欧州の直接メタノール燃料電池:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Direct Methanol Fuel Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644977

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

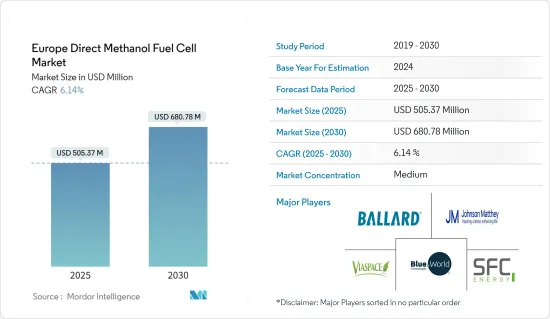

欧州の直接メタノール燃料電池市場規模は、2025年に5億537万米ドルと推定され、予測期間中(2025-2030年)のCAGRは6.14%で、2030年には6億8,078万米ドルに達すると予測されます。

主なハイライト

- 中期的には、政府のイニシアティブと民間投資の増加が市場の成長を牽引すると予想されます。

- 一方、リチウムイオン電池の価格低下とリチウムイオン電池ベースのアプリケーションの増加は、予測期間中の欧州の直接メタノール燃料電池市場の成長を妨げると予想されます。

- とはいえ、燃料電池の需要を創出する将来的な目標は、予測期間中に欧州の直接メタノール燃料電池市場に有利な成長機会を生み出す可能性が高いです。

欧州の直接メタノール燃料電池市場動向

政府のイニシアティブと民間投資の増加

直接メタノール燃料電池市場は、過去2年間に著しい成長を遂げたが、これは主に主要市場における政府のイニシアティブのイントロダクションと民間部門からの投資支援の増加によるものです。

ドイツは欧州で最も多くの水素燃料ステーションを有しています。2022年9月現在、93カ所の水素ステーションが稼働しています。次いでフランスが21カ所です。

2017年6月、エリザベス女王は「自動運転・電気自動車法案」のイントロダクションを発表しました。同法案は、燃料電池車と水素インフラへの資金援助を拡大することを求めました。法案導入後、同国の水素・燃料電池産業は目覚ましい発展を遂げています。さらに2020年2月、政府は水素製造に焦点を当てた5つのプロジェクトに3,000万米ドルの資金提供を発表しました。

欧州では、2020年までに5カ国で139台のゼロ・エミッション燃料電池バスと燃料補給インフラの導入を目指すJIVE(水素自動車共同イニシアティブ)が市場を牽引しています。JIVEは2017年1月に開始され、燃料電池・水素共同事業体(FCH JU)からの3,400万米ドルの助成金が共同出資されています。このプロジェクト・コンソーシアムには、7カ国から22のパートナーが参加しています。

さらに、2018年1月にはJIVE2が開始され、JIVE2プロジェクトを合わせると、2020年代初頭までに欧州の22都市に約300台の燃料電池バスを配備する予定です。

さらに2020年1月には、PEM燃料電池の出力密度を向上させる新たなプロジェクトが、2つの運輸OEM(Fuel Cell PowertrainとBMW)、燃料電池中東・アフリカ・サプライヤー(Johnson Matthey Fuel Cells)、1つの研究機関(SINTEF)、2つの大学機関(ケムニッツ工科大学とフライブルク大学IMTEK)で構成されるコンソーシアムによって開始されました。

プロジェクトの目的は、自動車用新世代PEM燃料電池の中東・アフリカ(Membrane Electrode Assemblies)における電荷・質量・熱輸送メカニズムを理解することです。プロジェクトの資金は250万米ドルで、2020年から2022年にかけて実施されます。

2021年1月、ジョンソン・マッセイ(JM)は、据置型および移動型のハイブリッド電源ソリューション用水素・直接メタノール燃料電池の世界的リーダーであるSFCエナジーAG(SFC)に、40万個の直接メタノール型MEA(膜電極接合体)燃料電池部品を提供する新たな数百万ポンドの契約を獲得しました。この契約は2021年2月から3年以上の期間とされています。

したがって、政府のイニシアティブと民間投資の増加が、今後数年間、欧州の直接メタノール燃料電池市場を牽引すると予想されます。

市場を独占するドイツ

ドイツは、国内の温室効果ガス排出量を削減しながら、燃料電池電気バスの導入を推進しています。地域交通局であるRegionalverkehr Kolnは、30台のFCEBと2基の水素補給ステーション(HRS)を購入するために、政府から790万米ドルを獲得しました。同国はまた、2030年末までに1000カ所のステーション配備を推進することを目指しています。このような取り組みにより、今後数年間、同地域での燃料電池の展開が大きく後押しされることが期待されます。

水素協議会の統計によれば、2020年の欧州における燃料電池電気自動車(FCEV)の保有台数は約1,300台でした。予測では、この数は2030年までに400万台を超える可能性があります。

ドイツ政府が2020年6月に承認した「国家水素戦略」は、水素によるエネルギー生成を通じて排出量を削減する世界的責任を担うことを目的としており、主に水素の競争力を高め、コスト削減を推進し、水素を代替エネルギーキャリアとして確立することを目指しています。

同戦略はまた、化石エネルギーに基づく現在の生産を再生可能エネルギーに転換することにより、水素を産業の持続可能性のための原料として確立することを目指すとともに、2030年までに産業規模のソリューションを体系的に応用できるようにするため、調査や有資格者の育成を支援します。

2021年7月、SFCエナジーAGは次世代水素燃料電池ソリューションの発売を発表しました。EFOY水素燃料電池2.5パワーソリューションは、信頼性が高く、堅牢で、環境に優しい発電形態と、可能な限り高い接続性と使いやすさを兼ね備えています。

そのため、ドイツが打ち出した様々な政府イニシアティブにより、予測期間中、欧州が直接メタノール燃料電池市場を独占すると予想されます。

欧州の直接メタノール燃料電池産業概要

欧州の直接メタノール燃料電池市場は、適度に統合されています。同市場の主要企業(順不同)には、Blue World Technologies ApS、Johnson Matthey、SFC Energy AG、Viaspace Inc.、Ballard Power Systems Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 政府のイニシアティブと民間投資の増加

- 抑制要因

- リチウムイオン電池価格の下落

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 地域

- 英国

- フランス

- イタリア

- ドイツ

- その他欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Blue World Technologies ApS

- Johnson Matthey

- SFC Energy AG

- Viaspace Inc.

- Ballard Power Systems Inc.

- MeOH Power, Inc.

- Oorja Protonics Inc.

- Horizon Fuel Cell Technologies

- TreadStone Technologies, Inc.

- Fujikura Ltd.

第7章 市場機会と今後の動向

- 地域の燃料電池需要を創出する将来のターゲット

目次

The Europe Direct Methanol Fuel Cell Market size is estimated at USD 505.37 million in 2025, and is expected to reach USD 680.78 million by 2030, at a CAGR of 6.14% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, government initiatives and increasing private investments are expected to drive the market's growth.

- On the other hand, declining lithium-ion battery prices and an increase in lithium-ion battery-based applications are expected to hamper the growth of Europe's direct methanol fuel cell market during the forecast period.

- Nevertheless, future targets creating fuel cell demand will likely create lucrative growth opportunities for the Europe direct methanol fuel cell market in the forecast period.

Europe Direct Methanol Fuel Cell Market Trends

Government Initiatives and Increasing Private Investments

The direct methanol fuel cell market witnessed significant growth in the last two years, mainly due to the introduction of government initiatives in key markets and increasing investment support from the private sector.

Germany has the most significant number of hydrogen fuel stations in Europe. As of September 2022, 93 operational hydrogen refueling stations were in the country. This was followed by France, with 21 such stations.

In June 2017, Queen Elizabeth II announced the introduction of the 'Automated and Electric Vehicles Bill.' The bill called for greater funding for fuel cell vehicles and hydrogen infrastructure. After the bill's introduction, the country's hydrogen and fuel cell industry has seen impressive developments. Furthermore, in February 2020, the government announced USD 30 million in funding for five projects focused on hydrogen production.

In Europe, the market is driven by the JIVE (Joint Initiative for Hydrogen Vehicles), which seeks to deploy 139 new zero-emission fuel cell buses and refueling infrastructure across five countries by 2020. The JIVE started in January 2017 and is co-funded by USD 34 million grant from the Fuel Cells and Hydrogen Joint Undertaking (FCH JU). The project consortium involves 22 partners from seven countries.

Further, JIVE2 started in January 2018, and on a combined basis, the JIVE2 projects are expected to deploy around 300 fuel cell buses in 22 cities across Europe by the early 2020s.

Moreover, a new project in January 2020 to improve the power density of PEM fuel cells was taken up by the consortium consisting of two transport OEMs (Fuel Cell Powertrain and BMW), a fuel cell MEA supplier (Johnson Matthey Fuel Cells), one research institute (SINTEF) and two university institutes (Chemnitz University of Technology and IMTEK at the University of Freiburg).

The project's objective consists of understanding the charge, mass, and heat transport mechanism in new generation PEM fuel cell MEA (Membrane Electrode Assemblies) for automotive applications. The project has funding of USD 2.5 million and will run from 2020-2022.

In January 2021, Johnson Matthey (JM), has won a new multi-million-pound agreement to provide 400,000 Direct Methanol MEA (Membrane Electrode Assemblies) fuel cell components to SFC Energy AG (SFC), a global leader of hydrogen and direct methanol fuel cells for stationary and mobile hybrid power solutions. The agreement is considered from February 2021 for a duration of over three years.

Therefore, government initiatives and increasing private investments are expected to drive the Europe direct methanol fuel cell market in the coming years.

Germany to Dominate the Market

Germany is promoting the deployment of fuel cell electric buses in conformation while reducing the GHG emission in the country. The regional transport authority, Regionalverkehr Koln, was awarded USD 7.9 million by the government to purchase 30 FCEBs and two hydrogen refueling stations (HRS). The country also aims to promote the deployment of 1000 stations by the end of 2030. Such initiatives are expected to significantly support the deployment of fuel cells in the region in the coming years.

As per Hydrogen Council statistics, there were about 1,300 fuel cell electric vehicles (FCEVs) in the European fleet in 2020. Projections indicate that this number could exceed four million units by 2030.

Germany's National Hydrogen Strategy, which the government approved in June 2020, aims to assume global responsibility for reducing emissions through energy generation from hydrogen, primarily by making hydrogen competitive, pushing cost reductions, and establishing hydrogen as an alternative energy carrier.

The strategy also aims to establish hydrogen as a raw material for industry sustainability by switching current production based on fossil energies to renewable energies while supporting research and training qualified personnel to get industrial-scale solutions to application maturity by 2030 systematically.

In July 2021, SFC Energy AG announced the launch of the next generation of its hydrogen fuel cell solution. The EFOY Hydrogen Fuel Cell, 2.5 power solution, combines a reliable, robust, and environmentally friendly form of power generation with the highest possible connectivity and ease of use.

Therefore, with various government initiatives launched by Germany, Europe is expected to dominate the direct methanol fuel cell market during the forecast period.

Europe Direct Methanol Fuel Cell Industry Overview

The Europe Direct Methanol Fuel Cell Market is moderately consolidated in nature. Some of the major players in the market (in no particular order) include Blue World Technologies ApS, Johnson Matthey, SFC Energy AG, Viaspace Inc., and Ballard Power Systems Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Initiatives and Increasing Private Investments

- 4.5.2 Restraints

- 4.5.2.1 Declining Lithium-ion Battery Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 United Kingdom

- 5.1.2 France

- 5.1.3 Italy

- 5.1.4 Germany

- 5.1.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Blue World Technologies ApS

- 6.3.2 Johnson Matthey

- 6.3.3 SFC Energy AG

- 6.3.4 Viaspace Inc.

- 6.3.5 Ballard Power Systems Inc.

- 6.3.6 MeOH Power, Inc.

- 6.3.7 Oorja Protonics Inc.

- 6.3.8 Horizon Fuel Cell Technologies

- 6.3.9 TreadStone Technologies, Inc.

- 6.3.10 Fujikura Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Targets Creating Fuel Cell Demand in the Region

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日