|

市場調査レポート

商品コード

1851167

機械式人工呼吸器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Mechanical Ventilators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 機械式人工呼吸器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

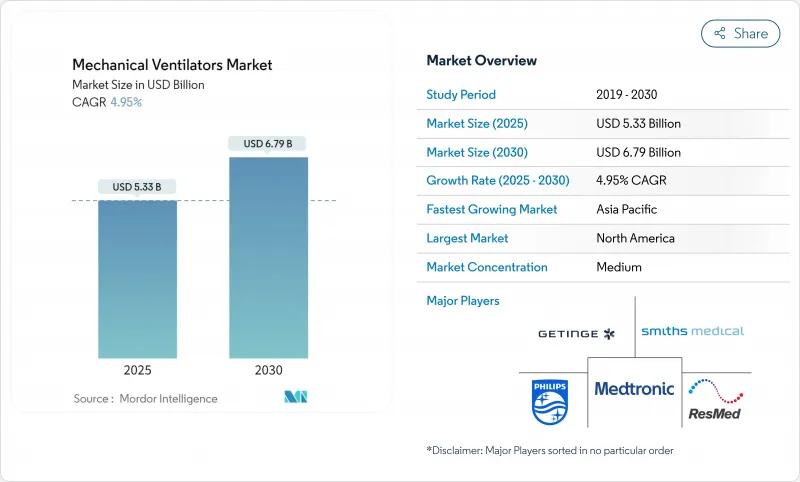

機械式人工呼吸器市場の2025年の市場規模は53億3,000万米ドルで、2030年には67億9,000万米ドルに達すると予測され、CAGRは4.95%で推移します。

成長は、パンデミックによる急増から、ICUでの長期滞在を必要とする高齢化やCOPDなどの慢性呼吸器疾患の増加に支えられた着実な拡大へと移行しつつあります。人工知能がクローズドループの人工呼吸を自動化し、臨床医の負担を軽減し、合併症を減少させるため、資本予算が厳しいにもかかわらず、病院は医療機器を更新する傾向にあります。メディケアの規則が更新され、慢性呼吸不全に対する非侵襲的人工呼吸がカバーされ、患者が再入院を回避できるようになったため、在宅医療が並行して成長エンジンとして台頭してきています。特にアジア太平洋地域では、重症患者向け医療インフラが地域的に不均衡であるため、より低い急性期ニーズに対応する費用対効果の高い機器のホワイトスペースとなる可能性があります。

世界の機械式人工呼吸器市場の動向と洞察

COPD有病率の上昇

世界のCOPD患者数は増加の一途をたどっており、侵襲的・非侵襲的デバイスの需要が強化されています。メディケア&メディケイド・サービスセンター(Centers for Medicare &Medicaid Services)は、PaCO2が52mmHg以上の場合に在宅人工呼吸の適用範囲を2025年までに拡大し、COPDの治療対象者を拡大した。在宅療法は、日中の呼吸困難は残るもの、再入院を減らし、血液ガス交換を改善します。このような成果は、支払者に受け入れられ、メーカーがコンパクトでメンテナンスの少ない非侵襲的モデルを調整する原動力となっています。疾病負担が高齢化するにつれて、慢性合併症管理への幅広い人口統計学的シフトに伴い、需要も収束していきます。

高齢化とICU能力の拡大

高齢者はすでにオーストラリアの人口の22%を占めており、同様の傾向は欧米にも見られます。慢性疾患の増加に伴い、米国では2030年までに1億7,000万日の入院日数が発生すると病院協会は予測しています。換気コースの長期化が機器の入れ替えを促進し、集中治療専門医の不足が続くと、病院は手による調整を減らすよりスマートなモードに投資するようになります。フランスでは現在、ICUの3分の2が少なくとも1人の医師を欠員としており、自動化の価値を高めています。中国のような国々は、今世紀半ばまでに一人当たりの医療費を10倍以上に引き上げる可能性のある大規模な支出増を計画しており、これは持続的な能力増強を示唆しています。COVID-19のパンデミックは地理的な不均衡を露呈したが、テクノロジー・サプライヤーはモジュール式で迅速な配備が可能なユニットを通じて、その是正を支援することができます。

高い医療機器とメンテナンス・コスト

地政学的ショックによる部品価格の高騰により、サプライチェーン費用総額は機器収益の最大20%を吸収します。人工呼吸器はメディケアの「頻繁かつ実質的な保守点検」のカテゴリーに分類され、定期的な保守点検が義務付けられているため、所有コストが膨れ上がっています。FDAの2026年品質規則への対応により、特にAIソフトウェア更新のための文書化・検証費用がさらに増加します。ICUの病床数が平均以下の新興病院は、プレミアムモデルの資金調達に苦戦し、再生品や現地組み立てのユニットに舵を切っています。サプライヤーは、ロジスティクスのオーバーヘッドを抑制するため、急性期病床の階層間で部品を共有するモジュラー設計で対応しています。

セグメント分析

集中治療室が機械式人工呼吸器市場シェアの54.91%を占めています。集中治療室の購買決定がサプライヤーの研究開発の主導権を握り、適応性の高いクローズドループモードと低騒音タービンが生産され、それが搬送用バリエーションに移行しています。ICUモデルの機械式人工呼吸器市場規模は、引き続き全体の売上高を上回ると予測されます。これは、ソフトウェアの進歩により測定可能な品質向上が促進されると、病院が低施設よりも早くフリート更新を行うためです。ポータブル機器は、より小さいベースからスタートするもの、救急サービスや災害対応チームがバッテリー駆動時間と頑丈なハウジングを優先するため、CAGR 5.34%で加速します。HAMILTON-C6は、ICUグレードのアルゴリズムを10kg以下の可動式筐体にパッケージ化することで、セグメントを超えた技術移転を実現しています。特に北米では、診療報酬コードで施設間移動時の請求が可能になると、搬送の採用も増えます。

亜急性期病棟向けのハイブリッド製品クラスが登場し、離床ツールと中程度のフロー機能を融合させることで、フルプライスのICUハードウェアを回避しています。フリートマネージャーは、シャーシファミリーに共通する消耗品を高く評価し、在庫を減らしています。モビリティ・クラス間で共通のユーザー・インターフェイスを設計するサプライヤーは、トレーニングを簡素化し、ユーザー・エラーを削減します。このような価値提案は、公共入札が最低コスト準拠の入札を重視する中でも、割高な価格設定を守るのに役立っています。

侵襲的人工呼吸は、2024年の売上高の64.25%を占める。これは、重症ARDSや外科手術では依然として気管内アクセスが必要なためです。侵襲的システムに関連する機械式人工呼吸器の市場規模は小幅に拡大する一方、非侵襲的ラインは家庭内への普及と早期介入プロトコルのおかげでCAGR 5.71%を記録します。IntelliTrigのような漏れを補償するソフトウェアは、患者の同調性を高め、挿管へのエスカレーションを減少させる。病院では、臨床医がハードウェアを交換することなく切り替えられるよう、デュアルモード機器の導入が進んでいます。

非侵襲的な利点は、小児および新生児用アプリケーションの増加にも起因します。小さな気道や顔の構造に合わせたインターフェースは、長時間の治療を可能にすると同時に、皮膚の傷害を軽減します。ヘルメットやマウスピース型人工呼吸器は、マスクが閉所恐怖症の引き金となる場合に、代替手段を提供します。高流量鼻カニューレの規制承認は、軽度の低酸素血症の症例をカバーすることで、従来のNIVに競争相手を加えます。メーカーは、モジュール式マニホールドコネクターやセンサーアレイを通じて、ポートフォリオの幅と在庫の複雑さのバランスをとっています。

地域分析

機械式人工呼吸器市場シェアの42.91%を占める北米は、広範なICUインフラ、連邦政府の備蓄、支援的な償還の枠組みから利益を得ています。公共調達政策は現在、集中的な予備購入と病院設備の更新補助を組み合わせており、2020~2022年の需要急増後の注文パターンをスムーズにしています。FDA(米国食品医薬品局)のサイバーセキュリティ・ガイダンスの遵守も、有効なソフトウェア・ライフサイクルを持つ国内サプライヤーに有利です。

欧州は、成熟しつつも革新的なバイヤーとして続きます。同地域では、エネルギー効率の高いタービンや暗号化されたクラウドコネクターにベンダーを向かわせる厳しい環境設計とデータ保護規則が施行されています。数カ国がクリティカルケアのためのAIロードマップを策定し、試験的導入に資金を提供しています。平均販売価格とソフトウェア・サブスクリプションの上昇により収益が増加。

アジア太平洋地域はCAGR最速の6.71%を記録。中所得国の人口10万人当たりの重症患者ベッド数を5床以上に引き上げることを目指す医療インフラ構想が原動力となっています。地域内のばらつきは大きいです。日本のような高所得国は5年ごとのアップグレードサイクルを維持しているのに対し、低所得国は助成金による資金調達に依存しています。サプライヤーは、壁掛け式とコンプレッサー式の両方の酸素源を受け入れる拡張可能なプラットフォームを提供することで成功を収めています。

2009年に中国が集中治療を専門分野として認めたことで、プロトコルを標準化し、機器の入札を加速させる専門学会のネットワークに火がついた。地元企業は輸入関税を回避するために欧米のタービン技術を共同ライセンスし、多国籍企業に価格圧力をかけています。インドとインドネシアは、国内での付加価値向上を30%以上促進するMake-in-Country制度を優先しています。

ラテンアメリカではCOVID-19の間に緊急製造ブームが起きました。各国政府は現在、一部のポップアップ施設を常設の重症患者用病棟に転換し、中堅クラスの人工呼吸器に対する基本需要を維持しています。それにもかかわらず、通貨変動が資本輸入を複雑にしているため、リースモデルが人気を集めています。

中東とアフリカは普及が遅れているが、長期的な可能性を秘めています。石油資源の豊富な湾岸諸国は、ハイスペックなICUに資金を提供し、一酸化窒素供給機能を内蔵した高級機を求めています。資源の乏しい国々はドナーからの資金援助に依存しており、埃っぽい環境や可変電源に対応できる頑丈なユニットを必要としています。サプライヤーはNGOと提携し、トレーニングをバンドルすることで採用を容易にしています。

米国は北米の機械式人工呼吸器市場を独占し、2024年の人工呼吸器市場シェアの約45%を占める。同国の市場リーダーシップは、高度な集中治療施設を備えた5,000以上の病院からなる広範なヘルスケアネットワークによって支えられています。大手メーカーの存在、強固なヘルスケア・インフラ、高い医療費支出により、同国の市場地位はさらに強化されています。米国市場は、慢性呼吸器疾患の罹患率の上昇と長期的な換気サポートを必要とする高齢化によって、集中治療用人工呼吸器とポータブル換気ソリューションの両方に対する旺盛な需要が特徴となっています。

カナダは北米で最も急成長している市場で、2024~2029年の成長率は約7%と予測されています。同国の市場成長の原動力は、ヘルスケア支出の増加、在宅ヘルスケアソリューションの採用拡大、呼吸ケア管理に対する意識の高まりです。カナダのヘルスケア施設では、患者の予後を改善するために高度な換気技術への投資が増加しています。政府の支援的なヘルスケア政策とクリティカルケアインフラの強化に注力する姿勢が市場拡大に寄与しています。同国では、特に遠隔地のヘルスケア環境や在宅ケア用途で、ポータブル換気装置の需要も高いです。

欧州の機械式人工呼吸器市場は、ドイツ、英国、フランス、イタリア、スペインの確立されたヘルスケアシステムに支えられ、大きな力強さを示しています。この地域の市場は、先進医療技術の採用率が高く、大手人工呼吸器メーカーが強い存在感を示しているのが特徴です。欧州諸国は医療機器に対する厳しい規制基準を維持する一方で、ヘルスケアインフラの改善に継続的に投資しています。同市場は、在宅ヘルスケアソリューションへの注目の高まりと、携帯型人工呼吸器に対する需要の高まりから恩恵を受けています。

ドイツは欧州の機械式人工呼吸器市場をリードしており、2024年にはこの地域の人工呼吸器市場シェアの約20%を占める。同国が市場をリードしている理由は、強固なヘルスケアシステム、多額の医療費、強力な国内製造能力にあります。ドイツの病院は高水準の集中治療施設を維持しており、先進的な人工呼吸ソリューションに対する一貫した需要を示しています。大手メーカーや研究機関の存在が換気技術の絶え間ない技術革新に貢献する一方、高齢化が市場の持続的成長を後押ししています。

英国は欧州の中でも重要な市場であり、2024~2029年の成長率は約7%と予測されています。英国のヘルスケアシステムは、クリティカルケアインフラの近代化と高度な呼吸ケアソリューションへのアクセス拡大に投資を続けています。同国では、在宅ヘルスケアサービスの重視が高まっていることを背景に、ポータブル換気ソリューションや在宅換気ソリューションの採用が増加しています。英国のヘルスケア施設は、患者ケアの転帰と業務効率を改善するため、新しい換気技術を積極的に取り入れています。

