|

市場調査レポート

商品コード

1683806

アルミニウムリサイクル- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Aluminum Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アルミニウムリサイクル- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

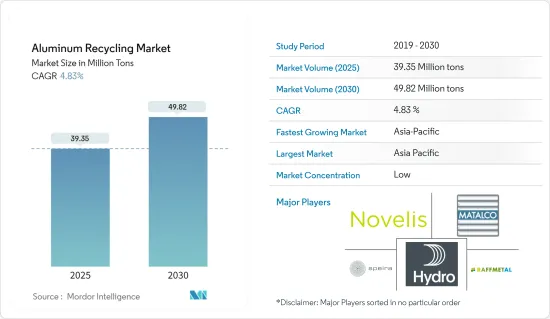

アルミニウムリサイクル市場規模は、2025年には3,935万トンと推定され、予測期間(2025~2030年)のCAGRは4.83%で、2030年には4,982万トンに達すると予測されています。

COVID-19の流行はアルミニウムリサイクル市場に大きな影響を与えました。アルミニウムの主要なシンクである建築・建設は、特に、住宅登録の停止や住宅ローンの返済の遅れを招いた住宅不動産の抑制により、大きな打撃を受けました。しかし、規制が解除されて以来、このセクターは順調に回復しています。2021~22年のアルミニウム市場は、様々なエンドユーザー産業からの消費増加により大幅に回復しました。

主なハイライト

- 短期的には、自動車および建設業界における再生アルミニウムの利用拡大が市場の需要を牽引すると予想されます。

- 逆に、鉄のような好ましくない不純物の存在が市場の成長を妨げる可能性が高いです。

- 電気自動車分野の成長とカーボンフットプリントの削減への関心の高まりは、市場に新たな成長機会をもたらすと思われます。

- アジア太平洋地域が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

アルミリサイクル市場動向

建築・建設業界からの需要の増加

- アルミニウムは、建築・建設業界で2番目に広く使用されている金属です。建築物に使用されるアルミニウムの約60%はリサイクル材料で構成されています。

- リサイクルされたアルミニウム鋳造合金、押出板、その他の製品は、浮き天井、窓、ドア、階段、壁パネル、屋根板、その他様々な用途に使用されています。

- 再生アルミニウムの使用は、エネルギー面でも大きなメリットをもたらします。使用済みアルミニウムの再溶解に必要なエネルギーは、一次金属の生産に必要なエネルギーのわずか5%です。そのため、社会の廃棄物問題の増大に貢献するのではなく、アルミニウムを再溶解し、改質して新世代の建築部品を生産することができるのです。

- アルミニウム二次製品/リサイクルアルミニウム製品は、建築物のファサード、カーテンウォール、屋根、クラッディング、日除け、ソーラーパネル、手すり、階段、棚、その他の仮設構造物に幅広く使用されています。また、高層ビル、超高層ビル、橋梁の建設にも使われています。

- オックスフォード・エコノミクスの報告書によると、世界の建設生産高は、2030年までにアジア太平洋地域で約40%、次いで北米地域で約16%、最も伸びると予想されています。

- 世界の建設活動の活発化は、最近調査された市場を牽引する重要な要因のひとつです。特にアジア太平洋、北米、中東は、建築・建設業界においてプラスの成長率を示しています。したがって、アルミニウムリサイクル市場の需要は予測期間中に増加する可能性が高いです。

- アジア太平洋では、中国が建設ブームに沸いています。世界的に見て、中国は最も重要な建築市場であり、全世界の建設投資の約20%を占めています。同国だけでも、2030年までに約13兆米ドルを建築に投じると見られています。

- 建設産業はインドで2番目に大きいです。2022年の成長率は10.7%でした。予測期間終了時には、インドの建設産業は約1兆米ドルの規模を持つ世界第3位の市場に成長する可能性があります。

- カナダ建設協会のデータによると、建設部門はカナダ最大の雇用者のひとつであり、カナダ経済の成功に大きく貢献しています。同産業は国内総生産(GDP)の7%に貢献しています。

- カナダ政府は「カナダへの投資計画」の一環として、2028年までに国内の重要なインフラ開発のために約1,400億米ドルを投資する計画を発表しました。2019年から20年にかけて、政府は国内の新規インフラ・プロジェクトに56億米ドルの投資を承認する予定です。

- サウジアラビアのビジョン2030と国家変革計画(NTP)の発表により、同国の経済成長を支援するため、教育やヘルスケアなどさまざまな分野への投資が増加しています。サウジアラビア政府は、国内の社会インフラ開発について広範な計画を持っています。同国の様々な分野への政府・民間投資は、商業ビル建設活動の増加につながる可能性が高いです。

- したがって、上記の要因により、再生アルミニウムの需要は予測期間中にプラスの影響を受けるでしょう。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、予測期間中、再生アルミニウムの最大の成長市場になると予想されます。中国、インド、日本などの国々では、エレクトロニクス、自動車、建築・建設、航空宇宙・防衛などの産業が成長しています。

- 中国は1970年代から国内でアルミニウムをリサイクルしています。また、近年はアルミニウムの二次利用にも力を入れています。この点に関して、2030年までに一次アルミニウム製錬能力を約4,500万トンに制限することを計画しています。

- 国際貿易局(ITA)のデータによると、中国は年間販売台数・生産台数ともに世界最大の自動車市場を維持しています。国内生産台数は2025年までに3,500万台近くに達すると予想されています。COVID-19の大流行を受け、中国政府は自動車消費を後押ししています。世界で新たに販売される電気自動車の半分以上(58%)を中国が占めています。国際エネルギー機関(IEA)によると、2022年には全国で590万台の新型電気自動車が販売され、2021年比で80%以上増加します。

- 国際貿易機関の報告書によると、中国は世界最大の建設市場であり、世界で最も都市化率が高いです。アメリカ建築家協会(AIA)上海のデータによると、2025年までに中国は1990年代以降、ニューヨークの10個分に相当する都市を建設するといいます。

- インド・ブランド・エクイティ財団(IBEF)によると、民間航空産業は近年、インドで最も急成長している産業のひとつとなっています。2023年(2022年4月~12月)の航空輸送量は2億3,671万人で、前年同期が1億3,161万人であったことからもわかるように、インドの航空産業は新型コロナウイルスの影響を受けると予想されています。さらに、2023年6月、インドのエア・インディア社は、エアバス社およびボーイング社と、推定700億米ドルで470機を購入する契約を締結しました。

- 日本の家電産業は世界有数の産業です。日本は、コンピューター、ゲーム機、携帯電話、その他の重要部品の生産で世界をリードしています。さらに、家電製品は日本の経済生産の約3分の1を占めています。インド、中国、韓国などの国々との厳しい競争により、日本のエレクトロニクス生産全体は減少しています。

- 日本電子情報技術産業協会(JEITA)によると、2023年1月の日本の消費者用電子機器の生産額は234億2,500万円(1億6,500万米ドル)で、前年同期比79.8%の大幅増となりました。一方、電子機器の生産額は2023年1月に2,903億900万円(20億4,200万米ドル)となり、前年同期比89.6%増となりました。

- したがって、上記の要因は、予測期間中に調査された市場の需要に影響を与える可能性が高いです。

アルミニウムリサイクル業界の概要

アルミニウムリサイクル市場は細分化されています。主なプレーヤーとしては、Novelis Inc.、Speira GmbH、Norsk Hydro ASA、Matalco Inc.、Raffmetalなどが挙げられる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設業界における再生アルミニウムの利用拡大

- 自動車産業における再生アルミニウム需要の増加

- 抑制要因

- 鉄のような好ましくない不純物の存在

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- 鋳造合金

- 押出

- シート

- その他の製品タイプ

- エンドユーザー産業

- 自動車

- 航空宇宙・防衛

- 建築・建設

- 電気・電子

- 包装

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェアランキング分析

- 主要企業の戦略

- 企業プロファイル

- Alcoa Corporation

- Amag Austria Metall AG

- Constellium

- Kuusakoski OY

- Matalco Inc.

- Norsk Hydro Asa

- Novelis

- Raffmetal Spa

- Real Alloy

- Speira Gmbh

- Stena Metall AB

- Ye Chiu Group

第7章 市場機会と今後の動向

- 電気自動車セグメントの成長

- カーボンフットプリント削減への注目の高まり

The Aluminum Recycling Market size is estimated at 39.35 million tons in 2025, and is expected to reach 49.82 million tons by 2030, at a CAGR of 4.83% during the forecast period (2025-2030).

The COVID-19 pandemic had a substantial impact on the aluminum recycling market. Building and construction, a major sink for aluminum, was badly hit, especially due to curtailment in residential real estate resulting in the suspension of home registrations and slow home loan disbursements. However, the sector has been recovering well since restrictions were lifted. The aluminum market recovered significantly in the 2021-22 period, owing to rising consumption from various end-user industries.

Key Highlights

- Over the short term, the growing utilization of recycled aluminum in the automotive and construction industry is expected to drive demand for the market.

- On the contrary, the presence of undesirable impurities like iron is likely to hamper the market's growth.

- Growth in the electric vehicles segment and growing focus on the reduction of carbon footprint are likely to provide new growth opportunities for the market.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Aluminum Recycling Market Trends

Increasing Demand from the Building and Construction Industry

- Aluminum is the second most widely used metal in the building and construction industry. Around 60% of the aluminum used in the buildings consists of recycled material.

- Recycled aluminum casting alloys, extruded sheets, and other products were used in floating ceilings, windows, doors, stairs, wall panels, roof sheets, and a variety of other applications.

- The use of recycled aluminum also offers substantial energy benefits. Remelting used aluminum requires only 5 percent of the energy needed to produce primary metal. Thus, rather than contributing to society's growing waste problem, aluminum can be remelted and reformed to produce a new generation of building parts.

- Secondary aluminum/recycled aluminum products are extensively used in building facades, curtain walls, roofing and cladding, solar shading, solar panels, railings, staircases, shelves, and other temporary structures. They are also used in the construction of high-rise buildings, skyscrapers, and bridges.

