|

市場調査レポート

商品コード

1683986

欧州の除草剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の除草剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 206 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

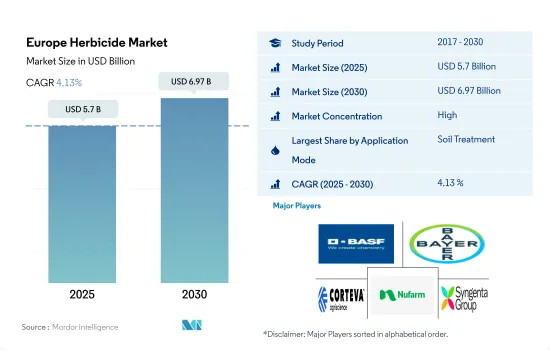

欧州の除草剤市場規模は2025年に57億米ドルと推計され、2030年には69億7,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは4.13%で成長する見込みです。

欧州では、土壌治療が除草剤散布の主要な手段として最も重要です。

- 欧州では、農業における雑草を効率的に管理するために、さまざまな除草剤散布方法が採用されています。適切な散布方法を選択することで、農家は費用対効果の高いソリューションを実現し、対象地域を正確にカバーし、無駄を最小限に抑えることができます。この効率向上により、除草剤の使用量が最適化され、最終的には農家の投入コストの削減につながります。

- 農業慣行では、土壌散布が除草剤使用の優勢なモードとして際立っており、2022年には除草剤散布セグメント全体の48.2%を占めました。この方法は主に穀物・穀類の栽培で採用されており、62.0%と最大の市場シェアを占めています。除草剤の土壌処理が好まれるのは、雑草の生育を防止または最小限に抑えることによって穀物や穀類の品質を保護する効果があるためです。これらの除草剤は、雑草の発生前や生育初期の段階で雑草を防除するのに有効です。

- さらに、葉面散布法は金額ベースで第2位の市場シェアを確保し、2022年には30.6%を占めました。この散布技術は雑草防除に有利であることが証明されており、特に正確なターゲティングが必要な作物、例えば対象植物の葉に直接散布する場合に有利です。この方法は出穂後の雑草を防除するのに有効で、多くの農作物で一般的に使用されています。

- 欧州の農業部門では、除草剤の使用は作物の生産性を最適化し、全体的な収益性を高めることに重点が置かれています。米国除草剤市場シェアのCAGRは4.1%と予測されており、市場は大きな成長が見込まれています。

小麦、トウモロコシ、テンサイなどの主要作物で雑草の蔓延が拡大し、これらの作物の栽培面積が拡大していることが市場を牽引する可能性があります。

- 真菌病や害虫とは別に、雑草は欧州農業部門の脅威となりつつあり、同地域の主要作物に甚大な被害をもたらしています。この地域における除草剤の消費は市場シェアの大半を占め、欧州の作物保護化学市場の34.7%を占め、2022年の市場価値は49億3,000万米ドルでした。

- 2022年の市場シェアは61.7%で、穀物・穀類が欧州の除草剤市場を独占しました。この優位性は、これらの作物における栽培面積の増加と雑草感染の増加に起因しています。作物の損失を引き起こす雑草は数多く存在します。実施された実験によると、研究者はフランスの小麦栽培で108種の雑草を発見し、欧州5カ国の小麦栽培(デンマーク、フィンランド、ドイツ、ラトビア、スウェーデン)では197種の雑草を発見しました。これらの雑草種の増加は、小麦、トウモロコシ、テンサイなどの主要作物に被害をもたらしました。毎年平均して、雑草が制御されないために、小麦の収穫損失は25~30%、トウモロコシの収穫損失は60~85%、テンサイの収穫損失は90~95%に達します。

- 欧州諸国では、土壌処理による除草剤治療が人気を集めています。この適用モードは2022年に48.2%の主要市場シェアを占めました。この優位性は、初期成長段階での雑草の防除効果に大きく関係しており、これにより作物の発芽が早まり、後の段階での除草剤の必要性が減少します。こうした利点から、この適用モードは成長すると予測され、予測期間中の推定CAGRは4.1%です。

- 欧州の除草剤市場は、主要作物における雑草蔓延の増加に牽引され、予測期間中にCAGR 4.0%を記録して成長すると予測されます。

欧州の除草剤市場の動向

農家は雑草の課題を管理する重要なツールとして除草剤への依存度を高めると予想される

- 欧州では、主に様々な要因によって除草剤の消費が大幅に伸びています。重要な要因のひとつは、何百万人もの人々が農村部から都市部に移住したため、手作業で除草できる労働者が不足していることです。その結果、除草剤の使用は、作物の収穫の質と量の両方を高める効果的でコスト効率の高い方法として浮上してきました。この動向は2019年から2022年にかけて特に顕著で、同地域の除草剤消費量は31.4%増加しました。

