欧州の非乳製品チーズ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Non-dairy Cheese - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683844

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

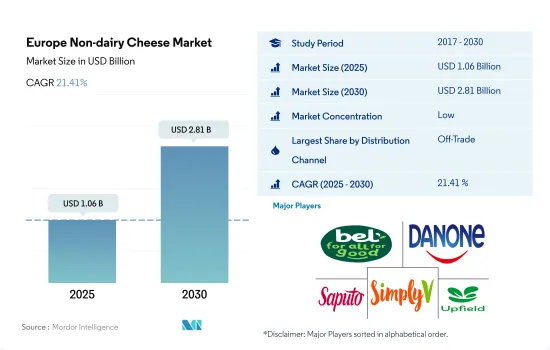

欧州の非乳製品チーズ市場規模は2025年に10億6,000万米ドルと推定され、2030年には28億1,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは21.41%で成長する見込みです。

大手小売業者がeコマース・プラットフォームを採用し、より大きな市場を獲得しようとしています。

- 欧州の非乳製品チーズ市場の流通チャネルは、非商業部門が支配的です。オフトレードセグメントでは、オンライン小売チャネルのサブセグメントが最も急成長しており、予測期間のCAGRは27.3%を記録すると予測されています。eコマースの成長により、企業はより大きなターゲット市場にアクセスし、顧客のニーズに効果的に応える機会を得ています。多くの人々が、多忙なスケジュールや2020年の全国的な封鎖のために、非乳製品チーズのような乳製品代替品をオンラインで注文し始めました。乳製品代替品の主なeコマース・チャネルは、消費者直販、クリック・アンド・コレクト、小売食料品配送、コンシェルジュ・サービスの4つです。

- 世界全体では、オントレードチャネルを通じた非乳製品チーズの販売額は、アウトブレイクにより外食産業が閉鎖されたため、2020年には2019年に比べ3.51%減少しました。2020年のドイツのレストラン数は65,090店で、2019年から8.49%減少しました。流通チャネルに基づくと、2022年の非乳製品チーズの消費量は全体で1人当たり約0.03kgでした。ヴィーガンレストランの急速な設立とメニューへのヴィーガンオプションの導入が、予測期間中の非乳製品チーズ市場を促進すると思われます。

- 非売品部門では、スーパーマーケットとハイパーマーケットが金額ベースで58.3%の主要シェアを占めています。これらの小売チャネルは、提供されるブランドの品揃えの豊富さ、棚面積の広さ、頻繁な価格プロモーションにより、強い地位を占めています。スーパーマーケットやオンライン小売店で広く入手可能な非乳製品チーズを含め、乳製品代替製品に対する需要が高まっています。世界の主要小売業者が採用するオムニチャネル・アプローチが、非乳製品チーズ市場を牽引しています。

スペイン、ドイツ、英国ではフレキシタリアンやベジタリアンの人口が増加しており、今後の市場需要を牽引すると推定されます。

- 非乳製品チーズの一人当たり消費量は、2023年の0.83kgから103.56%増加し、2029年には年間1.69kgに達すると推定されます。ドイツと英国では、ベジタリアンやフレキシタリアンが従来のチーズを植物性チーズ製品に置き換える可能性が高いため、非乳製品チーズの普及が著しいです。植物性チーズに関しては、英国の消費者の38%が2020年にスーパーマーケットで植物性スライスチーズを探していました。

- トルコとスペインは、欧州で最も急成長している市場です。スペインでは、非乳製品チーズの消費が伸び、予測期間中にCAGR 19.69%を記録し、2029年末には販売量2,603.467トンに達すると予測されます。これらの国々でフレキシタリアンやベジタリアンの人口が増加していることが、将来の市場需要を牽引すると推定されます。2020年には、スペインでは消費者の30%がフレキシタリアンであり、6%がビーガンおよびベジタリアンです。

- 植物性栄養に対する消費者の高い意識と良好なマクロ経済環境が、欧州の非乳製品チーズ産業を形成する主な要因です。EUの2022年推進政策では、赤身肉や加工肉を発ガンリスクとして烙印を押した後、より植物ベースの食事へのシフトが奨励されます。これは外食産業全体にチャンスをもたらすと思われます。ドイツでは、ピザハットがヴィオライフの植物性チーズをトッピングした3種類の常設ヴィーガン・ピザを提供しています。ドミノ、マクドナルド、グレッグス、サブウェイといった他のファーストフードチェーンも、ヴィーガン料理に非乳製品チーズを使用しています。ドイツにおける非乳製品チーズの販売額は成長し、市場推計・予測期間中にCAGR 20.01%を記録し、2029年には6億1,387万米ドルの市場規模に達すると推定されます。

