東南アジアの石油・ガスパイプライン- 市場シェア分析、産業動向、成長予測(2025年~2030年)

South-East Asia Oil And Gas Pipeline - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645074

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

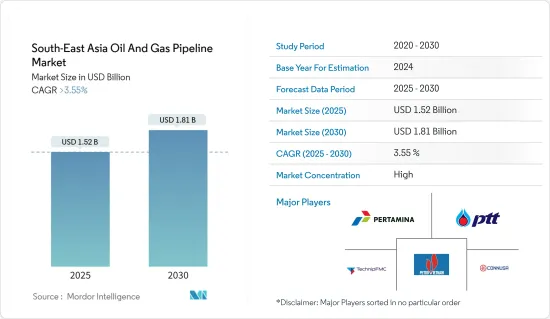

東南アジアの石油・ガスパイプライン市場規模は2025年に15億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.55%を超え、2030年には18億1,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、この地域におけるエネルギー需要の増加と新たな輸出機会が、東南アジアの石油・ガスパイプライン市場を牽引すると予想されます。

- しかし、エネルギー価格の変動は、東南アジアで研究されている市場の成長を妨げると予想されます。

- モニタリングシステムなどのスマートパイプラインシステムの導入が増加していることから、予測期間中に成長機会がもたらされると期待されています。

- インドネシアは、最大のエネルギー消費国であり、予測期間中にこの地域で石油・ガスの需要が増加するため、東南アジアの石油・ガスパイプライン市場を独占すると予想されます。

東南アジアの石油・ガスパイプライン市場動向

ガスパイプラインセグメントが市場を独占

- 人口急増と経済拡大に伴い、よりクリーンで効率的なエネルギー源の必要性が高まっています。天然ガスは、比較的クリーンな化石燃料として、環境への配慮と経済成長の願望に合致しています。天然ガスへのエネルギー嗜好のシフトは、ガスパイプラインインフラの開発と拡大を後押ししています。

- Energy Institute Statistical Review of World Energyによると、2022年の天然ガス消費量は、同地域の産業減速のため、過去10年間で過去最低を記録しました。しかし、この地域のほとんどの国が化石燃料消費の削減と天然ガス消費の増加に注力しているため、消費量は今後数年間で増加すると予想されます。

- さらに、東南アジアの地理的特性は、ガス・パイプラインの優位性に有利です。この地域には多くの群島や島があり、石油の海上輸送は論理的に困難でコストがかかります。対照的に、ガス・パイプラインは、こうした困難な地形を越えて天然ガスを輸送するための、費用対効果が高く効率的なソリューションを記載しています。この地理的優位性が、エネルギー輸送手段としてガス・パイプラインが好まれる要因となっています。

- 東南アジアでは、液化天然ガス(LNG)ターミナルや関連パイプラインの開発など、ガスインフラへの投資が増加しています。こうした投資はLNGの輸入と流通を促進し、よりクリーンな代替エネルギーを記載しています。天然ガスが一次エネルギー源として脚光を浴びるにつれ、パイプラインはLNGをターミナルから消費地まで輸送する上で極めて重要な役割を果たすようになり、ガスパイプラインセグメントの重要性を高めています。

- 例えば、2023年9月、マレーシアのBumi Armadaは、インドネシアのエネルギー会社プルタミナの子会社と天然ガス商社PT Davenergy Mulia Perkasaと契約を結びました。この契約は、液化天然ガス(LNG)の開発と商業化に関するものです。この取り決めの一環として、両社はインドネシアのマドゥラガス田と隣接する油田から採掘されるLNGの開発と商業化のための基本原則を確立します。

- 以上のことから、予測期間中はガス・パイプラインセグメントが市場を独占すると予想されます。

最大の地域セグメントとなるインドネシア

- インドネシアは豊富な天然資源を有しており、特に石油・天然ガスの埋蔵量が多いです。同国は石油・ガスの重要な生産国であり、これらの資源を精製所、流通拠点、輸出ターミナルに効率的に輸送する必要性が最も高いです。膨大な埋蔵量と新たな供給源の絶え間ない探索は、インドネシアにおける石油・ガス・パイプラインインフラの拡大に説得力を与えています。

- Energy Institute Statistical Review of World Energyによると、インドネシアの石油消費量は2021~2022年にかけて8.5%増加しました。2021年の石油消費量は146万1,000バレル/日であったのに対し、2022年には158万5,000バレル/日となりました。

- インドネシアの戦略的な地理的位置は、石油・ガスパイプライン市場における優位性において重要な役割を果たしています。同国は多数の島や群島から構成されており、効率的なエネルギー輸送のためにパイプラインの建設が必要となっています。特にガス・パイプラインは、厳しい地形を越えて天然ガスを輸送し、生産拠点と都市部や工業地帯を結ぶ、費用対効果が高く信頼性の高い手段です。

- 2023年1月、Casakhaは、設計、エンジニアリング、プロジェクト管理活動をジャカルタ事務所で速やかに開始すると発表しました。インドネシアの海底・海洋コンサルタント会社によって、洋上設置は2023年に予定されています。定められた業務範囲は、LPROとEPROのプラットフォームを結ぶ16インチ(40.6センチ)の海上パイプラインに関する詳細なエンジニアリング設計、設置、輸送、エンジニアリング業務を包含します。

- インドネシアにおけるエネルギー需要の拡大は、石油・ガスパイプラインセグメント拡大の原動力となっています。同国では経済開発と相まって人口が拡大しており、エネルギー資源の必要性が高まっています。この需要を満たすためには、パイプラインプロジェクトへの投資が不可欠であり、これらのパイプラインは、家庭、企業、産業のエネルギー需要を満たすための石油・ガス輸送の主要手段として機能しています。

- インドネシアの石油・ガスパイプライン市場における優位性は、規制の枠組みと政府の支援にあります。政府はエネルギーインフラの開発を積極的に推進し、パイプラインプロジェクトへの投資を奨励しています。規制当局が提供する有利な規制やインセンティブは、国内使用と輸出の両方でパイプライン・セクターの成長を助長する環境を作り出しています。

- 従って、上述の点から、予測期間中はインドネシアが市場を独占すると予想されます。

東南アジアの石油・ガスパイプライン産業概要

東南アジアの石油・ガスパイプライン市場は適度にセグメント化されています。同市場の主要企業(順不同)には、PT Pertamina、PTT Public Company Limited、TechnipFMC PLC、PetroVietnam、PT.Connusa Energindoなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 東南アジアの主要パイプラインプロジェクト一覧(パイプラインの長さ、輸送燃料、オペレーター、総CAPEX、着工年、試運転年)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- エネルギー需要の増加

- 輸出機会の増加

- 抑制要因

- エネルギー価格の変動

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所

- 陸上

- 洋上

- タイプ

- 原油

- 天然ガス

- 国名

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他の東南アジア諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- Companies Profiles

- PT Pertamina

- PTT Public Company Limited

- TechnipFMC PLC

- PetroVietnam

- PT. Connusa Energindo

- 市場シェア

第7章 市場機会と今後の動向

- スマートパイプラインシステムの導入拡大

目次

Product Code: 50002037

The South-East Asia Oil And Gas Pipeline Market size is estimated at USD 1.52 billion in 2025, and is expected to reach USD 1.81 billion by 2030, at a CAGR of greater than 3.55% during the forecast period (2025-2030).

Key Highlights

- In the medium term, the increasing energy demand in the region and emerging export opportunities in the area are expected to drive the Southeast Asian oil and gas pipeline market.

- However, the volatility in energy prices is expected to hinder the growth of the market studied in Southeast Asia.

- The increasing deployment of smart pipeline systems, such as monitoring systems, is expected to provide growth opportunities in the forecast period.

- Indonesia is expected to dominate the Southeast Asian oil and gas pipeline market due to the country being the largest energy consumer and the increasing demand for oil and gas in the region during the forecast period.

South-East Asia Oil And Gas Pipeline Market Trends

Gas Pipeline Segment to Dominate the Market

- With the region's burgeoning population and economic expansion, the need for cleaner and more efficient energy sources has intensified. Natural gas, as a relatively cleaner-burning fossil fuel, aligns with environmental concerns and economic growth aspirations. This shift in energy preference toward natural gas drives the development and expansion of gas pipeline infrastructure.

- According to the Energy Institute Statistical Review of World Energy, in 2022, natural gas consumption reached an all-time low in the past decade due to the industrial slowdown in the region. However, consumption is expected to increase in the coming years as most countries in the area focus on reducing fossil fuel consumption and rising natural gas consumption.

- Furthermore, Southeast Asia's geographical characteristics favor the dominance of gas pipelines. The region comprises numerous archipelagos and islands, and maritime transport of oil can be logistically challenging and costly. In contrast, gas pipelines provide a cost-effective and efficient solution for transporting natural gas across these difficult terrains. This geographic advantage contributes to the inclination toward gas pipelines as the preferred mode of energy transportation.

- Southeast Asia is witnessing increased investments in gas infrastructure, including the development of liquefied natural gas (LNG) terminals and associated pipelines. These investments facilitate the import and distribution of LNG, offering a cleaner energy alternative. As natural gas gains prominence as a primary energy source, channels play a pivotal role in transporting LNG from terminals to consumption centers, thereby bolstering the significance of the gas pipeline segment.

- For instance, in September 2023, Malaysia's Bumi Armada made an agreement with a subsidiary of the Indonesian energy company Pertamina and natural gas trading firm PT Davenergy Mulia Perkasa. The agreement pertains to the development and commercialization of liquefied natural gas (LNG). As part of this arrangement, the companies would establish fundamental principles for the development and commercialization of LNG extracted from the Madura Gas Field and the adjacent fields in Indonesia.

- Therefore, according to the points discussed above, the gas pipeline segment is expected to dominate the market studied during the forecast period.

Indonesia expected to be the Largest Geographic Segment

- Indonesia has abundant natural resources, notably its extensive reserves of oil and natural gas. The country is a significant oil and gas producer, and the need to efficiently transport these resources to refineries, distribution points, and export terminals is paramount. The vast reserves and the continuous exploration for new sources create a compelling case for the expansion of oil and gas pipeline infrastructure in Indonesia.

- According to the Energy Institute Statistical Review of World Energy, oil consumption in the country increased by 8.5% between 2021 and 2022. In 2022, oil consumption was 1,585 thousand barrels per day compared to 1,461 thousand barrels per day in 2021.

- Indonesia's strategic geographic location plays a crucial role in its expected dominance in the oil and gas pipeline market. The nation consists of numerous islands and archipelagos, necessitating the construction of pipelines for efficient energy transportation. Gas pipelines, in particular, offer a cost-effective and reliable means of transporting natural gas across challenging terrain, connecting production sites to urban centers and industrial zones.

- In January 2023, Casakha announced that the commencement of design, engineering, and project management activities would take place promptly at its Jakarta offices. The offshore installation is scheduled for 2023, as outlined by the Indonesian subsea and offshore consultancy. The defined scope of work encompasses detailed engineering design, installation, transportation, and engineering tasks related to a 16-inch (40.6 centimeters) offshore pipeline connecting the LPRO and EPRO platforms.

- The growing demand for energy in Indonesia is a driving force behind the expansion of the oil and gas pipeline sector. The country's expanding population, coupled with economic development, fuels the need for energy resources. To meet this demand, investments in pipeline projects are imperative, and these pipelines serve as the primary mode of transporting oil and gas to meet the energy requirements of households, businesses, and industries.

- Indonesia's regulatory framework and government support are instrumental in its dominance in the oil and gas pipeline market. The government actively promotes the development of energy infrastructure and encourages investment in pipeline projects. Favorable regulations and incentives provided by regulatory bodies create an environment conducive to the growth of the pipeline sector, both for domestic use and export.

- Therefore, according to the points discussed above, Indonesia is expected to dominate the market studied during the forecast period.

South-East Asia Oil And Gas Pipeline Industry Overview

The Southeast Asian oil and gas pipeline market is moderately fragmented. Some of the major players in the market (in no particular order) include PT Pertamina, PTT Public Company Limited, TechnipFMC PLC, PetroVietnam, and PT. Connusa Energindo, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 List of Major Upcoming and in Pipeline Projects, Southeast Asia (Length of Pipeline, Transportation Fuel, Operator, Total CAPEX, Year of Start of Construction, and Commissioning Year)

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Energy Demand

- 4.6.1.2 Increasing Export Opportunities

- 4.6.2 Restraints

- 4.6.2.1 Volatility in Energy Prices

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Type

- 5.2.1 Crude Oil

- 5.2.2 Natural Gas

- 5.3 Country

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Thailand

- 5.3.4 Vietnam

- 5.3.5 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Companies Profiles

- 6.3.1 PT Pertamina

- 6.3.2 PTT Public Company Limited

- 6.3.3 TechnipFMC PLC

- 6.3.4 PetroVietnam

- 6.3.5 PT. Connusa Energindo

- 6.4 Market Share

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Deployment of Smart Pipeline Systems

東南アジアの石油・ガスパイプライン- 市場シェア分析、産業動向、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日