|

市場調査レポート

商品コード

1683977

アフリカの除草剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Africa Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの除草剤:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 174 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

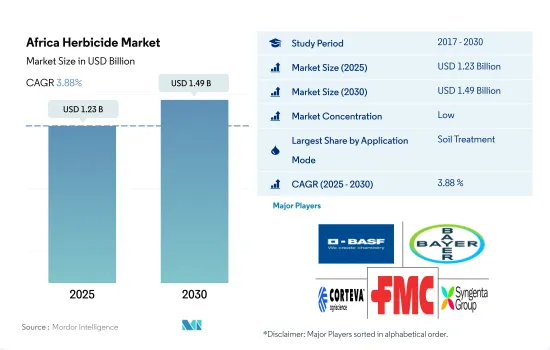

アフリカの除草剤市場規模は2025年に12億3,000万米ドルと推定・予測され、2030年には14億9,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは3.88%で成長すると予測されています。

さまざまな適用モードの採用は、作物の成長段階と雑草の種類に大きく左右される

- アフリカの農業部門はさまざまな課題に直面しており、なかでも雑草が大きな脅威となっています。この地域の集約的な農法、不耕起、主要作物の単一栽培は、様々な雑草種の繁殖を助け、作物の成長を妨げています。様々な社会経済的要因により、農家はより良い雑草管理と作物の生育を促進するために、様々な散布方法で除草剤散布を実施しています。

- 除草剤の土壌治療施用モードは、雑草の生育初期段階で防除するための予防措置として農家で主に採用されており、除草剤のさらなる使用量と生産コストを削減します。この適用モードの市場価値は、予測期間中に1億5,310万米ドル増加すると予想されます。

- 葉面除草剤散布は、次に多く採用されている散布モードであり、様々な作物の広葉雑草を防除するための一般的な伝統的慣行です。葉面散布法の使用は予測期間中に成長し、1億40万米ドルの市場成長を占めると予想されます。

- 水不足の増加とマイクロ灌漑システムの進歩は、より良い雑草管理のために化学除草剤を均一に散布するケミゲーション・モードの台頭に役立っています。化学灌漑モードの市場は、2023年~2029年に5,440万米ドル成長します。

- 除草剤燻蒸の採用は、噴霧ドリフトや人体への害の可能性など、関連するリスクのために制限されています。その一方で、土壌などに浸透して雑草を効果的に防除できることがわかっています。

- 同地域の除草剤市場は、雑草蔓延の増加を背景に、予測期間中に3億1,230万米ドルの成長が見込まれています。

伝統的な除草方法に伴うリスクが、この地域での除草剤ニーズを高めています。

- アフリカの農業部門は、南アフリカ、エチオピア、ナイジェリア、エジプト、ケニアなどの国に集中しています。農業は最も重要な部門のひとつであり、人口の大半が農業に従事しています。この部門は、サハラ以南のアフリカのGDPに約14%貢献しています。様々な生物・生物学的課題の中で、雑草は農業部門にとって大きな脅威となっています。伝統的な雑草管理方法は、時間がかかり、コストが高くなり、労働力が必要になるため、農家は雑草防除の主要な方法として除草剤を採用するようになりました。

- 歴史的な期間に除草剤の消費量は大きく伸びた。2017年には16万2,000トンで、2022年には19万8,100トンに増加しました。消費の伸びは、雑草蔓延の増加と除草剤採用の増加が主な原因です。アフリカでは毎年平均して、雑草によって最大25%の収量損失が発生しています。収量損失の増加は、2023年から2029年にかけて9,611トンもの除草剤消費量増加をさらに促進します。

- 穀物・穀類作物生産者は、栽培に化学除草剤を主に利用しており、2022年には45.1%を占めました。これらの作物が優勢なのは、主に栽培面積が多く、単作農業が様々な雑草種の生育に有利なためです。雑草は、この地域の穀類作物に最大34%の潜在的収量損失をもたらします。そのため、これらの作物では除草剤の使用率が高くなっています。

- この地域の除草剤市場は、予測期間中にCAGR 4.1%を記録すると予測されており、雑草管理の他の方法に関連する問題を解決することになります。

アフリカの除草剤市場動向

同地域における食糧需要の増加と作物の高生産性ニーズが除草剤市場を牽引する

- 近年、アフリカでは除草剤の使用が顕著に急増しています。農業慣行や雑草管理における除草剤需要の高まりを反映して、除草剤の消費量が大幅に増加しています。2017年から2022年にかけて、アフリカにおける1ヘクタール当たりの除草剤消費量は89.3%という大幅な伸びを示しました。この急増は、除草剤の利点に関する農民の意識の高まりと、単位土地当たりの農業生産性を高めたいという農民の願望によるものと考えられます。市場に多様な除草剤が広く出回っていることが、除草剤使用量の増加を促進する上で重要な役割を果たしています。

- 適切なローテーションや多様化なしに、単一の除草剤または限られた除草剤セットを継続的かつ広範囲に使用すると、抵抗性雑草の個体群が選択される可能性があります。時間の経過とともに、これらの抵抗性雑草が景観を支配するようになり、除草剤の防除効果が低下します。異なる作用機序の除草剤をローテーション使用することで、抵抗性雑草の優占を防ぐことができます。一般にパーマー・アマランサスとして知られるアマランサス・パルメリ(Amaranthus palmeri)に最も広く見られるグリホサート耐性メカニズムは、2022年に南アフリカ共和国で確認されました。グリホサートは様々な作物の雑草管理に頻繁に使用される農薬です。しかし、グリホサート耐性雑草の増加は、雑草防除を成功させる上で大きな障害となっています。

- アフリカでは食糧需要が増加しているため、農業生産性の向上が強く求められています。除草剤は、農作物の損失を減らすことで農業収量の増加に大きく貢献します。人口の食糧需要を満たす必要性から、除草剤への依存が高まっています。

除草剤製品への依存度の高さと、除草剤の輸入関税に関する規制の変化が、この地域における有効成分価格の変動につながっています。

- アフリカの農業セクターでは、雑草が大きな脅威となっており、穀物や主食作物で最大34%の収量損失をもたらしています。この問題に対処するため、農家は効果的な雑草防除のために化学除草剤に大きく依存しています。手作業による除草や機械除草のような代替方法は、労働力不足や賃金の上昇によりコスト高になっているためです。

- メトリブジンは、トウモロコシ、ニンジン、トマト、ビートルート、アスパラガス、カブ、大豆、アブラナ科植物、ウリ科植物、タマネギ、エンドウ豆、豆類、小麦、レタス、タバコ、イチゴなどの作物で、さまざまな一年生広葉樹や草を防除する除草剤です。メトリブジンの価格は2022年に1トン当たり16,580.9米ドルと記録され、2017年より31.3%上昇しました。この価格上昇は、需要の高まりと、アフリカ以外の国から輸入されるため入手できないことが主な原因です。南アフリカは主要輸入国で、インドからメトリブジンを輸入しています。

- アトラジンは、南アフリカやナイジェリアなどのトウモロコシ生産国で主に使用されている除草剤で、トウモロコシ栽培面積の約88%が雑草防除のためにアトラジンに依存しています。アトラジンの用途は、陸上の食用作物、非食用作物、森林、住宅の芝生、ゴルフ場、レクリエーションエリア、放牧地など多岐にわたり、農場で広く採用されている雑草防除手段となっています。さまざまな作物で使用されているため、アトラジンの価格は年々上昇しています。2022年には、2017年に記録された価格と比較してメートルトン当たり3,292.7米ドルの成長を経験しました。

- グリホサートは、主にその費用対効果の高さから、この地域で2番目に普及している除草剤として広く採用されています。2022年現在、グリホサートの有効成分価格は1トン当たり1,143.2米ドルを記録しています。

アフリカの除草剤産業概要

アフリカ除草剤市場は細分化されており、上位5社で27.04%を占めています。この市場の主要企業は以下の通り。 BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 南アフリカ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- 南アフリカ

- その他のアフリカ

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001679

The Africa Herbicide Market size is estimated at 1.23 billion USD in 2025, and is expected to reach 1.49 billion USD by 2030, growing at a CAGR of 3.88% during the forecast period (2025-2030).

Adoption of various application modes majorly depends upon the crop growth stage and weed type

- Africa's agricultural sector is facing various challenges, among which weeds are becoming a major threat to the sector. The region's intensive agricultural practices, no-tillage, and monoculture practices in major crops help various weed species to grow and hamper crop growth. Due to various socio-economic factors, farmers implement herbicide application through different application modes for better weed management and enhanced crop growth.

- The herbicide soil treatment application mode is majorly adopted by farmers as a precaution to control weeds in their early growth stages, which reduces further herbicide use and production costs. The market value for this application mode is expected to increase by USD 153.1 million during the forecast period.

- Foliar herbicide application is the next most adopted application mode and common traditional practice for controlling broadleaf weeds in various crops, which is effective in rapid action by targeting the weed species. The use of the foliar method is expected to grow during the forecast period, accounting for a market value growth of USD 100.4 million.

- Increasing water shortages and advancements in micro-irrigation systems help in the rise of the chemigation mode, which provides the uniform distribution of chemical herbicide applications for better weed management. The market for the chemigation mode will grow by USD 54.4 million during 2023-2029.

- The adoption of herbicide fumigation is limited due to its associated risks, such as spray drift and potential harm to human health. On the other hand, it has been found to effectively control weeds by penetrating the soil and other areas.

- The herbicide market in the region is expected to grow by USD 312.3 million during the forecast period, driven by the increasing weed infestations.

The risk associated with the traditional weeding methods is increasing the need for herbicides in the region

- The African agricultural sector is majorly concentrated in countries like South Africa, Ethiopia, Nigeria, Egypt, and Kenya. Agriculture is one of the most important sectors, and the majority of the population works in it. The sector contributes around 14% to Sub-Saharan Africa's GDP. Among various biotic and abiotic challenges, weeds are becoming a major threat to the agricultural sector. Traditional weed management practices are associated with being time-consuming, becoming more expensive, and needing more labor, and these factors divert farmers to adopt herbicides as a primary method for weed control.

- There was a significant growth in herbicide consumption during the historical period. In 2017, it was 162.0 thousand metric ton, which increased to 198.1 thousand metric ton in 2022. The consumption growth is majorly attributed to the increasing weed infestations and rise in herbicide adoption. On average, every year, weeds are causing yield loss of up to 25% in Africa. The increasing yield losses further drive the herbicide consumption growth by 9,611 metric ton during 2023-2029.

- Grain and cereal crop growers are majorly utilizing chemical herbicides in their cultivation, which accounted for 45.1% in 2022. The dominance of these crops is mainly due to their higher cultivation area and monoculture agriculture practices favoring various weed species to grow. Weeds cause a potential yield loss of up to 34% to cereals crops in the region. This resulted in higher utilization of herbicides in these crops.

- The herbicide market in the region is projected to register a CAGR of 4.1% during the forecast period, which will solve the problems associated with other methods of weed management.

Africa Herbicide Market Trends

Rising food demand in the region coupled with need for high productivity of the crops will drive the herbicide market

- In recent years, the use of herbicides in Africa has experienced a notable surge. There has been a substantial increase in the consumption of herbicides, reflecting a growing demand for these products in agricultural practices and weed management. From 2017 to 2022, herbicide consumption per hectare in Africa witnessed a significant growth of 89.3%. This upsurge can be attributed to the increased awareness among farmers regarding the advantages of herbicides and their desire to enhance agricultural productivity per unit of land. The wide availability of diverse herbicides in the market has played a significant role in driving the upswing in herbicide usage.

- Continuous and extensive use of a single herbicide or a limited set of herbicides without proper rotation or diversification can lead to the selection of resistant weed populations. Over time, these resistant weeds dominate the landscape, making herbicides less effective in controlling them. Rotation of herbicides with different modes of action to prevent the dominance of resistant weed populations. The most prevalent glyphosate resistance mechanism in Amaranthus palmeri, commonly known as palmer amaranth, was seen in the Republic of South Africa in 2022. Glyphosate is a frequently used pesticide for weed management in a variety of crops. However, the rise of glyphosate-resistant weed populations offers a considerable obstacle to successful weed control.

- Africa's rising food demand has led to a determined push to boost agricultural productivity. Herbicides contribute significantly to increased agricultural yields by lowering crop losses. The necessity to fulfill the population's food requirements drives the reliance on herbicides.

Heavy reliance on herbicide products and changing regulations on import tariffs on herbicides are leading to fluctuating active ingredient prices in the region

- In the African agriculture sector, weeds have emerged as a substantial threat, leading to yield losses of up to 34% in cereals and staple food crops. To address this issue, farmers heavily rely on chemical herbicides for effective weed control, as alternative methods like hand weeding and mechanical weeding have become cost-prohibitive due to labor shortages and rising wages.

- Metribuzin is a herbicide for control of various annual broadleafs and grasses in crops like maize, carrots, tomatoes, beetroot, asparagus, turnip, soybeans, brassicas, cucurbits, onions, peas, beans, wheat, lettuce, tobacco, and strawberries. The price of metribuzin was recorded as USD 16,580.9 per metric ton in 2022, which was 31.3% more than in 2017. This price increase is majorly attributed to the rising demand and unavailability as it is imported from other non-African countries. South Africa is the major importing country, and it imports metribuzin from India.

- Atrazine is the predominant herbicide utilized in maize-producing nations such as South Africa and Nigeria, with approximately 88% of the maize area relying on atrazine for weed control. Its application extends to numerous terrestrial food crops, non-food crops, forests, residential turf, golf courses, recreational areas, and rangelands, making it a widely adopted weed control measure on farms. Due to its expanding usage across different crops, the price of atrazine has been consistently rising each year. In 2022, it experienced a growth of USD 3,292.7 per metric ton compared to the price recorded in 2017.

- Glyphosate is extensively adopted as the region's second most prevalent herbicide, mainly owing to its cost-effectiveness. As of 2022, the price of glyphosate's active ingredient was recorded at USD 1,143.2 per metric ton.

Africa Herbicide Industry Overview

The Africa Herbicide Market is fragmented, with the top five companies occupying 27.04%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 South Africa

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 South Africa

- 5.3.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms