|

市場調査レポート

商品コード

1683177

分子細胞遺伝学市場-市場シェア分析、産業動向・統計、成長予測(2025~2030年)Molecular Cytogenetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

価格

| 分子細胞遺伝学市場-市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

概要

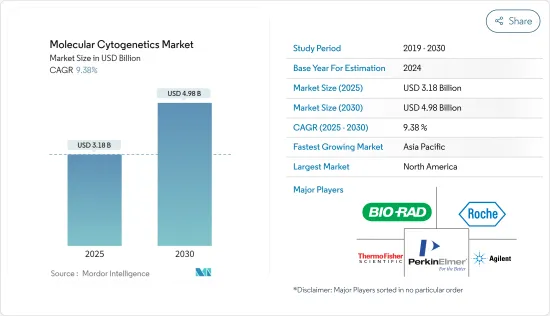

分子細胞遺伝学市場規模は2025年に31億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.38%で、2030年には49億8,000万米ドルに達すると予測されます。

主要ハイライト

- 分子細胞遺伝学市場は、染色体異常や遺伝性疾患を理解するための重要なツールを提供し、現代の診断学において極めて重要な役割を担っています。蛍光in situハイブリダイゼーション(FISH)や比較ゲノムハイブリダイゼーション(CGH)のような先進技術を活用することで、このセグメントは、がんや遺伝性疾患の診断に不可欠な染色体の構造的変化と数値的変化の両方を同定する上で大きな進歩を遂げました。これらの疾患の罹患率の増加が分子細胞遺伝学の需要を牽引し、個別化医療や標的治療における礎石として位置づけられています。

がん診断:重要な焦点

主要ハイライト

- プレシジョン・オンコロジーにおける重要な役割:分子細胞遺伝学はプレシジョン・オンコロジーに不可欠であり、がんの進行を促進する特定の遺伝子変異の同定を可能にします。FISHやCGHのような治療技術は、これらの変異を検出するために不可欠であり、従来の治療と比較してより効果的で副作用の少ない標的療法の開発を促進します。この精度は、患者の転帰を向上させるだけでなく、効果のない治療を最小限に抑えることで、医療費全体を削減します。

- 染色体マイクロアレイ分析(CMA)の進歩:染色体マイクロアレイ分析は、他の手法では見落とされる可能性のある微細な染色体異常を検出することができるため、がん診断において支持を集めています。CMAは、がんに関連するコピー数多型(CNV)やその他の構造的ゲノム変化の同定に特に有用です。この技術が進歩するにつれて、がん診断における標準的なツールとなり、分子細胞遺伝学市場をさらに押し上げると予想されます。

- 次世代シーケンサー(NGS)との統合:分子細胞遺伝学と次世代シーケンサー(NGS)の統合は、がん診断における新たな機会を生み出しています。NGSは全ゲノムにわたる遺伝子変異の包括的な分析を可能にし、がんの分子基盤のより詳細な理解を記載しています。細胞遺伝学とNGSのこの相乗効果は、がん診断の精度と範囲を高め、より個別化された治療戦略につながり、市場の主要な成長促進要因になると考えられます。

導入における課題:コストと認知度

主要ハイライト

- 高い治療費:分子細胞遺伝学市場における重要な課題の1つは、こうした先進的診断技術に伴うコストの高さです。FISHやCGHのような細胞遺伝学的分析に必要な装置、試薬、専門知識は高価であるため、中低所得国での導入が制限されています。これらのコストはしばしば患者に転嫁されるため、特に医療インフラが未発達な地域では、アクセスや購入のしやすさが制限されることになります。

- 新興市場における認知度の低さ:新興市場では最新の細胞遺伝学的診断技術に対する認識が低いことが大きな抑制要因となっています。北米や欧州のような先進地域では比較的高い普及率を示しているが、アジア太平洋、ラテンアメリカ、アフリカの医療従事者の多くは、これらの技術の利点や応用について十分に理解していないです。潜在的な利用者がこれらの技術の価値を認識していなかったり、なじみのないツールへの投資をためらっていたりするためです。

