|

市場調査レポート

商品コード

1645087

世界の空気圧式廃棄物管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Pneumatic Waste Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の空気圧式廃棄物管理システム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

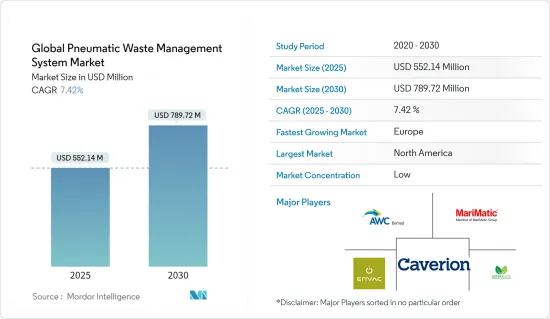

空気圧式廃棄物管理システムの世界市場規模は、2025年に5億5,214万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.42%で、2030年には7億8,972万米ドルに達すると予測されます。

主要ハイライト

- スマートシティソリューションに対する需要の高まり、サステイナブル開発を推進する政府の取り組み、都市固形廃棄物発生量の増加を考慮すると、空気圧式廃棄物管理システムは今後数年間で大きく成長すると予想されます。こうしたシステムには、騒音や交通渋滞の緩和、公衆衛生と安全性の向上、従来の廃棄物収集方法と比べた温室効果ガス排出量の削減など、多くの利点があります。

- 持続可能性の目標に沿い、公的インセンティブから恩恵を受ける可能性のあるこうしたシステムは、環境規制が厳しくなるにつれてますます魅力的になっています。世界の固形廃棄物生産量は2050年までに増加すると予想されており、これも大きな促進要因となっています。効率的な廃棄物管理を促進し、埋立地への依存を減らすことで、空気式廃棄物収集システムは実用的なソリューションを記載しています。

- 2023年7月、ローマ、パリ、バルセロナを視察したGreater Chennai Corporation(GCC)は、これらの都市が実践している固形廃棄物管理(SWM)システムの改善策の導入を検討しました。

- 廃棄物を簡単に処理し、こぼれたり直接触れたりするのを避けるため、GCCは、蓋に穴が開いたごみ箱を設置し、廃棄物タイプを示す色のついたバンドを付ける予定です。これらは、ビーチのような人通りの多い場所に導入される予定です。また、2~3ヶ月の間、ガラス瓶用の別容器もビーチに設置される予定です。さらに、GCCは、さまざまな利用者から排出される重量を測定し、粗大ゴミ排出者を特定するために、検査的にゴミ収集車に計量機を設置することを提案しました。

世界の空気圧式廃棄物管理システム市場動向

欧州は今後数年で大幅な市場成長が見込まれる

- 何十年もの間、空気圧式廃棄物管理システムは欧州全土で導入されており、先進技術であると考えられています。これらのシステムはスカンジナビアで普及しており、スウェーデンとフィンランドが最も集中しています。よりサステイナブル環境へのニーズが高まるにつれ、廃棄物管理戦略はますますグローバリゼーションしています。交通量と公害を減らす必要がある都市部では、空気圧による廃棄物収集が従来の道路運搬に代わる選択肢を提供しています。

- 欧州の情報源によると、据置型真空廃棄物収集システムへの投資コストは、建設工事や予備調査・検査を除くと、230万ユーロ(250万米ドル)から1,360万ユーロ(1,476万米ドル)です。システムの規模により、これらの費用は大きく異なります。流入口の数、ネットワークの長さ、収集される廃棄物の分別数、真空廃棄物収集システム1基の規模は、接続人口に応じて調整されます。

- パイプ1メートルあたりの平均コストは1,000~3,000ユーロ、流入口1つあたりの平均コストは2万~7万ユーロ(21,706~7万5,974米ドル)でした。平均投資額は住宅1戸当たり2,400ユーロ(2,604米ドル)、住民1人当たり835ユーロ(906米ドル)でした。

- 2023年8月、エンバックは、手順を地下に移動させ、個々のごみシュートからの手動のごみ収集に取って代わる空気圧式ごみ収集システムを発明し、ごみに関連する大渋滞と二酸化炭素排出を劇的に削減しました。中国では、多くのスマートシティや病院がこの技術を採用しています。

病院向け空気圧式廃棄物管理システムの需要が高まる

- 医療とフードサービスの観点から、空気圧式廃棄物システムは医療廃棄物、生ごみ、その他の潜在的に危険な物質の運搬に使用されています。衛生と安全の促進は、空気圧システムで管理される特定タイプのゴミに貢献しています。

- 2023年10月、Envac Franceは、イッシー・ル・ムリノー市とロマンヴィル市、パリのバティニョール地区への空気圧式廃棄物収集システムの設置を担当しました。この先進技術により、従来の廃棄物収集車の収集ルートが大幅に削減され、NO2とCO2の排出量が80%削減されました。

- 現在、ムーランとロマンヴィルの2つの廃棄物収集施設が稼動しているイッシー・ル・ケベック市とバティニョール市では、エンバックがサステイナブル都市開発のためのサプライヤーと協力し、空気圧式廃棄物管理システムを導入しました。さらに、モンペリエ病院とストラスブール病院の2つの手術室では、1,500床以上のベッドを組み合わせて利用できます。

- 合計で、パリベルトの都市施設は1万1,000世帯の自動廃棄物収集サービスをカバーしており、3万6,000人以上の住民が、便利さに加えて都市の環境改善にも貢献する革新的な廃棄物管理サービスの恩恵を受けていることになります。

世界の空気圧廃棄物管理システム産業概要

空気圧式廃棄物管理システム市場は、世界の参入企業によって統合され、支配されています。参入企業は市場の主要シェアを獲得するため、地理的プレゼンスの拡大に注力しています。市場の主要企業には、Envac Group、Stream、MariMatic Oy、Aerbin ApS、Logiwaste ABなどがあります。これらの企業は、より多くの市場シェアを獲得するために、M&A、戦略的提携、合弁事業、パートナーシップなどの戦略を継続的に採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 市場における技術の進歩

- 市場における政府の規制と取り組み

- 輸送料金の注目点

- バリューチェーン/サプライチェーン分析

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 都市化と人口の増加

- 政府の規制と取り組み

- 技術進歩への投資

- 市場抑制要因

- 社会的認識と受容

- 保守・運用コスト

- 市場機会

- 発展途上地域における市場拡大

- サーキュラー・エコノミー・モデルの採用

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- エンドユーザー別

- 住宅用

- 商業(オフィス)

- 病院

- ホスピタリティ

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- マレーシア

- タイ

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- エジプト

- その他のMENA

- ラテンアメリカ

- ブラジル

- アルゼンチン

- その他のラテンアメリカ

- 北米

第7章 競合情勢

- Market Concentration

- 企業プロファイル

- ENVAC

- MARIMATIC OY

- AWC BERHAD

- Stream

- ATREO

- Ecosir Group OY

- GreenWave Solutions

- CAVERION Corporation

- Air-Log International GmbH

- LOGIWASTE AB

- AERBIN APS

- Peakway Environmental Sci & Tech Co. Ltd*

- その他の企業

第8章 市場の将来

第9章 付録

The Global Pneumatic Waste Management System Market size is estimated at USD 552.14 million in 2025, and is expected to reach USD 789.72 million by 2030, at a CAGR of 7.42% during the forecast period (2025-2030).

Key Highlights

- In view of the growing demand for smart city solutions, government initiatives promoting sustainable development, and increasing municipal solid waste generation, pneumatic waste management systems are expected to grow significantly over the next few years. Such systems offer a number of advantages, such as reducing noise and traffic congestion, improving public health and safety, and lowering greenhouse gas emissions compared to conventional waste collection methods.

- These systems, aligned with sustainability objectives and the potential to benefit from public incentives, are becoming increasingly attractive as environmental regulations become more stringent. The global municipal solid waste production is expected to increase by 2050, and this is another major growth driver. By facilitating efficient waste management and reducing reliance on landfills, pneumatic waste collection systems provide a practical solution.

- In July 2023, following a trip to Rome, Paris, and Barcelona, the Greater Chennai Corporation (GCC) mulled over the introduction of measures practiced by these cities to improve the solid waste management (SWM) system.

- In order to allow easy disposal of waste and avoid spilling and direct contact with it, GCC intends to install dustbins with holes in the lids and colored bands to indicate the category of waste to be disposed of. These are expected to be introduced in high-traffic areas such as beaches. For a period of 2 to 3 months, separate containers for glass bottles will also be placed on the beach. Additionally, the GCC proposed installing a weighing machine in garbage collection vehicles on a pilot basis to determine the weight generated by different users and identify bulk waste generators.

Global Pneumatic Waste Management System Market Trends

Europe is Expected to Witness Significant Market Growth in the Coming Years

- For decades, pneumatic waste management systems have been in place throughout Europe and are considered to be an advanced technology. These systems are widespread in Scandinavia, with Sweden and Finland having the highest concentration. Waste management strategies are becoming increasingly global as the need for a more sustainable environment grows. In urban areas where there is a need to reduce traffic and pollution, pneumatic waste collection provides an alternative to traditional road haulage.

- According to European sources, the cost of investing in stationary vacuum waste collection systems, excluding construction works and preliminary studies or tests, is between EUR 2.3 million (USD 2.50 million) and EUR 13.6 million (USD 14.76 million). Due to the size of the systems, these costs differ significantly. The number of inlets, the length of the network, the number of waste fractions collected, and the size of one vacuum waste collection system are adjusted according to the connected population.

- The average cost per meter of pipe was EUR 1,000-3,000, and the average cost per inlet was EUR 20,000-70,000 (USD 21,706-75,974). The average investment was EUR 2,400 (USD 2,604) per dwelling and EUR 835 (USD 906) per inhabitant.

- In August 2023, Envac invented a pneumatic waste collection system that moves the procedure underground and replaces manual waste collection from individual refuse chutes, dramatically reducing waste-related heavy traffic and carbon emissions. In China, a number of smart cities and hospitals have adopted this technology.

The Demand for Pneumatic Waste Management Systems for Hospitals is Increasing

- In terms of healthcare and food services, pneumatic waste systems are used to transport medical waste, food scraps, and other potentially hazardous materials. Promoting hygiene and safety contributes to the specific types of garbage managed through pneumatic systems.

- In October 2023, Envac France was responsible for installing pneumatic waste collection systems in the municipalities of Issy-le-Moulineaux and Romainville, as well as in the Batignolles district of Paris. This advanced technology significantly reduces the number of conventional waste truck collection routes, resulting in an 80% reduction in NO2 and CO2 emissions.

- In the municipalities of Issy le Quebec, which currently have two waste collection facilities in operation, Moulin and Romainville, as well as Batignolles, Envac joined forces with suppliers for sustainable urban development to install pneumatic waste management systems. In addition, a combination of over 1,500 beds is available in two operating units at Montpellier Hospital and Strasbourg Hospital.

- In total, the urban facilities in the Paris Belt cover the automated waste collection service of 11,000 households, which means that more than 36,000 inhabitants benefit from an innovative waste management service that, in addition to being convenient, contributes to improving the environment in cities.

Global Pneumatic Waste Management System Industry Overview

The pneumatic waste system market is consolidated and dominated by global players. The players are focusing on expanding their geographical presence to capture a major share of the market. Some of the key players in the market include Envac Group, Stream, MariMatic Oy, Aerbin ApS, and Logiwaste AB. They are continuously adopting strategies like mergers and acquisitions, strategic alliances, joint ventures, and partnerships to gain more market shares.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technology Advancements in the Market

- 4.3 Government Regulations and Initiatives in the Market

- 4.4 Spotlight on Transport Rates

- 4.5 Value Chain/Supply Chain Analysis

- 4.6 Impact on COVID-19 on the Market

5 Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Growing Urbanization and Population

- 5.1.2 Government Regulations and Initiatives

- 5.1.3 Investments in Technology Advancements

- 5.2 Market Restraints

- 5.2.1 Public Awareness and Acceptance

- 5.2.2 Maintenance and Operational Costs

- 5.3 Market Opportunities

- 5.3.1 Market Expansions in Developing Regions

- 5.3.2 Adoption of Circular Economy Models

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Residential

- 6.1.2 Commercial (Offices)

- 6.1.3 Hospitals

- 6.1.4 Hospitality

- 6.1.5 Others

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Mexico

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 France

- 6.2.2.3 Spain

- 6.2.2.4 Italy

- 6.2.2.5 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Australia

- 6.2.3.5 Singapore

- 6.2.3.6 Malaysia

- 6.2.3.7 Thailand

- 6.2.3.8 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 Saudi Arabia

- 6.2.4.2 Qatar

- 6.2.4.3 United Arab Emirates

- 6.2.4.4 Egypt

- 6.2.4.5 Rest of MENA

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Argentina

- 6.2.5.3 Rest of Latin America

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Company Profiles

- 7.2.1 ENVAC

- 7.2.2 MARIMATIC OY

- 7.2.3 AWC BERHAD

- 7.2.4 Stream

- 7.2.5 ATREO

- 7.2.6 Ecosir Group OY

- 7.2.7 GreenWave Solutions

- 7.2.8 CAVERION Corporation

- 7.2.9 Air-Log International GmbH

- 7.2.10 LOGIWASTE AB

- 7.2.11 AERBIN APS

- 7.2.12 Peakway Environmental Sci & Tech Co. Ltd*

- 7.3 Other Companies