アジア太平洋市場は、中国、日本、インド、韓国、オーストラリアの多様なヘルスケア市場を包含し、力強い成長の可能性を示しています。同地域では、ヘルスケアインフラの整備が進み、ヘルスケア支出が増加し、呼吸ケアに対する意識が高まっています。急速な都市化、汚染レベルの上昇、呼吸器疾患の罹患率の上昇が、これらの国々における市場拡大の原動力となっています。この地域はまた、国内製造能力の向上と先進医療技術の採用増加からも利益を得ています。

中国はアジア太平洋地域最大の機械式人工呼吸器市場としての地位を維持しています。同国の広範なヘルスケアシステムの近代化、患者数の多さ、国内製造能力の向上が市場成長の原動力となっています。中国のヘルスケア施設はクリティカルケア能力を拡大し続けており、一方で在宅ヘルスケアソリューションへの注目が高まっていることが新たな市場機会を生み出しています。ヘルスケア・インフラへの投資と医療機器製造の自給自足を重視する姿勢が、同国の市場ポジションを強化しています。

韓国はアジア太平洋地域で最も急成長している市場です。同国の先進的なヘルスケアシステム、強力な技術力、ヘルスケアイノベーションへの注力の高まりが市場拡大の原動力となっています。韓国のヘルスケア施設は高度な換気技術の採用率が高く、高齢化が進む同国では持続的な需要が創出されています。同市場は、強力な国内製造能力とヘルスケア・インフラ開拓への継続的な投資によって利益を得ています。

中東・アフリカ機械式人工呼吸器市場は有望な成長ポテンシャルを示すが、地域によって大きなばらつきがあります。GCC諸国は、大規模なヘルスケア投資と近代的な医療施設の恩恵を受け、地域市場をリードしています。南アフリカも主要市場のひとつであり、医療インフラの整備と先進医療技術の導入が進んでいます。同地域では、救命救急施設の改善と高度な呼吸ケアソリューションへのアクセス拡大にますます焦点が当てられており、GCC諸国は同地域で最大かつ最も急成長している市場として浮上しています。

南米の機械式人工呼吸器市場は進化を続けており、ブラジルとアルゼンチンが同地域の主要市場となっています。同市場は、継続的なヘルスケアインフラの開拓、医療費の増加、呼吸ケアに対する意識の高まりなどの恩恵を受けています。ブラジルは同地域最大の市場としての地位を維持し、アルゼンチンは最も速い成長の可能性を示しています。同地域では、医療投資の拡大と先進医療技術へのアクセスの拡大により、集中治療用およびポータブル換気ソリューションの採用が増加しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- COPD有病率の上昇

- 高齢化とICUの能力拡大

- 政府のパンデミック対策備蓄

- AIによるクローズドループ換気の採用

- 肥満低換気症候群の家庭用NIVの成長

- マイクロタービンとバッテリーの効率向上

- 市場抑制要因

- 高い機器とメンテナンスコスト

- 人工呼吸器関連肺炎(VAP)

- 半導体サプライチェーンの変動

- 長期在宅使用に対する償還削減

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額・台数)

- モビリティ別

- 集中治療(ICU)用人工呼吸器

- 輸送/ポータブル換気装置

- 亜急性期および長期介護用人工呼吸器

- インターフェース別

- 侵襲的換気

- 非侵襲的人工呼吸(NIV)

- 患者年齢別

- 成人用

- 小児

- 新生児

- エンドユーザー別

- 病院

- ホームヘルスケア

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Medtronic plc

- Getinge AB

- GE HealthCare Technologies Inc.

- Dragerwerk AG & Co. KGaA

- Koninklijke Philips N.V.

- Smiths Medical(ICU Medical)

- ResMed Inc.

- Mindray Medical Intl.

- Nihon Kohden Corp.

- Zoll Medical Corp.

- Fisher & Paykel Healthcare

- Hamilton Medical AG

- Allied Healthcare Products

- Vyaire Medical

- Bunnell Inc.

- Airon Corp.

- Shenzhen SiareSys

- Lowenstein Medical

- Magnamed

- Bio-Med Devices

- Timpel S/A