|

市場調査レポート

商品コード

1683197

垂直共振器面発光レーザー市場:市場シェア分析、業界動向、成長予測(2025~2030年)Vertical Cavity Surface Emitting Laser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 垂直共振器面発光レーザー市場:市場シェア分析、業界動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 195 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

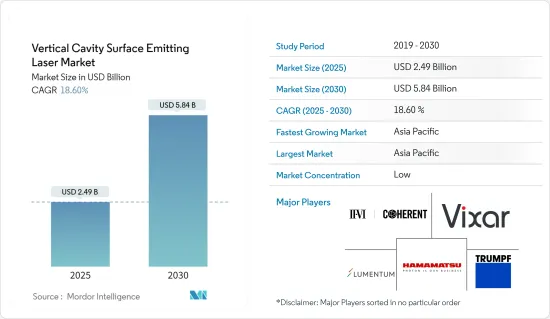

垂直共振器面発光レーザー市場規模は、2025年に24億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは18.6%で、2030年には58億4,000万米ドルに達すると予測されています。

出荷台数では、2025年の51億4,000万台から2030年には160億6,000万台に成長すると予測され、予測期間(2025~2030年)のCAGRは25.60%です。

垂直共振器面発光レーザー(VCSEL)は、レーザーが上面に対して垂直に放射される半導体です。端からレーザーを放出する端面発光レーザーとは異なります。VCSELは、高精度、高効率、高信頼性、高速性をコスト効率の高いソリューションで提供し、レーザー物理学における最も有望な新技術開発です。VCSELは、低消費電力、ビーム品質、変調速度、製造コストなど、さまざまな利点を備えています。

主要ハイライト

- VCSEL市場は、高速・高効率で長距離のデータ伝送に対する要求の高まり、車載LiDAR用途や産業用途におけるVCSELレーザー需要の高まりなど、いくつかの要因から予測期間中に力強い成長が見込まれます。2023年8月、Innoviz TechnologiesとBMWグループは、新世代LiDARのBサンプル開発フェーズを開始し、協業を拡大しています。

- ここ数年、データセンターにおける光相互接続インフラは、100Gビット/秒から次世代の400Gビット/秒のデータレートに進歩しています。これは主に、AI、VR/AR、モノのインターネット(IoT)などの新興技術の急速な市場成長や、5Gモバイルネットワークシステムの導入により、データセンター内のデータトラフィックが増加し続けていることに起因しています。

- スマートフォンメーカーによる3Dセンシングや近接センシング用途でのスマートフォンへのVCSEL採用の増加は、市場成長を促進する主要要因の1つです。3Dセンシングの成長は、iPhoneにフェイスIDモジュールが導入されたことで推進されました。それ以来、3Dセンシングには大きな進展がありました。徐々に、3Dセンシングはフロント側の顔認証モジュールから、写真撮影用途のリア側へと移行していりました。

- InPベースのVCSELは、低分散でファイバー損失が少ないため、一般に光通信などの用途に好まれます。しかし、InPベースのVSCELは、高い反射率と低い透過深度のために、大きな屈折率コントラストDBRミラーを提供することができないです。有効共振器長が同調範囲と閉じ込め係数を制限します。

- COVID-19の大流行は調査した市場に著しい影響を及ぼし、VCSELを導入するいくつかのエンドユーザー産業はいくつかの困難に直面しました。各産業は全国的な操業停止に見舞われ、足踏み状態に陥ったが、2020年第2四半期以降、徐々に操業を開始しました。原料は中国で購入するため、米国が課した関税の影響を受けています。

- 世界の地政学的緊張と紛争が軍事費需要を牽引しています。ストックホルム国際平和ラボ(SIPRI)によると、米国は2022年、軍事費が最も多い国のランキングで首位に立ち、軍事費に8,770億米ドルを投じた。これは同年の世界の軍事費総額2兆2,000億米ドルの40%近くを占めています。これは米国の国内総生産の3.5%に相当します。

垂直共振器面発光レーザーの市場動向

ADASとLiDARが急成長用途に

- 自動車産業は、VCSELメーカーにとって主要な新興市場の1つであり、自律走行車や自動車のハイエンド内装機能などの動向に起因しています。近年、自動車産業は不況に見舞われているが、自動車1台当たりのセンサ数の増加が主にベンダーを動かしています。市場ベンダーのほとんどは、自動車市場(内装と外装用途)の範囲を拡大しています。

