|

市場調査レポート

商品コード

1683983

中国の殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の殺菌剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

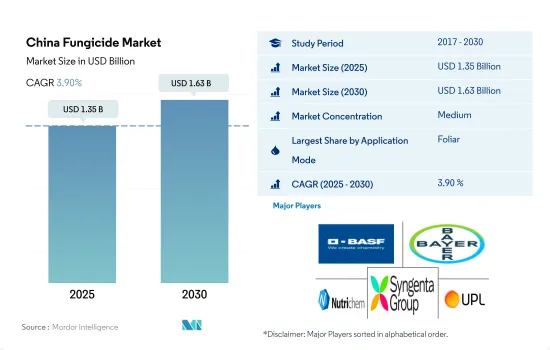

中国の殺菌剤市場規模は2025年に13億5,000万米ドルと推定・予測され、2030年には16億3,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは3.90%で成長すると予測されています。

速効性により葉面散布が中国の殺菌剤市場を独占

- 中国では殺菌剤製造産業が確立しており、複数の国内企業が殺菌剤製剤と有効成分を生産しています。中国で使用されている主な殺菌剤には、トリアゾール系、ストロビルリン系、ベンズイミダゾール系、ジチオカルバメート系、キノン外部阻害剤(QoI)などがあります。これらの殺菌剤は作用様式が異なり、特定の真菌病原菌を標的にします。中国は2022年のアジア太平洋殺菌剤市場の31.5%を占めました。

- 葉面散布が中国の殺菌剤市場を独占し、2022年には60.1%のシェアを占めました。葉面散布される殺菌剤は、真菌病原菌に対して迅速に作用することができます。通常、殺菌剤は植物体内で素早く吸収され、移行するように調合されています。これにより、殺菌剤は罹患した組織に到達し、菌類を抑制または死滅させ、病害の進行を抑え、さらなる被害を防ぐことができます。

- 種子治療は2022年の中国の殺菌剤市場の14.1%を占めました。真菌感染は植物を弱らせ、開発を阻害します。殺菌剤種子治療は、病害の被害を防止または低下させることで、植物の健康と活力を維持するのに役立ちます。これにより、植物はより多くのエネルギーを成長と開発に振り向けることができ、より健康で生産性の高い作物につながります。2017年から2022年にかけての種子処理剤の市場価値は9,190万米ドル増加しました。

- 中国からの殺菌剤の輸出も2026年までに増加すると予測されています。2021年、同国は1億1,020万kgの殺菌剤を輸出しました。2026年には、輸出量は1億2,560万kgに達すると予測されています。この要因は、予測期間中にCAGR 3.7%を記録すると予測される殺菌剤市場をさらに牽引する可能性があります。

中国の殺菌剤市場の動向

最大残留レベル規制の設定と病害防除のための他の代替手段の採用により、1ヘクタール当たりの殺菌剤消費量は大幅に減少しました。

- 過去期間中、中国では1ヘクタール当たりの殺菌剤消費量が約16%減少しました。中国政府は殺菌剤の使用を管理する規制と政策を実施しました。これには、農産物中の殺菌剤の最大残留レベルの制限設定や、安全かつ責任ある使用のためのガイドラインの策定などが含まれます。これらの規制を実施することで、中国は殺菌剤が適切な予防措置を講じた上で、慎重に使用されるようにすることを目指しています。

- 中国は総合的病害虫管理(IPM)戦略の実施を積極的に奨励しており、その戦略には予防措置、生物学的防除技術、殺菌剤などの農薬の適切な使用が含まれます。この包括的なアプローチにより、殺菌剤の使用率を下げることに成功しています。

- 中国政府はまた、伝統的な育種や遺伝子組み換え技術による耐病性作物品種の開発など、病害防除の代替方法も模索してきました。病害に対する作物の自然抵抗性を高めることに重点を置くことで、中国は殺菌剤への依存を減らしてきました。

- 中国は殺菌剤の代替として生物学的防除剤を活用してきました。これらの生物防除剤には、植物病原菌の増殖を抑制または阻害することができる細菌や真菌などの有益な微生物が含まれます。これらの生物防除剤を作物に適用すれば、殺菌剤の使用量を減らすことができます。

- 農家は、輪作や土壌管理などの技術を採用し、病害を効果的に予防・管理しています。これらの技術により、中国では1ヘクタール当たりの殺菌剤の消費量が減少しました。

マンコゼブ、プロピネブ、ジラムは中国で最もよく使用される殺菌剤成分です。

- マンコゼブ、プロピネブ、ジラムは中国で最も一般的に使用されている殺菌剤成分です。2021年、中国の殺菌剤輸出量は110,250,000kgで、ドイツ、フランス、中国に次いで4位でした。1997年以降、輸出は平均して前年比2.2%増となっています。2026年には1億2,564万kgに達すると予測されています。

- Mancozebは広スペクトルの接触殺菌剤で、ナタネ、レタス、小麦、リンゴ、トマト、テーブル・グレープ、ワイン・グレープ、球根タマネギ、ニンジン、パースニップ、エシャロット、デュラム小麦の炭疽病、ピシウム病、葉斑病、うどんこ病、ボトリティス病、さび病、かさぶた病など、多くの真菌病害の防除に使用されます。2022年の価格はトン当たり7,700米ドル。

- プロピネブはジチオカルバミン酸塩系接触殺菌剤で、2022年の価格はトン当たり3,500米ドルです。プロピネブはトマト、白菜、キュウリ、マンゴー、花卉などの作物に適用されます。マンゴーの早期晩枯病、ハクサイの炭そ病、ジャガイモのべと病、キュウリのべと病、トマトの晩枯病の予防と治療に使用されます。

