ポリマー生体材料の世界市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Polymeric Biomaterials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683218

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

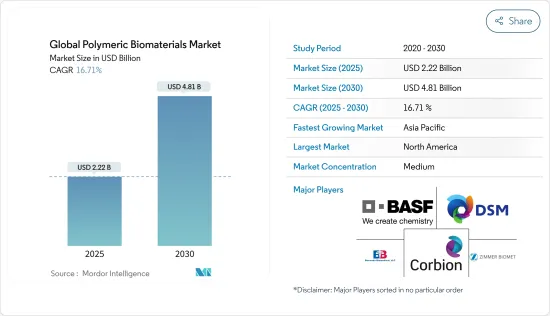

ポリマー生体材料の世界市場規模は、2025年に22億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.71%で、2030年には48億1,000万米ドルに達すると予測されます。

市場成長を後押しする主要要因としては、ポリマー生体材料の技術革新や、組織工学におけるポリマー生体材料の用途拡大などが挙げられます。神経と整形外科手術の件数が増加していることは、世界の市場成長の主要要因の1つです。

例えば、2024年2月にParkinson's United Kingdom(英国)で発表された報告書によると、英国では約15万3,000人がパーキンソン病を患っています。人口の高齢化と継続的な増加により、この数字は2030年までに20%近く増加し、17万2,000人になると予測されています。高齢化に伴うパーキンソン病の有病率の増加が、ポリマー生体材料市場の成長を後押ししています。これらの材料は、ドラッグデリバリーシステムや神経インプラントなど、先進的治療ソリューションの開発にますます使用されるようになっています。

さらに、ポリマー生体材料の用途の広がりと新製品の投入が相まって、市場の成長を促進すると予想されます。例えば、2023年6月、International Flavors & Fragrances(IFF)は、従来の化石由来材料と同等かそれ以上の性能を持ち、サステイナブル利点を提供するバイオベース材料の開発を目的とした画期的なDEB(Designated Enzymatic Biomaterials)技術を発表しました。この技術革新は、多様な産業における持続可能で高性能な代替材料に対する規制や消費者の要求の高まりに応えることで、ポリマー系生体材料市場の成長を促進すると期待されています。

結論として、ポリマー生体材料の技術革新、用途の拡大、サステイナブル生体材料の進歩が、ポリマー生体材料市場の成長を促進しています。しかし、ポリマー生体材料に関連する合併症が市場成長の妨げになると予想されます。

ポリマー生体材料の世界動向

整形外科セグメントは予測期間中に大きな成長が見込まれる

筋骨格系障害(MSD)の増加に伴い、MSDは外科的治療を必要とするため、整形外科セグメントは増加する可能性が高いです。したがって、このような治療のための生体材料に対する要求は高いです。例えば、オーストラリア政府が2024年6月に発表した報告書によると、オーストラリアでは2023年に人口の29%に相当する約730万人が慢性筋骨格系疾患に罹患すると推定されています。そのうち400万人が腰痛、370万人が関節炎、85万4,000人が骨粗鬆症または骨減少症です。慢性的な筋骨格系疾患の有病率の高さが、先進的整形外科ソリューションの需要を牽引しています。このような需要の増加が整形外科セグメントの成長を後押ししており、治療用と手術用の両方で、革新的で耐久性があり、生体適合性のある材料の必要性が浮き彫りになっています。

さらに、世界中で高齢者が増加しているため、関節炎、変形性関節症、関節リウマチなどの整形外科疾患を患う人の数が増加すると予想されています。例えば、世界保健機関(WHO)が2023年7月に発表した報告書によると、人口の高齢化が変形性関節症の大幅な増加につながっており、世界中で5億2,800万人以上が罹患しており、その大半が55歳以上です。整形外科疾患の罹患率が高い高齢者の増加は、先進的治療に対する需要を促進し、より効果的で耐久性のある生体材料の整形外科ソリューションに対するニーズを通じて、ポリマー生体材料市場の整形外科セグメントの成長を促進しています。

さらに、主要な市場参入企業による取り組みも、同セグメントの成長をもたらす要因のひとつです。例えば、2023年2月、Invibio Biomaterial Solutionsは、英国のリーズに新しい整形外科製品開発施設を開設しました。これは、医療機器の研究開発と製造能力を強化するための戦略的拡大を意味します。この開発により、インビビオは先進的なポリエーテルエーテルケトン(PEEK)ポリマー製インプラントデバイスの共同開発・上市において、OEMメーカーをサポートする能力を強化するとともに、学界や医療関連企業との協力関係を促進しました。

