戦略的鉱物材料市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Strategic Mineral Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683181

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

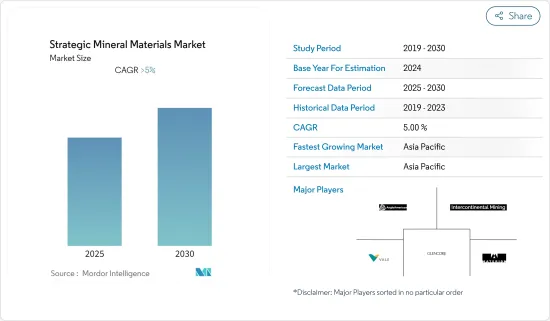

戦略的鉱物資源市場は予測期間中に5%を超えるCAGRで推移する見込み

主要ハイライト

- その反面、COVID-19パンデミックの影響と採掘作業に関する環境問題の高まりが市場成長の妨げになると予測されます。

- 様々な戦略的鉱物の用途ベースが増加していることは、将来的に好機として作用すると予測されます。

- アジア太平洋が市場を独占し、最大の消費国は中国、次いでインド、韓国、日本です。

戦略鉱物材料の市場動向

鉄鋼用途がニオブセグメントを支配する

- 一般に、鉄鋼の特性は、炭素、マンガン、リン、シリコン、合金元素、微細合金元素に関する化学組成と加工条件によって決まる。一般的に、鋼の強度を高める最も簡単な方法は、炭素含有量を高めることです。しかしこれは、溶接性、靭性、成形性など、他の必要な特性に悪影響を及ぼします。

- しかし、ニオブは炭素と親和性が高く、炭化物や炭窒化物を形成するため、鉄鋼やステンレスにフェロニオブという形で添加し、バランスの取れた特性を維持することが多いです。その結果、マイクロアロイ鋼製品として知られ、通常、約0.1重量%のニオブを含み、多くの場合、チタンやバナジウムと併用されます。

- HSLA鋼の場合、ニオブは合金全体の0.1%以下であることが多いが、結晶粒微細化剤としての役割は、鋼の強度、溶接性、延性、靭性を向上させ、大きな違いをもたらします。低級鋼の強度は結晶粒の微細化によって生み出され、高級鋼の強度は結晶粒の微細化と析出硬化の組み合わせによって生み出されます。

- 低級鋼の強度は結晶粒の微細化によって、高級鋼の強度は結晶粒の微細化と析出硬化の組み合わせによって生み出されます。ニオブとチタンは炭素や窒素のような介在元素を固定するため、これらの鋼は介在元素フリーと表現されます。

- しかし、最良の結果は通常、相乗的な利点を利用した微細合金の組み合わせによって達成されます。この例として、優れた表面品質が不可欠な「露出した」無機質鋼自動車部品にニオブとチタンを併用することが挙げられます。

- 最新のHSLA鋼のほとんどは、この「低炭素」カテゴリーに属します。世界的には、ニオブ製品の90%が鉄鋼業で使用されています。

- 高強度低合金(HSLA)鋼におけるニオブの最大の用途は、自動車、石油パイプライン、建設用です。HSLA鋼は、原子炉(ジルコニウムと合金化して炉心エレメントを作る)、風力タービン、鉄道線路、造船にも使われています。HSLA鋼は年間ニオブ生産量の約90%を消費しています。

- ニオブ鉄は鉄鋼業で最も広く使用されている製品であり、主にパイプライン、自動車、構造物、ステンレスの4セグメントで使用されています。パイプライン産業に関しては、中国での用途は世界の他の地域とほぼ同じであるが、自動車鋼材、構造鋼材、ステンレス材産業での用途では大きな違いがあります。

アジア太平洋が市場を独占

アジア太平洋が世界市場を独占しています。中国、インド、韓国、日本などの国々では、様々な用途で様々な鉱物の利用が加速しており、予測期間中にこの市場は大きな成長を遂げる可能性が高いです。アジア太平洋の電気・電子産業(半導体や通信を含む)は、インドや中国のような国々からの高い需要のおかげで、最近急速に成長しました。エレクトロニクス産業における技術革新の急速なペース、技術の進歩、研究開発活動により、最新のエレクトロニクス製品に対する需要が高いです。ハイエンド製品に特化した製造工場や開発センターの数も増加しています。航空宇宙は、戦略的鉱物材料のもう一つの主要なエンドユーザー産業です。航空機の需要は世界中で増加しており、航空宇宙産業は、製造時間の改善とコスト削減のために革新的なソリューションの導入を目指しています。したがって、前述の要因は、予測期間中に様々な用途から戦略的鉱物材料の使用を加速させています。しかし、2020年中も、経済パフォーマンスと需要は、この地域における現在のCOVID-19パンデミックの影響を受ける可能性が高いため、需要は影響を受ける可能性が高いです。

戦略的鉱物材料産業概要

世界の戦略的鉱物材料市場は、さまざまな鉱物を扱う数多くの企業が存在するため、その性質上細分化されています。市場の著名な企業には、Intercontinental Mining、Vale、Anglo American plc、Glencore、CBMM、Materion Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 様々なエンドユーザー産業からの需要拡大

- その他の促進要因

- 抑制要因

- COVID-19パンデミックの影響

- 採掘作業に対する環境問題の高まり

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 鉱物

- アンチモン

- 難燃剤

- 電池

- セラミックとガラス

- 触媒

- 合金

- バライト

- 石油・ガス

- その他の用途(塗料、化学製造、その他)

- ベリリウム

- エレクトロニクス

- 航空宇宙

- 自動車

- エネルギー

- その他

- コバルト

- 電池

- 超合金

- 超硬合金とダイヤモンド工具

- 触媒

- その他

- 蛍石

- 化学品

- 鉄鋼

- アルミニウム

- セメント

- その他

- ガリウム

- 集積回路

- レーザーダイオード

- 受光素子

- 太陽電池

- その他

- ゲルマニウム

- ファイバーオプティクス

- 赤外線光学部品

- 触媒

- 電気・ソーラー機器

- その他

- インジウム

- フラットパネルディスプレイ画面とタッチスクリーン

- 低融点合金とはんだ

- 半導体

- 透明熱反射板

- その他

- マンガン

- 鋳造合金

- 包装

- 輸送

- 建築

- その他

- ニオブ

- 鉄鋼

- 超合金

- 超電導マグネット

- コンデンサ

- ガラス

- その他

- 白金族元素

- 自己触媒

- 宝飾品

- 電気・電子

- 化学

- その他

- レアアース

- 触媒

- 電池

- 磁性合金

- 冶金

- その他

- タンタル

- エレクトロニクス

- 医療

- 航空宇宙

- 自動車

- その他

- アンチモン

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Anglo American plc

- CBMM

- Glencore

- Indium Corporation

- Intercontinental Mining

- Materion Corporation

- South32

- Vale

- WARRIOR GOLD INC.

第7章 市場機会と今後の動向

- 各種鉱物の用途拡大

目次

The Strategic Mineral Materials Market is expected to register a CAGR of greater than 5% during the forecast period.

Key Highlights

- On the flipside, the impact of COVID-19 pandemic and increasing environmental concerns regarding mining operations is expected to hinder the growth of the market.

- Increasing application base for various strategic minerals is projected to act as an opportunity in the future.

- Asia-Pacific dominated the market with the largest consumption coming from China, followed by India, South Korea, and Japan.

Strategic Mineral Materials Market Trends

Steel Application to Dominate the Niobium Segment

- In general, the properties of steel depend on its chemical composition concerning carbon, manganese, phosphorus, silicon, alloying and micro-alloying elements, and processing conditions. Generally, the easiest way to increase the strength of steel is improving its carbon content. But this adversely affects other necessary properties, such as weldability, toughness, and formability.

- However, niobium has a high affinity for carbon, forming carbides and carbon nitrides, therefore, it is often added to steel and stainless steel in the form of ferro-niobium to maintain a balanced package of properties, the carbon and niobium levels being carefully matched with processing conditions to achieve the desired properties. The result, known as a micro-alloyed steel product, typically contains around 0.1% niobium by weight, often in conjunction with titanium and vanadium.

- In HSLA steel niobium is often less than 0.1% of the total alloy, but its role as a grain refiner makes a significant difference by increasing strength, weldability, ductility, and toughness of the steel. Strength is generated by grain refinement for the lower grades and a combination of grain refinement and precipitation hardening for the higher grades.

- Strength is generated by grain refinement for the lower grades and a combination of grain refinement and precipitation hardening for the higher grades. These steels are described as interstitial-free, since niobium and titanium fix interstitial elements, like carbon and nitrogen.

- However, the best results are usually achieved with a combination of micro alloys that exploit synergistic benefits. An example of this is the use of niobium and titanium together in 'exposed' interstitial-free steel automobile parts where superior surface quality is essential.

- Most modern HSLA steels fall into this 'low carbon' category. Globally, 90% of the niobium products are used in the steel industry.

- The largest use for niobium in high-strength and low-alloy (HSLA) steel is for automobiles, oil pipelines, and construction. HSLA steels are also used in nuclear reactors (alloyed with zirconium to make core elements), wind turbines, railroad tracks, and in ship building. HSLA steels consume approximately 90% of the annual niobium production.

- Ferro niobium is the most widely used product in the steel industry, which is mainly applied in four fields of the pipeline, automobile, structure, and stainless steel. As for the pipeline industry, the application in China is in line with that in the other parts of the world, but the difference is significant in the application in automotive steel, structural steel, and stainless steel industries.

