中国の医薬品倉庫:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645035

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

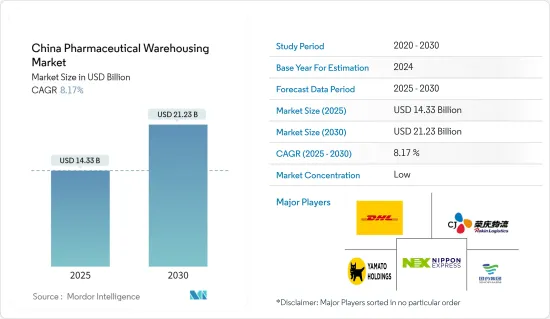

中国の医薬品倉庫市場規模は2025年に143億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.17%で、2030年には212億3,000万米ドルに達すると予測されます。

バイオテクノロジーと革新的な医薬品開発に牽引され、中国の医薬品市場は大きな転換期を迎えています。この変化は、中国政府の戦略的イニシアティブ、特に公衆衛生の強化と科学技術革新の推進を目指す「健康中国2030」計画に大きく後押しされています。

中国のバイオテクノロジーセクターは、研究開発(R&D)への多額の投資と支援的な規制状況に後押しされ、急成長を遂げています。同市場は、バイオテクノロジー新興企業、大手製薬会社、学術機関が連携し、医療研究の限界を押し広げ、新たな治療法を開拓する活気あるエコシステムを誇っています。

中国のバイオテクノロジー情勢で注目すべき動向は、人工知能(AI)とビッグデータ分析を医薬品開発に導入することです。WuXi AppTecのような企業は、AIを活用して創薬を改良し、臨床検査を合理化し、精密医療戦略を強化しています。AI主導のプラットフォームのおかげで、WuXi AppTecは有望な新薬候補の特定を早めただけでなく、研究開発努力の効率も高めました。

さらに、中国の規制改革、特に革新的な医薬品の迅速な承認プロセスは、画期的な治療法の迅速な市場参入への道を開き、継続的なイノベーションを促進する環境を育んでいます。バイオシミラーやバイオ医薬品は、費用対効果の高い代替治療を提供するだけでなく、最先端の治療へのアクセスを拡大します。

デジタルヘルス技術の拡大を支援する施策が中国政府によって展開されています。さらに、国家医療情報化開発計画などのイニシアチブにより、統一された医療情報システムに向けて取り組んでおり、多様なデジタルヘルスプラットフォームからのデータをシームレスに統合し、データの相互運用性と医療の連携を強化しています。

2023年6月、FDAはオンライン薬局が処方箋薬を調剤できるようにする動きを検討していました。この潜在的な変化は、AlibabaやJDのようなeコマース大手が急成長する市場に参入する道を開く可能性があります。この施策に関する議論は昨年半ばから行われており、承認されれば1兆人民元(約1,610億米ドル)を超える市場が開かれる可能性があります。このような動きは、伝統的病院からオンライン薬局に売上を転換させるだけでなく、市場における国営病院や流通業者の長年の支配に課題することになります。

中国の医薬品市場の変革は倉庫業にも及んでいます。医薬品産業の急成長に伴い、医薬品の効率的な保管と流通を確保するための先進的倉庫ソリューションに対する需要が高まっています。

中国の医薬品倉庫市場は、自動保管・検索システム(AS/RS)、温度管理された環境、リアルタイムの在庫管理システムなどの最先端技術を取り入れ、こうしたニーズに応えるべく進化しています。

これらの進歩は、サプライチェーン全体を通じて医薬品の完全性と品質を維持するために極めて重要です。市場が拡大を続ける中、洗練された倉庫インフラの開発は、中国の医薬品産業の全体的な成長と効率性を支える上で極めて重要な役割を果たすと考えられます。

中国の医薬品倉庫市場の動向

コールドチェーン倉庫開発の増加

2024年上半期、コールドチェーン物流量は2億2,000万トンに達し、4.4%増加しました。同時に、コールドチェーン物流の収益は2,779億人民元(389億米ドル)に達し、前年同期比で3.4%増加しました。