結論として、整形外科セグメントでの進歩、整形外科疾患の有病率の上昇、様々な医療セグメントでの用途の拡大により、ポリマー生体材料に対する需要の高まりが、同セグメントの成長を大きく促進すると予想されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米はポリマー生体材料市場で大きなシェアを占めており、今後もその牙城は揺るがないと予想されます。米国では、複数の非公開会社がバイオポリマーに関する豊富な専門知識を有し、先端技術やカスタム合成にアクセスしています。整形外科手術や整形外科的損傷などの外科手術の増加といった重要な要因が、市場の成長を後押しすると予想されています。

例えば、2024年6月に発表された国際美容整形外科学会の報告書によると、米国は世界で最も多くの美容整形外科手術を行い、2023年には610万件を超えました。このような手術、特に形成外科手術の件数の多さが、ポリマー生体材料市場の成長を後押ししています。これらの材料は組織適合性を高め、感染リスクを低減し、全体的な手術結果を改善します。

同様に、カナダにおける眼疾患の有病率の上昇も市場成長を促進すると予想されています。例えば、North Toronto Eye Careが発表した記事によると、2023年6月には、250万人のカナダ人が白内障とともに生活しています。同国では毎年35万件以上の白内障手術が行われています。カナダでは、白内障のような眼疾患の有病率が上昇しているため、先進的外科的介入に対する需要が高まっており、生体適合性と眼科手術での使用により、革新的なポリマー生体材料の必要性が加速しています。

同地域では、形成手術やその他の外科手術の件数が増加するにつれて、より患者に適合したポリマー生体材料への需要が急増し、調査期間中の市場の成長を牽引することになります。

ポリマー生体材料の世界産業概要

ポリマー生体材料市場の競争は中程度で、複数の大手企業で構成されています。市場シェアの面では、現在少数の大手企業が市場を独占しています。しかし、技術の進歩や製品の革新に伴い、中堅から中小の企業が市場での存在感を高めています。BASF SE、Bezwada Biomedical LLC、Corbion NV、Zimmer Biomet、Royal DSMといった企業がかなりの市場シェアを占めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ポリマー生体材料セグメントにおける新たなイノベーション

- 組織工学におけるポリマー生体材料の用途拡大

- 市場抑制要因

- ポリマー生体材料に関連する合併症

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-単位:米ドル)

- 製品タイプ別

- ポリアリールエーテルケトン

- ポリグリコール酸

- ポリ乳酸

- ポリテトラフルオロエチレン&発泡ポリテトラフルオロエチレン

- ポリウレタン

- その他

- 用途別

- 神経

- 循環器

- 整形外科

- 眼科

- 創傷治療

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- BASF SE

- Bezwada Biomedical LLC

- Collagen Solutions LLC

- Corbion NV

- Covestro AG

- Evonik Industries AG

- DSM-Firmenich AG

- Starch Medical Inc.

- Victrex Manufacturing Limited

- W. L. Gore & Associates, Inc.

- Zimmer Biomet

第7章 市場機会と今後の動向

目次

The Global Polymeric Biomaterials Market size is estimated at USD 2.22 billion in 2025, and is expected to reach USD 4.81 billion by 2030, at a CAGR of 16.71% during the forecast period (2025-2030).

The key factors propelling the market growth include innovations in polymeric biomaterials and increasing applications of polymeric biomaterials in tissue engineering. The rising number of neurological and orthopedic procedures is one of the major contributors to the market growth worldwide.

For instance, according to a report published in Parkinson's United Kingdom (UK) in February 2024, approximately 153,000 individuals in the United Kingdom are living with Parkinson's disease. With the aging population and continued growth, this figure is projected to rise by nearly 20% to 172,000 by 2030. The increasing prevalence of Parkinson's disease, driven by an aging population, is propelling the growth of the polymer biomaterials market. These materials are increasingly used in developing advanced therapeutic solutions, including drug delivery systems and neural implants.

Furthermore, widening applications of polymeric biomaterials coupled with introducing new products are expected to propel the market growth. For instance, in June 2023, International Flavors & Fragrances (IFF) introduced its groundbreaking Designed Enzymatic Biomaterials (DEB) technology, aimed at developing biobased materials that offer sustainability benefits with performance on par with or better than traditional fossil-based materials. This innovation is expected to drive growth in the polymer biomaterials market by meeting rising regulatory and consumer demands for sustainable, high-performance alternatives across diverse industries.

In conclusion, innovations in polymeric biomaterials, increasing applications, and advancements in sustainable biomaterials are propelling the growth of the polymer biomaterials market. However, complications associated with polymeric biomaterials are expected to hinder market growth.