欧州の非乳製品チーズ市場動向

この分野で起きている技術革新は、低脂肪と相まって欧州市場の消費率に大きな影響を与えています。

- 植物性チーズの消費は、欧州全域で植物性食品の消費が伸びているため、欧州で増加傾向にあります。欧州における植物性食品の消費は、2019年から2020年にかけて49%という驚異的な伸びを示しました。一人当たりの非乳製品チーズ消費量は2020年から2022年にかけて38%増加し、欧州では植物性ミルクに次いで消費量の多い乳製品代替品カテゴリーとなりました。

- この分野におけるいくつかのイノベーションが消費率に影響を与えています。多くの欧州諸国で人気のある非乳製品スライスチーズのように、いくつかの非乳製品チーズが市場に登場しています。スペインとドイツの消費者は、伝統的なチーズよりも植物性チーズを選ぶことを最も望んでいます。ドイツの消費者は、植物性クリームチーズ(32%)、スライスチーズ(32%)、植物性モッツァレラチーズ(31%)を好んで消費しており、これらはこの地域のスーパーマーケットで簡単に入手できます。ドイツでは、植物性チーズの代用品は90種類以上、ラベルは40種類あり、欧州最大の市場となっています。

- 欧州の人々は最近、カマンベール、フェタ、モッツァレラのような、カシューナッツ、マカダミアナッツ、アーモンドなどのナッツのみを原料とする発酵代替チーズの消費に傾倒しているが、大豆、種子、米など、他のベースも見つけることができます。シンプリーV社(ドイツ)、シース社(英国)、ビーガン・デリ社(モナコ)のような企業も、ゴーダチーズやチェダーチーズの「シンプルな」類似チーズやシュレッドチーズ(ピザ用チーズ)の製造に携わっています。植物性チーズの技術革新に対する需要の増加に伴い、欧州では2023年から2025年にかけて消費量が33.0%増加すると予測されています。

欧州の非乳製品チーズ産業の概要

欧州の非乳製品チーズ市場は断片化されており、上位5社で39.84%を占めています。この市場の主要企業は以下の通りです。Bel Group, Danone SA, Saputo Inc., Simply V and Upfield Holdings BV(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 一人当たり消費量

- 原材料/商品生産

- 代替乳製品-原材料生産

- 規制の枠組み

- フランス

- ドイツ

- イタリア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 流通チャネル

- オフトレード

- サブ流通チャネル別

- コンビニエンスストア

- オンライン小売

- 専門店

- スーパーマーケットとハイパーマーケット

- その他(倉庫クラブ、ガソリンスタンドなど)

- オントレード

- オフトレード

- 国名

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- スペイン

- トルコ

- 英国

- その他欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)。

- Bel Group

- Danone SA

- First Grade International Limited

- Granarolo SpA

- Otsuka Holdings Co. Ltd

- Saputo Inc.

- Simply V

- Tofutti Brands Inc.

- Upfield Holdings BV

- VBites Foods Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50000742

The Europe Non-dairy Cheese Market size is estimated at 1.06 billion USD in 2025, and is expected to reach 2.81 billion USD by 2030, growing at a CAGR of 21.41% during the forecast period (2025-2030).

Major retailers are adopting e-commerce platforms to captivate a larger market

- The off-trade segment dominates the distribution channels of the Europe non-dairy cheese market. In the off-trade segment, the online retail channel sub-segment is the fastest-growing one and is projected to record a CAGR of 27.3% over the forecast period. The growth of e-commerce provides companies the opportunity to access a larger target market and effectively serve customer needs. Many people started ordering dairy alternatives like non-dairy cheese online due to their hectic schedules and the nationwide lockdown in 2020. The four main e-commerce channels for dairy alternatives were direct-to-consumer, click-and-collect, retail grocery delivery, and concierge services.

- Globally, the sales of non-dairy cheese through on-trade channels in terms of value declined by 3.51% in 2020 compared to 2019 as foodservice sectors were shut down due to the outbreak. In 2020, there were 65,090 restaurants in Germany, a decrease of 8.49% from 2019. Based on the distribution channel, the overall non-dairy cheese consumption was around 0.03 kg per person in 2022. The rapid establishment of vegan restaurants and the introduction of vegan options in menus are likely to propel the non-dairy cheese market during the forecast period.

- In the off-trade segment, supermarkets and hypermarkets accounted for a major share of 58.3% by value. These retail channels have a strong position due to the wide selection of brands offered, considerable shelf space, and frequent price promotions. The demand for dairy alternative products is rising, including non-dairy cheese that is widely accessible at supermarkets and online retailers. The omnichannel approach adopted by major retailers globally is driving the non-dairy cheese market.

The rise in flexitarian and vegetarian populations across Spain, Germany, and U.K. is estimated to drive future market demand.