- ジラムはカルバマート系の農業用殺菌剤です。植物の葉面散布が可能だが、土壌や種子の処理にも用いられます。ポームフルーツ、ストーンフルーツ、ナッツ、つる性植物、野菜、観葉植物に使用でき、特にリンゴとナシのかさぶた、その他の果樹作物のアルテルナリア、セプトリア、モモ葉巻、ショットホール、さび病、黒腐病、炭疽病の防除に用いられます。Ziramの2022年の価格はトン当たり3,300米ドルでした。

- 有効成分価格は、国内の天候、病害の発生、エネルギー価格、人件費などの要因に大きく影響されます。

中国の殺菌剤産業の概要

中国の殺菌剤市場は適度に統合されており、上位5社で63.77%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Nutrichem, Syngenta Group and UPL Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nutrichem Co. Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001685

The China Fungicide Market size is estimated at 1.35 billion USD in 2025, and is expected to reach 1.63 billion USD by 2030, growing at a CAGR of 3.90% during the forecast period (2025-2030).

Foliar application dominated the Chinese fungicide market owing to its quick action

- China has a well-established fungicide manufacturing industry, with several domestic companies producing fungicide formulations and active ingredients. Major fungicide classes used in China include triazoles, strobilurins, benzimidazoles, dithiocarbamates, and quinone outside inhibitors (QoIs). These fungicides have different modes of action and target specific fungal pathogens. China accounted for 31.5% of the Asia-Pacific fungicide market in 2022.

- Foliar application dominated the Chinese fungicide market and accounted for a share of 60.1% in 2022. Fungicides applied in foliar can provide rapid action against fungal pathogens. They are typically formulated to have quick absorption and translocation properties within the plant. This allows the fungicide to reach the affected tissues and inhibit or kill the fungi, reducing disease progression and preventing further damage.

- Seed treatment accounted for 14.1% of the Chinese fungicide market in 2022. Fungal infections can weaken and stunt the development of plants. Fungicide seed treatments can help plants maintain their health and vigor by preventing or lowering disease damage. This allows the plants to allocate more energy toward growth and development, leading to healthier and more productive crops. The market value of seed treatment between 2017 and 2022 increased by USD 91.9 million.

- Exports of fungicides from China are also projected to increase by 2026. In 2021, the country exported 110.2 million kg of fungicides. By 2026, exports are projected to reach 125.6 million kg. This factor may further drive the fungicide market, which is anticipated to register a CAGR of 3.7% during the forecast period.

China Fungicide Market Trends

Setting regulations for controlling maximum residue levels and adopting other alternatives for disease control significantly reduced per-hectare fungicide consumption

- During the historical period, China witnessed a notable decrease of approximately 16% in the consumption of fungicides per hectare, attributed to several reasons. The Chinese government has implemented regulations and policies to control the use of fungicides. These include setting limits on the maximum residue levels of fungicides in agricultural products and establishing guidelines for their safe and responsible use. By enforcing these regulations, China aims to ensure that fungicides are used judiciously and with proper precautions.

- China has actively encouraged the implementation of integrated pest management (IPM) strategies, which encompass preventive measures, biological control techniques, and judicious application of pesticides, such as fungicides. This comprehensive approach has successfully led to a decrease in the rate of fungicide usage.

- The Chinese government has also explored alternative methods of disease control, including the development of disease-resistant crop varieties through traditional breeding or genetic modification techniques. By focusing on enhancing the natural resistance of crops to diseases, China has reduced the reliance on fungicides.

- China has been utilizing biological control agents as an alternative to fungicides. These agents include beneficial microorganisms, such as bacteria and fungi, which can suppress or inhibit the growth of plant pathogens. Applying these biocontrol agents to crops could lead to a reduction in the rate of fungicide usage.

- The farmers adopted techniques, such as crop rotation and soil management, to prevent and manage diseases effectively. These techniques reduced the consumption of fungicide per hectare in China.

Mancozeb, propineb, and ziram are the most commonly used fungicide ingredients in China

- Mancozeb, propineb, and ziram are the most commonly used fungicide ingredients in China. In 2021, the country exported 110,250,000 kg of fungicides and was fourth behind Germany, France, and China. On average, exports have grown by 2.2% Y-o-Y since 1997. Exports are projected to reach 125,640,000 kg by 2026.

- Mancozeb is a broad-spectrum contact fungicide that is used to control a number of fungal diseases, such as anthracnose, pythium blight, leaf spot, downy mildew, botrytis, rust, and scab, in oilseed rape, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrots, parsnip, shallots, and durum wheat. It was priced at USD 7.7 thousand per metric ton in 2022.

- Propineb is a dithiocarbamate contact fungicide, priced at USD 3.5 thousand per metric ton in 2022. Propineb is applicable to tomato, Chinese cabbage, cucumber, mango, flowers, and other crops. It is used in preventing and treating early late blight of mango, anthracnose of Chinese cabbage, potato downy mildews, cucumber downy mildew, and tomato late blight.

- Ziram is a carbamate, agricultural fungicide. It can be applied to the foliage of plants, but it is also used for soil and/or seed treatment. It can be used in pome fruit, stone fruit, nuts, vines, vegetables, and ornamentals, particularly to control scabs in apples and pears, as well as Alternaria, Septoria, peach leaf curl, shot-hole, rusts, black rot, and anthracnose in other fruit crops. Ziram was priced at USD 3.3 thousand per metric ton in 2022.

- The active ingredient prices are majorly influenced by factors like weather conditions, disease outbreaks, energy prices, and labor costs in the country.

China Fungicide Industry Overview

The China Fungicide Market is moderately consolidated, with the top five companies occupying 63.77%. The major players in this market are BASF SE, Bayer AG, Nutrichem Co. Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Nutrichem Co. Ltd

- 6.4.7 Rainbow Agro

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms