アジア太平洋のブースターコンプレッサ:市場シェア分析、産業動向、成長予測(2025~2030年)

Asia-Pacific Booster Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645103

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

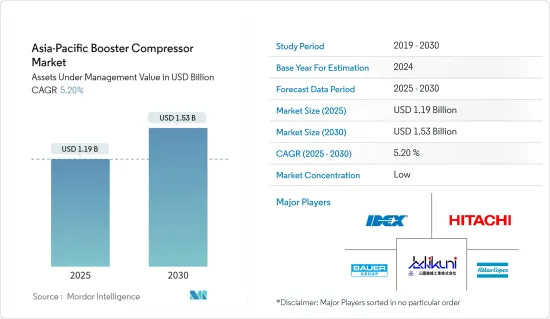

アジア太平洋のブースターコンプレッサ市場規模(運用資産額ベース)は、予測期間(2025~2030年)のCAGR 5.2%で、2025年の11億9,000万米ドルから2030年には15億3,000万米ドルに成長すると予測されます。

主要ハイライト

- 中期的には、地域全体の産業プロジェクトの増加や、様々な用途での天然ガス需要の高まりなど、様々な要因がブースターコンプレッサ市場の成長を促進しています。

- その一方で、この技術には高い設置コストがかかるため、新規設置にかかる高額な出費を避けるために既存の圧縮システムを利用することが、市場の成長を抑制する可能性もあります。

- 石炭発電所からガス発電所への急速な移行や、自動車でのガス使用の増加は、主要企業が今後数年間で市場での地位を維持するための有利な成長機会を提供すると予想されます。

- 中国は、エネルギー消費の増加により、予測期間中に市場を独占すると予想されます。

アジア太平洋のブースターコンプレッサ市場動向

石油・ガスセグメントが市場を独占する見込み

- ブースターコンプレッサは、石油・ガスのバリューチェーンにおける多くの用途で使用されており、上流・下流から中流までのすべてのセクターをカバーしています。最大の導入は、ガスパイプラインの通過システムにおける中流セグメントで観察されました。世界は現在、エネルギー需要のために天然ガスを大量消費する傾向にあり、ガス送達ネットワークの成長が加速しています。

- 2023年のアジア太平洋における天然ガス消費量は、2016年比34%増の905億立方フィート/日(bcf/日)と記録されました。この増加は主に、産業、商業、住宅部門において、よりクリーンなエネルギー生成方法への傾斜が強まったことによる。需給シナリオを均衡させるため、国をまたがる多くのガス・パイプラインが敷設されています。

- オーストラリアには、全国に張り巡らされたパイプライン網があります。同国のガス・パイプライン容量は、石油パイプラインと比較して圧倒的です。2023年には4万2,000kmを超える天然ガス送達パイプラインが敷設され、ガスの生産地から大小の都市近郊まで高圧で効率的に輸送されます。

- 同国は、既存のインフラを支え、ガス輸出能力と能力をさらに発展させるため、新たなパイプラインの開発に非常に熱心です。例えば、2023年8月、APAグループが西オーストラリア州に新設したノーザン・ゴールドフィールズ・インターコネクト(NGI)パイプラインが正式に開通しました。580kmの埋設パイプラインは、ダンピア市をバンバリー天然ガスパイプラインとゴールドフィールズ・ガスパイプラインに接続し、特にパース盆地における既存と新規の天然ガス生産地域とガス貯蔵インフラへのより良いアクセスを記載しています。

- マレーシアの天然ガスパイプライン網はアジアでも有数の規模を誇り、天然ガス配給システム(NGDS)の総延長は約2,468kmに及び、マレーシア国内のガス需要に対応しています。同国のパイプライン会社は、常に新しいプロジェクトを実施しています。

- 2023年8月、産業ガス会社のAir Productsは、ペナンのバヤンレパス自由工業地帯とバトゥカワン工業団地に2つの窒素プラントを建設、所有、運営すると発表しました。同社は両地域でパイプライン・ネットワークをさらに拡大する予定です。この追加能力とインフラへの戦略的投資は、マレーシア北部における同社の主導的地位と市場ニーズに対応する能力を強化することを意図したものです。

- このような開発は、アジア太平洋のブースターコンプレッサ市場の今後の成長を後押しすると予想されます。

中国が市場を独占する見込み

- 中国では高い都市化率によってエネルギー消費がエスカレートしており、発電プロジェクトや新しい燃料供給輸送システムが増加しています。天然ガスは、中国で最も普及している発電源のひとつです。

