軽量建材:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Lightweight Construction Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645043

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

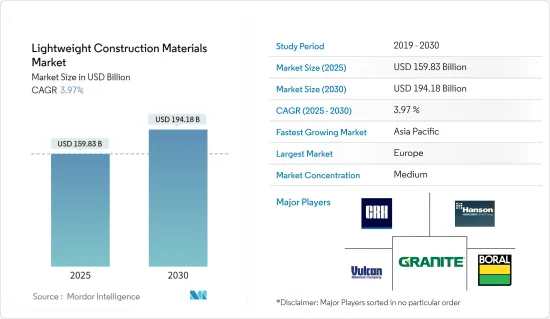

軽量建材市場規模は2025年に1,598億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.97%で、2030年には1,941億8,000万米ドルに達すると予測されます。

主要ハイライト

- 世界人口の都市化が進むにつれ、高層ビルの需要が高まっています。軽量建材を使用することで、これらの建物の重量を減らすことができ、基礎コストを節約し、地震のリスクを減らすことができます。例えば、2022年の北米の都市人口は3億879万8,139人で、2021年から0.77%増加しました。

- 2021年の北米都市人口は3億644万1,356人で、2020年から0.44%増加しました。2020年の北米都市人口は3億510万3,974人で、2019年から1.22%増加しました。さらに、2022年には、世界の都市化の度合いが57%に達しました。北米は最も都市化が進んだ地域で、人口の5分の4以上が都市部に居住しています。

- 軽量建材は、壁や屋根から失われる熱の量を減らすことで、建物のエネルギー効率を向上させることができます。例えば、2023年上半期のエネルギー効率の高い建物への投資額は、欧州が他のどの地域よりも高かったです。中国の同市場への投資額は220億米ドルで、米国(280億米ドル)をやや下回りました。こうした投資は、建築物が世界の温室効果ガス排出量の大きな割合を占めていることから、建築物が環境に与える影響を軽減するために必要です。これらの材料は、使用する原料を減らし、廃棄物を少なくすることで、建設による環境への影響を軽減するのに役立ちます。

- 軽量建材は航空宇宙・防衛セグメントで重要な役割を果たしており、航空機、宇宙船、防衛車両向けの高効率で耐久性の高い構造物の開発を可能にしています。これらの材料は大幅な軽量化に貢献し、燃料効率を高め、積載量を増やし、全体的な性能を向上させています。2013年以降、世界の宇宙関連企業に対して総額約2,720億米ドルの株式投資が行われました。米国の宇宙企業が投資総額の約47%を占め、次いで中国が29%を占めています。

軽量建材市場の動向

建築・建設セグメントが世界市場で大きなシェアを占める

- 建築・建設セグメントは軽量建材市場の主要促進要因であり、世界需要の大部分を占めています。軽量材料には、建設用途に特に適しているいくつかの利点があり、このセグメントでの普及につながっています。

- 軽量建材は建築物全体の重量を大幅に軽減するため、いくつかの利点があります。基礎にかかる負荷が最小限に抑えられるため、基礎コストの削減や耐震性の向上につながります。さらに、建築資材の輸送費が削減され、より高く細長い構造物の建設が可能になります。

- 産業筋によると、世界の建設産業の収益は今後数年間、安定的に成長すると予想されています。2030年には、2020年の2倍以上の規模になると予測されています。2020年の建設市場規模は6兆4,000億米ドルで、2030年には14兆4,000億米ドルに達すると予想されています。

- 軽量材料は設計の柔軟性を高め、ユニークな建築の特徴を生み出すことを可能にします。その多様性により、建築家やデザイナーはさまざまな形態、形態、仕上げを試すことができ、建物の美的魅力を高めることができます。多くの軽量建材はプレハブ式であるため、現場での組み立てが早く、建設時間と人件費を削減できます。これは、大規模なプロジェクトや、熟練労働者の数が限られている地域では特に有益です。

- 軽量材料は断熱性に優れていることが多く、室内温度の調節やエネルギー消費の削減に役立ちます。これは、エネルギー効率認証の取得や環境持続可能性目標の達成を目指す建物では特に重要です。

欧州が軽量建材の世界市場で大きなシェアを占める見込み

- 世界の軽量建材市場では、欧州が大きな市場シェアを占めると予想されます。欧州諸国は、建物に対する厳しいエネルギー効率規制を実施しており、断熱性に優れエネルギー消費を削減する軽量建材の需要を促進しています。クロスラミネート・ティンバー(CLT)、自動気泡コンクリート(AAC)、発泡ポリスチレン(EPS)などの軽量材料は、優れた断熱性を発揮するため、エネルギー消費を削減し、二酸化炭素排出量を削減することができます。

