜、果実、サトウキビ、タバコなどの作物で、アイスポット、リングスポット、いもち病、かさぶた、葉かび病、うどんこ病、茎亥病、茎腐敗病、褐色腐敗病、白色茎腐敗病、黒色茎腐敗病などの真菌病害の防除に使用されます。2022年には1トン当たり7,700米ドルと評価されました。

- プロピネブは接触殺菌剤で、2022年には1トン当たり3,500米ドルと評価されました。リンゴ、ジャガイモ、トウガラシ、トマトなどの作物で、疥癬早期・晩枯病、バッカイ腐敗病、うどんこ病、果実斑点病、褐色細葉斑点病など、さまざまな病害の防除に使用されます。

- Ziramは基本的な接触葉面殺菌剤で、2022年の価格は1トン当たり3,200米ドルです。主にジャガイモの早枯病と晩枯病、つる性植物とウリ科植物のべと病と黒腐病、リンゴのかさぶた、バナナのシガトカ、柑橘類のメラノースを防除します。

- 気候の変化は、真菌の生存能力、感染力、宿主の感受性に影響を与え、新たな病害の発生をもたらす可能性があります。例えば、インド亜大陸の西海岸、中央部、内陸半島、北東部の気候の温暖化動向は、ソルガムべと病(SDM)やトルコギク葉枯病(TLB)といったトウモロコシの病害にとって好条件を生み出しています。これらの要因は殺菌剤の価格と需要に影響を与えると予想されます。

インドの殺菌剤産業の概要

インドの殺菌剤市場は適度に統合されており、上位5社で53.11%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, PI Industries, Rallis India Ltd, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001692

The India Fungicide Market size is estimated at 227.3 million USD in 2025, and is expected to reach 271.1 million USD by 2030, growing at a CAGR of 3.59% during the forecast period (2025-2030).

The rising fungal diseases are driving the demand for fungicides in various application methods

- Fungicides can be applied using a variety of methods, depending on the specific requirements and diseases. These methods include chemigation, foliar application, fumigation, and seed and soil treatments. These diverse application methods play a crucial role in effectively applying fungicides to various crops, depending on the conditions.

- In 2022, foliar application dominated the fungicide application segment, which held the largest market share of 60.9%. This method was highly preferred as it provides efficient protection against foliar fungal diseases by directly targeting pathogens on leaves. The foliar application facilitates swift penetration and absorption of fungicides into the plant tissues, ensuring their effective action against fungal pathogens.

- Fungicide seed treatments are extensively employed to combat fungal infections in the early stages of plant development. These treatments provide a protective barrier around the seeds, effectively preventing a range of diseases such as seed rots, seedling blights, damping off, and root rots. The fungicide seed treatments segment held a market share of 13.8% in the Indian fungicide market in 2022.

- Grains and cereal crop growers are majorly adopting all the application methods in their cultivation based on the crop stage and insect pests as these crops are more susceptible to insect pests. Foliar insecticide application was majorly adopted by the farmers in these crops.

- The selection of the application mode is influenced by various factors, including the specific target disease, crop type, disease stage, and the availability of equipment. The fungicide market is expected to register a CAGR of 3.9% during the forecast period.

India Fungicide Market Trends

The changing climate and rising disease pressure are expected to drive the consumption of fungicides

- India is a significant consumer of crop protection chemicals, including fungicides. The country's agricultural sector is large, with diverse types of crops being cultivated, leading to a substantial demand for fungicides. Fungal diseases can significantly reduce agricultural output and quality, resulting in considerable crop losses. Fungicides are essential in the prevention and management of various diseases, maintaining the health and productivity of agricultural production. In 2022, the consumption of fungicides in India per hectare accounted for 101.5 g/ha.

- India has a high crop diversity, ranging from staple food crops like rice and wheat to cash crops like cotton, fruits, and vegetables, creating a varied disease spectrum. Rust, blight, mildew, and rot are a few examples of the devastating effects of fungal diseases on these crops. To mitigate the risks and protect their crops, farmers in India rely on fungicides as an important tool in their disease management strategies.

- Crop intensity is rising in India because of changing agricultural practices and increased food demand. Farmers frequently engage in repeated cropping or increase the number of crop cycles every year. This intensification leads to a higher risk of disease outbreaks, including fungal diseases, and, consequently, a greater need for fungicides. The consumption of fungicides in India per hectare increased by 5.0% from 2017 to 2022.

- The Indian government has developed several plans and programs to encourage the use of crop protection chemicals such as fungicides. The government has pushed farmers to utilize fungicides for disease management through subsidies, extension services, and training programs.

Climatic changes altering fungal survivability and infectivity as well as host susceptibility, leading to new disease outbreaks

- Fungal diseases are a major threat to important crops. Fungal pathogens cause large yield losses in different crops in India. They are known to be yield-limiting factors in cereals. The fungal infections-related decline in crop yield in India is believed to be approximately 5.0 million tons per year.

- Mancozeb is a broad-spectrum contact fungicide used to control fungal diseases like eyespot, ringspot, blast, scab, leaf mold, powdery mildew, stem bois, stem rot, brown rot, white stem rot, and black stem rot in corn, rice, wheat, vegetables, fruit, sugarcane, and tobacco crops. It was valued at USD 7.7 thousand per metric ton in 2022.

- Propineb is a contact fungicide valued at USD 3.5 thousand per metric ton in 2022. It is used to control various diseases like scab early & late blight dieback, buckeye rot, downy mildew, fruit spots, and brown, narrow leaf spot diseases in apple, potato, chili, and tomato crops.

- Ziram is a basic contact foliar fungicide priced at USD 3.2 thousand per metric ton in 2022. It mainly controls early & late blight of potatoes/tomatoes, downy mildew and black rot of vines and cucurbits, scab of apples, Sigatoka of bananas, and melanose of citrus.

- Climatic changes can affect fungal survivability, infectivity, and host susceptibility, resulting in new disease outbreaks. For instance, the warming trend in climate along the Indian subcontinent's west coast, central, interior peninsula, and northeast regions creates favorable conditions for maize diseases like sorghum downy mildew (SDM) and turcicum leaf blight (TLB). These factors are expected to influence the prices and demand for fungicides.

India Fungicide Industry Overview

The India Fungicide Market is moderately consolidated, with the top five companies occupying 53.11%. The major players in this market are Bayer AG, PI Industries, Rallis India Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 PI Industries

- 6.4.7 Rallis India Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms