|

市場調査レポート

商品コード

1683227

無人システム市場-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Unmanned Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 無人システム市場-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

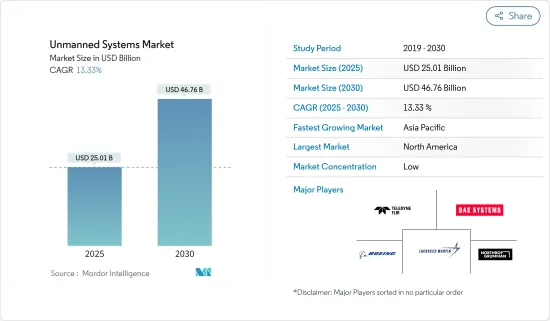

無人システム市場規模は2025年に250億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.33%で、2030年には467億6,000万米ドルに達すると予測されます。

世界の防衛費の増加、防衛力強化への注力、情報・モニタリング・偵察(ISR)や戦闘任務での無人システムの利用拡大が、市場の成長を後押ししています。国防軍は、有人システムよりも無人システムの開発・調達に大きく投資しています。無人システムは兵士の死傷リスクを軽減し、戦闘作戦中の精度を高めるからです。

消防や農業での無人地上車両(UGV)、海中探査や海洋調査での無人海上車両(USV)、災害救助やレクリエーション用途、写真・ビデオ撮影での無人航空機(UAV)など、商業セグメントでの無人システムの利用拡大が市場の成長を後押しします。

しかし、世界のいくつかの国では、目視外でのドローンの飛行に関する規制や制限がないことが、市場の成長を抑制しています。また、安全性やセキュリティへの懸念、訓練されたパイロットの不足など、その他の要因も市場の成長に一定の課題を与えると予想されます。

無人システム市場の動向

無人航空機セグメントが予測期間中に最も高い成長を遂げる

諜報・モニタリング・偵察(ISR)や戦闘任務への小型UAVの採用拡大、防衛セグメントへの支出増加が、予測期間中の市場成長を牽引する可能性があります。様々な商業・軍事用途の小型UAVの設計・開発に対する新興企業の増加や政府資金の増加が、市場成長をさらに後押しします。例えば、2023年10月、Teledyne FLIR LLCは、センサをアップグレードしたBlack Hornetナノドローンの最新版を発売しました。新たに発売されたBlack Hornet 4は、全長1フィート以下、重さ1ポンドのわずかなサイズです。30分以上の飛行が可能で、航続距離は2kmを超えます。日中の高感度カメラ、ビデオや画像を撮影する赤外線イメージャー、ソフトウェア定義データシステムを搭載しています。

また、2023年10月、台湾の国防省(MND)は、国内の民間企業から軍用ドローン3,221機を取得する計画を発表しました。国防省は5種類のUAVに約1億7,557万米ドルを費やす計画です。これらには、海軍の陸上モニタリング無人機、陸軍の標的無人機、超小型無人機、海軍の艦船搭載型モニタリング無人機、全軍のモニタリング無人機が含まれます。

また、地図作成、測量、検査、配送、農業、メディア、娯楽、公共の安全など、さまざまな用途にUAVを使用する潜在的な利点を認識する産業が増えているため、民間と商業セグメントもUAVの重要な市場として浮上しています。米連邦航空局(FAA)によると、米国で登録されている87万2248機のUAVのうち、33万8614機が商用UAVとして登録されています。同局は、米国の業務用UAVの規模は2026年までに85万8,000機にまで急増すると予測しています。

予測期間中、アジア太平洋が最も高い需要を生み出す見込み

アジア太平洋は、中国、インド、日本のような国々からの無人システムへの旺盛な投資により、予測期間中に著しい成長を示すと予想されます。このような成長は、この地域の国々による防衛費の増加や、商業セグメントでの無人システムの使用に関する有利な規制によるものです。

インド、日本、インドネシアなどアジアの様々な国々は現在、貨物や小包を輸送するために無人航空機の使用に取り組んでいます。国境を越えた紛争の増加、テロの増加、近隣諸国の政情不安などを背景に、インド、中国、オーストラリアなどからの先進的な無人システムの調達が増加しており、この地域全体の市場成長を牽引しています。同様に、無人地上車両(UGV)は韓国、中国、日本などで開発されており、現場装備や負傷者の避難、重い荷物の移動など、手作業によるさまざまな作業で防衛軍を支援しています。

例えば、2022年9月、日本を拠点とするドローンファンド(DF)は、Aerodyne India Groupと提携し、製造施設に投資し、インドの無人航空機エコシステムに4,000万米ドルを投資する予定です。さらに2023年8月、インド政府はAtmanirbhar Bharat施策の一環として、生産連動インセンティブ(PLI)スキームを承認しました。同制度では、UAVとUAVコンポーネントの開発に3年間で12億インドルピー(1,450万米ドル)の資金が割り当てられました。このような開発は、この地域の市場開拓の原動力となると考えられます。

無人システム産業概要

無人システム市場は非常にセグメント化されており、多くのサプライヤーがUGV、UAV、USVなどの無人プラットフォームを提供しています。同市場の主要企業には、Lockheed Martin Corporation、BAE Systems PLC、The Boeing Company、Teledyne FLIR LLC、Northrop Grumman Corporationなどがあります。これらのOEMはあらゆる種類の無人システムを提供しており、各社の資本増強や地理的プレゼンス拡大、キャッシュフローの多様化に役立っています。主要要因は製品の革新で、防衛・商業部門から新規契約を獲得するのに役立っています。さらに、地元企業と大手企業との合併・買収によって、製品ポートフォリオと市場での存在感を拡大することができます。2023年7月、SZ DJI TechnologyはDJI Air 3ドローンの発売を発表しました。Air 3は焦点距離24mmのF1.7プライマリーカメラと焦点距離70mmのF2.4望遠レンズを搭載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 無人航空機

- 小型UAV

- 中型UAV

- 大型UAV

- 無人地上車両

- 車輪付き

- 追跡型

- 脚式

- ハイブリッド

- 無人海上システム

- 無人潜水機(UUV)

- 無人水上機(USV)

- 無人航空機

- アプリケーション

- 軍事・法執行

- 商用

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 韓国

- 日本

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- QinetiQ Group

- Israel Aerospace Industries Ltd

- General Dynamics Corporation

- Rheinmetall AG

- Teledyne FLIR LLC

- ECA Group

- The Boeing Company

- Elbit Systems Ltd

- Lockheed Martin Corporation

- Saab AB

- BAE Systems PLC

- Northrop Grumman Corporation

- L3Harris Technologies Inc.

- SZ DJI Technology Co. Ltd

第7章 市場機会と今後の動向

The Unmanned Systems Market size is estimated at USD 25.01 billion in 2025, and is expected to reach USD 46.76 billion by 2030, at a CAGR of 13.33% during the forecast period (2025-2030).

Increasing global defense expenditures, a focus on strengthening defense forces, and the growing use of unmanned systems for intelligence, surveillance, and reconnaissance (ISR) and combat missions drive the market's growth. Defense forces are highly invested in developing and procuring unmanned systems over manned systems as they reduce the risks of soldier casualties and enhance accuracy during combat operations.

The growing use of unmanned systems in the commercial sectors, such as unmanned ground vehicles (UGVs) in firefighting and agriculture, unmanned sea vehicles (USVs) for underwater sea exploration and marine research, and unmanned aerial vehicles (UAVs) for disaster relief, recreational uses, and photo and videography, will boost the market growth.

However, the lack of regulations and restrictions on flying drones beyond the visual line of sight in several countries worldwide has restrained the market's growth. Other factors, such as safety and security concerns and the scarcity of trained pilots, are also anticipated to challenge the market's growth to a certain extent.

Unmanned Systems Market Trends

The Unmanned Aerial Vehicles Segment to Witness the Highest Growth During the Forecast Period

The growing adoption of small UAVs for intelligence, surveillance, and reconnaissance (ISR) and combat missions and rising spending on the defense sector may drive market growth during the forecast period. An increase in several start-ups and rising government funding to design and develop small UAVs for various commercial and military applications further boost the market growth. For instance, in October 2023, Teledyne FLIR LLC launched the latest edition of the Black Hornet nano-drone with upgraded sensors. The newly launched Black Hornet 4 is less than a foot long and weighs a fraction of a pound. It can fly for over 30 minutes and has a range of more than 2 kilometers (1.24 miles). It has a sensitive daytime camera, a thermal imager to capture videos and images, and a software-defined data system.