Global Polymeric Biomaterials Market Trends

The Orthopedic Segment is Expected to Witness Significant Growth Over the Forecast Period

With the increasing number of musculoskeletal disorders (MSDs), the orthopedic segment is likely to increase as MSDs require surgical treatment. Hence, the requirement for biomaterials for such treatments is high. For instance, according to a report published by the Australian Government in June 2024, approximately 7.3 million individuals in Australia, representing 29% of the population, were estimated to be affected by chronic musculoskeletal conditions in 2023. Among them, 4.0 million experienced back issues, 3.7 million had arthritis, and 854,000 were living with osteoporosis or osteopenia. The high prevalence of chronic musculoskeletal conditions drives the demand for advanced orthopedic solutions. This increasing demand is propelling the growth of the orthopedic segment, highlighting the necessity for innovative, durable, and biocompatible materials for both therapeutic and surgical applications.

Additionally, the growing geriatric population across the globe is expected to increase the number of people suffering from orthopedic diseases, such as arthritis, osteoarthritis, and rheumatoid arthritis, as they are more prone to develop joint-related disorders due to weaker bones. For instance, according to a report published by the World Health Organization in July 2023, aging populations are leading to a significant rise in osteoarthritis cases, with over 528 million people worldwide affected, the majority being over 55 years old. The growing geriatric population, prone to the incidence of orthopedic conditions, is propelling the demand for advanced treatments, thereby driving growth in the orthopedic segment of the polymer biomaterials market through the need for more effective and durable biomaterial orthopedic solutions.

Moreover, initiatives by the key market players are another factor responsible for the segment growth. For instance, in February 2023, Invibio Biomaterial Solutions inaugurated a new orthopedic product development facility in Leeds, United Kingdom. It marked a strategic expansion to enhance its medical device research and development and manufacturing capabilities. This development strengthens Invibio's ability to support original medical device manufacturers (OEMs) in co-developing and launching advanced polyetheretherketone (PEEK) polymer implantable devices while fostering collaboration with academia and medical businesses.

In conclusion, the growing demand for polymeric biomaterials, driven by advancements in the orthopedic segment, the rising prevalence of orthopedic conditions, and expanding applications in various medical fields, is expected to propel segment growth significantly.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America holds a significant market share in the polymer biomaterials market and is expected to continue its stronghold for a few more years. In the United States, several private companies have vast expertise in biopolymers with access to advanced technology and custom synthesis. Significant factors such as increasing surgical procedures such as plastic surgery and orthopedic injuries are expected to boost the market growth.

For instance, according to the International Society of Aesthetic Plastic Surgery report published in June 2024, the United States performed the most aesthetic and surgical procedures worldwide, with over 6.1 million in 2023. The high number of these procedures, particularly in plastic surgeries, is propelling the growth of the polymer biomaterials market. These materials enhance tissue compatibility, reduce infection risks, and improve overall surgical outcomes.

Similarly, the rising prevalence of eye disorders in Canada is also expected to propel the market growth. For instance, according to an article published by North Toronto Eye Care, in June 2023, 2.5 million Canadians are living with cataracts in 2023. In the country, more than 350,000 cataract surgeries are performed each year. The rising prevalence of eye disorders in Canada, such as cataracts, drives demand for advanced surgical interventions, accelerating the need for innovative polymer biomaterials due to their biocompatibility and use in ophthalmic procedures.

As the number of plastic surgeries and other surgical procedures rises in the region, the demand for more patient-compatible polymer biomaterials is set to surge, driving the market's growth during the study period.

Global Polymeric Biomaterials Industry Overview

The polymer biomaterials market is moderately competitive and consists of several major players. In terms of market share, a small number of significant players currently dominate the market. However, with technological advancements and product innovations, mid-size to smaller companies are increasing their market presence. Companies like BASF SE, Bezwada Biomedical LLC, Corbion NV, Zimmer Biomet, and Royal DSM hold a substantial market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 New Innovations in the Field of Polymeric Biomaterials

- 4.2.2 Increasing Applications of Polymeric Biomaterials in Tissue Engineering

- 4.3 Market Restraints

- 4.3.1 Complications Associated with Polymeric Biomaterials

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size- in USD)

- 5.1 By Product Type

- 5.1.1 Polyaryletheretherketone

- 5.1.2 Polyglycolic Acid

- 5.1.3 Polylactic Acid

- 5.1.4 Polytetrafluoroethylene & Expanded Polytetrafluoroethylene

- 5.1.5 Polyurethanes

- 5.1.6 Other Products

- 5.2 By Application

- 5.2.1 Neurology

- 5.2.2 Cardiology

- 5.2.3 Orthopedics

- 5.2.4 Ophthalmology

- 5.2.5 Wound Care

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BASF SE

- 6.1.2 Bezwada Biomedical LLC

- 6.1.3 Collagen Solutions LLC

- 6.1.4 Corbion NV

- 6.1.5 Covestro AG

- 6.1.6 Evonik Industries AG

- 6.1.7 DSM-Firmenich AG

- 6.1.8 Starch Medical Inc.

- 6.1.9 Victrex Manufacturing Limited

- 6.1.10 W. L. Gore & Associates, Inc.

- 6.1.11 Zimmer Biomet

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日