- According to the Oxford Economics report, global construction output is expected to grow the most in the Asia-Pacific region by around 40% by 2030, followed by the North American region by nearly 16%.

- Increasing construction activity worldwide is one of the key factors driving the market studied in recent times. Asia-Pacific, North America, and the Middle East, among others, are witnessing a positive growth rate in the building and construction industry. Hence, the demand for the recycling aluminum market is likely to increase over the forecast period.

- In Asia-Pacific, China is amid a construction mega-boom. Globally, China has the most significant building market, making up around 20% of all construction investments across the world. The country alone is likely to spend about USD 13 trillion on buildings by 2030.

- The construction industry is the second-largest in India. It grew at 10.7% in 2022. By the end of the forecast period, India's construction industry may emerge as the third-largest market across the world, with a size of around USD 1 trillion.

- As per the Canadian Construction Association data, the construction sector is one of largest employers in Canada and a significant contributor to the country's economic success. The industry contributes to 7% of the country's GDP.

- As part of the 'Investing in Canada Plan,' the Canadian government has announced plans to invest around USD 140 billion for significant infrastructure developments in the country by 2028. In 2019-20, the government plans to approve investments valuing USD 5.6 billion for new infrastructure projects in the country.

- The announcement of Vision 2030 and the National Transformation Plan (NTP) in Saudi Arabia have increased investments in different sectors, such as education and healthcare, to support the economic growth of the country. The government has expansive plans for the development of social infrastructure in the country. Government and private investments in various sectors of the country are likely to lead to a rise in commercial building construction activities.

- Therefore, owing to the factors mentioned above, the demand for recycled aluminum will be positively impacted during the forecasted period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to be the largest growing market for recycled aluminum during the forecast period. Industries such as electronics, automotive, building and construction, aerospace and defense, etc., are growing in countries such as China, India, and Japan, among others.

- China has been recycling aluminum domestically since the 1970s. Additionally, It has increased its focus on secondary Aluminum in recent years. In this regard, It is planning to cap the primary aluminum smelting capacity at around 45 million tons by 2030.

- As per the International Trade Administration (ITA) data, China remains the largest auto market globally in annual sales and production. Domestic production is anticipated to reach nearly 35 million units by 2025. The Chinese government is boosting car consumption following the COVID-19 pandemic. China accounts for over half (58%) of all new electric vehicles sold worldwide. According to the International Energy Agency (IEA), 5.9 million new electric cars will be sold nationwide in 2022, an increase of more than 80% compared to 2021.

- According to the report of the International Trade Organization, China is the largest construction market across the world and has the highest rate of urbanization globally. According to data from the American Institute of Architects (AIA) Shanghai, by 2025, China will have built a city equivalent to 10 in New York since the 1990s.

- According to the Indian Brand Equity Foundation (IBEF), the civil aviation industry has become one of India's fastest-growing industries in recent years. The aviation industry in India is expected to be affected by the new coronavirus, as can be seen from the fact that the air traffic volume in 2023 (April to December 2022) was 236.71 million, compared to 131.61 million in the same period of the previous year. Furthermore, In June 2023, the Indian company Air India signed agreements with Airbus and Boeing to purchase 470 planes for an estimated cost of USD 70 billion.

- The consumer electronics industry in Japan is one of the world's leading industries. The country is a world leader in producing computers, gaming stations, cell phones, and other vital components. Further, consumer electronics account for around one-third of the Japanese economic output. Japan's overall electronics production has declined due to stiff competition from countries such as India, China, and South Korea.

- According to the Japanese Electronics and Information Technology Industries (JEITA), the production value of consumer electronic equipment in the country stood at JPY 23,425 million (USD 165 million) in January 2023, increasing by a significant 79.8% during the same period last year. Meanwhile, the production value of electronic devices stood at JPY 290,309 million (USD 2,042 million) in January 2023, increasing by 89.6% annually.

- Thus, the factors above will likely affect the market demand studied during the forecast period.

Aluminum Recycling Industry Overview

The aluminum recycling market is fragmented in nature. Some major players include Novelis Inc., Speira GmbH, Norsk Hydro ASA, Matalco Inc., and Raffmetal, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Utilization of Recycled Aluminum in the Construction Industry

- 4.1.2 Growing Demand for Recycled Aluminum from the Automotive Industry

- 4.2 Restraints

- 4.2.1 Presence of Undesirable Impurities Like Iron

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Casting Alloys

- 5.1.2 Extrusion

- 5.1.3 Sheets

- 5.1.4 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Building and Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Packaging

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alcoa Corporation

- 6.4.2 Amag Austria Metall AG

- 6.4.3 Constellium

- 6.4.4 Kuusakoski OY

- 6.4.5 Matalco Inc.

- 6.4.6 Norsk Hydro Asa

- 6.4.7 Novelis

- 6.4.8 Raffmetal Spa

- 6.4.9 Real Alloy

- 6.4.10 Speira Gmbh

- 6.4.11 Stena Metall AB

- 6.4.12 Ye Chiu Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growth in the Electric Vehicles Segment

- 7.2 Growing Focus on Reduction of Carbon Footprint