- さらに、欧州は高度に都市化された地域で、人口が増加し、新しい建物やインフラの需要が高まっています。軽量材料は、建築設計の最適化、建設期間の短縮、環境への影響の最小化において重要な役割を果たしています。欧州には、ドイツ、オーストリア、イタリアなどの大手生産者がおり、軽量建材の製造拠点が確立されています。この強力なサプライチェーンにより、競合価格で高品質の材料を入手することができます。

- 成長の原動力となっているのは、エネルギー効率の高い建物に対する需要の高まり、輸送効率を高めるために建材を軽量化する必要性、オフサイト工法の人気の高まりなど、いくつかの要因です。例えば、CLTはロンドンの新しいオフィスビルの建設に使用されています。CLTは人工木材の一種で、木材を何層にも重ねて接着したものです。耐火性があり、丈夫で軽量な材料です。

- さらに、AACはドイツの学校建設にも使われています。AACは軽量コンクリートの一種で、セメント、砂、石灰、水に空気を混ぜて作る。AACは、セメント、砂、石灰、水に空気を混ぜて作られる軽量コンクリートの一種で、耐火性を備えた強靭な断熱材です。

軽量建材産業概要

軽量建材市場は、世界の参入企業と地域的な参入企業が混在する断片的な市場です。この市場は、都市化、持続可能性への投資、経済成長といったいくつかの要因により、予測期間中に成長すると予想されています。この市場の主要企業は以下の通りです。 HeidelbergCement, Granite, Trinity, James Hardie, and Hanson.

その他の特典

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 市場の技術動向

- 市場における政府の規制と取り組み

- サプライチェーン/バリューチェーン分析へ洞察

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 新興諸国における軽量材料の採用と航空機生産の増加

- 各国の航空宇宙・防衛セグメントの成長

- 用途指向の研究開発への投資の増加

- 市場抑制要因

- 発展途上地域における自動車セクターの景気減速と縮小

- 建材の高コスト

- 機会

- グリーンビルディングへの取り組み

- インフラ開発

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- 製品タイプ別

- 木材

- ブリックス

- コンクリート

- その他

- 構造タイプ別

- 住宅用

- 業務用

- 工業用

- インフラ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- ASEAN諸国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Granite

- HeidelbergCement

- Hanson

- LafargeHolcim

- Trinity

- Vulcan Materials

- Dyckerhoff

- Italcementi

- Taiheiyo Cement

- CRH

- James Hardie

- Boral

第8章 市場の将来展望

第9章 付録

- 活動別GDP分布

- 資本移動に関する洞察

- 対外貿易統計-輸出入(製品別)

- 主要輸出先に関する洞察

- 主要輸入原産国に関する洞察

目次

The Lightweight Construction Materials Market size is estimated at USD 159.83 billion in 2025, and is expected to reach USD 194.18 billion by 2030, at a CAGR of 3.97% during the forecast period (2025-2030).

Key Highlights

- As the world's population becomes increasingly urbanized, there is a growing demand for high-rise buildings. Lightweight construction materials can be used to reduce the weight of these buildings, which can save on foundation costs and reduce the risk of earthquakes. For example, the North American urban population for 2022 was 308,798,139, a 0.77% increase from 2021.

- The North American urban population for 2021 was 306,441,356, a 0.44% increase from 2020. The North American urban population for 2020 was 305,103,974, a 1.22% increase from 2019. Furthermore, in 2022, the degree of urbanization worldwide was at 57 percent. North America was the region with the highest level of urbanization, with over four-fifths of the population residing in urban areas.

- Lightweight construction materials can help to improve the energy efficiency of buildings by reducing the amount of heat that is lost through the walls and roof. For instance, the value of investments in energy-efficient buildings in H1 2023 was higher in Europe than in any other region. Investments for that market in China amounted to USD 22 billion, which was somewhat lower than in the United States (USD 28 billion). These investments are necessary to reduce the environmental impact of buildings, as they were responsible for a significant share of global greenhouse gas emissions. These materials can help to reduce the environmental impact of construction by using fewer raw materials and producing less waste.

- Lightweight construction materials play a crucial role in the aerospace and defense sectors, enabling the development of highly efficient and durable structures for aircraft, spacecraft, and defense vehicles. These materials contribute to significant weight reduction, enhancing fuel efficiency, increasing payload capacity, and improving overall performance. Since 2013, a total of approximately USD 272 billion of equity investments have been made in space companies worldwide. United States space companies have accounted for almost 47 percent of the total investment, followed by China with 29 percent.

Lightweight Construction Materials Market Trends

Building & Construction segment Holds the prominent share of Global Market

- The buildings and construction segment is a major driver of the lightweight construction materials market, accounting for a significant portion of global demand. Lightweight materials offer several advantages that make them particularly well-suited for construction applications, leading to their widespread adoption in this sector.

- Lightweight construction materials significantly reduce the overall weight of a building, which has several benefits. It minimizes the load on foundations, leading to lower foundation costs and improved seismic resistance. Additionally, it reduces transportation expenses for building materials and enables the construction of taller and more slender structures.

- According to industry sources, the revenue of the global construction industry is expected to grow steadily over the next years. In 2030, it is projected to be more than twice as big as it was in 2020. The size of the construction market amounted to USD 6.4 trillion in 2020, and it is expected to reach USD 14.4 trillion in 2030.

- Lightweight materials offer greater design flexibility and enable the creation of unique architectural features. Their versatility allows architects and designers to experiment with different shapes, forms, and finishes, enhancing the aesthetic appeal of buildings. The prefabricated nature of many lightweight construction materials allows for faster assembly on-site, reducing construction time and labor costs. This is particularly beneficial for large-scale projects and in areas with limited skilled labor availability.

- Lightweight materials often possess superior thermal insulation properties, helping to regulate indoor temperatures and reduce energy consumption. This is particularly important in buildings seeking to achieve energy efficiency certifications and meet environmental sustainability goals.

Europe to Constitute Major Share of Global Lightweight Construction Materials Market

- Europe is expected to hold a significant market share in the global lightweight construction materials market. European countries have implemented stringent energy efficiency regulations for buildings, driving the demand for lightweight construction materials that offer better thermal insulation and reduce energy consumption. Lightweight materials like cross-laminated timber (CLT), autoclaved aerated concrete (AAC), and expanded polystyrene (EPS) offer superior thermal insulation properties, reducing energy consumption and lowering carbon emissions.

- Furthermore, Europe is a highly urbanized region with a growing population and increasing demand for new buildings and infrastructure. Lightweight materials play a crucial role in optimizing building designs, reducing construction time, and minimizing environmental impact. Europe has a well-established manufacturing base for lightweight construction materials, with leading producers like Germany, Austria, and Italy. This strong supply chain ensures the availability of high-quality materials at competitive prices.

- The growth is being driven by several factors, including the increasing demand for energy-efficient buildings, the need to reduce the weight of construction materials to improve transportation efficiency, and the growing popularity of off-site construction methods. For example, CLT is being used to construct a new office building in London. CLT is a type of engineered wood that is made up of layers of timber that are glued together. It is a strong and lightweight material with fire-resistant properties.

- Furthermore, AAC is used to construct schools in Germany. AAC is a type of lightweight concrete that is made by mixing cement, sand, lime, and water with air. It is a strong and insulating material with fire-resistant properties.

Lightweight Construction Materials Industry Overview

The lightweight construction materials market is fragmented in nature, with a mix of global and regional players. The market is expected to grow during the forecast period due to several factors, such as urbanization, sustainability investments, and growing economies. The major players in this market are HeidelbergCement, Granite, Trinity, James Hardie, and Hanson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends in the Market

- 4.3 Governemnt Regulations and Initiatives in the Market

- 4.4 Insights into Supply Chain/Value Chain Analysis

- 4.5 Impact of Covid-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Adoption of Lightweight Materials and Increase in the production of aircraft in developing countries

- 5.1.2 Growth of the Aerospace and Defence Sector in countries

- 5.1.3 Rise in investments in application-oriented research and development

- 5.2 Market Restraints

- 5.2.1 Economic slowdown and contraction of the automotive sector in developing regions

- 5.2.2 High cost of Construction Materials

- 5.3 Opportunities

- 5.3.1 Green Building Initiatives

- 5.3.2 Infrastructure Development

- 5.4 Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Wood

- 6.1.2 Brics

- 6.1.3 Concrete

- 6.1.4 Other Product Types

- 6.2 By Constrution Type

- 6.2.1 Resdential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.2.4 Infrastructure

- 6.3 By Goegraphy

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 France

- 6.3.2.3 United Kingdom

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 ASEAN

- 6.3.3.5 Rest of APAC

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.5 Middle East & Africa

- 6.3.5.1 GCC

- 6.3.5.2 South Africa

- 6.3.5.3 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration, Major Players)

- 7.2 Company Profiles

- 7.2.1 Granite

- 7.2.2 HeidelbergCement

- 7.2.3 Hanson

- 7.2.4 LafargeHolcim

- 7.2.5 Trinity

- 7.2.6 Vulcan Materials

- 7.2.7 Dyckerhoff

- 7.2.8 Italcementi

- 7.2.9 Taiheiyo Cement

- 7.2.10 CRH

- 7.2.11 James Hardie

- 7.2.12 Boral

8 FUTURE OUTLOOK OF THE MARKET

9 Appendix

- 9.1 GDP Distribution, by Activity

- 9.2 Insights on Capital Flows

- 9.3 External Trade Statistics - Export and Import, by Product

- 9.4 Insights on Key Export Destinations

- 9.5 Insights on Key Import Origin Countries

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日