航空機スラストリバーサーアクチュエータシステム:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Aircraft Thrust Reverser Actuation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 98 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683192

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

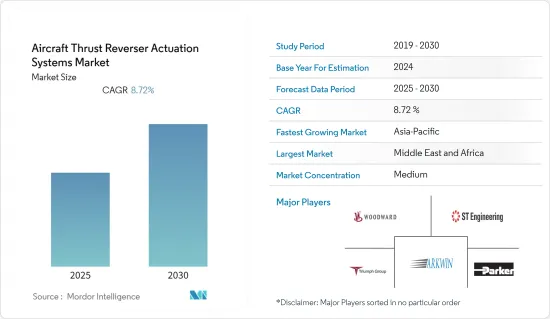

航空機スラストリバーサーアクチュエータシステム市場は予測期間中にCAGR 8.72%を記録する見込みです。

主なハイライト

- COVID-19パンデミックは航空機スラストリバーサーアクチュエータシステム市場にマイナスの影響を与えました。パンデミックの発生により、ウイルスの蔓延を抑えるために世界各地で飛行禁止や閉鎖措置がとられました。閉鎖措置の発動により、需要と供給の両面で世界の混乱が生じた。しかし、ロックダウンの制限が解除された後は、航空需要が急増し、航空会社は機材の拡大や近代化の取り組みを行うようになりました。

- 航空機スラストリバーサーアクチュエータ市場に影響を与えるサプライチェーンのボトルネックはまだあるもの、同市場はこうしたシステムに対するOEMやアフターマーケットの需要に連動して成長すると予想されます。さらに、新たな排ガス規制の状況も、電子スラスト・アクチュエーター・システムへの投資を促進すると予想されます。現在、ジェットエンジンで使用されている推力反転システムは、ターゲットシステム、クラムシェルシステム、コールドストリームシステムの3種類が主流です。

- 積層造形技術の採用が拡大していることも、航空機推力作動システムの重要なコンポーネントの全体的な生産コストとメンテナンスコストを下げるため、市場に大きな影響を与えると予想されます。

航空機スラストリバーサーアクチュエータシステム市場の動向

ビジネスジェット機セグメントが予測期間中に大きな成長を遂げる

- 富裕層(HNWI)の増加が、過去10年間のビジネス航空機の成長の引き金となりました。また、フラクショナル・オーナーシップ・プログラムの登場やエア・チャーター・サービスへの需要の高まりも、ビジネスジェット機に対する需要の増加をもたらしています。

- さらに、航空チャーター便運航の収益性が高まっていることも、航空会社のチャーター便運航への魅力を高めると同時に、ビジネス航空分野への新規参入を促しています。例えば、2023年1月、ノルウェーの航空会社Flyrは、2023年5月からチャーター便の運航を開始する計画を発表しました。

- 市場で著名なビジネスジェット機には、ボーイング・ビジネスジェットB777X、ボーイングB787ドリームライナー、ボンバルディア・世界7500、セスナ・サイテーション・ロンジチュード、セスナ・サイテーション・ソブリン、ダッソー・フラコン8X、ダッソー・ファルコン7X、エンブラエル・フェノム300F、ガルフストリームG500、ガルフストリームG650などがあります。

- ガルフストリームG550とガルフストリームG500は、サフランSAが提供するターゲット型スラストリバーサーを搭載し、ロールス・ロイスplcのBR710エンジンを2基搭載しています。両機とも油圧式スラストリバーサー作動システムを備えています。Woodward Inc.は、ガルフストリームG450およびガルフストリームG500/550用のスラスト・リバーサー・アクチュエーション・システムを提供しています。一方、ファルコン7Xは3基のエンジンを搭載しているが、スラストリバーサーは中央のエンジンに装備されており、油圧作動システムを備えています。ファルコン7Xは2007年に就航し、2022年12月現在、40カ国以上で運航されています。

- さらに、スミス・エアロスペース社は当初、油圧式スラストリバーサーの作動システムを提供することになりました。ボンバルディア社は2022年8月、エア・コーポレートSRL社からチャーター便用のビジネスジェット機「チャレンジャー3500」を受注したと発表しました。これは、同機の発売以来、欧州地域からの初の受注となります。

- このように、富裕層の可処分所得の増加、フラクショナル・オーナーシップ・プログラムの普及、エア・チャーター・サービスへの需要の高まりは、市場に明るい展望をもたらし、予測期間中に市場を成長へと導くと予想されます。

アジア太平洋地域が予測期間中に急成長を遂げる

- 中国の航空旅客輸送量は過去10年間で数倍に増加しました。中国は米国を抜き、最大の航空市場になるとさえ予想されています。空港インフラの絶え間ない開発と航空ネットワークの拡大が、新路線就航のための新型機需要を牽引しています。

- 他方、インドでも国内航空旅客数の増加が予測され、航空各社が野心的な拡張計画を採用し、予測期間中にインド航空セクターの急回復が見込まれます。航空会社による新たな航空機発注は、同国に高成長のシナリオをもたらします。

- 2022年上半期、日本の航空業界は他の国内市場と同様に回復を続けたが、世界の回復はこの地域の他の国々に比べて大きく遅れました。その他アジア太平洋地域の主要市場には、オーストラリア、韓国、シンガポール、マレーシア、タイ、インドネシアなどが含まれます。良好な経済状況と政府の支援は、この地域における航空機スラストリバーサーアクチュエータ・システムの手頃な価格と需要を支える主な要因の一部です。

航空機スラストリバーサーアクチュエータシステム業界の概要

民間航空機リース市場の有力企業には、Triumph Group、Woodward Inc、Parker Hannifin Corporation、Singapore Technologies Engineering Ltd.、Arkwin Industries Inc.などがあります。これらの企業は、さまざまな地域でプレゼンスを拡大し、システム・インテグレーターや航空機OEM、MROにコスト効率の高い生産と供給を可能にする柔軟な航空機スラストリバーサーアクチュエータ・システム製造オプションを提供しています。市場の魅力は、世界の航空産業の回復に伴って市場が成長し、OEMとMROの両方のチャネルからこのようなシステムの需要が発生するため、高まると予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム別

- 商用航空機

- 軍用機

- ビジネスジェット機

- メカニズム別

- 油圧式

- 電気式

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Woodward Inc.

- Arkwin Industries Inc.(TransDigm Group Inc.)

- Honeywell International Inc.

- Safran SA

- Collins Aerospace(Raytheon Technologies Corporation)

- Triumph Group

- Parker Hannifin Corporation

- Diakont

- Singapore Technologies Engineering Ltd.

- The NORDAM Group LLC

- Spirit AeroSystems Inc.

第7章 市場機会と今後の動向

目次

The Aircraft Thrust Reverser Actuation Systems Market is expected to register a CAGR of 8.72% during the forecast period.

Key Highlights

- The COVID-19 pandemic had a negative impact on the aircraft thrust reverser actuation systems market. The onset of the pandemic resulted in the grounding of flights as well as lockdowns being imposed worldwide to curb the spread of the virus. The imposition of the lockdown created a global disruption both in terms of supply and demand. However, post the removal of lockdown restrictions, air travel demand has surged, encouraging airlines to undertake fleet expansion and modernization initiatives.

- Though there are still some supply chain bottlenecks that affect the aircraft thrust reverser actuation systems market, the market is expected to grow in tandem with the OEM and aftermarket demand for such systems. Furthermore, the emerging emission regulation landscape is also anticipated to drive investments in electronic thrust actuation systems. Currently, the target, clam-shell, and cold stream systems are the three most prevalent types of thrust reversal systems that are used in jet engines.

- The growing adoption of additive manufacturing technologies is also anticipated to have a profound effect on the market as it lowers the overall production and maintenance costs of critical components of aircraft thrust actuation systems.

Aircraft Thrust Reverser Actuation Systems Market Trends

Business Jets Segment to Witness Significant Growth During the Forecast Period

- An increase in the number of high-net-worth individuals (HNWIs) has triggered the growth of business aviation in the past decade. Besides, the advent of fractional ownership programs and the rising demand for air charter services have also resulted in higher demand for business jets.

- Moreover, the growing profitability of air charter operations has also attracted airlines to operate charter services while also encouraging the entry of new market players in the business aviation sector. For instance, in January 2023, the Norwegian carrier Flyr announced its plans to start operating charter services from May 2023.

- Some of the prominent business jets in the market are Boeing Business Jet B777X, Boeing B787 Dreamliner, Bombardier Global 7500, Cessna Citation Longitude, Cessna Citation Sovereign, Dassault Flacon 8X, Dassault Falcon 7X, Embraer Phenom 300F, Gulfstream G500, Gulfstream G650, etc.

- The Gulfstream G550 and Gulfstream G500 aircraft have target-type thrust reversers offered by Safran SA and are powered by two Rolls-Royce plc's BR710 engines. Both aircraft have hydraulic thrust reverser actuation systems. Woodward Inc. offers thrust reverser actuation systems for the Gulfstream G450 and Gulfstream G500/550 aircraft. On the other hand, the Falcon 7X has three engines, but the thrust reverser is provided in the center engine and has a hydraulic actuation system. Falcon 7X entered service in 2007, and as of December 2022, this airplane is being operated in over 40 countries.

- Furthermore, Smiths Aerospace was initially selected to provide the hydraulic thrust reverser actuation system. In August 2022, Bombardier Inc. announced receiving an order for the Challenger 3500 business jet from Air Corporate SRL for charter services. This is the first order for the aircraft from the Europe region since its launch.

- Thus, an increase in disposable resources of HNWIs, the proliferation of fractional ownership programs, and the rising demand for air charter services are anticipated to have a positive outlook on the market and drive the market towards growth during the forecast period.

Asia Pacific to Witness Rapid Growth During the Forecast Period

- The Chinese air passenger traffic has grown multi folds during the last decade. China is even envisioned to surpass the United States and become the largest aviation market. The constant development of airport infrastructure and expansion of air networks has driven the demand for new aircraft to service new routes.

- On the other hand, India is also projected to witness high domestic air passenger traffic, which would encourage airlines to adopt ambitious expansion plans resulting in a steep recovery of the Indian aviation sector during the forecast period. New aircraft orders from airlines render a high-growth scenario in the country.

- During the first half of 2022, the Japanese aviation industry continued to recover in line with other domestic markets, but global recovery lagged significantly compared to other countries in the region. The major markets in the rest of Asia-Pacific include Australia, South Korea, Singapore, Malaysia, Thailand, and Indonesia, among others. The positive economic conditions and the support of the government are some of the prime factors supporting the affordability and demand for aircraft thrust reverser actuation systems in the region.

Aircraft Thrust Reverser Actuation Systems Industry Overview

Some of the prominent players in the commercial aircraft leasing market are Triumph Group, Woodward Inc, Parker Hannifin Corporation, Singapore Technologies Engineering Ltd., and Arkwin Industries Inc., amongst others. These companies have expanded their presence in various regions to provide flexible aircraft thrust reverser actuation systems manufacturing options facilitating cost-effective production and supply of such systems to the system integrators or aircraft OEMs and MROs. The market attractiveness is envisioned to increase as the market's growth would be in line with the recovery of the global aviation industry, and demand for such systems would be generated from both OEM and MRO channels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Commercial Aircraft

- 5.1.2 Military Aircraft

- 5.1.3 Business Jets

- 5.2 Mechanism

- 5.2.1 Hydraulic

- 5.2.2 Electric

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Woodward Inc.

- 6.2.2 Arkwin Industries Inc. (TransDigm Group Inc.)

- 6.2.3 Honeywell International Inc.

- 6.2.4 Safran SA

- 6.2.5 Collins Aerospace (Raytheon Technologies Corporation)

- 6.2.6 Triumph Group

- 6.2.7 Parker Hannifin Corporation

- 6.2.8 Diakont

- 6.2.9 Singapore Technologies Engineering Ltd.

- 6.2.10 The NORDAM Group LLC

- 6.2.11 Spirit AeroSystems Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 98 Pages

- 納期

- 2~3営業日