|

市場調査レポート

商品コード

1906996

本質安全防爆機器(IS機器):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Intrinsically Safe Equipment (IS Equipment) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 本質安全防爆機器(IS機器):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

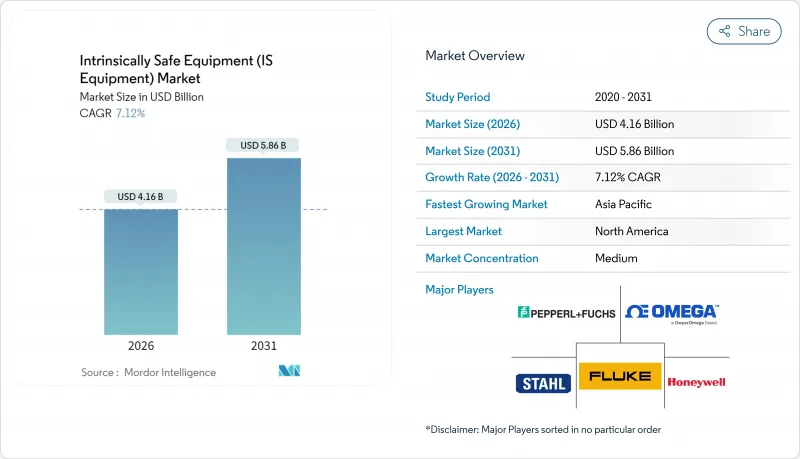

本質安全防爆機器(IS機器)市場は、2025年に38億8,000万米ドルと評価され、予測期間(2026-2031年)においてCAGR7.12%で成長し、2026年の41億6,000万米ドルから2031年までに58億6,000万米ドルに達すると推定されています。

この拡大は、重厚な防爆ハウジングから、規制順守とインダストリー4.0の接続性を融合したデジタル対応の本質安全アーキテクチャへの移行を反映しています。世界の基準の厳格化、鉱業およびプロセス産業の拡大、無線モジュールによる従来は採算が取れないと考えられていた改修プロジェクトの実現により、需要は加速しています。石油・ガス事業者は依然として主要顧客ですが、揮発性溶剤が生産ラインに導入されるにつれ、個別部品メーカーも認証取得済みの自動化技術を採用するようになりました。施設所有者が新システムの仕様を決定する際、ライフサイクルコスト、サプライチェーンの確実性、予知保全機能を考慮するため、認証とサイバーセキュリティの両方を習得した企業が最大の価値を獲得しています。

世界の本質安全防爆機器(IS機器)市場の動向と洞察

厳格化する世界の防爆安全規制

2024年1月に発行されたIEC 60079-11第7版では、173の技術的改正が導入されました。これには、より厳格な電池試験やグループIIC環境における触媒式センサーの使用禁止が含まれており、既存設備全体での改修投資を促す内容となっております。EN IEC 60079-11:2024は2024年12月に欧州連合官報に掲載され、2012年版は2027年12月までに調和解除されるため、義務的なアップグレードの明確な実施期間が設定されました。多国籍企業はATEXとIECExの書類対応に奔走していますが、技術的な整合性にもかかわらず、提出スケジュールの同期化はまだ実現していません。また、本規制は機器の範囲を超え、IEC 60079-14:2024に基づく現場配線も対象に拡大し、認証済み設置および再認証サービスの需要を喚起しています。これらの動きが相まって、事業者が非準拠資産を交換し、新規則に連動した長期保守契約を締結するにつれ、本質安全防爆機器市場は拡大しています。

インダストリー4.0が牽引する本質安全防爆センサー・計装機器の需要

デジタルトランスフォーメーションの進展に伴い、危険区域からのリアルタイムデータ収集ニーズが高まっており、本質安全防爆センサーが最前線の実現手段として位置づけられています。イーサネットAPL技術により、電力とデータを単一のツイストペアで最大1km伝送可能となり、プラント所有者は性能を損なうことなくゾーン1およびゾーン2にスマート計装を設置できます。無線ノードは配線コストを削減し、過酷な環境下でも複数年のバッテリー寿命を実現するSmartPowerモジュールが示すように、改修を簡素化します。地下鉱山では、これらのデバイスを採用してガスレベルや設備の状態を地上操作センターにストリーミングし、安全対策を一連の定期点検から継続的な監視へと移行しています。同じアーキテクチャが予知保全の基盤となっており、エッジアナリティクスが異常な振動を検出し、故障が発生する前にサービスニーズを通知します。これにより、施設所有者はコンプライアンスの保証と生産性の向上を同時に実現し、アジア太平洋地域および湾岸協力会議(GCC)諸国での購入が加速しています。

認証コストの高さと設計の複雑さ

ATEX認証の取得には、バリエーションごとに15,000~5万ユーロの費用がかかり、IECEx試験にはさらに20,000~6万米ドルが追加でかかるため、中小企業は競争から脱落せざるを得ません。第7版規則の変更により、追加のバッテリーストレス試験、火花点火試験、部品間隔試験が必要となり、多くの場合、設計の複数回の修正が必要となります。また、企業は、認証を維持するためにISO 9001およびQA監査を維持しなければならず、各製品ラインに定期的な間接費が組み込まれています。この費用は、社内の研究所と専任のコンプライアンスチームを擁する多国籍企業に競合を偏らせ、知的財産を集中させ、新規参入者を阻んでいます。新興市場のサプライヤーは、現地の研究所の処理能力が不足しているため、海外での試験を余儀なくされ、リードタイムが長くなり、予算が膨らむため、最も苦戦しています。

セグメント分析

2025年時点で、ゾーン1用途は本質安全防爆機器市場の38.15%を占め、保守作業中に爆発性雰囲気が発生する製油所や化学プラントにおけるその普遍性を裏付けています。予測保全を効率化するIoT対応新デバイスと従来配線を併用する運用形態により、ゾーン1向け支出は安定を維持しています。一方、ゾーン0は8.31%のCAGRを示しています。これは、可燃性ガスが継続的に存在する環境において、印刷型センサーや無線ハブが遂にリアルタイム監視を可能にしたためです。この増加傾向は、特にダウンタイムコストが機器のプレミアムを上回る海底油井や製薬用反応器において、隔離から積極的なリスク軽減への考え方の転換を示しています。ゾーン2は、低コストのコンプライアンスソリューションを必要とする荷役ドックや倉庫において依然として重要性を保ちます。一方、粉塵区域であるゾーン20~22は、自動化投資を進める食品・製薬施設で緩やかな需要拡大を見せています。サプライヤーは現在、ファームウェアの切り替えやヒューズの変更により複数のゾーン要件を満たすモジュラー基板を開発しており、これにより開発サイクルと在庫の圧縮が図られています。

ゾーン1認定の無線ゲートウェイは、単線イーサネット経由で安全区域のヒストリカルシステムと連携可能となりました。これにより本質安全防爆機器市場全体が、追加のケーブルトレイを必要とせず対応可能なエンドポイントを拡大しています。インテグレーターは、複雑なバリア計算にかかるエンジニア工数を削減できる点で、こうしたゲートウェイを高く評価しています。規格策定機関が多ガス・多粉塵エリア向けの指針を精緻化する中、ゾーン横断アーキテクチャは設計上のベストプラクティスとして定着し、現在の改修需要のピークが過ぎた後もゾーン0向け出荷が二桁成長を維持することが確実視されます。

ガス・蒸気危険に焦点を当てたクラス1システムは、2025年の収益の62.10%を占め、メタン検知、水素漏洩監視、LNG取扱によるセンサー更新需要を背景に、2031年までCAGR8.76%で拡大が見込まれます。事業者はパイプラインに光学式ガスイメージングカメラを後付けし、現場でAIベースの漏洩定量化を行う本質安全エッジボックスと連動させることで、修復時間を大幅に短縮しています。クラス2粉塵対策機器は、微細粉塵による発火リスクが従来見過ごされていたバイオマス発電所や積層造形工場で新たな購入先を見出しています。より多くの国がNFPA 652規格に準拠した規制を導入するにつれ、クラス2の本質安全防爆機器市場規模は緩やかな拡大が見込まれます。

クラス3の用途は繊維・木工分野などニッチな状態が続きますが、切断ラインの自動化進展に伴う浮遊繊維発生により需要は安定しています。供給業者はガスケット交換と粉塵フィルター追加によるクラス1設計の再利用を目指し、試験コスト削減を図っています。特にイーサネットAPLはクラス1に有利です。ガスグループは粉塵より高い許容電力が認められるため、スイッチ導入が簡素化されるためです。この互換性により、クラス1は新たな本質安全ネットワーク概念の試験場としての地位をさらに固め、後に粉塵・繊維分野へ波及していきます。

