中東・アフリカのフラックスタック-市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Middle-East And Africa Frac Stack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645051

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

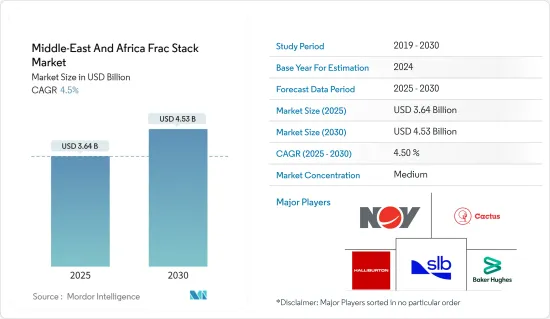

中東・アフリカのフラックスタック市場規模は2025年に36億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.5%で、2030年には45億3,000万米ドルに達する見込みです。

主要ハイライト

- 中期的には、非在来型資源からの生産増加やエネルギー需要の拡大などの要因が、予測期間中のフラックスタック市場を牽引すると予想されます。

- その一方で、環境問題への懸念や資本市場やインセンティブの不足が市場の成長を抑制しています。

- 探査・生産(E&P)中に収集される大量のデータを分析するためのモノのインターネット(IoT)の採用により、安全上の懸念に対処し、フラッキングプロセスの効率を向上させる上で、先進的分析とシミュレーションソフトウェアの重要性が増しています。フラッキング作業におけるビッグデータ分析とIoTシステムは、フラックスタック市場に大きなビジネス機会をもたらす可能性が高いです。

- シェールブームにより、サウジアラビアはフラックスタックの最大市場になると予想されています。これにより、経済的生産のために破砕が必要なシェール埋蔵量の開発が増加しています。

中東・アフリカのフラックスタック市場動向

陸上部門が市場を独占する見込み

- 中東・アフリカのフラックスタック市場では、産業力学を浮き彫りにするいくつかの重要な要因によって、陸上部門の優位が予想されます。この優位性の主要触媒の1つは、この地域におけるかなりの陸上石油・ガス生産活動です。

- 特に中東は広大な陸上埋蔵量を抱えており、坑井の生産性を高めるためにフラックスタックを使用する必要があります。陸上プロジェクトに関連するアクセスの良さと費用対効果は、このセグメントの持続的成長に大きく貢献しています。

- Energy Institute Statistical Review of World Energy 2023によると、2022年の同地域の石油生産量は日量約3,778万6,000バレルで、2021年と比較して6%以上の成長でした。同地域でのフラッキング活動の増加に伴い、生産量も同時に増加すると予想されます。

- さらに、陸上事業が提供する物流の優位性が、その優位性において重要な役割を果たしています。陸上では一般に、輸送やインフラの面で、沖合に比べ課題が少ないです。この物流の容易さは、フラックスタックの効率的な配置につながり、作業の複雑さとコストを削減します。中東・アフリカの石油・ガス産業が拡大を続ける中、陸上操業に関連する実際的な利点により、このセグメントはフラックスタック利用の中心的な位置づけとなっています。

- さらに、陸上採掘技術における技術の進歩と革新が、このセグメントの優位性をさらに高めています。水圧破砕技術と貯留層管理技術の継続的な改善により、陸上作業の効率が向上し、水圧破砕スタックの需要を促進しています。進化する採掘方法と水圧破砕スタック利用との相乗効果により、陸上部門は市場で主導的な地位を強化しています。

- その結果、多くの事業会社がシェールガスやタイトガスのような非在来型の陸上埋蔵量の開発に重点を移しており、大規模な海洋プロジェクトよりもリスクが低く、設備投資も少なくて済みます。予測期間中、非在来型陸上埋蔵物の水圧破砕の増加により、フラックスタックの需要が増加すると予想されます。