2024年6月までに、中国のコールドストレージ容量は2億3,700万立方メートルに拡大し、前年同期比7.73%の伸びを示しました。今年だけで942万立方メートルの新たな冷蔵倉庫容量が追加されました。2024年上半期には、全国の冷蔵倉庫のリース量は2,900万立方メートルを超え、8%以上の伸びを示しました。

生物製剤、ワクチン、特殊医薬品など、温度の影響を受けやすい品目の生産と消費の増加は、大規模な冷蔵倉庫の必要性を裏付けています。生物製剤は、従来の医薬品とは異なり、ヒトや動物を含む生物学的実体から供給される複雑な物質です。これらの生物製剤は、ワクチンから血液成分まで、幅広いスペクトルを網羅しています。

先進的治療に頻繁に利用される生物製剤は、その物理的環境のわずかな変動にも高い感受性を示します。そのため、これらの製品に対する需要の急増に対応するためには、製薬・医療企業は迅速で信頼性の高いサプライチェーンソリューションを重視しなければならないです。

2024年10月、China National Medical Products Administration(NMPA)は、生物製剤の非エンド・ツー・エンド製造を許可する検査的イニシアチブを発表しました。これまでNMPAは、生物製剤を単一の製造拠点でエンド・ツー・エンドで製造することを義務付けていました。

基本的に、これは原薬とそれに対応する製品の両方が同じ施設内で製造されることが理想的であることを意味します。しかし、国内のバイオ医薬品セクターは、特に外国のバイオ医薬品メーカーが原薬と製品を別々の場所で製造する自由裁量を認められている事実を考慮し、この規則の緩和を求めてきました。

コールドチェーン倉庫開発の大幅な増加は、中国における効率的な医薬品倉庫の重要性の高まりを浮き彫りにしています。温度に敏感な製品の需要が増加し続ける中、コールドストレージ施設の拡大は、これらの重要な製品の完全性と可用性を確保する上で重要な役割を果たすと考えられます。この動向は、製薬産業の進化する要件をサポートするために、コールドチェーンロジスティクスへの継続的な投資と技術革新の必要性を強調しています。

医薬品メーカーの開発増加

中国の施策立案者は、イノベーションの促進を目的とした規制の緩和により、外資の誘致に積極的に取り組んでいます。これは、国境を越えた研究開発に制限を課していた以前の姿勢とは異なるものです。注目すべきは、政府が今年初めて「革新的医薬品」にスポットを当てたことです。2023年だけでも、220件以上の革新的医薬品のライセンシングと提携取引があり、その額は2,660億人民元(約370億米ドル)にのぼります。

中国政府は医療部門を強化し、国際的な協力を促進するためにいくつかのイニシアチブを展開しています。CGTセグメントの国際的な参入企業は、投資、新規事業体の設立、合併、買収、あるいは4つの指定FTZへの移転といった行動に目を向け、機会をうかがっています。これらのベンチャーは、iPSCやCAR-TからmRNA、遺伝子配列決定、体外診断(IVD/LDT)に至るまで、CGT関連の幅広い領域に及んでいます。

新Circularのおかげで、中国のバイオ製薬企業は海外からの投資を直接呼び込めるようになりました。つのFTZに子会社を設立または移転することで、これまで義務付けられていた変動持分事業体(VIE)構造を回避することができます。

重要な動きとして、インディアナポリスに本社を置く企業が2024年11月に2億1,200万米ドルを投資し、蘇州工場を拡大する予定です。この拡大により、1996年以来の蘇州への累積投資額は150億元(21億米ドル)に達します。この決定は、2024年7月に同社の主要な減量薬であるゼップバウンドの中国での承認に続くものです。その直後、Bayerは北京にメディカル・イノベーションセンターを開設し、米国外で初のイノベーション・インキュベーターとなるゲートウェイ・ラボの計画を発表しました。

2024年9月、ドイツの大手製薬会社Bayerは、上海にライフサイエンス・インキュベーターを開設し、中国のイノベーション能力を「世界のトップ2に入る」と称賛しました。そのわずか1ヶ月前には、スイスの巨大企業ロシュ・ダイアグノスティックスの一部門が、蘇州の製造施設を強化するため、これまでで最大規模の投資となる4億2,000万米ドルの大規模プロジェクトを発表しました。