- BP Statistical Review of World Energyによると、2023年の同国の天然ガスベースの発電量は約297.8TWhでした。政府は、よりクリーンな発電源に対する厳しい規制を敷き、今後数年間、数多くのガスベースの発電所プロジェクトに拍車をかけた。

- 中国は世界最大の天然ガス輸入国であり、石炭火力発電所による発電を削減しようとしているため、エネルギー需要を満たすために天然ガスの需要が増加しています。例えば、2023年10月、GE Vernovaのガス発電事業とHarbin Electricは、SDIC(国家開発投資公司)の津能(舟山)ガス発電が中国浙江省の舟山群島に新設する複合火力発電所向けにGE 9HA.02ガスタービン2基を受注したと発表しました。

- 中国はアジア太平洋最大の原油・天然ガス生産国で、2023年の同地域の原油・天然ガス総生産量の約57.6%、33.8%をそれぞれ占めています。2023年の原油生産量は日量419万8,000バレルで、前年比2.1%増、2020年比7.6%増となりました。

- 2023年1月現在、中国では約1万7,800km(約219億米ドル相当)、インドでは1万4,300km(約207億米ドル相当)のガスパイプラインが建設中であり、これは地球の4分の3以上を一周する距離です。

- ブースターコンプレッサ市場は、中国における天然ガス需要の増加に対応するための、同国の新しいガス送達パイプライン計画によっても牽引されています。2022年10月、中国国家開発改革委員会(NDRC)は、四川省(中国南西部)のガス田と湖北省(中国中部)を結ぶ年間200億立方フィートの天然ガスパイプラインの建設を承認しました。工事は2022年12月に開始され、2024年末までに完成する予定です。このプロジェクトはパイプチャイナの西南パイプライン社が開発しました。

- こうした新興国市場の開拓は、今後の中国ブースターコンプレッサ市場の成長につながりそうです。

アジア太平洋ブースター圧縮機産業概要

アジア太平洋のブースターコンプレッサ市場はセグメント化されています。同市場の主要企業には、IDEX India Private Ltd、Hitachi、Bauer Kompressoren、Mikuni Kikai Kogyo、Atlas Copco Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 産業プロジェクトの成長

- 様々な用途での天然ガス需要の増加

- 抑制要因

- 高い設置コスト

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 冷却タイプ

- 空冷式

- 水冷式

- エンドユーザー

- 石油・ガス

- 化学

- 発電

- その他

- 地域

- 中国

- インド

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- IDEX India Private Ltd

- Hitachi Ltd

- Bauer Kompressoren

- Mikuni Kikai Kogyo Co. Ltd

- Atlas Copco Ltd

- Haskel International, Inc.

- Kirloskar Pneumatic Co. Ltd

- General Electric Company

- Ingersoll-Rand PLC

- Aircomp Enterprise

- 市場ランキング分析

- その他の著名な企業一覧

第7章 市場機会と今後の動向

- 石炭発電所からガス発電所への移行

- 自動車におけるガス使用の増加

目次

Product Code: 50002214

The Asia-Pacific Booster Compressor Market size in terms of assets under management value is expected to grow from USD 1.19 billion in 2025 to USD 1.53 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, various factors, such as the growth in industrial projects across the region and the escalating natural gas demand for various applications, are driving the growth of the booster compressor market.

- On the other hand, since the technology involves high installation costs, the use of existing compression systems to avoid the high expenditure on new installations could constrain market growth.

- Nevertheless, there is a rapid transition from coal to gas power stations, as well as a rise in the use of gas in motor vehicles, which is expected to provide lucrative growth opportunities for key players to maintain their position in the market in the coming years.

- China is expected to dominate the market during the forecast period due to the increase in energy consumption.

Asia-Pacific Booster Compressor Market Trends

The Oil and Gas Segment is Expected to Dominate the Market

- Booster compressors are used in a number of applications in the oil and gas value chain, covering all the sectors from upstream and downstream to the midstream. The maximum deployment was observed in the midstream segment in the gas pipeline transit systems. The world is currently drifting toward high natural gas consumption for energy requirements, upscaling the growth of gas transmission networks.

- The natural gas consumption in Asia-Pacific in 2023 was recorded as 90.5 billion cubic feet per day (bcf/day), an increase of 34% compared to 2016. The growth was primarily due to the increased inclination toward cleaner methods of energy generation in the industrial, commercial, and residential sectors. Many cross-country and national gas pipelines are being laid down to balance the supply-demand scenario.

- Australia has an extensive pipeline network all over the country. The country's gas pipeline capacity dominates the landscape relative to oil pipelines. The country has more than 42,000 km of natural gas transmission pipelines in 2023 that efficiently transported gas under high pressure from where it is produced to the outskirts of cities both large and small.