- 欧州諸国の中では、ドイツとフランスがこの地域の他国と比べて除草剤の使用率が高いです。2022年、ドイツは1ヘクタール当たり3,100の使用率を記録し、フランスは2,800で僅差で続いた。これらの国々は、農業生産の安定性、量、食糧安全保障を確保するため、除草剤を含む化学農薬の散布に大きく依存しています。雑草の持続性と適応性により、これらの地域では除草剤の散布率を高める必要があります。

- さらに、欧州の人口増加により、今後30年間の食糧需要の急増が予測されています。その結果、収穫量を増やし、作物を有害な雑草から守ることで、食糧生産に対するニーズの高まりに対応するため、除草剤の需要も高まると予想されます。

- したがって、食糧需要の増加、労働力不足、気候変動が、予測期間(2023年~2029年)における除草剤の消費を促進すると予想されます。農家は今後数年間、これらの課題に対処し、増加する食糧需要を満たし、持続可能な農業生産性を確保するための重要な手段として、除草剤への依存度を高めていくと思われます。

欧州諸国の中で、2022年のグリホサート価格はドイツとフランスが最も高く、1トン当たり1,150米ドルでした。

- 2022年、メトリブジンは1トン当たり1万6,700米ドルと評価されました。メトリブジンは、特定の広葉雑草やイネ科雑草を選択的に防除する除草剤として広く利用されている有機合成化合物です。メトリブジンの用途は、野菜や畑作物、レクリエーション地域の芝草、非農耕地に使用されます。製剤としては、湿潤性粉剤、乳化性濃縮剤、水分散性粒剤(乾燥流動性)、流動性濃縮剤などがあります。メトリブジンの散布には、空中散布、化学散布、地上散布などさまざまな方法が用いられます。

- ペンディメタリンペンディメタリンは残留活性を有する出芽前除草剤で、園芸、芝、林業など、さまざまな作物の一年生草や広葉雑草に対して幅広い防除効果を発揮します。主な作用機序は、影響を受けやすい雑草の細胞分裂と伸長を阻害し、根や芽の成長を妨げることです。2022年、この除草剤の価格は1トン当たり3,300米ドルでした。

- グリホサート系除草剤は、欧州で最も広く使用されている除草剤としての地位を維持しており、EUの除草剤市場の33%を占めています。2022年のグリホサート系除草剤の価格は1トン当たり1,200米ドルでした。グリホサート系除草剤の使用量は大幅な伸びを続けており、欧州、特にEUの大規模農業加盟国での販売量は依然として大きいです。Farm Accountancy Data Network(FADN)のデータは、農家の農薬への支出が全般的に増加していることを示しています。

- EU諸国の中で、2022年のグリホサートの価格はドイツとフランスが最も高く、それぞれ1トン当たり1,150米ドル、次いで英国が1トン当たり1,140米ドルでした。

欧州の除草剤産業の概要

欧州の除草剤市場はかなり統合されており、上位5社で65.24%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001688

The Europe Herbicide Market size is estimated at 5.7 billion USD in 2025, and is expected to reach 6.97 billion USD by 2030, growing at a CAGR of 4.13% during the forecast period (2025-2030).

In Europe, soil treatment holds the utmost importance as the primary mode of herbicide application

- In Europe, various modes of herbicide application are employed to efficiently manage weeds in agriculture. By selecting appropriate application methods, farmers can achieve cost-effective solutions, ensuring precise coverage of targeted areas and minimizing wastage. This enhanced efficiency optimizes herbicide usage, ultimately leading to reduced input costs for farmers.

- In agricultural practices, soil application stands out as the predominant mode of herbicide usage, which represented 48.2% of the total herbicide application segment in 2022. This method is majorly employed in the cultivation of grains and cereals, which holds the largest market share at 62.0%. The preference for soil treatment of herbicides is driven by their efficacy in protecting the quality of grains and cereals by preventing or minimizing weed growth. They are effective in controlling weeds during their pre-emergent and early growth stages.

- Furthermore, the foliar application method secured the second-largest market share by value, which accounted for 30.6% in 2022. This application technique has proven to be advantageous for weed control, particularly in crops that require accurate targeting, for instance, when applied directly onto the leaves of target plants. This method is effective for controlling post-emergence weeds and is commonly used in many agricultural crops.

- In the European agricultural sector, herbicide usage is focused on optimizing crop productivity and enhancing overall profitability. The market is expected to witness significant growth, with a projected CAGR of 4.1% in terms of the US herbicide market share.