このような戦略的投資は、中国市場のユニークな機会に光を当てています。景気減速、厳しい国内競合、地政学的緊張といった課題にもかかわらず、ハイテクから自動車に至るセグメントでは躊躇が見られるもの、医薬品の領域は依然として光明を放っています。多くの外資系企業は、地元のバイオテクノロジー企業との利益と実りある協力の道をまだ見出しています。

北京の医療セクターの自由化というイニシアチブの一部は、高齢化する国民が一流の世界医薬品にアクセスできるようにしたいという願望によって推進されています。この自由化は医薬品製造施設の開発増加にも拍車をかけ、中国の医薬品倉庫市場に大きな影響を与えています。

中国の医薬品倉庫産業概要

中国の医薬品倉庫市場は、世界で最も競争が激しく、急成長している市場のひとつです。その背景には、同国の医療セクターの成長、医薬品製造の拡大、流通戦略の変化があります。中国の医薬品産業が成長を続ける中、シームレスな倉庫管理、効果的な物流、最先端のソリューションを提供できる企業は、この競争の激しい市場で優位に立つことができると考えられます。同市場は非常に細分化されており、Sinopharm Logistics、DHL、CJ Rokin Logisticsなど、多くの国内外の参入企業が同市場で事業を展開しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要(市場と経済の現在の市場シナリオ)

- 政府の規制と取り組み

- 技術動向

- 市場力学

- 市場促進要因

- 急拡大する医薬品産業

- 人口増加は倉庫市場の主要促進要因のひとつ

- 市場抑制要因/課題

- サプライチェーンの混乱

- 温度管理とコールドチェーン管理

- 市場機会

- 技術革新

- 市場促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- サービスタイプ別

- 保管

- 流通

- 在庫管理

- 包装

- その他

- モード別

- コールドチェーン倉庫

- 非コールドチェーン倉庫

- エンドユーザー別

- 製薬会社

- 病院・クリニック

- 研究機関と政府機関

- その他

第6章 競合情勢

- 企業プロファイル

- Sinopharm Logistics

- SF Express

- Kerry Logistics

- Yunda Holding

- CJ Rokin Logistics

- DHL Supply Chain

- DB Schenker

- Nippon Express

- Yamato Holdings

- CJ Rokin Logistics

- SF Express

- JD Logistics*

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 関連医薬品の輸出入統計

目次

The China Pharmaceutical Warehousing Market size is estimated at USD 14.33 billion in 2025, and is expected to reach USD 21.23 billion by 2030, at a CAGR of 8.17% during the forecast period (2025-2030).

Driven by biotechnology and innovative drug development, the Chinese pharmaceutical market is undergoing a significant transformation. This shift is largely propelled by strategic initiatives from the Chinese government, notably the "Healthy China 2030" plan, which seeks to bolster public health and champion scientific innovation.

China's biotechnology sector is on a rapid ascent, buoyed by hefty investments in research and development (R&D) and a supportive regulatory landscape. The market boasts a vibrant ecosystem where biotech startups, major pharmaceutical firms, and academic institutions collaborate, pushing the boundaries of medical research and pioneering new therapies.

A notable trend in China's biotechnology landscape is the infusion of artificial intelligence (AI) and big data analytics into drug development. Companies such as WuXi AppTec harness AI to refine drug discovery, streamline clinical trials, and bolster precision medicine strategies. Thanks to AI-driven platforms, WuXi AppTec has not only sped up the identification of promising drug candidates but also heightened the efficiency of its R&D endeavors.

Moreover, China's regulatory reforms, notably the expedited approval process for innovative drugs, have paved the way for swifter market entry of groundbreaking therapies, fostering an environment ripe for continuous innovation. The market is increasingly gravitating towards biosimilars and biopharmaceuticals, which not only provide cost-effective treatment alternatives but also broaden access to cutting-edge therapeutics.