本質安全防爆機器レポートは、ゾーン別(ゾーン0、ゾーン20、ゾーン1など)、クラス別(クラス1、クラス2、クラス3)、製品タイプ別(センサー、検出器、スイッチなど)、エンドユーザー別(石油・ガス、鉱業、電力・公益事業、化学・石油化学、加工・製造など)、地域別に分類されています。市場予測は金額(米ドル)ベースで提供されます。

地域別分析

北米は2025年の収益の38.20%を占めております。これは、OSHAおよびNFPAの規制が、シェール盆地、メキシコ湾岸の製油所、地下鉱山における継続的な近代化を支えたためです。ハネウェル社の2024年の再編により、センシング技術と安全技術が単一のオートメーション部門に統合され、主要サプライヤーが安全性と生産性の両方のニーズを満たす統合されたハードウェア・ソフトウェア・スタックの提供を目指していることを示しています。米国事業者は、労働力不足への対策として、本質安全型LTE/5Gゲートウェイの導入においても主導的立場にあります。

アジア太平洋地域は2031年までに8.55%という最速のCAGRで推移する見込みです。これは中国における新規製油所建設、インドの石油化学拡張、オーストラリアの大規模銅・リチウム採掘が牽引しています。各国政府は輸出許可をIECまたはATEX準拠と連動させることで、現地メーカーを認証部品へ誘導しています。中国の自動化ベンダーは欧州の試験機関と協力し認証スケジュールを短縮することで、地域のサプライヤーエコシステムを拡大し、本質安全防爆機器市場を活性化させています。欧州ではATEX指令に基づく大規模な既存設備が維持されており、EN IEC 60079-11:2024規格が2027年までに義務化される見込みで、設備更新が加速するでしょう。ドイツは先進的な化学複合施設を主導し、排出目標達成のためにゾーン越境センサーネットワークを統合しています。英国とノルウェーは北海移行局が定める本質安全防爆とサイバーセキュリティの双方の規則を満たす海洋作業用機器への投資を継続しています。その他の地域では、中東の国営石油会社(NOC)が大規模ガスプロジェクトで本質安全型SCADAシステムの更新を展開する一方、ブラジルの砂糖・エタノール蒸留所では防爆モーターから本質安全型可変周波数駆動装置へ切り替え、エネルギー使用量を削減しています。こうした地域的な動向が相まって、世界の需要は堅調に推移しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 厳格な世界の防爆安全規制

- インダストリー4.0が牽引するISセンサーおよび計測機器への需要

- 石油・ガスおよび鉱業活動の拡大

- 防爆構造におけるコスト削減のため、Ex dからEx iアーキテクチャへの移行

- 遠隔・予知保全向け無線ISモジュールの成長

- 印刷された超低消費電力センサーアレイが改修市場を開拓

- 市場抑制要因

- 認証コストの高さと設計の複雑さ

- 地域ごとに異なる承認スケジュール

- IS規格認定済み電子部品の不足

- IS無線機器におけるサイバーセキュリティ対応コストの上昇

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ゾーン別

- ゾーン0

- ゾーン20

- ゾーン1

- ゾーン21

- ゾーン2

- ゾーン22

- クラス別

- クラス1

- クラス2

- クラス3

- 製品タイプ別

- センサー

- 検出器

- スイッチ

- 送信機

- アイソレーターおよびバリア

- LEDインジケーター

- その他のタイプ

- エンドユーザー別

- 石油・ガス

- 鉱業

- 電力・公益事業

- 化学および石油化学

- 加工・製造

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Pepperl+Fuchs SE

- Honeywell International Inc.

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Schneider Electric SE

- R. Stahl AG

- BARTEC Top Holding GmbH

- Emerson Electric Co.

- Rockwell Automation Inc.

- MSA Safety Inc.

- Dragerwerk AG and Co. KGaA

- OMEGA Engineering(Spectris plc)

- Fluke Corporation(Fortive)

- Banner Engineering Corp.

- Extronics Ltd.

- CorDEX Instruments Ltd.

- Bayco Products Inc.

- Kyland Technology Co. Ltd.

- Georgin SAS

- ABB Measurement and Analytics(added sub-brand)

- Teledyne FLIR LLC

- PATLITE Corp.

- G.M. International srl

- RAE Systems by Honeywell