- LiDARはADASの重要なコンポーネントであり、高効率のVCSELは、その小さなフットプリント、魅力的な価格設定、顕著な信頼性と性能により、ADAS LiDARに適しています。VCSELは、物体検出や距離マッピング用のLiDARシステム、ADASや自律走行用の車外センシング技術、車内・車外用の車載3Dセンシングなどに使用されています。

- LEVEL 4の自律性を実現するため、先進国と新興国地域のほとんどが新車へのADAS搭載を義務付けているか、または義務付ける予定であり、市場ベンダーに大きな成長機会をもたらすと期待されています。例えば、米国では新車の80~90%が少なくとも1つのADAS機能を搭載しています。

- National Safety Councilによると、2026年までに登録車の約71%にリアカメラが搭載され、60%にリア・パーキングセンサが搭載されるといいます。このようなADASの採用増加は、調査対象市場の成長を促進すると考えられます。

- 自動運転車や自律走行車の採用増加は、ADAS市場の主要な成長要因です。例えば、Intel社によると、世界の自動車販売台数は2030年に1億140万台以上に達すると予想されており、自律走行車は2030年までに自動車登録台数の約12%を占めると予想されています。

アジア太平洋は中国が市場を独占し、大幅な成長が見込まれる

- アジア太平洋では、自動車、医療、コンシューマーエレクトロニクス産業でのVCSEL採用が増加していることから、中国の大幅な成長が見込まれています。

- 中国は、世界でも有数の民生用電子機器メーカーです。同地域では製造業が急成長しており、さまざまな製造技術や通信技術が導入されています。

- 世界の多様な電子機器が中国に流入し続けているため、中国の半導体消費は他国よりも急速に伸びています。世界の著名な携帯電話会社上位5のうち3社がこの国に拠点を置いており、半導体を採用する絶好の機会となっています。

- 中国政府はまた、市民を追跡・モニタリングするための人工知能とセンサを動力源とするテクノオーソリティー国家の創設に取り組んでいます。このようなプログラムにより、同国で研究される市場の需要は拡大すると予想されます。中国政府の「メイド・イン・チャイナ2025」構想は、2030年までに半導体産業の生産高を3,050億米ドルに到達させ、国内需要の80%を満たすことを目指しています。このような動きは、同国市場の成長を後押しすると推定されます。

- 大手企業は市場での地位を強化するため、革新的な製品の開発に注力しています。例えば、VCSEL半導体研究開発のパイオニアであり、高速光通信用VCSELや3D深度カメラのメーカーであるBerxel Photonicsは、2023年9月、中国の深センで開催されたChina International Optoelectronic Expositionで、106Gbps VCSEL搭載800Gトランシーバのライブデモを発表しました。

- VCSELの成長に寄与するもう1つの要因は、電気自動車の採用が拡大していることです。例えば、ジェスチャーの認識、ドライバー・モニタリング、自律走行センサなどの用途に自動車産業でこの技術が使用されると予想されています。この地域では、自動車産業が素晴らしい速度で成長しています。この地域では、カスタム半導体やセンサの需要が増加しています。したがって、VCSEL技術はこの地域で重要な役割を果たすと期待されています。CAAMによると、2023年8月に中国で生産されたバッテリー電気自動車は58万9,000台で、そのうち乗用BEVが55万1,000台、ビジネスBEVが3万8,000台でした。同月、中国では25万4,000台のPHEVが生産され、そのうち25万3,000台が乗用PHEV、1,000台が商用PHEVでした。

- 中国政府は、自動車部品部門を含む自動車産業を基幹産業のひとつと位置づけています。政府は、中国の自動車生産台数が2025年までに3,500万台に達すると見込んでいます。このような事例は、市場が予測期間中に成長すると予想されることを示しています。

垂直共振器面発光レーザー産業概要

VCSEL市場は、Coherent Corporation、Lumentum Operations LLC、Vixar Inc(OSRAM AG)、Hamamatsu Photonics KK、TRUMPF Groupなどの大手企業が存在し、細分化されています。市場参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年10月-データ通信用高速VCSELとフォトダイオードソリューションの世界参入企業であるトルンプフォトニックコンポーネンツ社と、スペインに本拠を置く高速光ネットワーキングソリューションのエキスパートであるKDPOFは、グラスゴーで開催された欧州光通信会議(ECOC)で、車載システム向け初の980nmマルチギガビット相互接続システムを展示しました。

- 2023年6月-世界有数の光ソリューションサプライヤーであるAMS Osramは、垂直共振器面発光レーザー(VCSEL)のTARA2,000-AUT-SAFEファミリーの発売を発表しました。車載用車室内センシング用赤外レーザーモジュールのポートフォリオを強化しながら、信頼性が高く、より堅牢なアイセーフティ機能を記載しています。新型TARA2,000-AUT-SAFEは、ピーク波長940nmで厳密に制御された赤外光ビームを生成します。ドライバー・モニタリング、ジェスチャー・センシング、車内モニタリングなど、既存のTARA2,000-AUTシリーズと同様の用途シナリオに対応します。このコンパクトなモジュールには、amsのオスラムVCSELチップとマイクロレンズアレイ(MLA)が搭載されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 特許情勢

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第4章 市場力学

- 市場促進要因

- データセンターにおけるVCSEL採用の増加

- スマートフォンにおける3Dセンシング用途の需要拡大

- 市場抑制要因

- InPベースVCSELの普及率の低さとデータ伝送範囲の狭さ

第5章 材料動向分析

- 窒化ガリウム

- ガリウムヒ素

- その他の材料タイプ

第6章 市場セグメンテーション

- 波長別

- 赤色(650~750 nm)

- 近赤外線(750~1,400 nm)

- 短波長赤外線(1,400~3,000 nm)

- ダイサイズ別

- 0.02~0.06 mm2

- 0.06~0.4 mm2

- 0.4~1.3 mm2

- 10~75 mm2

- エンドユーザー産業別

- テレコム

- モバイルとコンシューマー

- 自動車

- 医療

- 産業

- 航空宇宙・防衛

- 用途別

- データコム

- 光学式マウス

- 顔認識と深度カメラ

- ジェスチャー認識

- レーザーオートフォーカス

- 近接センサ

- 虹彩スキャン

- 医療用

- ADAS LiDAR

- 産業用途

- その他

- 地域別

- 北米

- 欧州

- 台湾

- 中国

- 韓国

- 日本

- その他

第7章 競合情勢

- 企業プロファイル

- Coherent Corporation

- Lumentum Operations LLC

- Vixar Inc(OSRAM AG)

- Hamamatsu Photonics KK

- TRUMPF Group

- ams OSRAM AG

- HLJ Technology Co. Ltd

- Teledyne FLIR Systems Inc.

- Vertilite Inc.

- Leanardo Electronics US(Lasertel)

- Broadcom Inc.

- Santec Corporation

第8章 投資分析

第9章 市場機会と今後の動向

The Vertical Cavity Surface Emitting Laser Market size is estimated at USD 2.49 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 18.6% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 5.14 billion units in 2025 to 16.06 billion units by 2030, at a CAGR of 25.60% during the forecast period (2025-2030).

The vertical-cavity surface-emitting laser (VCSEL) is a semiconductor whose laser is emitted perpendicular to the top surface. It differs from an edge-fired laser, which emits the laser from the edge. VCSELs offer precision, high efficiency, reliability, and high speed with a cost-effective solution, and these are the most promising new technological developments in laser physics. VCSELs offer various advantages, such as lower power consumption, beam quality, modulation speeds, and manufacturing costs.

Key Highlights

- The VCSEL market is anticipated to witness robust growth during the forecast period owing to several factors like increasing requirements for transmitting data over long distances with high speed and efficiency, rising demand for these lasers in automotive LiDAR applications, and industrial applications. In August 2023, Innoviz Technologies and the BMW Group are expanding their collaboration by starting a B-sample development phase on a new generation of LiDAR.

- Over the past few years, optical interconnect infrastructures in the data centers have advanced to the next-generation 400 Gbit/s data rate from 100 Gbit/s. This is primarily driven by the ever-increasing data traffic in data centers due to the rapid market growth of emerging technologies, such as AI, VR/AR, and the Internet of Things (IoT), and the introduction of 5G mobile network systems.

- The increasing adoption of VCSELs in smartphones by smartphone manufacturers for 3D sensing or proximity sensing applications is one of the primary factors driving the market growth. The growth of 3D sensing was propelled by the introduction of face ID modules in iPhones. Since then, there have been significant developments in 3D sensing. Slowly, there was a transition of 3D sensing from front-side face ID modules to the rear side for photography applications.

- InP-based VCSELs are typically preferred for applications such as optical communication due to their low dispersion and low fiber loss. However, InP-based VSCELs cannot provide large refractive index contrast DBR mirrors, owing to the high reflectivity and low penetration depth. The effective cavity length limits the tuning range and the confinement factor.

- The COVID-19 pandemic had a remarkable impact on the market studied, with several end-user industries that deploy VCSEL facing several difficulties. The industries were stuck with nationwide lockdowns, which brought them to a standstill, but after Q2 of 2020, they gradually started their operation. Since the raw materials are bought in China, the sourcing has been affected by the tariffs imposed by the United States.

- Geopolitical tensions and conflicts worldwide drive the demand for military spending. According to the Stockholm International Peace Research Institute (SIPRI), the United States led the ranking of countries with the highest military expenditure in 2022, with USD 877 billion dedicated to the military. That constituted nearly 40 percent of the total military spending worldwide that year, which amounted to USD 2.2 trillion. This amounted to 3.5 percent of the US gross domestic product.

Vertical Cavity Surface Emitting Laser Market Trends

ADAS and LiDAR to be the Fastest-growing Application

- The automotive industry is one of the major emerging markets for the VCSEL manufacturers, owing to trends like autonomous vehicles and high-end interior features in vehicles. Although the automotive industry has been witnessing a recession in recent years, the growing number of sensors per vehicle is mainly motivating the market vendors. Most of the market vendors are expanding their scope for the automotive market (interior and exterior applications).

- LiDAR is a critical component of ADAS, and highly efficient VCSELs, with their tiny footprint, attractive pricing, and remarkable reliability and performance, are making them suitable for ADAS LIDAR. VCSELs are used in LiDAR systems for object detection and mapping distances, exterior sensing technologies for ADAS and autonomous driving, and automotive 3D sensing for in-cabin and outside the vehicle, among others.

- In order to achieve LEVEL 4 autonomy, most of the developed and developing regions have mandated or are planning to mandate ADAS in new vehicles, which is expected to create massive growth opportunities for the market vendors. For instance, 80-90% of new vehicles in the United States have at least one ADAS feature.

- According to the National Safety Council, by 2026, approximately 71% of registered vehicles will be equipped with rear cameras, while 60% will have rear parking sensors. Such increasing adoption of ADAS would aid the growth of the market studied.

- The increasing adoption of self-driving or autonomous vehicles is a primary growth factor for the ADAS market. For instance, according to Intel, global car sales are expected to reach over 101.4 million units in 2030, and autonomous vehicles are expected to account for about 12% of car registrations by 2030.

Asia-Pacific Expected to Witness Significant Growth with China Dominating the Market

- China is expected to grow substantially in the Asia-Pacific region due to the increasing adoption of VCSEL in the automotive, healthcare, and consumer electronics industries.

- China is one of the prominent consumer electronics producers across the world. The manufacturing industry is rapidly growing in the region and is witnessing the deployment of various manufacturing and telecommunications technologies, which is expected to aid in the market's growth.

- Due to the continued flow of global, diversified electronics equipment into China, the consumption of semiconductors in China is growing faster than in others. Three of the world's top five most prominent mobile phone companies are based in this country, which presents enormous opportunities for adopting semiconductors.

- The Chinese government is also working to create a techno-authoritarian state powered by artificial intelligence and sensors to track and monitor its citizens. The demand for market studied in the country is expected to grow with such programs. The Chinese government's "Made in China 2025" initiative aims to make its semiconductor industry reach USD 305 billion in output by 2030 and meet 80% of domestic demand. Such instances are estimated to boost the market's growth in the country.

- Major players focus on developing innovative products to strengthen their market positions. For instance, in September 2023, Berxel Photonics, a pioneer in VCSEL semiconductor R&D and manufacturer of high-speed optical communications VCSELs and 3D depth cameras, announced a live demo of its 106 Gbps VCSEL-powered 800G transceiver in China International Optoelectronic Exposition in Shenzhen, China.

- Another factor contributing to the growth of VCSEL is the growing adoption of electric vehicles. For example, this technology is anticipated to be used in the vehicle industry for applications like recognition of gestures, driver monitoring, and autonomous driving sensors. In this region, the auto industry is growing at an excellent rate. The demand for custom semiconductors and sensors is increasing in the area. Therefore, VCSEL technology is expected to play a significant role in the region. As per CAAM, 589,000 battery-electric vehicles were made in China in August 2023, with 551,000 passenger BEVs and 38,000 business BEVs. In the same month, 254,000 PHEVs were produced in China, of which 253,000 were passenger PHEVs, and 1,000 were commercial PHEVs.

- The Chinese government views its automotive industry, including the auto parts sector, as one of its pillar industries. The government expects China's automobile output to reach 35 million units by 2025. Such instances show that the market is anticipated to grow over the forecast period.

Vertical Cavity Surface Emitting Laser Industry Overview

The VCSEL market is fragmented with the presence of major players like Coherent Corporation, Lumentum Operations LLC, Vixar Inc (OSRAM AG), Hamamatsu Photonics KK, and TRUMPF Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - TRUMPF Photonic Components, a global player in high-speed VCSEL and photodiode solutions for data communication, and KDPOF, an expert in high-speed optical networking solutions based in Spain, showcased its first 980nm multi-gigabit interconnect system for automotive systems at the European Conference for Optical Communication (ECOC), held in Glasgow.

- June 2023 - AMS Osram, the world's significant supplier of optical solutions, announced the launch of the TARA2000-AUT-SAFE family of vertical cavity surface emitting lasers (VCSELs), Reliable and more robust eye safety features while enhancing the portfolio of infrared laser modules for automotive in-cabin sensing. The new TARA2000-AUT-SAFE generates a tightly controlled beam of infrared light at a peak wavelength of 940nm. It suits the same application scenarios as the existing TARA2000-AUT series: driver monitoring, gesture sensing, and in-cabin monitoring. The compact module contains an ams Osram VCSEL chip and a microlens array (MLA).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Overview

- 3.2 Industry Attractiveness - Porter's Five Forces Analysis

- 3.2.1 Bargaining Power of Suppliers

- 3.2.2 Bargaining Power of Buyers/Consumers

- 3.2.3 Threat of New Entrants

- 3.2.4 Threat of Substitute Products and Services

- 3.2.5 Intensity of Competitive Rivalry

- 3.3 Patent Landscape

- 3.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Adoption of VCSEL in Data Centers

- 4.1.2 Growing Demand for 3D Sensing Applications in Smartphones

- 4.2 Market Restraints

- 4.2.1 Low Penetration of InP-based VCSELs and Limited Data Transmission Range

5 MATERIAL TREND ANALYSIS

- 5.1 Gallium Nitride

- 5.2 Gallium Arsenide

- 5.3 Other Material Types

6 MARKET SEGMENTATION

- 6.1 By Wavelength

- 6.1.1 Red (650-750 nm)

- 6.1.2 Near-infrared (750-1400 nm)

- 6.1.3 Shortwave-infrared (1400-3000 nm)

- 6.2 By Die-size

- 6.2.1 0.02 - 0.06 mm2

- 6.2.2 0.06 - 0.4 mm2

- 6.2.3 0.4 - 1.3 mm2

- 6.2.4 10 - 75 mm2

- 6.3 By End-user Industry

- 6.3.1 Telecom

- 6.3.2 Mobile and Consumer

- 6.3.3 Automotive

- 6.3.4 Medical

- 6.3.5 Industrial

- 6.3.6 Aerospace and Defense

- 6.4 By Application

- 6.4.1 Datacom

- 6.4.2 Optical Mouse

- 6.4.3 Facial Recognition and Depth Camera

- 6.4.4 Gesture Recognition

- 6.4.5 Laser Autofocus

- 6.4.6 Proximity sensing

- 6.4.7 Iris Scan

- 6.4.8 Medical

- 6.4.9 ADAS LiDAR

- 6.4.10 Industrial Applications

- 6.4.11 Other Applications

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Taiwan

- 6.5.4 China

- 6.5.5 South Korea

- 6.5.6 Japan

- 6.5.7 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Coherent Corporation

- 7.1.2 Lumentum Operations LLC

- 7.1.3 Vixar Inc (OSRAM AG)

- 7.1.4 Hamamatsu Photonics KK

- 7.1.5 TRUMPF Group

- 7.1.6 ams OSRAM AG

- 7.1.7 HLJ Technology Co. Ltd

- 7.1.8 Teledyne FLIR Systems Inc.

- 7.1.9 Vertilite Inc.

- 7.1.10 Leanardo Electronics US (Lasertel)

- 7.1.11 Broadcom Inc.

- 7.1.12 Santec Corporation