- 例えば、2022年9月、TAG Oil Ltdは、エジプト西部砂漠に位置する107km2(2万6,000エーカー)の鉱区、バドル油田(「BED-1」)内の非在来型アブ・ロアシュ「F」貯留層(「ARF」)を開発するため、バドル石油会社(「BPCO」)から石油サービス契約を受注しました。

- 従って、上記の点から、予測期間中は陸上部門が市場を独占すると予想されます。

著しい成長が期待されるサウジアラビア

- サウジアラビアは世界の産油国として重要な役割を担っており、石油・ガス探査・生産活動の中心的な拠点となっています。サウジアラビアの膨大な陸上埋蔵量には、効率的で先進的抽出方法が必要であり、坑井の性能を最適化するための重要なコンポーネントとしてフラックスタックが浮上しています。したがって、陸上石油・ガス部門が堅調であることが、フラックスタック市場におけるサウジアラビアの優位性に大きく寄与しています。

- 例えば、Energy Institute Review of World Energy 2023によると、サウジアラビアのガス生産量は2021~2022年にかけて5.2%以上増加しました。2022年のガス生産量は、2021年の114.5bcmに対して120.4bcmであり、これは同国の石油・ガス部門の増加を示しており、コンプレッサー市場を牽引しています。

- さらに、サウジアラビア政府による「ビジョン2030」の枠組みで概説された戦略的イニシアチブが極めて重要な役割を果たしています。この経済多様化戦略の一環として、陸上石油・ガス事業の強化に重点を置いていることは、フラックスタックに対する需要の高まりと一致しています。採掘プロセスの近代化と最適化に取り組むサウジアラビアの姿勢は、同国が中東・アフリカのフラックスタック市場を独占する態勢を整えているとの見方を強めています。

- サウジアラビアの地理的優位性は、フラックスタック市場における優位性をさらに高めています。サウジアラビアは中東・アフリカの中心に位置しているため、費用対効果の高い輸送と物流が可能であり、投資家にとって陸上プロジェクトがより実現可能で魅力的なものとなっています。この戦略的な位置付けは、サウジアラビアが陸上石油・ガス事業でフラックスタックを効率的に配備する能力に貢献しており、地域市場のフロントランナーとしての地位を確固たるものにしています。

- さらに、サウジアラビアが石油・ガス部門における技術の進歩と革新に重点を置いていることは、陸上採掘方法が複雑化していることと一致しています。事業者がより効率的でサステイナブルソリューションを求めるにつれ、先進的なフラックスタックへの需要が高まっています。サウジアラビアは最先端技術の導入に積極的に取り組んでおり、中東・アフリカにおけるフラックスタック市場の最前線に位置しています。

- 2023年5月、サウジアラビアの巨大石油会社Aramcoは、石油精製大手のSinopec Corpとフランスの石油大手TotalEnergiesの提案を受け入れ、約100億米ドル相当のジャフラ・シェールガス開発プロジェクトの一部への投資に関心を示しています。Sinopec CorpとTotalEnergiesの両社は、サウジアラビアに位置するジャフラ開発への投資の可能性について個別に協議を行っています。Saudi Aramcoは、近隣のメキシコ湾岸からの海水を利用する革新的なフラッキング法を活用し、ジャフラ油田から2030年までに毎日約20億立方フィートのガスが産出されると見込んでおり、総投資額は240億米ドルになると予測しています。

- サウジアラビアの規制環境の安定性と予測可能性は、フラックスタック市場における優位性をさらに裏付けています。安定した規制枠組みは投資家の信頼を高め、陸上石油・ガスプロジェクトの長期計画を後押しします。サウジアラビアの事業者は構造化された信頼性の高い展開戦略を実施できるため、この安定性はフラックスタック市場の持続的成長にとって極めて重要な要素です。

- したがって、上記の点から、サウジアラビアは予測期間中に大きな成長を遂げることが期待されます。

中東・アフリカのフラックスタック産業概要

中東・アフリカのフラックスタック市場は半固体化しています。主要参入企業(順不同)には、Halliburton Company、Schlumberger Limited、NOV Inc.、Baker Hughes Company、Cactus Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 非在来型資源からの生産増加

- 地域におけるエネルギー需要の増大

- 抑制要因

- 環境への懸念

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所

- オンショア

- オフショア

- 坑井タイプ

- 水平・逸脱

- 産業別

- 2028年までの市場規模と需要予測(地域別)

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Halliburton Company

- Schlumberger Limited

- NOV Inc.