Also, in October 2023, Taiwan's Ministry of National Defense (MND) unveiled a plan to acquire 3,221 military-grade commercial drones from the country's private sector. The MND plans to spend approximately USD 175.57 million on five types of UAVs. These include land surveillance drones for the Navy, target drones for the Army, micro drones, ship-based surveillance UAVs for the Navy, and surveillance drones for all armed forces.

The civil and commercial sectors are also emerging as significant markets for UAVs as more and more industries realize the potential benefits of using UAVs for various applications, such as mapping, surveying, inspection, delivery, agriculture, media, entertainment, and public safety. According to the Federal Aviation Administration (FAA), 338,614 of the 872,248 UAVs registered in the US are registered as commercial UAVs. The agency forecasts that the size of the commercial UAV fleet in the US could jump to as much as 858,000 by 2026.

Asia-Pacific is Expected to Generate the Highest Demand during the Forecast Period

Asia-Pacific is expected to show remarkable growth during the forecast period due to robust investments from countries like China, India, and Japan in unmanned systems. This growth is attributed to a rise in defense expenditures by the countries in this region and favorable regulations to use unmanned systems in the commercial sector.

Various Asian countries such as India, Japan, and Indonesia are currently working on using unmanned aerial vehicles to transport cargo and parcels. Rising procurement of advanced unmanned systems from India, China, Australia, and others due to rising cross-border conflicts, increasing terrorism, and political unrest among neighboring countries drive market growth across the region. Similarly, unmanned ground vehicles (UGVs) are being developed in South Korea, China, and Japan, among others, to assist their defense forces with a range of manual handling tasks such as field equipment and casualty evacuations and moving heavy loads.

For instance, in September 2022, Japan-based Drone Fund (DF) tied up with Aerodyne India Group to invest in manufacturing facilities and is planning to invest USD 40 million in India's unmanned aerial vehicle ecosystem. In addition, in August 2023, as a part of the Atmanirbhar Bharat policy, the Indian government approved the Production Linked Incentive (PLI) scheme. It allocated a fund of INR 120 crore (USD 14.5 million) for three years to develop UAVs and UAV components. Such development will drive market growth across the region.

Unmanned Systems Industry Overview

The unmanned systems market is highly fragmented, with many suppliers providing unmanned platforms such as UGVs, UAVs, and USVs. Some of the key players in the market are Lockheed Martin Corporation, BAE Systems PLC, The Boeing Company, Teledyne FLIR LLC, and Northrop Grumman Corporation. These OEMs provide all types of unmanned systems, which help the companies capitalize and expand their geographic presence and diversify their cash flows. The primary factor is product innovation, which aids companies in getting new contracts from the defense and commercial sectors. In addition, the mergers and acquisitions of local companies with major companies allow them to expand their product portfolio and market presence. In July 2023, SZ DJI Technology Co. Ltd announced the DJI Air 3 drone launch. The Air 3 has an f/1.7 primary camera with a focal length of 24 mm and an f/2.4 telephoto lens with a focal length of 70 mm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Unmanned Aerial Vehicles

- 5.1.1.1 Small UAVs

- 5.1.1.2 Medium UAVs

- 5.1.1.3 Large UAVs

- 5.1.2 Unmanned Ground Vehicles

- 5.1.2.1 Wheeled

- 5.1.2.2 Tracked

- 5.1.2.3 Legged

- 5.1.2.4 Hybrid

- 5.1.3 Unmanned Sea Systems

- 5.1.3.1 Unmanned Underwater Vehicles (UUVs)

- 5.1.3.2 Unmanned Surface Vehicles (USVs)

- 5.1.1 Unmanned Aerial Vehicles

- 5.2 Application

- 5.2.1 Military and Law Enforcement

- 5.2.2 Commercial

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 South Korea

- 5.3.3.4 Japan

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 QinetiQ Group

- 6.2.2 Israel Aerospace Industries Ltd

- 6.2.3 General Dynamics Corporation

- 6.2.4 Rheinmetall AG

- 6.2.5 Teledyne FLIR LLC

- 6.2.6 ECA Group

- 6.2.7 The Boeing Company

- 6.2.8 Elbit Systems Ltd

- 6.2.9 Lockheed Martin Corporation

- 6.2.10 Saab AB

- 6.2.11 BAE Systems PLC

- 6.2.12 Northrop Grumman Corporation

- 6.2.13 L3Harris Technologies Inc.

- 6.2.14 SZ DJI Technology Co. Ltd