|

市場調査レポート

商品コード

1683984

中国の除草剤市場:シェア分析、産業動向・統計、成長予測(2025年~2030年)China Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の除草剤市場:シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 162 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

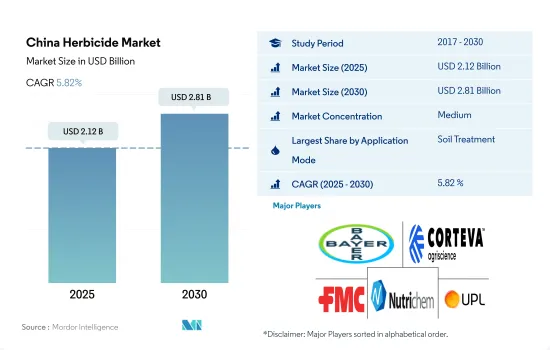

中国の除草剤市場規模は2025年に21億2,000万米ドルと推定され、2030年には28億1,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは5.82%で成長すると予測されます。

市場を牽引するのは、除草剤の効果的なコントロールに対するニーズです。

- 中国の農家は除草剤の散布にさまざまな方法を採用しています。これらすべての方法の市場規模は、2022年に17億8,000万米ドルとなりました。

- 2022年には、土壌治療法が8億4,150万米ドルと最も高い市場シェアを占め、除草剤市場全体の47.2%を占めました。土壌治療の人気は、特に雑草の種子を標的にし、作物の播種前にその発芽を阻害する、出穂前除草剤の利用におけるその有効性によるものです。2022年の市場シェアは31.9%で、除草剤の葉面散布は雑草防除に多くの利点をもたらします。除草剤が雑草の葉に直接接触し、葉の表面からの吸収が促進されるため、正確な標的を定めることができます。

- 化学灌漑法は、2017年の1億9,940万米ドルから2022年には3億3,980万米ドルに成長しました。2022年には、穀物・穀類分野で主に使用され、市場シェアの52.3%を占めました。これは、これらの作物ではマイクロ灌漑システムが普及しており、化学灌漑に適しているためです。

- 葉面散布は雑草防除においていくつかの利点があります。葉面散布は、除草剤が雑草の葉に直接接触するため、的を絞った作用が得られます。

- 燻蒸による雑草防除は、その特異性の高さと環境への配慮から、適用範囲が限定されるため、他の散布方法に比べて一般的とはいえないです。しかし、他の方法では防除できないような手ごわい雑草を効果的に防除することができます。

- 農家にとっての各施用方法の有効性、特異性、不可欠性を考慮すると、除草剤市場は2023年から2029年の予測期間中にCAGR 6.1%を記録すると予測されます。

中国の除草剤市場動向

輪作のような代替方法の採用と除草剤散布の技術的進歩-除草剤散布の制御がヘクタール当たりの消費量減少に寄与

- 中国における除草剤の使用量は、いくつかの重要な要因により大幅に減少しています。その一因として、輪作や生物的防除が、農業、園芸、造園などさまざまな分野における効果的な雑草管理に欠かせないツールとして認識され、採用されるようになってきたことが挙げられます。

- 輪作とは、同じ土地で異なる作物を特定の順序で長期間にわたって栽培することです。作物によって成長パターンや必要な栄養が異なるため、雑草のライフサイクルを断ち切るのに役立ちます。作物を交互に栽培することで、中国の農家は雑草の成長サイクルを乱し、雑草の個体数を減らし、除草剤を大量に使用する必要性を最小限に抑えています。

- 中国の農家は、さまざまな作物の雑草を効果的に管理するために生物防除剤を巧みに利用し、除草剤の使用量を顕著に減らしています。このような生物防除剤の導入は非常に有益であり、その結果、さまざまな農業慣行を通じて除草剤散布への依存度が低下しています。

- 中国の農家は、雑草管理を強化するために無人航空システム(UAS)の画像解析とコンピューター・ビジョン技術を利用しています。このアプローチを採用することで、雑草が発生している畝を特定し、雑草が発生していない畝はそのままにして、選択的に除草剤を正確に散布しています。この革新的な方法は、不必要な散布を避けることで除草剤の無駄を効果的に最小限に抑え、1ヘクタールあたりの除草剤消費量を全体的に削減しています。

- 農家は遺伝子組み換え作物を採用することで、追加投資の必要性を最小限に抑え、ヘクタールあたりの除草剤消費量を大幅に削減しています。

中国は世界最大のグリホサート生産・輸出国です。

- 雑草は中国の食糧安全保障にとって重要な作物生産にとって大きな制約となっています。500種を超える侵略的雑草が、中国の農業生産と生態系に対する脅威となっています。アトラジン、パラコート、グリホサートは中国で一般的に使用されている除草剤です。

- アトラジンは、さまざまな広葉雑草やイネ科植物の防除に広く使用されている除草剤です。中国では年間1万6,000トン以上(技術的に97%)のアトラジンが消費されています。アトラジンは主にトウモロコシやサトウキビ畑の一年生雑草の防除に使用されます。中国は世界のアトラジンの主要供給国のひとつです。2022年の価格は1トン当たり1万3,700米ドルでした。