Asia-Pacific to Dominate the Market

Asia-Pacific dominated the global market. With accelerating usage of various minerals in different applications in countries, such as China, India, South Korea, and Japan, the market studied is likley to witness significant growth during the forecast period. The Asia-Pacific electrical and electronics industry (including semiconductors and telecommunications) grew rapidly in the recent past, owing to the high demand from countries, like India and China. There is a high demand for modern electronic products, due to the rapid pace of innovation, the advancement of technology, and R&D activities in the electronics industry. There is a growth in the number of manufacturing plants and development centers, focusing on high-end products. Aerospace is the another major end-user industry for strategic mineral materials. The demand for aircraft is increasing across the world, and the aerospace industry is aiming to introduce innovative solutions to improve the manufacturing time and save costs. Therefore, the aforementioned factors are accelerating the usage of strategic mineral materials from various applications during the forecast period. However, the demand is likely to be affected during 2020 as well, as economic performance and demand are likely to remain affected by the current COVID-19 pandemic in the region.

Strategic Mineral Materials Industry Overview

The global strategic mineral materials market is fragmented in nature with the presence of numerous players for different minerals. The prominent companies in the market includes Intercontinental Mining, Vale, Anglo American plc, Glencore, CBMM, and Materion Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Various End-user Industries

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Impact of COVID-19 Pandemic

- 4.2.2 Growing Environmental Concerns over Mining Operations

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Mineral

- 5.1.1 Antimony

- 5.1.1.1 Flame Retardants

- 5.1.1.2 Batteries

- 5.1.1.3 Ceramics and Glass

- 5.1.1.4 Catalyst

- 5.1.1.5 Alloys

- 5.1.2 Barite

- 5.1.2.1 Oil and Gas

- 5.1.2.2 Other Applications (paints, chemical manufacturing and others)

- 5.1.3 Beryllium

- 5.1.3.1 Electronics

- 5.1.3.2 Aerospace

- 5.1.3.3 Automotive

- 5.1.3.4 Energy

- 5.1.3.5 Other Applications

- 5.1.4 Cobalt

- 5.1.4.1 Batteries

- 5.1.4.2 Superalloys

- 5.1.4.3 Cemented Carbides and Diamond Tools

- 5.1.4.4 Catalysts

- 5.1.4.5 Other Applications

- 5.1.5 Fluorspar

- 5.1.5.1 Chemicals

- 5.1.5.2 Steel

- 5.1.5.3 Aluminum

- 5.1.5.4 Cement

- 5.1.5.5 Other Applications

- 5.1.6 Gallium

- 5.1.6.1 Integrated Circuits

- 5.1.6.2 Laser diodes

- 5.1.6.3 Photodetectors

- 5.1.6.4 Solar Cells

- 5.1.6.5 Other Applications

- 5.1.7 Germanium

- 5.1.7.1 Fiber Optics

- 5.1.7.2 Infrared Optics

- 5.1.7.3 Catalyst

- 5.1.7.4 Electrical and Solar Equipment

- 5.1.7.5 Other Applications

- 5.1.8 Indium

- 5.1.8.1 Flat-Panel Display Screens and Touchscreens

- 5.1.8.2 Low Melting Alloys and Solders

- 5.1.8.3 Semiconductors

- 5.1.8.4 Transparent Heat Reflectors

- 5.1.8.5 Other Applications

- 5.1.9 Manganese

- 5.1.9.1 Casting Alloys

- 5.1.9.2 Packaging

- 5.1.9.3 Transportation

- 5.1.9.4 Construction

- 5.1.9.5 Other Applications

- 5.1.10 Niobium

- 5.1.10.1 Steel

- 5.1.10.2 Super Alloys

- 5.1.10.3 Superconducting Magnets

- 5.1.10.4 Capacitors

- 5.1.10.5 Glass

- 5.1.10.6 Other Applications

- 5.1.11 Platinum Group Elements

- 5.1.11.1 Autocatalyst

- 5.1.11.2 Jewelry

- 5.1.11.3 Electrical & Electronics

- 5.1.11.4 Chemical

- 5.1.11.5 Other Applications

- 5.1.12 Rare Earth Elements

- 5.1.12.1 Catalyst

- 5.1.12.2 Batteries

- 5.1.12.3 Magnetic Alloys

- 5.1.12.4 Metallurgy

- 5.1.12.5 Other Applications

- 5.1.13 Tantalum

- 5.1.13.1 Electronics

- 5.1.13.2 Medical

- 5.1.13.3 Aerospace

- 5.1.13.4 Automotive

- 5.1.13.5 Other Applications

- 5.1.1 Antimony

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations and Agreements

- 6.2 Market Share/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anglo American plc

- 6.4.2 CBMM

- 6.4.3 Glencore

- 6.4.4 Indium Corporation

- 6.4.5 Intercontinental Mining

- 6.4.6 Materion Corporation

- 6.4.7 South32

- 6.4.8 Vale

- 6.4.9 WARRIOR GOLD INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Application base of Various Minerals

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 250 Pages

- 納期

- 2~3営業日