分子細胞遺伝学市場の動向

がんセグメントは予測期間中に力強い成長が見込まれる

- 分子細胞遺伝学市場は、世界のがん罹患率の増加を背景に、特にがんセグメントで大きな成長を遂げようとしています。例えば、Cancer Australiaは、2022年に162,163人の新規がん患者が発生すると推定しています。このようながん患者の急増は、FISHやCMAのような先進的な細胞遺伝学的検査に対する需要を煽るものであり、これらの検査は染色体異常を検出し、がんの正確な診断と治療に役立つ極めて重要なものです。

- 精密医療を後押しする技術の進歩:次世代シークエンシング(NGS)と従来の細胞遺伝学的手法の統合により、遺伝子分析の感度と特異度が大幅に向上しました。これらの進歩により、複雑な遺伝子変異や染色体異常を検出する能力が強化され、がん領域における精密医療に欠かせないものとなっています。がんセグメントの成長は、2023年に開催される「第10回がん遺伝子・細胞遺伝学的診断に関する国際ワークショップ」のような、がん診断の進歩に焦点を当てたワークショップやセミナーによってさらに支えられています。

- 研究開発投資の増加がイノベーションを促進がん細胞遺伝学セグメントは、バイオテクノロジー企業や製薬企業による大規模な研究開発投資の恩恵を受けており、先進的な細胞遺伝学的ツールや技術の開発につながっています。こうした投資は、がん研究、診断、治療への応用を拡大しています。詳細な遺伝子分析に大きく依存する精密医療の重視は、分子細胞遺伝学市場の境界を押し広げ、個別化がん治療をますます実現可能なものにしています。

- 政府の取り組みと戦略的提携:がん治療の改善を目的とした政府の取り組みと主要市場参入企業間の戦略的提携は、がん細胞遺伝学セグメントの成長に寄与しています。例えば、Pfizer社の2022年度医療助成金は、カナダにおける成人急性骨髄性白血病(AML)患者の細胞遺伝学的検査と治療指導の改善に焦点を当てたものです。このようなイニシアチブは、細胞遺伝学的診断と個別化治療の利用可能性と有効性を高めることにより、市場成長をさらに促進すると予想されます。

北米が分子細胞遺伝学市場で大きなシェアを占める見込み

- 強力な医療インフラと規制支援:北米は強固な医療インフラと確立された規制の枠組みにより、分子細胞遺伝学市場を独占すると予想されます。米国は先進的な細胞遺伝学技術の導入でリードしており、遺伝子研究や診断への投資が活発です。この地域は精密医療に注力しており、正確な遺伝子分析と標的治療開発に不可欠なFISH、核型分析、CGHの採用を加速させています。

- 遺伝性疾患とがんの高い有病率:北米におけるがんと遺伝性疾患の罹患率の上昇は、市場成長の重要な促進要因です。カナダがん協会によると、カナダでは2022年に233,900人の新規がん患者が発生すると予想されています。乳がん、前立腺がん、大腸がんなどのがんの有病率の高さが、特にがんや出生前診断における分子細胞遺伝学の需要を高めています。この動向は、インディアナ州の医療保険制度が小児の遺伝子異常診断にCMAを含めるなど、政府の施策によってさらに後押しされています。

- 産業との協力と研究資金:北米では学術機関とバイオテクノロジー企業との共同研究が分子細胞遺伝学の革新を促進しています。このような共同研究は、腫瘍学、生殖医療、個別化医療を含む様々なセグメントで細胞遺伝学的技術の応用を拡大しています。この地域はまた、Pfizerによる2022年の助成金のような、カナダにおける患者の転帰、特にAMLの細胞遺伝学的検査を改善するための独自のイニシアチブを支援する研究資金の増加からも利益を得ています。

- 市場シェアとイノベーションにおける優位性:プレシジョン・メディシン(精密医療)における北米のリーダーシップは、先進的医療インフラと強力な研究開発能力と相まって、世界の分子細胞遺伝学市場で大きなシェアを確保しています。同地域の技術革新へのコミットメントと、早期かつ正確な診断における細胞遺伝学的分析の需要の高まりは、予測期間を通じて同地域の優位性を維持すると予想されます。個別化されたがん診断と治療の必要性が高まり続ける中、北米は分子細胞遺伝学産業の最前線であり続ける可能性が高いです。

分子細胞遺伝学産業概要

- 適度に統合された市場:分子細胞遺伝学市場は、世界コングロマリットと専門企業が混在する、中程度の連結構造を特徴とします。既存のコングロマリットと高度に専門化された企業の両方を含む世界参入企業がこの市場を独占しており、幅広い製品とサービスを提供しています。市場競争は激しいが、少数の主要企業が優位に立つことで、適度な統合環境が保たれ、安定性を維持しながら競争が可能になっています。

- 主要市場リーダー分子細胞遺伝学市場の主要企業には、Agilent Technologies、Bio-Rad Laboratories、F. Hoffmann-La Roche、PerkinElmer、Thermo Fisher Scientificなどがあります。これらの企業は、強力な世界事業と包括的な製品ポートフォリオを確立しており、大きな市場シェアを維持しています。これらの企業の強みは、技術革新能力、広範な販売網、戦略的買収による市場拡大にあります。また、分子細胞遺伝学的手法やアプリケーションの継続的な進歩により、リーダーとしての地位はさらに強固なものとなっています。

- 動向と成功戦略:分子細胞遺伝学市場の2つの大きな動向は、個別化医療に対する需要の高まりと、次世代シーケンス(NGS)などの先端技術の統合です。成功するためには、企業は技術力の拡大、研究開発への投資、戦略的パートナーシップの形成に注力し、製品ラインナップを充実させる必要があります。また、費用対効果の高いソリューションを提供し、世界の需要に対応できるよう事業規模を拡大できる企業が、この競争市場で成功する可能性が高いです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- がんと遺伝子疾患の有病率の増加

- がん治療における標的治療への注目の高まり

- 研究と臨床診断のための資金調達の増加

- 市場抑制要因

- 治療費の高騰

- 細胞遺伝学における新たな診断技術に関する認識不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース市場規模-米ドル)

- 製品別

- 器具

- キット・試薬

- ソフトウェア&サービス

- 技術別

- 蛍光in situハイブリダイゼーション

- 比較ゲノムハイブリダイゼーション

- 核型分析

- その他

- 用途別

- がん

- 遺伝子疾患

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- F.Hoffmann-La Roche Ltd.

- Illumina, Inc.

- Oxford Gene Technology

- PerkinElmer, Inc.

- Quest Diagnostics

- Thermo Fisher Scientific

- Empire Genomics

- Genial Genetic Solutions Ltd

- CytoTest Inc.

第7章 市場機会と今後の動向

目次

Product Code: 60441

The Molecular Cytogenetics Market size is estimated at USD 3.18 billion in 2025, and is expected to reach USD 4.98 billion by 2030, at a CAGR of 9.38% during the forecast period (2025-2030).

Key Highlights

- The molecular cytogenetics market stands as a pivotal force in contemporary diagnostics, offering critical tools for understanding chromosomal abnormalities and genetic disorders. Utilizing advanced techniques such as fluorescence in situ hybridization (FISH) and comparative genomic hybridization (CGH), the field has made significant strides in identifying both structural and numerical chromosomal changes, which are essential in diagnosing cancer and genetic disorders. The increasing incidence of these conditions is driving demand for molecular cytogenetics, positioning it as a cornerstone in personalized medicine and targeted therapies.

Cancer Diagnostics: A Pivotal Focus

Key Highlights

- Critical Role in Precision Oncology: Molecular cytogenetics is integral to precision oncology, enabling the identification of specific genetic mutations that drive cancer progression. Techniques like FISH and CGH are essential for detecting these mutations, facilitating the development of targeted therapies that are more effective and have fewer side effects compared to traditional treatments. This precision not only enhances patient outcomes but also reduces overall healthcare costs by minimizing ineffective treatments.