- パラコートはグラモキソンの有効成分で、雑草やイネ科植物を防除します。また、収穫前の綿花のような作物の乾燥にも使用されます。パラコートは2022年に1トン当たり4,600米ドルと評価されました。中国はパラコート輸出大国で、パラコート生産量の80%以上が世界各国に輸出されています。

- グリホサートは有機リン系広域スペクトル浸透性除草剤であり、作物乾燥剤でもあります。2022年の価格はトン当たり1,100米ドルでした。グリホサートは主に、イネ科、スゲ科、広葉樹などの雑草の防除に使用されます。中国は世界最大のグリホサート生産・輸出国です。中国におけるグリホサートの生産量は、2010年の31万6,000トンから2017年には約50万5,000トンに増加しました。2017年、中国は30万トン以上のグリホサート技術を輸出し、世界のグリホサート需要の半分以上を満たしました。

- 国内の天候、雑草の蔓延、エネルギー価格、人件費などの要因が、有効成分の価格に大きく影響しています。

中国の除草剤産業の概要

中国の除草剤市場は適度に統合されており、上位5社で64.14%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, Corteva Agriscience, FMC Corporation, Nutrichem and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Nutrichem Co. Ltd

- Rainbow Agro

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001686

The China Herbicide Market size is estimated at 2.12 billion USD in 2025, and is expected to reach 2.81 billion USD by 2030, growing at a CAGR of 5.82% during the forecast period (2025-2030).

The market is driven by the need for effective control of herbicides

- Farmers in China employ various methods of herbicide application. The market for all these methods was valued at USD 1.78 billion in 2022.

- In 2022, the soil treatment method had the highest market share of USD 841.5 million, accounting for 47.2% of the total herbicide market. The popularity of soil treatment is due to its efficacy in utilizing pre-emergent herbicides, specifically targeting weed seeds, inhibiting their germination before crop sowing. With a market share of 31.9% in 2022, foliar application of herbicides offers numerous benefits in weed control. It provides precise targeting as the herbicides directly contact the weed's foliage, facilitating absorption through the leaf surfaces.

- The chemigation method grew from USD 199.4 million in 2017 to USD 339.8 million in 2022. In 2022, it was predominantly used in the grains and cereals segment, representing 52.3% of the market share. This is due to the prevalence of micro-irrigation systems in these crops, making them well-suited for chemigation.

- The foliar application offers several advantages in weed control. It provides targeted action, as the herbicides come into direct contact with the weed's foliage.

- The fumigation method of weed control is less common than other application methods due to its limited applicability attributed to its high specificity of usage and environmental concerns. However, it effectively controls a few tough weeds that other methods cannot.

- Considering the effectiveness, specificity, and essentiality of each application method for farmers, the market for herbicides is projected to register a CAGR of 6.1% during the forecast period from 2023 to 2029.

China Herbicide Market Trends

Adoption of alternative methods like crop rotation and technical advancements in herbicide application-controlled herbicide application contributes to lower consumption per hectare

- The usage of herbicides in China has reduced significantly due to several key factors. Some factors contributing to this are the growing recognition and adoption of crop rotation and biological controls as essential tools for effective weed management in various sectors, such as agriculture, horticulture, and landscaping.

- Crop rotation is a practice where different crops are grown in a specific sequence on the same land over time. This helps break the lifecycle of weeds, as different crops have different growth patterns and nutritional needs. By alternating crops, Chinese farmers have disrupted weed growth cycles, reduced weed populations, and minimized the need for higher use of herbicides.

- Chinese farmers skillfully employ biocontrol agents to effectively manage weeds in a wide array of crops, thereby leading to a notable decrease in the usage of herbicides. The implementation of these biocontrol agents is highly beneficial, resulting in reduced reliance on herbicide applications throughout various agricultural practices.

- Chinese farmers use unmanned aerial systems (UAS) imagery analysis and computer vision techniques to enhance weed management practices. By employing this approach, they identify weed-infested rows and selectively apply herbicides accurately, leaving non-weed-infested rows untouched. This innovative method effectively minimizes the wastage of herbicides by avoiding unnecessary applications and reducing overall herbicide consumption per hectare.

- Farmers adopt genetically modified organism (GMO) crops to minimize additional investment requirements, resulting in a significant reduction in herbicide consumption per hectare.

China is the world's largest producer and exporter of glyphosate

- Weeds are a major constraint to crop production, which is crucial for food security in China. Over 500 invasive weeds are an increasing threat to agricultural production and ecosystems in China. Atrazine, paraquat, and glyphosate are commonly used herbicides in China.

- Atrazine is an herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Paraquat is the active ingredient of gramoxone, which controls weeds and grasses. It is also used for desiccating crops, like cotton, before harvest. Paraquat was valued at USD 4.6 thousand per metric ton in 2022. China is a major paraquat export country, and over 80% of its paraquat output is exported to countries worldwide.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant. It was priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the world's largest producer and exporter of glyphosate in the world. The output of glyphosate in China increased from 316,000 ton in 2010 to about 505,000 ton in 2017. In 2017, China exported over 300,000 ton of glyphosate technical, which satisfied more than half of the global glyphosate demand.

- Factors like weather conditions, weed infestation, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

China Herbicide Industry Overview

The China Herbicide Market is moderately consolidated, with the top five companies occupying 64.14%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Nutrichem Co. Ltd and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Nutrichem Co. Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms