|

市場調査レポート

商品コード

1644988

アジア太平洋の水中ポンプ:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia Pacific Submersible Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の水中ポンプ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

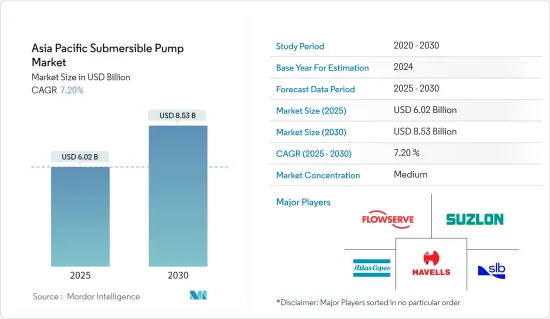

アジア太平洋の水中ポンプ市場規模は2025年に60億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.2%で、2030年には85億3,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、エンドユーザー産業への投資の増加が市場の成長を牽引すると予想されます。

- 一方、高いメンテナンス・運転コストと石油・ガス価格の変動が、予測期間中のアジア太平洋水中ポンプ市場の成長を妨げると予想されます。

- 改修、老朽化した既存インフラのアップグレード、新技術の革新は、予測期間中にアジア太平洋水中ポンプ市場に有利な成長機会を生み出す可能性が高いです。

- 中国が市場を独占しており、予測期間中に最も高いCAGRで推移する可能性も高いです。この成長は、エンドユーザー産業における投資の増加と政府の支援施策によるものです。

アジア太平洋の水中ポンプ市場動向

石油・ガス産業で大きな需要が見込まれる

- 石油・ガス上流産業では、水中ポンプは、使用済みの掘削泥を埋蔵ピットから出し入れし、人工揚水によって石油・ガス生産を最大化し、生産された廃水を処理するために使用されます。

- 水中ポンプの需要は、主に産業の低迷により過去数年間不安定でした。しかし、原油価格の回復と低い損益分岐点価格が、予測期間中の市場における生産活動の原動力となっています。

- 2022年には、中国が7.99エクサジュール生産し、アジア太平洋で最大の天然ガス生産国となりました。同年、オーストラリアは約5.5エクサジュールの天然ガスを生産し、同地域で2番目に大きな生産国でした。

- アジア太平洋の石油・ガス産業は、生産効率の改善や新規鉱区の立ち上げなど、数多くの開発を目の当たりにしており、2021年の天然ガス生産量は前年比1.6%増加しました。また、単位操業コストは今後数年間で低下すると予想されます。

- 2021年6月、CNOOCの深海ガス田は日産1,000万立方メートルの生産能力を開始しました。このガス田は霊水17-2とも呼ばれ、南シナ海の海面下1,500メートルに位置します。このガス田は年間30億立方メートルのガスを供給することができ、これは中国のガス需要のおよそ1%に相当します。

- 2021年9月、CNOOCは渤海湾でケンリ10-2油田を発見したと発表しました。ケンリ10-2油田は渤海湾南部の莱州湾サグに位置し、平均水深は約50フィートです。

- 2022年現在、インドでは77基のリグが稼動しています。同国の石油生産量は、油田の老朽化と大発見の不在により、ほぼ10年間減少し続けています。国営企業も民間企業も、古い油田からの回収率を上げるための投資計画に取り組んでいます。

- したがって、上記の要因やプロジェクトに基づいて、石油・ガス産業は、予測期間にわたってアジア太平洋の水中ポンプ市場に大きな需要を確認すると予想されます。

市場を独占する中国

- 中国は、世界の製造業の成長に不可欠な要因となっています。同国は鉱業と建設産業のリーダーであり、石油・ガスのトップ参入企業でもあります。COVID-19の発生にもかかわらず、同国の工業部門は2020年4月以降3%以上の成長を記録しており、2021年1月には過去最高の35.1%に達しました。中国国家統計局によると、2021年、中国の工業生産は前年比9.6%増加しました。

- 2022年、中国の原油生産量は約2億400万トンでした。原油生産量は前年比で2.5%増加しました。

- 中国は、こうした都市部や農村部に必要なインフラの拡大に力を入れており、これが今後数年間の水中ポンプ需要にプラスの影響を与えると予想されます。水中ポンプ市場は、石油・ガス、廃水処理、鉱業・建設、その他の産業の成長によって牽引されると予想されます。

- 中国は産業活動の増加を目の当たりにしており、それによって原油や化学品などの需要が伸びています。中国は、アジア太平洋における2019~2025年にかけての原油精製能力の大幅な伸びを占めると予想されます。同国は、2025年までに同地域の総精製拡大能力の26.8%を占めると予想されます。これは、同地域の水中ポンプ市場の需要に貢献する可能性が高いです。

- 中国は、シェールガスのような非在来型資源の国内生産を促進することを目標としています。中国のシェールガス生産量は、2035年までに約2,800億立方メートル(bcm)に達するとも推定されています。そのため、シェールガスの生産量を増やす計画は、今後数年間で機会を生み出すと期待されています。

- 2021年2月、中国海洋石油(CNOOC)は総額139億1,000万~154億6,000万米ドル、原油換算生産量5億4,500万~5億5,500万バレル(Mboe)を目標に設備投資を行うと発表しました。

- シノペックは2021年3月、中国南西部でのシェールガス開発と沿岸部での液化天然ガス(LNG)基地建設を中心に、上流探査に92億8,000万米ドルを投資すると発表しました。

- したがって、このような開発に基づき、予測期間中、中国がアジア太平洋水中ポンプ市場を独占すると予想されます。

アジア太平洋水中ポンプ産業概要

アジア太平洋の水中ポンプ市場は半分断されています。同市場の主要企業(順不同)には、Schlumberger Limited、Sulzer AG、Flowserve Corporation、Atlas Copco AB、Havells India Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- ボアウェル水中ポンプ

- オープンウェル水中ポンプ

- ノンクロッグ水中ポンプ

- 駆動タイプ

- トラック

- 電動式

- 油圧式

- その他

- ヘッド

- 50m以下

- 50~100 m

- 100m以上

- エンドユーザー

- 上下水道

- 石油・ガス産業

- 鉱業と建設業

- その他

- 地域

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Baker Hughes Co.

- Schlumberger Limited

- Halliburton Co.

- Weir Group PLC

- Sulzer AG

- Flowserve Corporation

- Atlas Copco AB

- Crompton Greaves Consumer Electricals Limited

- Havells India Ltd.

- Falcon Pumps Pvt. Ltd.

- Shimge Pump Industry Group Co., Ltd.

第7章 市場機会と今後の動向

目次

Product Code: 5000238

The Asia Pacific Submersible Pump Market size is estimated at USD 6.02 billion in 2025, and is expected to reach USD 8.53 billion by 2030, at a CAGR of 7.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, increasing investments in end-user industries are expected to drive the market's growth.

- On the other hand, high maintenance and operation costs and volatility in oil and gas prices are expected to hamper the Asia-Pacific submersible pump market growth during the forecast period.

- Nevertheless, retrofitting, upgrading aging, existing infrastructure, and new technology innovations will likely create lucrative growth opportunities for the Asia-Pacific submersible pump market in the forecast period.

- China dominates the market, and it is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the increasing investments and supportive government policies in the end-user industries.

Asia Pacific Submersible Pump Market Trends

Oil and Gas Industry to Witness Significant Demand

- In the oil and gas upstream industry, submersible pumps are used to move spent drilling mud in and out of the reserve pits, maximizing oil and gas production through the artificial lift and treating the produced wastewater.

- The demand for submersible pumps has been volatile in the past few years, mainly due to the downturn in the industry. However, the recovery in crude oil price and the low breakeven price drive the production activity in the market during the forecast period.

- In the year 2022, China was the largest producer of natural gas in the Asia-Pacific region with a production of 7.99 exajoules. In the same year, Australia produced around 5.5 exajoules of natural gas, making it the second biggest producer in the region.

- The oil and gas industry in the Asia Pacific region has witnessed numerous developments, such as production efficiency improvements and new fields startup, the natural gas production increased by 1.6% in 2021 compared to the previous year. Also, unit operating costs are expected to decline in the coming years.

- In June 2021, CNOOC's deepwater gas field commenced production capacity of 10 million cubic meters daily. The gas field, also named Lingshui 17-2, sits 1,500 meters below the sea surface in the South China Sea. The field will be able to supply 3 billion cubic meters of gas a year, or roughly 1% of China's gas demand.

- In September 2021, CNOOC Limited announced the discovery of Kenli 10-2 oilfield in Bohai Bay. The Kenli 10-2 oilfield is located in Laizhou Bay Sag in Southern Bohai Bay, with an average water depth of about 50 feet.

- As of 2022, India has 77 active rigs. The country's oil production has been falling for almost a decade due to aging fields and the absence of major discoveries. Both state-owned and private players have been working on investment plans to raise recovery from older fields.

- Therefore, based on the factors and projects mentioned above, the oil and gas industry is expected to witness significant demand for the submersible pump market in the Asia Pacific over the forecast period.

China to Dominate the Market

- China has been an essential factor in the growth of the manufacturing sector worldwide. The country is the leader in the mining and construction industries and is a top oil and gas player. Despite the outbreak of COVID-19, the industrial sector in the country has been registering a growth of over 3% since April 2020, reaching an all-time high of 35.1% in January 2021. As per the National Bureau of Statistics of China, in 2021, China's industrial production increased by 9.6% compared to the previous year.

- In 2022, Crude oil production in China was approximately 204 million tons. Crude oil production has witnessed a 2.5% increase compared to the previous year.

- China is committed to expanding the infrastructure required for these urban and rural areas, which is expected to positively impact the demand for submersible pumps in the coming years. The submersible pump market is expected to be driven by growth in oil and gas, wastewater treatment, mining and construction, and other industries.

- China is witnessing an increase in industrial activities, thereby inducing growth in demand for crude oil and chemicals, among others. China is expected to account for significant crude oil refining capacity growth between 2019 and 2025 in Asia-Pacific (APAC). The country is expected to account for 26.8% of the total refining expansion capacity in the region by 2025. This will likely contribute to the region's market demand for submersible pumps.

- China targets to boost domestic production of unconventional sources like shale gas. It is also estimated that China's shale gas production may reach around 280 billion cubic meters (bcm) by 2035. Thus, the plans to boost its shale gas production are expected to create an opportunity in the coming years.

- In February 2021, CNOOC announced total capital expenditure in the range of USD 13.91 billion to USD 15.46 billion, with targeted net production of 545-555 million barrels of oil equivalent (Mboe).

- In March 2021, Sinopec announced to invest USD 9.28 billion in upstream exploration, focusing on shale gas development in southwest China and the construction of liquefied natural gas (LNG) terminals in coastal areas.

- Therefore, based on such developments, China is expected to dominate the Asia Pacific submersible pump market during the forecast period.

Asia Pacific Submersible Pump Industry Overview

The Asia-Pacific submersible pump market is semi-fragmented. Some of the major players in the market (in no particular order) include Schlumberger Limited, Sulzer AG, Flowserve Corporation, Atlas Copco AB, and Havells India Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Borewell Submersible Pump

- 5.1.2 Openwell Submersible Pump

- 5.1.3 Non-clog Submersible Pump

- 5.2 Drive Type

- 5.2.1 Truck

- 5.2.2 Electric

- 5.2.3 Hydraulic

- 5.2.4 Other Drive Types

- 5.3 Head

- 5.3.1 Below 50 m

- 5.3.2 Between 50 m to 100 m

- 5.3.3 Above 100 m

- 5.4 End User

- 5.4.1 Water and Wastewater

- 5.4.2 Oil and Gas Industry

- 5.4.3 Mining and Construction Industry

- 5.4.4 Other End Users

- 5.5 Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 South Korea

- 5.5.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Baker Hughes Co.

- 6.3.2 Schlumberger Limited

- 6.3.3 Halliburton Co.

- 6.3.4 Weir Group PLC

- 6.3.5 Sulzer AG

- 6.3.6 Flowserve Corporation

- 6.3.7 Atlas Copco AB

- 6.3.8 Crompton Greaves Consumer Electricals Limited

- 6.3.9 Havells India Ltd.

- 6.3.10 Falcon Pumps Pvt. Ltd.

- 6.3.11 Shimge Pump Industry Group Co., Ltd.