- The country is very keen on developing new pipelines to support its existing infrastructure and further develop its gas exporting capacity and capability. For instance, in August 2023, The APA Group's new Northern Goldfields Interconnect (NGI) pipeline in Western Australia was officially opened. The 580-kilometer buried pipeline connects Dampier City to the Bunbury Natural Gas Pipeline and the Goldfields Gas Pipeline, providing better access to existing and new natural gas production regions and gas storage infrastructure, especially in the Perth Basin.

- Malaysia has one of the most extensive natural gas pipeline networks in Asia, totaling about 2,468 km for the Natural Gas Distribution System (NGDS) to meet the domestic demand for gas in Malaysia. The pipeline companies in the country are constantly executing new projects.

- In August 2023, Air Products, an industrial gas company, announced that it would build, own, and operate two nitrogen plants in Penang's Bayan Lepas Free Industrial Zone and Batu Kawan Industrial Park. The company is expected to extend its pipeline network further in both areas. This strategic investment in additional capacity and infrastructure was intended to strengthen the company's leading position in Northern Malaysia and its capability to meet market needs.

- Developments like these are expected to boost the growth of the Asia-Pacific booster compressor market in the future.

China is Expected to Dominate the Market

- A high urbanization rate in China has led to an escalation of energy consumption, which has led to a rise in power generation projects and new fuel supply transit systems. Natural gas is one of the most prevalent power generation sources in China.

- According to the BP Statistical Review of World Energy, the country's natural gas-based power generation was around 297.8 TWh in 2023. The government laid down stringent regulations for cleaner power generation sources, spurring numerous gas-based power plant projects for the coming years.

- China is the largest importer of natural gas globally, and as the nation tries to reduce electricity generation through coal-fired power plants, the demand for natural gas is increasing to meet the energy requirements. For example, in October 2023, GE Vernova's Gas Power business and Harbin Electric announced that the SDIC (State Development & Investment Corp. Ltd) Jineng (Zhoushan) Gas Power Generation Co. Ltd ordered two GE 9HA.02 gas turbines for a new combined cycle power plant in the Zhoushan archipelago in Zhejiang Province, China.

- China is the largest crude oil and natural gas producer in the Asia-Pacific region; it accounted for around 57.6% and 33.8% of the total production of crude oil and natural gas, respectively, in the region in 2023. In 2023, 4198 thousand barrels per day of crude oil were produced, an increase of 2.1% over the previous year and an increase of 7.6% over 2020.

- As of January 2023, nearly 17,800 kilometers of gas pipelines were under construction in China, worth around USD 21.9 billion, and 14,300 km in India, worth around USD 20.7 billion, a distance circling over three-quarters of Earth.

- The booster compressor market is also driven by the country's new gas transmission pipeline plans to meet the growing natural gas demand in China. In October 2022, the Chinese National Development and Reform Commission (NDRC) approved the construction of a 20 billion cubic feet/year natural gas pipeline connecting gas fields in Sichuan province (southwestern China) to Hubei province (central China). Construction was expected to begin in December 2022, and the project is expected to be completed by the end of 2024. The project was developed by PipeChina's Southwest Pipeline Company.

- Such developments are likely to lead to the growth of the Chinese market for booster compressors in the future.

Asia-Pacific Booster Compressor Industry Overview

The Asia-Pacific booster compressor market is fragmented. Some of the key players in the market include IDEX India Private Ltd, Hitachi Ltd, Bauer Kompressoren, Mikuni Kikai Kogyo Co. Ltd, and Atlas Copco Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Industrial Projects

- 4.5.1.2 Escalating Natural Gas Demand for Various Applications

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Cooling Type

- 5.1.1 Air-cooled

- 5.1.2 Water-cooled

- 5.2 End User

- 5.2.1 Oil and Gas

- 5.2.2 Chemical

- 5.2.3 Power Generation

- 5.2.4 Other End Users

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Indonesia

- 5.3.4 Malaysia

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 IDEX India Private Ltd

- 6.3.2 Hitachi Ltd

- 6.3.3 Bauer Kompressoren

- 6.3.4 Mikuni Kikai Kogyo Co. Ltd

- 6.3.5 Atlas Copco Ltd

- 6.3.6 Haskel International, Inc.

- 6.3.7 Kirloskar Pneumatic Co. Ltd

- 6.3.8 General Electric Company

- 6.3.9 Ingersoll-Rand PLC

- 6.3.10 Aircomp Enterprise

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Transition from coal to gas power stations

- 7.2 Rise in the use of gas in motor vehicles

アジア太平洋のブースターコンプレッサ:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日