Growing weed infestations in major crops like wheat, maize, and sugar beet and extending cultivation area under this crops may drive the market

- Apart from fungal diseases and insect pests, weeds are becoming a threat to the European agriculture sector, causing huge damage to the major crops in the region. The consumption of herbicides in the region occupied a majority market share, which accounted for 34.7% of the European crop protection chemical market, with a market value of USD 4.93 billion in 2022.

- Grains and cereal crops dominated the European herbicide market with a 61.7% market share in 2022. This dominance was attributed to the higher cultivation area and increased weed infections in these crops. There are numerous weed species causing crop losses. According to an experiment conducted, researchers found 108 weed species in France's wheat crops, and 197 weed species were found in five European countries' wheat cultivations (Denmark, Finland, Germany, Latvia, and Sweden). These increased weed species caused damage to major crops such as wheat, maize, sugar beet, and other crops. On average, every year, uncontrolled weeds cause wheat crop loss of 25-30%, maize crop loss of 60-85%, and sugar beet crop loss of 90-95%.

- The application of herbicide products through soil treatment is gaining popularity in European countries. This application mode occupied a major market share of 48.2% in 2022. The dominance is majorly related to the effectiveness of controlling weeds in the early growth stage, which could give more strength to the crops for faster germination, reducing the herbicide's necessity in the later stages. Due to these benefits, the application mode is projected to grow, registering an estimated CAGR of 4.1% during the forecast period.

- The European herbicides market is anticipated to grow, registering a CAGR of 4.0% during the forecast, driven by increased weed infestations in major crops.

Europe Herbicide Market Trends

Farmers are expected to increasingly rely on herbicides as a key tool to manage weed challenges

- Europe has experienced substantial growth in the consumption of herbicides, primarily driven by various factors. One significant factor is the shortage of workers available for manual weeding, as millions of people have migrated from rural to urban areas. As a result, herbicide usage has emerged as an effective and cost-efficient method to enhance both the quality and quantity of crop yields. This trend was particularly notable from 2019 to 2022, with herbicide consumption in the region increasing by 31.4%.

- Among European countries, Germany and France have high herbicide usage rates compared to others in the region. In 2022, Germany recorded a usage rate of 3.1 thousand per hectare, while France followed closely with 2.8 thousand per hectare. These countries heavily rely on the application of chemical pesticides, including herbicides, to ensure the stability, quantity, and food security of their agricultural production. The persistence and adaptability of weeds have necessitated higher rates of herbicide application in these regions.

- Furthermore, the increasing European population has projected a rapid growth in food demand over the next three decades. Consequently, the demand for herbicides is also expected to rise to meet the increasing need for food production by increasing the yield and protecting crops from harmful weeds.

- Therefore, the rising demand for food, labor shortages, and climate change are expected to drive the consumption of herbicides during the forecast period (2023-2029). Farmers will increasingly rely on herbicides as a key tool over the coming years to address these challenges and meet the increasing food demand, ensuring sustainable agricultural productivity.

Among countries in Europe, the price of glyphosate in 2022 was highest in Germany and France, priced at USD 1.15 thousand per metric ton

- In 2022, Metribuzin was valued at USD 16.7 thousand per metric ton. It represents a synthetic organic compound widely utilized as a herbicide with selective control over specific broadleaf weeds and grassy weed species. The applications of Metribuzin are used in vegetable and field crops, turf grasses in recreational areas, and non-crop areas. Its available formulations include wettable powder, emulsifiable concentrate, water-dispersible granules (dry flowable), and flowable concentrate. Various methods, such as aerial, chemigation, and ground application, are employed for Metribuzin's application.

- Pendimethalin is a pre-emergence herbicide with residual activities that deliver broad-spectrum control against annual grasses and broadleaf weeds across different crops, including horticultural, turf, and forestry. Its primary mode of action involves inhibiting cell division and elongation in susceptible weeds, thus impeding root and shoot growth. In 2022, this herbicide was priced at USD 3.3 thousand per metric ton.

- Glyphosate-based herbicides maintain their position as the most widely used herbicide in Europe, which accounts for 33% of the EU herbicide market. In 2022, the price of glyphosate-based herbicides stood at USD 1.2 thousand per metric ton. The usage of glyphosate-based herbicides continues to witness significant growth, while sales in Europe, especially in larger agricultural member states of the European Union, remain substantial. Data from the Farm Accountancy Data Network (FADN) indicates a general increase in farmers' spending on pesticides.

- Among EU countries, the price of glyphosate in 2022 was highest in Germany and France, each priced at USD 1.15 thousand per metric ton, followed by the United Kingdom at USD 1.14 thousand per metric ton.

Europe Herbicide Industry Overview

The Europe Herbicide Market is fairly consolidated, with the top five companies occupying 65.24%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms