|

市場調査レポート

商品コード

1683863

アジア太平洋地域のLFP電池パック:市場シェア分析、産業動向・統計、成長予測(2025~2029年)Asia-Pacific LFP Battery Pack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のLFP電池パック:市場シェア分析、産業動向・統計、成長予測(2025~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 274 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

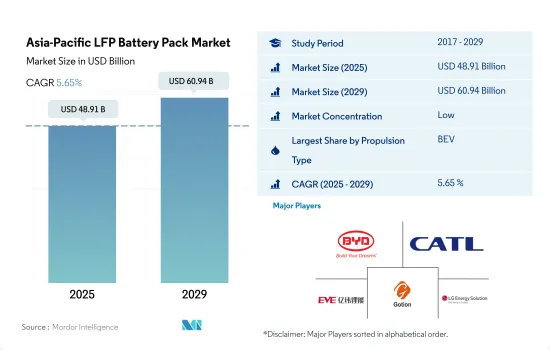

アジア太平洋地域のLFP電池パック市場規模は、2025年に489億1,000万米ドルと推定され、2029年には609億4,000万米ドルに達すると予測され、予測期間中(2025-2029年)のCAGRは5.65%で成長すると予測されます。

LFP電池の需要は、生産設備の拡張とBEVおよびPHEV市場の拡大につながる電動モビリティの増加により、アジア太平洋地域で拡大しています。

- アジア太平洋地域のいくつかの国々で電動モビリティが増加しており、近年電池需要が増加しています。アジア諸国では、ほとんどの自動車メーカーがLFP電池パックを最も一般的な種類の電池として自動車に採用しています。様々なBEVやPHEVにこれらの電池が搭載されているのは、寿命が長く、安全で、安価に生産できるといった特徴が後押ししています。これらの要因の結果、BEVとPHEV用のLFP電池タイプは、地域全体で2017年よりも2021年に成長を示しました。

- PHEVおよびBEV用LFP電池の主な市場は、中国、インド、日本などのアジア諸国です。この電池タイプは、アジア太平洋地域のBEVおよびPHEV電池消費のすべてを占めています。アジアの主要LFP電池メーカーには、CATL、BYD、Gotion High Tech、CALB、LGなどがあります。インド、日本、中国、タイなどの国々では、BEVとPHEVの需要が急速に増加しており、LFP電池のニーズが高まっています。その結果、電気自動車に使用されるLFP電池の需要は2022年には2021年よりも増加しました。

- 様々な企業がLFP電池を生産する工場を設立しており、アジア太平洋地域ではBEVやPHEVを含む様々な電気自動車となります。2022年11月、VinES Energy SolutionsとGotion High-Techはベトナムで新しいバッテリーギガファクトリーの建設を開始しました。この工場の年間生産能力は5gWHで、LFP電池を生産します。生産開始は2023年第3四半期を予定しています。その結果、BEVとPHEV向けLFP電池の需要は、予測期間中、アジア太平洋地域に属する様々な国々で拡大すると予測されます。

アジア太平洋地域諸国におけるLFPマターリーパック市場の急拡大は予測期間中も継続すると予測される

- アジア太平洋地域市場の最近の動向は、複数の国々におけるLFP電池パック市場の活発な拡大を示しています。中国がトップランナーで、2022年には2億2,986万kWhの大幅な数量となり、2023年には約2億6,254万kWhに成長すると予測されています。この成長は日本や韓国のような他の重要な市場でも同様で、2022年の販売量はそれぞれ3,179万kWhと302万kWhであり、2023年にはさらなる成長が見込まれています。注目すべきは、インドやその他アジア太平洋地域のような市場セグメンテーションです。2022年の市場規模は小さいが、有望な動向を示し、LFP電池パックの受け入れが急増しています。このような上昇基調は、グリーンモビリティを推進する政府の取り組み、バッテリー技術の進歩、自動車産業における持続可能なエネルギーソリューションの採用重視の高まりなど、いくつかの要因によるものと考えられます。

- 予測期間では、アジア太平洋地域諸国におけるLFP電池パック市場の継続的かつ堅調な成長が見込まれています。中国は首位の座を維持し、2029年には約5億4,158万kWhに達すると予測されます。日本もこれに続き、同時期に約7,654万kWhの数量達成を目指し、着実な成長を予測しています。同様に、韓国、インド、その他アジア太平洋地域も大幅な成長が見込まれており、これらの市場ではLFP電池パックが広く受け入れられ、統合されていることが強調されています。予想される成長は、バッテリー技術の研究開発の進行、インフラ能力の拡大、電動モビリティへの移行を促進する政府の政策によって促進されます。

アジア太平洋地域のLFP電池パック市場動向

トヨタ、テスラ、武陵が市場を牽引し、多様な自動車メーカーが参入

- APACの電気自動車市場は多数の競合企業で賑わっているが、その勢いは主に支配的な5つの企業が牽引しており、合計で2022年の市場シェアの50%以上を占めています。トップを走るのはBYDで、同地域のEV販売台数の20.93%を占める。BYDの強力な財務基盤は、先進的な研究開発インフラと相まって、BYDを強豪企業として位置付けています。競争力のある価格設定と広大な販売・アフターセールス網は、新規消費者に効果的にアピールしています。

- BYDに続く第2位はトヨタグループで、市場の約12.88%を占めています。BYDはアジア太平洋地域で高い評価を得ており、その広範な販売・サービス体制が消費者の信頼を得て、その地位をさらに強固なものにしています。第3位はテスラで、市場の8.27%を占めています。前衛的な技術主導の製品で有名なテスラは、中国やオーストラリアをはじめとする各国をまたぐシームレスなサプライチェーンを享受しています。

- 4位は武陵で、市場の約7.10%を占めています。親会社である柳州五菱汽車工業の下で運営されている五菱は、中国やインドネシアなどの国々でニッチを切り開き、多様なEVラインナップで多様な顧客に対応しています。トップ5の最後尾はホンダで、市場シェアは3.85%です。APACのEV市場では他に、日産、奇瑞、長安、Netaなどのブランドが競合しています。

2022年には、Wuling、Tesla、BYDがAPACにおける最大のバッテリー・パック需要メーカーとなります。

- 自動車、バス、トラックを含む電気自動車は、ここ数年、アジア各国で顕著な盛り上がりを見せています。電気自動車に対する意欲は地域や国によって異なるが、SUVが中国、インド、日本などの主要市場でニッチを築いていることは明らかです。ユーティリティの高さと広さを理由に、アジアでは従来のセダンよりもSUVを好む傾向が強まっています。

- 最近、アジアの人々の間でコンパクトSUVへの人気が急上昇しています。テスラのモデルYは、オール電化のドライブトレイン、5つ星のNCAP安全性、7人乗り、航続距離などで際立っており、特に中国をはじめとするアジア太平洋地域の主要市場で人気の高い選択肢となっています。BYDのSong DMは、競争力のある価格設定と効率的な燃費性能で、アジア全域の顧客に支持されています。

- 2022年には、テスラのModel 3がアジア地域でトップセラーの1つに輝いたが、これは純粋な電気自動車であることと、魅力的な機能性の数々が評価されたものです。ダイナミックなAPACのEV分野では、既存の世界・メーカーによる無数の電動SUVやセダンの選択肢もあります。2022年には、トヨタのYaris CrossやBYDのDolphinのような車の好調な販売が予想されます。トヨタCorollaやWulingのHongguang MINIEVといった他のメーカーも、APACのEVエコシステムにおいて強力なラインナップを形成しています。

アジア太平洋地域のLFP電池パック産業の概要

アジア太平洋地域のLFP電池パック市場は断片化されており、上位5社で7.17%を占めています。この市場の主要企業は以下の通りです。BYD Company Ltd., Contemporary Amperex Technology(CATL), EVE Energy, Gotion High-Tech and LG Energy Solution Ltd.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 電気自動車販売台数

- OEM別電気自動車販売台数

- 売れ筋EVモデル

- 選好されるバッテリーケミストリーを持つOEM

- 電池パック価格

- 電池材料コスト

- 各電池化学の価格表

- 誰が誰に供給するか

- EVバッテリーの容量と効率

- EVの発売モデル数

- 規制の枠組み

- 中国

- インド

- インドネシア

- 日本

- タイ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 車体タイプ

- バス

- LCV

- M&HDT

- 乗用車

- 推進タイプ

- BEV

- PHEV

- 容量

- 15 kWh~40 kWh

- 40 kWh~80 kWh

- 80kWh以上

- 15kWh未満

- バッテリー形状

- 円筒形

- 袋

- 角型

- 方式

- レーザー

- ワイヤー

- コンポーネント

- アノード

- カソード

- 電解液

- セパレーター

- 材料タイプ

- リチウム

- 天然黒鉛

- その他の材料

- 生産国

- 中国

- インド

- 日本

- 韓国

- タイ

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BYD Company Ltd.

- Contemporary Amperex Technology Co. Ltd.(CATL)

- EVE Energy Co. Ltd.

- Exide Industries Ltd.

- Farasis Energy(Ganzhou)Co. Ltd.

- FinDreams Battery Co. Ltd.

- Gotion High-Tech Co. Ltd.

- GS Yuasa International Ltd.

- Leapmotor(Jinhua)New Energy Vehicle Parts Technology Co., Ltd.

- LG Energy Solution Ltd.

- Panasonic Holdings Corporation

- Resonac Holdings Corporation

- SAIC Volkswagen Power Battery Co. Ltd.

- Samsung SDI Co. Ltd.

- SK Innovation Co. Ltd.

- SVOLT Energy Technology Co. Ltd.(SVOLT)

- Tesla Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific LFP Battery Pack Market size is estimated at 48.91 billion USD in 2025, and is expected to reach 60.94 billion USD by 2029, growing at a CAGR of 5.65% during the forecast period (2025-2029).

The demand for LFP batteries is growing in the APAC region due to rising electric mobility leading to expansion of production facilities and increase in BEV and PHEV markets

- Rising electric mobility across several countries, falling under Asia-Pacific, has increased the demand for batteries in recent years. In Asian countries, most auto manufacturers employ LFP battery packs as one of the most popular types of batteries in their automobiles. The installation of these batteries in various BEVs and PHEVs is encouraged by features like their extended lifespans, safety, and affordable production. As a result of these factors, LFP battery type for BEV and PHEV witnessed a growth in 2021 over 2017 across the region.

- The main LFP batteries for PHEV and BEV markets are in Asian nations like China, India, and Japan. This battery type accounted for all BEV and PHEV battery consumption in the APAC region. Some of the major Asian manufacturers of LFP batteries include CATL, BYD, Gotion High Tech Co. Ltd, CALB, and LG. In various countries like India, Japan, China, and Thailand, the demand for BEV and PHEV is rising rapidly, increasing the need for LFP batteries. As a result, the demand for LFP batteries used in electric vehicles increased in 2022 over 2021.

- Various companies are setting up factories to produce LFP batteries, which will be various electric vehicles in the APAC region, including BEVs and PHEVs. In November 2022, VinES Energy Solutions and Gotion High-Tech started the construction of the new battery gigafactory in Vietnam. The plant will have an annual capacity of 5gWH and produce LFP batteries. Production is expected to start by the third quarter of 2023. As a result, the demand for LFP batteries for BEV and PHEV is projected to grow in various countries, falling under the APAC region during the forecast period.

Rapid expansion of the LFP mattery pack market in Asia-Pacific countries is projected to witness a continuous growth in the forecast period

- The recent trends in the Asia-Pacific market indicate a vigorous expansion in the LFP battery pack market across several countries. China was the frontrunner, with a substantial volume of 229.86 million kWh in 2022, projected to grow to approximately 262.54 million kWh in 2023. This growth was mirrored in other significant markets like Japan and South Korea, which showcased volumes of 31.79 million kWh and 3.02 million kWh, respectively, in 2022, with expectations of further growth in 2023. Notably, markets like India and the Rest of Asia-Pacific segment, although started from a smaller base, showed promising trends with increasing volumes in 2022 and registered a burgeoning acceptance of LFP battery packs. This upward trajectory can be attributed to several factors, including governmental initiatives promoting green mobility, advancements in battery technology, and a growing emphasis on adopting sustainable energy solutions in the automotive industry.

- The forecast period anticipates continuous and robust growth in the LFP battery pack market in the Asia-Pacific countries. China is projected to maintain its leadership position, with volumes expected to reach around 541.58 million kWh by 2029. Japan, following suit, predicts steady growth, aiming to achieve a volume of approximately 76.54 million kWh in the same period. Similarly, South Korea, India, and the Rest of Asia-Pacific segment are forecast to witness substantial growth, emphasizing the broadening acceptance and integration of LFP battery packs in these markets. The anticipated growth is fostered by ongoing research and development in battery technology, expanding infrastructural capabilities, and governmental policies promoting the transition toward electric mobility.

Asia-Pacific LFP Battery Pack Market Trends

A VARIETY OF AUTOMAKERS ARE PRESENT IN THE MARKET, MAJORLY DRIVEN BY TOYOTA, TESLA, AND WULING

- The APAC electric vehicle market is bustling with numerous competitors, but its momentum is chiefly steered by five dominant corporations, collectively grasping over 50% of the 2022 market share. Leading the charge is BYD, securing a remarkable 20.93% of EV sales in the region. Its potent financial standing, coupled with its advanced R&D infrastructure, has positioned BYD as a powerhouse. The company's competitive pricing, coupled with its vast sales and after-sales network, effectively appeals to new consumers.

- Following BYD, the Toyota Group clinches the second spot, with about 12.88% of the market. Its well-established reputation across the APAC region, bolstered by its extensive sales and service framework, instills trust among consumers, further cementing its footprint. Tesla claims the third position, seizing 8.27% of the market. Renowned for its avant-garde, tech-driven offerings, Tesla enjoys a seamless supply chain across nations, notably China and Australia.

- Wuling comes in fourth, holding approximately 7.10% of the market. Operating under its parent company, Liuzhou Wuling Automobile Industry Co. Ltd, Wuling has carved a niche in countries like China and Indonesia, catering to a diverse clientele with its varied EV lineup. Rounding out the top five is Honda, with a 3.85% market share. Other notable contenders in the APAC EV market encompass brands like Nissan, Chery, Changan, and Neta, among others.

IN 2022, WULING, TESLA, AND BYD WERE THE BIGGEST BATTERY PACK DEMAND GENERATORS IN APAC

- The electric vehicle landscape, encompassing cars, buses, and trucks, has witnessed a notable upswing across various Asian countries in the past few years. While the appetite for electric vehicles fluctuates across regions and nations, it is evident that SUVs have carved a niche in major markets like China, India, and Japan. As a direct reflection of Asia's growing preference for SUVs over traditional sedans, due to their enhanced utility and spaciousness, electric SUVs have seen a parallel surge across the Asia-Pacific belt.

- Recent times have spotlighted a burgeoning affinity for compact SUVs among the Asian populace. Tesla's Model Y stands out with its all-electric drivetrain, sterling 5-star NCAP safety rating, seven-seat capacity, commendable range, and other features, making it a sought-after option in pivotal APAC markets, notably China. BYD's Song DM, with its competitive pricing and efficient fuel dynamics, has resonated well with customers across several Asian territories.