Policies backing the expansion of digital health technologies have been rolled out by the Chinese government. Furthermore, initiatives such as the National Health Informatization Development Plan are working towards a unified health information system, seamlessly integrating data from diverse digital health platforms to boost data interoperability and healthcare coordination.

In June 2023, the FDA was contemplating a move to allow online pharmacies to dispense prescription drugs. This potential shift could pave the way for e-commerce giants like Alibaba and JD to tap into a burgeoning market. Discussions about this policy have been circulating since mid-last year, and its approval could unlock a market exceeding CNY 1 trillion (approximately USD 161 billion). Such a move would not only divert sales from traditional hospitals to online pharmacies but also challenge the longstanding dominance of state-run hospitals and distributors in the market.

The transformation of the Chinese pharmaceutical market also extends to the warehousing sector. With the rapid growth of the pharmaceutical industry, there is an increasing demand for advanced warehousing solutions to ensure the efficient storage and distribution of pharmaceutical products.

The Chinese pharmaceutical warehousing market is evolving to meet these needs, incorporating state-of-the-art technologies such as automated storage and retrieval systems (AS/RS), temperature-controlled environments, and real-time inventory management systems.

These advancements are crucial for maintaining the integrity and quality of pharmaceutical products throughout the supply chain. As the market continues to expand, the development of sophisticated warehousing infrastructure will play a pivotal role in supporting the overall growth and efficiency of the Chinese pharmaceutical industry.

China Pharmaceutical Warehousing Market Trends

Increase In Cold Chain Warehouse Development

In the first half of 2024, the volume of cold chain logistics hit 220 million tons, a rise of 4.4%. Concurrently, revenue from cold chain logistics climbed to CNY 277.9 billion (USD 38.9 billion), reflecting a 3.4% uptick compared to the same timeframe last year.

By June 2024, China's cold storage capacity expanded to 237 million cubic meters, showcasing a year-on-year growth of 7.73%. This year alone saw the addition of 9.42 million cubic meters in new cold storage capacity. In the first half of 2024, the leasing volume for cold storage across the nation surpassed 29 million cubic meters, marking an increase of over 8%.

The rising production and consumption of temperature-sensitive items, such as biologics, vaccines, and specialty drugs, underscore the need for expansive cold storage facilities. Biologics, unlike conventional drugs, are intricate substances sourced from biological entities, including humans and animals. These biological products encompass a wide spectrum, from vaccines to blood components.

Frequently utilized in advanced treatments, biologics exhibit heightened sensitivity to even minor fluctuations in their physical environment. Consequently, to cater to the surging demand for these products, pharmaceutical and healthcare firms must emphasize swift and dependable supply chain solutions.

In October 2024, the China National Medical Products Administration (NMPA) unveiled a pilot initiative permitting non-end-to-end manufacturing of biologics. Historically, the NMPA mandated that biologics undergo end-to-end production at a singular manufacturing site.

Essentially, this means both the drug substance and its corresponding product should ideally be produced within the same facility. However, the domestic biopharmaceutical sector has been pushing for a relaxation of this rule, particularly in light of the fact that foreign biologics manufacturers have been granted the leeway to produce the drug substance and its product at distinct locations.

The significant increase in cold chain warehouse development highlights the growing importance of efficient pharmaceutical warehousing in China. As the demand for temperature-sensitive products continues to rise, the expansion of cold storage facilities will play a crucial role in ensuring the integrity and availability of these critical products. This trend underscores the need for ongoing investment and innovation in cold chain logistics to support the pharmaceutical industry's evolving requirements.

Increase in Development of Pharmaceutical Manufactures

Chinese policymakers are actively working to attract foreign investment by relaxing regulations, a move aimed at fostering innovation. This marks a departure from their previous stance, which imposed restrictions on cross-border research and development. Notably, the government spotlighted "innovative drugs" in its work report for the first time this year. In 2023 alone, there were over 220 licensing and partnership deals for innovative drugs, amounting to a substantial RMB 266 billion (approximately USD 37 billion).