- Baker Hughes Company

- Cactus Inc.

- National Energy Services Reunited Corp.

- Oil States International Inc.

- The Weir Group PLC

- SPM Oil & Gas Inc.

- Superior Energy Services Inc.

第7章 市場機会と今後の動向

- 先進的分析とシミュレーション技術

目次

Product Code: 50001813

The Middle-East And Africa Frac Stack Market size is estimated at USD 3.64 billion in 2025, and is expected to reach USD 4.53 billion by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing production from unconventional resources and growing energy demand are expected to drive the frac stack market during the forecast period.

- On the other hand, environmental concerns and a lack of capital markets and incentives are restraining market growth.

- Nevertheless, with the adoption of the Internet of Things (IoT) to analyze a large amount of data collected during exploration and production (E&P), advanced analytics and simulation software have become increasingly important in addressing safety concerns and improving the efficiency of the fracking process. Big Data analytics and IoT systems in fracking operations are likely to lead to significant opportunities for the frac stack market.

- Due to the shale boom, Saudi Arabia is expected to be the largest market for frac stacks. This has led to increased exploitation of shale reserves that need to be fractured for economic production.

Middle-East And Africa Frac Stack Market Trends

The Onshore Sector is Expected to Dominate the Market

- The dominance of the onshore segment is anticipated in the Middle-East and African frac stack market, driven by several key factors that underscore the industry dynamics. One primary catalyst for this dominance is the considerable onshore oil and gas production activities in the region.

- The Middle East, in particular, hosts extensive onshore reserves, and the prevalent exploration and extraction operations necessitate the use of frac stacks to enhance well productivity. The accessibility and cost-effectiveness associated with onshore projects contribute significantly to the sustained growth of this segment.

- According to the Energy Institute Statistical Review of World Energy 2023, in 2022, the oil production in the region was around 37,786 thousand barrels per day, which was a growth of over 6% compared to 2021. As the fracking activities increase in the region, the production is expected to increase simultaneously.

- Additionally, the logistical advantages offered by onshore operations play a crucial role in their dominance. Onshore sites generally present fewer challenges in terms of transportation and infrastructure compared to offshore counterparts. This logistical ease translates into more efficient deployment of frac stacks, reducing operational complexities and costs. As the oil and gas industry in Middle-East and Africa continues to expand, the practical advantages associated with onshore operations position this segment as a focal point for frac stack utilization.

- Moreover, the technological advancements and innovations in onshore extraction techniques further bolster the dominance of this segment. Continuous improvements in hydraulic fracturing technologies and reservoir management techniques enhance the efficiency of onshore operations, driving the demand for frac stacks. The synergy between evolving extraction methods and frac stack utilization reinforces the onshore segment's leading position in the market.

- As a result, a number of operating companies have shifted their focus to the exploitation of unconventional onshore reserves, such as shale and tight gas reserves, which present lower risk and require a lower capital investment than large offshore projects. During the forecast period, there is expected to be an increase in the demand for frac stacks due to the increased hydraulic fracking of unconventional onshore reserves.

- For instance, in September 2022, TAG Oil Ltd was awarded a petroleum services contract by Badr Petroleum Company ("BPCO") to develop the unconventional Abu Roash "F" reservoir ("ARF") within the Badr Oil Field ("BED-1"), a 107 km2 (26,000 acres) concession located in the Western Desert of Egypt.

- Therefore, as per the points mentioned above, the onshore segment is expected to dominate the market during the forecast period.

Saudi Arabia is Expected to Witness Significant Growth

- The Kingdom's prominent role as a global oil producer positions it as a central hub for oil and gas exploration and production activities. Saudi Arabia's vast onshore reserves necessitate efficient and advanced extraction methods, with frac stacks emerging as crucial components to optimize well performance. The robust onshore oil and gas sector, therefore, contributes significantly to the expected dominance of Saudi Arabia in the frac stack market.

- For instance, according to the Energy Institute Review of World Energy 2023, gas production in Saudi Arabia increased by more than 5.2% between 2021 and 2022. In 2022, gas production was 120.4 bcm compared to 114.5 bcm in 2021, signifying the country's increasing oil and gas sector, which drives the compressor market.

- Furthermore, the strategic initiatives outlined in the Vision 2030 framework by the Saudi Arabian government play a pivotal role. As part of this economic diversification strategy, the focus on enhancing onshore oil and gas operations aligns with the growing demand for frac stacks. Saudi Arabia's commitment to modernizing and optimizing its extraction processes reinforces the notion that the country is poised to dominate the frac stack market in Middle-East and Africa.

- The geographical advantage of Saudi Arabia further enhances its dominance in the frac stack market. The country's central location in the region facilitates cost-effective transportation and logistics, making onshore projects more feasible and attractive for investors. This strategic positioning contributes to Saudi Arabia's ability to efficiently deploy frac stacks in its onshore oil and gas operations, solidifying its position as a frontrunner in the regional market.

- Additionally, Saudi Arabia's focus on technological advancements and innovation in the oil and gas sector aligns with the increasing complexity of onshore extraction methods. As operators seek more efficient and sustainable solutions, the demand for advanced frac stacks rises. The Kingdom's commitment to adopting cutting-edge technologies positions it at the forefront of the evolving frac stack market in the Middle East and Africa.

- In May 2023, Saudi Arabia's oil behemoth, Aramco, is receptive to proposals from refining giant Sinopec Corp and the French oil major TotalEnergies, considering their interest in investing in a portion of the Jafurah shale gas development project valued at approximately USD 10 billion. Both Sinopec and TotalEnergies are engaged in separate discussions regarding potential investments in the Jafurah development situated in Saudi Arabia. Leveraging an innovative fracking method utilizing seawater from the nearby Gulf coast, Saudi Aramco anticipates the Jafurah field to yield around 2 billion cubic feet of gas daily by 2030, with a projected total investment of USD 24 billion.

- The stability and predictability of Saudi Arabia's regulatory environment further support its dominance in the frac stack market. A stable regulatory framework enhances investor confidence and encourages long-term planning for onshore oil and gas projects. This stability is a crucial factor for the sustained growth of the frac stack market, as operators in Saudi Arabia can implement well-structured and reliable deployment strategies.

- Therefore, as per the above-mentioned points, the country is expected to witness significant growth during the forecasted period.

Middle-East And Africa Frac Stack Industry Overview

The Middle-East and African frac stack market is semi-consolidated. Some of the major players (in no particular order) include Halliburton Company, Schlumberger Limited, NOV Inc., Baker Hughes Company, and Cactus Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Production from Unconventional Sources

- 4.5.1.2 Growing Energy Demand in the Region

- 4.5.2 Restraints

- 4.5.2.1 Environmental Concerns

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Well Type

- 5.2.1 Horizontal and Deviated

- 5.2.2 Vertical

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Nigeria

- 5.3.4 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Halliburton Company

- 6.3.2 Schlumberger Limited

- 6.3.3 NOV Inc.

- 6.3.4 Baker Hughes Company

- 6.3.5 Cactus Inc.

- 6.3.6 National Energy Services Reunited Corp.

- 6.3.7 Oil States International Inc.

- 6.3.8 The Weir Group PLC

- 6.3.9 SPM Oil & Gas Inc.

- 6.3.10 Superior Energy Services Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advance Analysis and Simulation Technology

中東・アフリカのフラックスタック-市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日