|

市場調査レポート

商品コード

1644953

中東のパイプライン保守:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Middle East Pipeline Maintenance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東のパイプライン保守:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

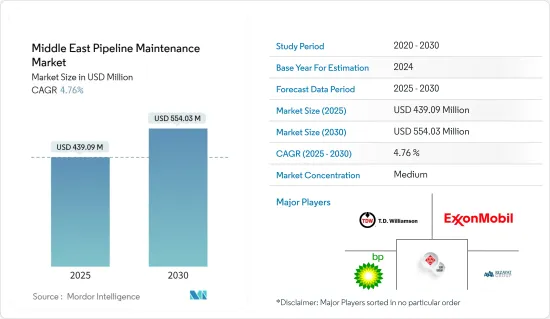

中東のパイプライン保守の市場規模は、2025年に4億3,909万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.76%で、2030年には5億5,403万米ドルに達すると予測されます。

市場は2020年のCOVID-19によってマイナスの影響を受けました。現在、市場はパンデミック以前の水準に達しています。

主なハイライト

- 中期的には、パイプラインインフラの老朽化、国内天然ガス需要の増加、非在来型埋蔵量開拓による石油・ガス生産の増加が、調査対象市場の成長を牽引すると予想されます。

- 一方、原油価格の変動が大きいことは、市場にとって大きな抑制要因のひとつです。

- とはいえ、オフショア探査・生産プロジェクトの増加は、予測期間中、市場プレーヤーに絶好の機会をもたらすと予想されます。これらのプロジェクトは、パイプライン産業がさらに成長する道を開いています。

中東のパイプライン保守市場動向

ピギングセグメントが市場で大きなシェアを占める

- ピギングとは、パイプラインの保守・運用に用いられる一般的な技術です。パイプライン内で様々な機能を果たすために、「ピグ」と呼ばれる特殊な装置を使用します。これらのピグは通常、円筒形または球形で、パイプラインに挿入され、製品の流れまたは圧縮空気や油圧などの外部手段によって推進され、パイプライン内を移動します。

- 養豚は、中東のパイプライン保守において、いくつかの地域特有の要因から、支配的なセグメントになると考えられています。中東には老朽化したパイプラインインフラが存在するため、定期的なメンテナンスと清掃が必要となり、ピギングが不可欠な技術となっています。この地域は石油・ガス生産と輸送の主要なハブであるため、中東のパイプラインは長距離にわたって大量の炭化水素を扱います。ピギングは、これらのパイプラインの流量効率と完全性を維持し、運転効率を最適化し、混乱を最小限に抑える上で重要な役割を果たしています。

- よりクリーンなエネルギー源として中東で天然ガスの需要が増加していることも、パイプライン保守におけるピギングの重要性を高めています。天然ガスパイプラインは、効率的で安全なガス輸送を確保するため、洗浄、保守、点検のための定期的なピギングを必要とします。

- 例えば、2022年11月、イラン石油相は、同省がガス田やガス輸出トランスミッション・ラインの開発とともに、国内のLNGコンプレックス建設のためにガスプロムと400億米ドル相当の協力協定を締結したと発表しました。

- さらに、この地域ではパイプラインの建設が増加傾向にあります。例えば、世界・エネルギー・モニターによると、2023年5月現在、イランは6,000km以上の石油パイプラインを、サウジアラビアは4,600km以上の石油パイプラインを運営しています。

- したがって、上記の点から、パイプライン保守インフラへの投資の増加が、予測期間中の市場を牽引することになります。

サウジアラビアはパイプライン保守市場で最も急成長している地域

- サウジアラビアは世界第2位の原油生産国で、2021年の中東原油生産量の約12.5%を占める。また、世界最大の原油輸出国のひとつでもあります。さらにサウジアラビアは、2020年にはベネズエラに次いで世界第2位の確認埋蔵量を占める。

- サウジアラビアの大規模な炭化水素生産と輸出活動を支えるパイプラインの広範なネットワークにより、石油・ガスインフラを拡大するための継続的な投資により、メンテナンスの必要性が高まることが予想されます。サウジアラビアの多くのパイプラインは老朽化しているため、漏れや腐食などの問題を軽減するための定期的なメンテナンスと修理の必要性がさらに強調されています。世界・エネルギー・モニターによると、2023年5月現在、サウジアラビアでは86.2kmの石油パイプラインが建設中です。

- サウジアラビアの野心的な生産・輸出目標も、パイプライン保守の需要増加の一因となっています。パイプライン・ネットワークの信頼性と完全性は、これらの目標を達成するために不可欠であり、検査、清掃、修理などの積極的なメンテナンス対策が必要となります。さらに、砂漠、山岳地帯、沖合など、サウジアラビアには多様な地理的課題が存在するため、パイプライン保守には専門的な専門知識と設備が必要です。

- 2020年、サウジアラビアは乾式天然ガス生産量のマイルストーンを達成し、1日平均110億立方フィートに達しました。これは2010年の生産水準と比較して30%の大幅な増加となった。

- 2021年現在、国営石油会社サウジアラムコは、国内全域で90以上のパイプラインと12,000マイルの原油・石油製品パイプラインを運営し、これらすべてが生産地域と処理施設、輸出ターミナル、消費センターを結んでいます。

- さらに、ロシアとウクライナの紛争により、同地域からの天然ガスの供給が増加し、パイプラインの需要が高まり、その結果、パイプライン保守・サービスの需要が高まっています。

- 例えば2022年11月、サウジアラビアはバングラデシュへのLNG商業供給を緊急支援すると発表しました。この保証は、サウジアラビア・バングラデシュ合同経済委員会の第14回会合で発表されました。

- 以上のことから、サウジアラビアは予測期間中、パイプライン保守市場で大きな市場成長が見込まれます。

中東のパイプライン保守産業概観

中東のパイプライン保守市場は統合されています。この市場の主要企業(順不同)には、T.D. Williamson、Exxon Mobil、BP PLC、Rezayat Group、EEW Groupなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- パイプラインインフラの拡大

- エネルギー需要の拡大

- 抑制要因

- パイプラインインフラに対する政情不安と武装勢力による攻撃

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービスタイプ

- ピギング

- フラッシング・化学洗浄

- パイプラインの修理とメンテナンス

- 乾燥

- その他

- 配備場所

- 陸上

- オフショア

- 地域

- アラブ首長国連邦

- サウジアラビア

- カタール

- その他中東地域

第6章 競争情勢

- 合併、買収、提携、合弁事業

- 主要企業の戦略

- 企業プロファイル

- パイプラインオペレーター

- ExxonMobil Corporation

- BP PLC

- Saudi Aramco

- Egyptian General Petroleum Corporation

- Chevron Corporation

- パイプライン保守サービスプロバイダー

- Arabian Pipes Company

- Abu Dhabi Metal Pipes & Profiles Industries Complex LLC

- Rezayat Group

- Vallourec SA

- STATS Group

- Halliburton Company

- EEW Group

- T. D. Williamson Inc

- パイプラインオペレーター

第7章 市場機会と今後の動向

- パイプライン保守におけるデジタル技術と自動化の採用

The Middle East Pipeline Maintenance Market size is estimated at USD 439.09 million in 2025, and is expected to reach USD 554.03 million by 2030, at a CAGR of 4.76% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, aging pipeline infrastructure, increasing domestic natural gas demand, and the increase in oil and gas production caused by unconventional reserve development is expected to drive the growth of the market studied.

- On the other hand, the high volatility of crude oil prices is one of the major restraints for the market.

- Nevertheless, the rise in offshore exploration and production projects is expected to create an excellent opportunity for the market players in the forecast period. These projects are paving the way for the pipeline industry to grow more.

Middle East Pipeline Maintenance Market Trends

Pigging Segment to have a Significant Share in the Market

- Pigging is a common technique used in pipeline maintenance and operations. It involves the use of specialized devices called "pigs" to perform various functions within the pipeline. These pigs are typically cylindrical or spherical in shape and are inserted into the pipeline to travel through it, propelled by the flow of the product or by external means such as compressed air or hydraulic pressure.

- Pigging is poised to be a dominant segment in Middle East pipeline maintenance due to several region-specific factors. The presence of aging pipeline infrastructure in the Middle East necessitates regular maintenance and cleaning, making pigging an essential technique. With the region being a major hub for oil and gas production and transportation, pipelines in the Middle East handle high volumes of hydrocarbons over long distances. Pigging plays a critical role in maintaining these pipelines' flow efficiency and integrity, optimizing operational efficiency, and minimizing disruptions.

- The increasing demand for natural gas in the Middle East as a cleaner energy source also contributes to the prominence of pigging in pipeline maintenance. Natural gas pipelines require regular pigging for cleaning, maintenance, and inspection to ensure efficient and safe gas transportation.

- For instance, in November 2022, the Iranian Petroleum Minister announced that his ministry had signed a cooperation agreement worth USD 40 billion with Gazprom for the construction of LNG complexes in the country, along with the development of gas fields and gas export transmission lines.

- Moreover, the construction of pipelines are on a rise in the region for instance, according to global energy monitor, as of May 2023, Iran is operating more than 6,000 KM oil pipeline, and Saudi Arabia is operating more than 4,600 KM oil pipeline

- Hence, owing to the above points, increasing investment in Pipeline Maintenance infrastructure will drive the market during the forecast period.

Saudi Arabia is the fastest growing region in the Pipeline Maintenance market

- Saudi Arabia is the world's second-largest crude oil producer, accounting for about 12.5% of the Middle East crude oil produced in 2021. The country is also one of the largest crude oil exporters in the world. Moreover, Saudi Arabia accounted for the second-largest proven oil reserves in the world, after Venezuela, in 2020.

- With an extensive network of pipelines supporting the country's substantial hydrocarbon production and export activities, Saudi Arabia's ongoing investments in expanding its oil and gas infrastructure will necessitate increased maintenance requirements. The aging nature of many pipelines in the country further emphasizes the need for regular maintenance and repairs to mitigate issues like leaks and corrosion. According to global energy monitor, as of May 2023, Saudi Arabia has 86.2 kms oil pipe line unde construction.

- Saudi Arabia's ambitious production and export targets also contribute to the rising demand for pipeline maintenance. The reliability and integrity of the pipeline network are vital in achieving these targets, necessitating proactive maintenance measures such as inspections, cleaning, and repairs. Additionally, the diverse geographical challenges present in the country, including deserts, mountains, and offshore areas, require specialized expertise and equipment for pipeline maintenance.

- In 2020, Saudi Arabia achieved a milestone in its dry natural gas production, reaching an average of 11 billion cubic feet per day. This marked a significant 30% increase compared to the production levels of 2010.

- As of 2021, Saudi Aramco, the national oil company, operated more than 90 pipelines and 12,000 miles of crude oil and petroleum product pipelines throughout the country, all of which linked the production areas to the processing facilities, export terminals, and consumption centers.

- Furthermore, due to the Russia-Ukraine conflict, the supply of natural gas has increased from the region, increasing the demand for pipelines, consequently increasing the demand for pipeline maintenance services.

- For instance, in November 2022, Saudi Arabia announced that it would assist with the commercial supply of LNG to Bangladesh on an emergency basis. This assurance came during the 14th meeting of the Joint Economic Commission of Saudi Arabia and Bangladesh

- Hence, owing to the above points, Saudi Arabia is expected to see significant market growth in the Pipeline Maintenance market during the forecast period.

Middle East Pipeline Maintenance Industry Overview

The Middle East Pipeline Maintenance market is consolidated. Some of the key players in this market (in no particular order) included are T.D. Williamson, Exxon Mobil, BP PLC, Rezayat Group, and EEW Group., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Expanding Pipeline Infrastructure

- 4.5.1.2 Growing Energy Demand

- 4.5.2 Restraints

- 4.5.2.1 Political Instability and Militant Attacks on Pipeline Infrastructure

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Service Type

- 5.1.1 Pigging

- 5.1.2 Flushing & Chemical Cleaning

- 5.1.3 Pipeline Repair & Maintenance

- 5.1.4 Drying

- 5.1.5 Others

- 5.2 Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Geography

- 5.3.1 United Arab Emirates

- 5.3.2 Saudi Arabia

- 5.3.3 Qatar

- 5.3.4 Rest of Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Pipeline Operators

- 6.3.1.1 ExxonMobil Corporation

- 6.3.1.2 BP PLC

- 6.3.1.3 Saudi Aramco

- 6.3.1.4 Egyptian General Petroleum Corporation

- 6.3.1.5 Chevron Corporation

- 6.3.2 Pipeline Maintenance Services Providers

- 6.3.2.1 Arabian Pipes Company

- 6.3.2.2 Abu Dhabi Metal Pipes & Profiles Industries Complex LLC

- 6.3.2.3 Rezayat Group

- 6.3.2.4 Vallourec SA

- 6.3.2.5 STATS Group

- 6.3.2.6 Halliburton Company

- 6.3.2.7 EEW Group

- 6.3.2.8 T. D. Williamson Inc

- 6.3.1 Pipeline Operators

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Adoption Of Digital Technologies And Automation In Pipeline Maintenance