The Chinese government has rolled out several initiatives to bolster the healthcare sector and promote international collaboration. International players in the CGT arena are eyeing opportunities and considering actions like investments, establishing new entities, mergers, and acquisitions, or even relocating to four designated FTZs. These ventures span a wide array of CGT-related domains, from iPSCs and CAR-T to mRNA, gene sequencing, and in vitro diagnostics (IVD/LDT).

Thanks to the new Circular, biopharmaceutical firms in China can now directly draw foreign investments. By setting up or moving subsidiaries to the four FTZs, they sidestep the previously mandatory variable interest entity (VIE) structure.

In a significant move, an Indianapolis-based firm is set to invest a whopping USD 212 million in November 2024, expanding its Suzhou plant. This expansion will elevate its cumulative investment in Suzhou since 1996 to a staggering 15 billion yuan (USD 2.1 billion). This decision follows China's green light for its major weight loss drug, Zepbound, in July 2024. Shortly after, the firm launched a medical innovation center in Beijing and announced plans for a Gateway Labs, marking its inaugural innovation incubator outside the U.S.

In September 2024, Bayer, the German pharmaceutical giant, inaugurated a life science incubator in Shanghai, lauding China's innovation prowess as "among the world's top two." Just a month earlier, Roche Diagnostics, a Swiss behemoth's division, unveiled a massive USD 420 million project - its largest investment to date - to enhance its manufacturing facility in Suzhou.

These strategic investments shine a light on a unique opportunity within the Chinese market. Despite challenges like an economic slowdown, stiff domestic competition, and geopolitical strains causing hesitance in sectors from tech to automotive, the pharmaceutical realm remains a beacon. Many foreign entities still perceive avenues for profit and fruitful collaborations with local biotechs.

Part of Beijing's initiative to liberalize the healthcare sector is driven by a desire to ensure its aging populace has access to premier global medicines. This liberalization has also spurred an increase in the development of pharmaceutical manufacturing facilities, significantly impacting the Chinese pharmaceutical warehousing market.

China Pharmaceutical Warehousing Industry Overview

China's pharmaceutical warehousing market is one of the most competitive and fastest-growing in the world. It is due to the country's growing healthcare sector, growing pharmaceutical manufacturing, and changing distribution strategies. As the pharmaceutical industry in China continues to grow, companies that can provide seamless warehousing, effective distribution, and cutting-edge solutions will gain a competitive advantage in this highly competitive market. The market is highly fragmented, with many local and International players operating in the market, such as Sinopharm Logistics, DHL, CJ Rokin Logistics, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview (Current Market Scenario of Market and Economy)

- 4.2 Government Regulations and Initiatives

- 4.3 Technological Trends

- 4.4 Market Dynamics

- 4.4.1 Market Drivers

- 4.4.1.1 Rapidly Expanding Pharmaceutical Industry

- 4.4.1.2 Population Growth is one of the main drivers for the warehousing market

- 4.4.2 Market Restraints/ Challenges

- 4.4.2.1 Supply Chain Disruptions

- 4.4.2.2 Temperature Controlled and Cold Chain Management

- 4.4.3 Market Opportunities

- 4.4.3.1 Technological Innovations

- 4.4.1 Market Drivers

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Powers of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Storage

- 5.1.2 Distribution

- 5.1.3 Inventory Management

- 5.1.4 Packaging

- 5.1.5 Others

- 5.2 By Mode

- 5.2.1 Cold Chain Warehouse

- 5.2.2 Non-Cold Chain Warehouse

- 5.3 By End User

- 5.3.1 Pharmaceutical Companies

- 5.3.2 Hospital and Clinics

- 5.3.3 Research Institiutes and Government Agencies

- 5.3.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Sinopharm Logistics

- 6.2.2 SF Express

- 6.2.3 Kerry Logistics

- 6.2.4 Yunda Holding

- 6.2.5 CJ Rokin Logistics

- 6.2.6 DHL Supply Chain

- 6.2.7 DB Schenker

- 6.2.8 Nippon Express

- 6.2.9 Yamato Holdings

- 6.2.10 CJ Rokin Logistics

- 6.2.11 SF Express

- 6.2.12 JD Logistics*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, By Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 Export and Import Statistics of Related Pharmaceutical Products

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日