- Advancements in Chromosomal Microarray Analysis (CMA): Chromosomal microarray analysis is gaining traction in cancer diagnostics due to its capability to detect submicroscopic chromosomal abnormalities that other techniques might miss. CMA is particularly valuable in identifying copy number variations (CNVs) and other structural genome changes associated with cancer. As the technology advances, it is expected to become a standard tool in oncological diagnostics, further propelling the molecular cytogenetics market.

- Integration with Next-Generation Sequencing (NGS): The integration of molecular cytogenetics with next-generation sequencing (NGS) is creating new opportunities in cancer diagnostics. NGS enables comprehensive analysis of genetic mutations across the entire genome, providing a more detailed understanding of the molecular basis of cancer. This synergy between cytogenetics and NGS enhances the accuracy and scope of cancer diagnostics, leading to more personalized treatment strategies, and is likely to be a key growth driver in the market.

Challenges in Adoption: Cost and Awareness

Key Highlights

- High Cost of Treatment: One significant challenge in the molecular cytogenetics market is the high cost associated with these advanced diagnostic techniques. The equipment, reagents, and expertise required for cytogenetic analyses like FISH and CGH are expensive, limiting adoption in low- and middle-income countries. These costs are often passed on to patients, resulting in limited accessibility and affordability, particularly in regions with underdeveloped healthcare infrastructures.

- Limited Awareness in Emerging Markets: A major restraint is the lack of awareness about the latest cytogenetic diagnostic technologies in emerging markets. While adoption is relatively high in developed regions like North America and Europe, many healthcare providers in Asia-Pacific, Latin America, and Africa are not fully aware of the benefits and applications of these techniques. This lack of awareness hampers market penetration, as potential users may not recognize the value of these technologies or may be hesitant to invest in unfamiliar tools.

Molecular Cytogenetics Market Trends

Cancer Segment Expected to Show Robust Growth Over the Forecast Period

- The molecular cytogenetics market is poised for significant growth, particularly in the cancer segment, driven by the increasing prevalence of cancer worldwide. For instance, Cancer Australia estimated 162,163 new cancer cases in 2022. This surge in cancer cases fuels demand for advanced cytogenetic tests like FISH and CMA, which are crucial for detecting chromosomal abnormalities and aiding in accurate cancer diagnosis and treatment.

- Technological Advancements Boosting Precision Medicine: The integration of next-generation sequencing (NGS) with traditional cytogenetic methods has significantly improved the sensitivity and specificity of genetic analyses. These advancements enhance the ability to detect complex genetic mutations and chromosomal abnormalities, crucial for precision medicine in oncology. The cancer segment's growth is further supported by workshops and seminars focusing on advancing cancer diagnostics, such as the '10th International Workshop on Cancer Genetic & Cytogenetic Diagnostics' in 2023.

- Increased R&D Investments Driving Innovation: The cancer cytogenetics segment benefits from substantial R&D investments by biotech and pharmaceutical companies, leading to the development of advanced cytogenetic tools and technologies. These investments are expanding applications in cancer research, diagnosis, and treatment. The emphasis on precision medicine, heavily reliant on detailed genetic analysis, pushes the boundaries of the molecular cytogenetics market, making personalized cancer treatment increasingly feasible.

- Government Initiatives and Strategic Alliances: Government initiatives aimed at improving cancer care, coupled with strategic alliances among key market players, contribute to the growth of the cancer cytogenetics segment. For instance, Pfizer's 2022 medical grant focused on improving cytogenetic testing and treatment guidance for adult Acute Myeloid Leukemia (AML) patients in Canada. Such initiatives are expected to further fuel market growth by enhancing the availability and efficacy of cytogenetic diagnostics and personalized therapies.

North America Expected to Hold a Significant Share in the Molecular Cytogenetics Market

- Strong Healthcare Infrastructure and Regulatory Support: North America is anticipated to dominate the molecular cytogenetics market, supported by its robust healthcare infrastructure and well-established regulatory framework. The U.S. leads in adopting advanced cytogenetic technologies, driven by high levels of investment in genetic research and diagnostics. The region's focus on precision medicine has accelerated the adoption of FISH, karyotyping, and CGH, essential for accurate genetic analysis and targeted therapy development.

- High Prevalence of Genetic Disorders and Cancer: The rising incidence of cancer and genetic disorders in North America is a significant driver of market growth. According to the Canadian Cancer Society, 233,900 new cancer cases were expected in Canada in 2022. The high prevalence of cancers such as breast, prostate, and colorectal cancer is increasing the demand for molecular cytogenetics, particularly in cancer and prenatal diagnostics. This trend is further supported by government policies, like the Indiana Health Coverage Program's inclusion of CMA for diagnosing genetic abnormalities in children.

- Industry Collaboration and Research Funding: Collaborations between academic institutions and biotech companies in North America are fostering innovation in molecular cytogenetics. These collaborations are expanding the application of cytogenetic technologies across various fields, including oncology, reproductive health, and personalized medicine. The region also benefits from increased research funding, such as Pfizer's 2022 grant supporting independent initiatives to improve patient outcomes in Canada, particularly in cytogenetic testing for AML.

- Dominance in Market Share and Innovation: North America's leadership in precision medicine, combined with its advanced healthcare infrastructure and strong R&D capabilities, ensures a significant share in the global molecular cytogenetics market. The region's commitment to innovation and the rising demand for cytogenetic analysis in early and accurate diagnostics are expected to sustain its dominance throughout the forecast period. As the need for personalized cancer diagnostics and treatments continues to grow, North America is likely to remain at the forefront of the molecular cytogenetics industry.

Molecular Cytogenetics Industry Overview

- Moderately Consolidated Market: The molecular cytogenetics market is characterized by a moderately consolidated structure, with a mix of global conglomerates and specialized companies. Global players, including both established conglomerates and highly specialized firms, dominate this market, offering a wide range of products and services. While the market is competitive, the dominance of a few key players ensures a moderately consolidated environment, allowing for competition while maintaining stability.

- Key Market Leaders: Leading companies in the molecular cytogenetics market include Agilent Technologies, Bio-Rad Laboratories, F. Hoffmann-La Roche, PerkinElmer, and Thermo Fisher Scientific. These companies have established strong global operations and comprehensive product portfolios, enabling them to maintain a significant market share. Their strengths lie in their innovation capabilities, extensive distribution networks, and strategic acquisitions that have expanded their market reach. Their leadership positions are reinforced by continuous advancements in molecular cytogenetic techniques and applications.

- Trends and Success Strategies: Two major trends in the molecular cytogenetics market are the increasing demand for personalized medicine and the integration of advanced technologies such as next-generation sequencing (NGS). To succeed, companies must focus on expanding technological capabilities, investing in research and development, and forming strategic partnerships to enhance their product offerings. Additionally, companies that can provide cost-effective solutions and scale operations to meet global demand are likely to succeed in this competitive market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Prevalence of Cancer and Genetic Disorders

- 4.2.2 Increasing Focus on Targeted Therapies for Cancer Treatment

- 4.2.3 Rise in Funding for Research and Clinical Diagnosis

- 4.3 Market Restraints

- 4.3.1 High Cost of Treatment

- 4.3.2 Lack of Awareness about the Emerging Diagnostic Technologies in Cytogenetics

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Products

- 5.1.1 Instruments

- 5.1.2 Kits & Reagents

- 5.1.3 Software & Services

- 5.2 By Technique

- 5.2.1 Fluorescence in Situ Hybridization

- 5.2.2 Comparative Genomic Hybridization

- 5.2.3 Karyotyping

- 5.2.4 Other Techniques

- 5.3 By Application

- 5.3.1 Cancer

- 5.3.2 Genetic Disorders

- 5.3.3 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Agilent Technologies, Inc.

- 6.1.3 Bio-Rad Laboratories, Inc.

- 6.1.4 F.Hoffmann-La Roche Ltd.

- 6.1.5 Illumina, Inc.

- 6.1.6 Oxford Gene Technology

- 6.1.7 PerkinElmer, Inc.

- 6.1.8 Quest Diagnostics

- 6.1.9 Thermo Fisher Scientific

- 6.1.10 Empire Genomics

- 6.1.11 Genial Genetic Solutions Ltd

- 6.1.12 CytoTest Inc.