- The per capita consumption of non-dairy cheese is estimated to reach 1.69 kg annually in 2029, up by 103.56% from 0.83 kg in 2023. Non-dairy cheese has significant penetration across Germany and the United Kingdom, as vegetarians and flexitarians in the countries are most likely to replace conventional cheese with plant-based cheese products. Regarding plant-based cheese, 38% of UK consumers were looking for plant-based sliced cheese at supermarkets in 2020.

- Turkey and Spain are identified as the fastest-growing markets in Europe. In Spain, the consumption of non-dairy cheese is anticipated to grow, registering a CAGR of 19.69% during the forecast period to reach a sales volume of 2,603.467 metric tonnes by the end of 2029. The rise in flexitarian and vegetarian populations across these countries is estimated to drive future market demand. In 2020, 30% of consumers were flexitarian in Spain, and 6% were vegan and vegetarian.

- High consumer awareness about plant-based nutrition and favorable macroeconomic environments are the key factors shaping the European non-dairy cheese industry. The EU's 2022 promotional policy will encourage a shift to more plant-based diets after branding red and processed meat as a cancer risk. This will create opportunities across the foodservice industry. In Germany, Pizza Hut offers three permanent vegan pizzas topped with Violife plant-based cheese. Other fast-food chains such as Domino's, McDonald's, Greggs, and Subway also use non-dairy cheese in their vegan dishes. The sales value of non-dairy cheese in Germany is estimated to grow, registering a CAGR of 20.01% during the forecast period and reaching a market value of USD 613.87 million by 2029.

Europe Non-dairy Cheese Market Trends

The innovations taking place within the sector, coupled with lower fat content, is largely influencing the consumption rate in the European market.

- Plant-based cheese consumption has been on the rise in Europe owing to the growing consumption of plant-based foods across the region. Consumption of plant-based foods in Europe increased by a staggering 49% between 2019 and 2020. The non-dairy cheese per capita consumption increased by 38% from 2020-2022, making it the second most consumed category of dairy alternatives after plant-based milk in Europe.

- Several innovations in the sector are influencing the consumption rate. Several non-dairy cheese varieties are emerging on the market, like non-dairy sliced cheese, which is popular across many European nations. Consumers in Spain and Germany are the most willing to choose plant-based cheese over traditional cheese. German consumers prefer to consume plant-based cream cheese (32%), sliced cheese (32%), and plant-based mozzarella (31%), which are easily available in supermarkets across the region. In Germany, there are over 90 distinct plant-based cheese substitutes and 40 different labels, making it the largest market in Europe.

- Europeans recently became inclined toward the consumption of fermented alternatives for cheeses like camembert, feta, and mozzarella, which are made exclusively from nuts like cashew, macadamia, or almond, but other bases can be found as well, including soy, seeds, and rice. Several companies like Simply V (Germany), Sheese (UK), and Vegan Deli (Monaco) are also involved in producing 'simple' cheese analogs of gouda and cheddar, as well as shredded (pizza) cheese, owing to the increased demand for various non-dairy cheese in the region. With the growing demand for plant-based cheese innovations, consumption is anticipated increase by 33.0% during 2023-2025 in Europe.

Europe Non-dairy Cheese Industry Overview

The Europe Non-dairy Cheese Market is fragmented, with the top five companies occupying 39.84%. The major players in this market are Bel Group, Danone SA, Saputo Inc., Simply V and Upfield Holdings BV (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Per Capita Consumption

- 4.2 Raw Material/commodity Production

- 4.2.1 Dairy Alternative - Raw Material Production

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Distribution Channel

- 5.1.1 Off-Trade

- 5.1.1.1 By Sub Distribution Channels

- 5.1.1.1.1 Convenience Stores

- 5.1.1.1.2 Online Retail

- 5.1.1.1.3 Specialist Retailers

- 5.1.1.1.4 Supermarkets and Hypermarkets

- 5.1.1.1.5 Others (Warehouse clubs, gas stations, etc.)

- 5.1.2 On-Trade

- 5.1.1 Off-Trade

- 5.2 Country

- 5.2.1 Belgium

- 5.2.2 France

- 5.2.3 Germany

- 5.2.4 Italy

- 5.2.5 Netherlands

- 5.2.6 Spain

- 5.2.7 Turkey

- 5.2.8 United Kingdom

- 5.2.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Bel Group

- 6.4.2 Danone SA

- 6.4.3 First Grade International Limited

- 6.4.4 Granarolo SpA

- 6.4.5 Otsuka Holdings Co. Ltd

- 6.4.6 Saputo Inc.

- 6.4.7 Simply V

- 6.4.8 Tofutti Brands Inc.

- 6.4.9 Upfield Holdings BV

- 6.4.10 VBites Foods Ltd

7 KEY STRATEGIC QUESTIONS FOR DAIRY AND DAIRY ALTERNATIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州の非乳製品チーズ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 181 Pages

- 納期

- 2~3営業日