- The year 2022 saw Tesla's Model 3 clinching accolades as one of the top sellers in the Asian domain, a testament to its purely electric mechanism, paired with an array of attractive functionalities. The dynamic APAC EV arena also presents a myriad of electric SUV and sedan alternatives from established global manufacturers. The year 2022 anticipated robust sales for vehicles like Toyota's Yaris Cross and BYD's Dolphin. Other players, such as the Toyota Corolla and Wuling's Hongguang MINIEV, also form a robust lineup in the APAC EV ecosystem.

Asia-Pacific LFP Battery Pack Industry Overview

The Asia-Pacific LFP Battery Pack Market is fragmented, with the top five companies occupying 7.17%. The major players in this market are BYD Company Ltd., Contemporary Amperex Technology Co. Ltd. (CATL), EVE Energy Co. Ltd., Gotion High-Tech Co. Ltd. and LG Energy Solution Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Electric Vehicle Sales

- 4.2 Electric Vehicle Sales By OEMs

- 4.3 Best-selling EV Models

- 4.4 OEMs With Preferable Battery Chemistry

- 4.5 Battery Pack Price

- 4.6 Battery Material Cost

- 4.7 Price Chart Of Different Battery Chemistry

- 4.8 Who Supply Whom

- 4.9 EV Battery Capacity And Efficiency

- 4.10 Number Of EV Models Launched

- 4.11 Regulatory Framework

- 4.11.1 China

- 4.11.2 India

- 4.11.3 Indonesia

- 4.11.4 Japan

- 4.11.5 Thailand

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Body Type

- 5.1.1 Bus

- 5.1.2 LCV

- 5.1.3 M&HDT

- 5.1.4 Passenger Car

- 5.2 Propulsion Type

- 5.2.1 BEV

- 5.2.2 PHEV

- 5.3 Capacity

- 5.3.1 15 kWh to 40 kWh

- 5.3.2 40 kWh to 80 kWh

- 5.3.3 Above 80 kWh

- 5.3.4 Less than 15 kWh

- 5.4 Battery Form

- 5.4.1 Cylindrical

- 5.4.2 Pouch

- 5.4.3 Prismatic

- 5.5 Method

- 5.5.1 Laser

- 5.5.2 Wire

- 5.6 Component

- 5.6.1 Anode

- 5.6.2 Cathode

- 5.6.3 Electrolyte

- 5.6.4 Separator

- 5.7 Material Type

- 5.7.1 Lithium

- 5.7.2 Natural Graphite

- 5.7.3 Other Materials

- 5.8 Country

- 5.8.1 China

- 5.8.2 India

- 5.8.3 Japan

- 5.8.4 South Korea

- 5.8.5 Thailand

- 5.8.6 Rest-of-Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BYD Company Ltd.

- 6.4.2 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.4.3 EVE Energy Co. Ltd.

- 6.4.4 Exide Industries Ltd.

- 6.4.5 Farasis Energy (Ganzhou) Co. Ltd.

- 6.4.6 FinDreams Battery Co. Ltd.

- 6.4.7 Gotion High-Tech Co. Ltd.

- 6.4.8 GS Yuasa International Ltd.

- 6.4.9 Leapmotor (Jinhua) New Energy Vehicle Parts Technology Co., Ltd.

- 6.4.10 LG Energy Solution Ltd.

- 6.4.11 Panasonic Holdings Corporation

- 6.4.12 Resonac Holdings Corporation

- 6.4.13 SAIC Volkswagen Power Battery Co. Ltd.

- 6.4.14 Samsung SDI Co. Ltd.

- 6.4.15 SK Innovation Co. Ltd.

- 6.4.16 SVOLT Energy Technology Co. Ltd. (SVOLT)

- 6.4.17 Tesla Inc.

7 KEY STRATEGIC QUESTIONS FOR EV BATTERY PACK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms