|

市場調査レポート

商品コード

1644896

英国のサイバーセキュリティ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)UK Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のサイバーセキュリティ-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

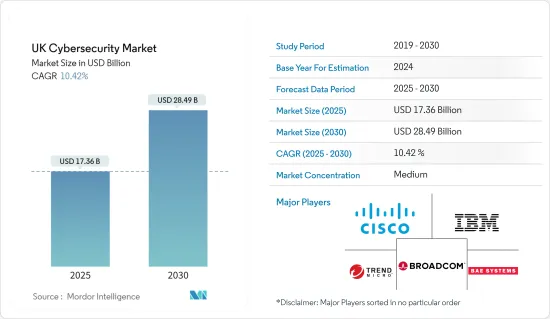

英国のサイバーセキュリティ市場規模は2025年に173億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.42%で、2030年には284億9,000万米ドルに達すると予測されます。

主要ハイライト

- 同国におけるサイバー攻撃の増加により、防衛能力の強化が推進されています。また、デジタル化と拡大可能なi.T.インフラに対する需要の高まり、サードパーティベンダーのリスクに取り組む必要性の高まり、クラウドファースト戦略の採用が、同国におけるサイバーセキュリティソリューションとサービスの成長を促進しています。

- 英国政府は最近、新たな国家サイバーセキュリティ戦略を打ち出し、英国をサイバー脅威から守り、「世界のサイバー大国としての地位を確固たるものにする」ための「青写真」として歓迎されました。この戦略はまた、「米国の価値観」を共有しない国際的なサプライヤーや技術への英国の依存を減らすためのさらなる動きも示唆しています。

- gov.ukによると、英国のサイバーセキュリティ部門は急速に拡大しており、1400以上の企業が昨年89億ポンドの収益を上げ、46,700人の熟練した雇用を支え、外部からの多額の投資を集めています。このビジネスは、サイバーパワー、安全保障、世界的影響力、経済開発にとって不可欠です。

- ビジョン2030のために、英国とインドは2022年4月、包括的かつ社会全体のアプローチを進めることで相互のサイバー耐性を強化するために協力しました。この提携を達成するため、両国はサイバー・ガバナンス、レジリエンス、抑止力、能力開発に集中した協力プログラムへのコミットメントを強調しました。

- 英国では5Gと光ファイバーによるブロードバンドネットワークが拡大しており、政府は通信会社と協力して、サイバー攻撃に対処し、英国の通信セクター全体のセキュリティ基準とプラクティスを改善するためのイニシアチブをとっています。

- サイバー犯罪の増加により、サイバー犯罪に対処するための新たなソリューションの開発に注目が集まっており、これが同国の投資状況を特徴づけています。例えば、マネージドディテクション・レスポンスとセキュリティオペレーションセンターを手がけるサイバーセキュリティサービス会社、ブライドウェル・コンサルティングは、英国とその他の欧州での事業拡大のため、非公開会社グロース・キャピタル・パートナーから数百万米ドルの投資を受けました。

- 英国はまた、欧州最大のサイバーセキュリティイベントであるInfosecurity Europeの開催地でもあります。このイベントには、120社以上の米国企業を含む400社以上の出展者があり、1万9,500人以上の産業関係者に最新の情報セキュリティソリューションや製品を発表しています。

- さらに、モノのインターネット(IoT)機器の増加に伴い、多様なサイバー攻撃に対する脆弱性と暴露が増加しています。スマートシティへの取り組みとともに、同国におけるIoTやコネクテッドデバイスの増加傾向は予測期間中も続くとみられます。

英国のサイバーセキュリティ市場動向

クラウド展開セグメントが市場で大きな成長を記録する見込み

- 新たなデータストレージを構築・維持するのではなく、データをクラウドに移行することでコストとリソースを節約することの重要性に対する企業の認識が高まっていることが、クラウドベースのソリューションに対する需要、ひいては英国におけるオンデマンドセキュリティサービスの採用を後押ししています。クラウドプラットフォームとエコシステムは、さまざまな利点があるため、今後数年間でデジタル革新のペースと規模が爆発的に拡大するための発射台としての役割を果たすと予想されています。

- ITの提供がオンプレミスから社外に移ったことで、クラウド導入サイクルの各段階において、セキュリティは重要な検討事項となっています。中小企業は、サイバーセキュリティの予算が限られているため、セキュリティインフラに資本を投下するよりも、自社のコアコンピタンスに集中できるクラウド導入を好みます。

- さらに、パブリッククラウドサービスを導入することで、信頼の境界が組織を超えて広がるため、クラウドインフラにとってセキュリティは不可欠な要素となっています。しかし、クラウドベースのソリューションの利用が増えたことで、企業のサイバーセキュリティ対策は大幅に簡素化されました。

- Google Drive、Dropbox、Microsoft Azureなどのクラウドサービスの導入が進み、これらのツールがビジネスプロセスの不可欠な一部となりつつある中、企業は機密データの管理ができなくなるなどのセキュリティ問題に対処しなければならないです。このため、国内ではオンデマンド・サイバーセキュリティソリューションの導入が増加しています。

- さらに、クラウドベースの電子メールセキュリティサービスの採用が増加したことで、IPSやNGFWなど他のセキュリティプラットフォームと統合されたサービスの採用が進んでいます。この動向により、企業はオンプレミスや専用の電子メールやウェブセキュリティソリューションに費用をかける必要がなくなっています。

- また、クラウドベースのソリューションは、資本支出要件が低いというメリットもあるため、ビジネスの説得力が格段に増しています。クラウドベースのサービスを導入すれば、企業はハードウェアコンポーネントに投資する必要がないため、設備投資要件を大幅に削減することができ、国内でのクラウドベースのソリューションの成長を後押ししています。

BFSIセグメントが市場で大きなシェアを占める

- BFSI産業は、多数のデータ漏洩やサイバー攻撃に直面する重要インフラセグメントのひとつです。

- サイバー犯罪者は、驚異的なリターンと、比較的低リスクで検出可能というプラス面を持つ、非常に有利なオペレーション・モデルであるため、金融セクターを動けなくするために、多数の極悪非道なサイバー攻撃を最適化しています。こうした攻撃の脅威は、トロイの木馬、マルウェア、ATMマルウェア、ランサムウェア、モバイルバンキングマルウェア、データ侵害、機関への侵入、データ盗難、財政侵害など多岐にわたります。

- さまざまな公的機関や民間銀行が、ITプロセスやシステムの安全確保、顧客の重要データの保護、政府規制の遵守といった戦略を掲げ、サイバー攻撃を防ぐための最新技術の導入に注力しています。加えて、顧客の期待の高まり、技術力の向上、規制要件により、銀行機関は積極的なセキュリティアプローチを採用する必要に迫られています。

- モバイルバンキングやインターネット・バンキングなど、技術的な普及とデジタルチャネルの拡大により、オンラインバンキングは銀行サービスの選択肢として顧客に好まれるようになりました。銀行が先進的認証とアクセス制御プロセスを活用する必要性は大きいです。

- 2022年、世界中の金融機関が、脅威行為者のROIを最大化する革新的な新しいランサムウェアの手口の影響を受けました。金融機関がランサムウェア攻撃の直接の標的となる被害者の割合は少ないもの、金融機関は、主要な標的であるサードパーティに対する攻撃によって影響を受ける可能性があり、実際に影響を受けています。このような脅威は、同国のBFSIセクターにおけるサイバーセキュリティソリューションの利用を増加させる態勢を整えています。

英国のサイバーセキュリティ産業概要

英国のサイバーセキュリティ市場は半分断されており、この市場での地位を強化するために、M&A、新製品の発売、事業拡大、合弁事業、パートナーシップなど、さまざまな成長戦略を採用している主要企業がいくつかあります。主要参入企業は、IBM Corporation、Cisco Systems Inc.、Trend Micro Incorporated(UK)、Broadcom Limited、BAE Systems Inc.などがあります。

2022年10月、ブライトンを拠点とするデジタル化サービスプロバイダーのSimplex Servicesは、ダラスを拠点とする技術ソリューションベンダーのNovigoSolutionsと提携しました。この提携により、Simplex ServicesはPower Platform、SharePoint、Dynamics、Microsoft 365、UiPathによるRobotic Process Automation、サイバーセキュリティなど、Microsoftのクラウド機能を活用できるようになります。シンプレクスは、ノビーゴのリソースプールを利用することで、クライアントをサポートし、市場へのリーチを拡大し、成長の可能性を高め、様々なセグメントの課題に対応することができます。

2022年7月、サイバーセキュリティとインフラセキュリティ機関(CISA)は、ロンドンに初のアタッシュオフィスを設置すると発表しました。アタッシュ・オフィスは、CISA、英国政府関係者、その他の連邦政府機関関係者間の国際協力のために機能します。これにより、サイバーセキュリティ、重要インフラ保護、緊急通信におけるCISAの任務が推進され、同機関の世界のネットワークが活用されます。

2022年4月、インドと英国は、ビジョン2030に向けた全体的かつ社会全体からのアプローチにより、相互のサイバー耐性を高めるために提携しました。両国は、サイバー・ガバナンス、抑止力、回復力、能力開発に焦点を当てたパートナーシップを実現するための共同協力プログラムへのコミットメントを概説しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン分析

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- デジタル化と拡大可能なITインフラへの需要の高まり

- サードパーティベンダーのリスク、MSSPの進化、クラウドファースト戦略の採用など、さまざまな動向によるリスクへの取り組みの必要性

- 市場抑制要因

- サイバーセキュリティ専門家の不足

- 従来の認証方法への依存度の高さと準備不足

- 動向分析

- タイではサイバーセキュリティ戦略強化のためにAIを活用する組織が増加

- クラウドベースのデリバリーモデルへのシフトにより、クラウドセキュリティが飛躍的に成長

第6章 市場セグメンテーション

- サービス別

- セキュリティタイプ

- クラウドセキュリティ

- データセキュリティ

- ID確認・アクセス管理

- ネットワークセキュリティ

- コンシューマーセキュリティ

- インフラ保護

- その他のセキュリティ

- サービス別

- セキュリティタイプ

- 展開別

- クラウド

- オンプレミス

- エンドユーザー別

- BFSI

- 医療

- 製造業

- 政府・防衛

- IT・通信

- その他

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Cisco Systems Inc

- Trend Micro Incorporated (UK)

- Broadcom Limited

- BAE Systems Inc.

- Dell Technologies Inc.

- Fortinet Inc.

- Palo Alto Networks

- Mcafee, LLC

- Intel Security(Intel Corporation)

第8章 投資分析

第9章 市場の将来

The UK Cybersecurity Market size is estimated at USD 17.36 billion in 2025, and is expected to reach USD 28.49 billion by 2030, at a CAGR of 10.42% during the forecast period (2025-2030).

Key Highlights

- Increasing cyberattacks in the country have propelled it to strengthen its defensive capabilities, and the rising demand for digitalization and scalable I.T. Infrastructure, the increasing need to tackle risks from third-party vendor risks, and the adoption of a cloud-first strategy has been driving the growth of cybersecurity solutions and services in the country.

- The British government recently launched a new National Cyber Security Strategy, hailed as a 'blueprint' to protect the U.K. from cyber threats and 'solidify its position as a global cyber power.' The strategy also signals further moves to reduce the U.K.'s reliance on international suppliers or technologies that do not share 'the U.K.'s values.

- According to gov. uk, the U.K.'s cybersecurity sector is quickly increasing, with over 1400 businesses making £8.9 billion in revenue last year, supporting 46,700 skilled jobs, and attracting significant outside investment. This business is vital to cyber power, security, global influence, and economic development.

- For Vision 2030, the United Kingdom and India collaborated in April 2022 to strengthen their mutual cyber resilience by advancing a comprehensive and whole-of-society approach. To accomplish the alliance, the states emphasized their commitment to a collaborative program of cooperation concentrating on cyber governance, resilience, deterrence, and capacity building.

- With the growing 5G and total fiber broadband networks in the country, the government, in collaboration with telecommunication companies, is taking initiatives to tackle cyberattacks and improve security standards and practices across the United Kingdom's telecoms sector.

- The increased rate of cybercrimes has driven the focus on developing new solutions to tackle them, which has characterized the country's investment landscape. For instance, Bridewell Consulting, a cybersecurity services company dealing with Managed Detection Response and Security Operations Centre, acknowledged a multi-million dollar investment from Growth Capital Partners, a private equity firm, to expand its operations in the U.K. and the rest of Europe.

- The U.K. is also home to the largest cybersecurity event in Europe, Infosecurity Europe. The event has over 400 exhibitors, including over 120 U.S. companies, that showcase their latest information security solutions and products to over 19,500 industry professionals.

- Further, the vulnerability and exposure to diverse cyber-attacks have increased with the increased Internet of Things (IoT) devices. Along with smart city initiatives, the trend of increasing IoT and connected devices in the country is expected to continue during the forecast period.

UK Cyber Security Market Trends

Cloud Deployment Segment is Expected to Register a Significant Growth in the Market

- The increasing realization among enterprises regarding the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage drives the demand for cloud-based solutions and, hence, the adoption of on-demand security services in the United Kingdom. Owing to multiple benefits, cloud platforms, and ecosystems are anticipated to serve as a launchpad for an explosion in the pace and scale of digital innovation over the next few years.

- Security has been a critical consideration at each step of the cloud adoption cycle as IT provision has moved from on-premise to outside of a company's walls. SMEs prefer cloud deployment as it allows them to focus on their core competencies rather than invest their capital in security infrastructure since they have limited cybersecurity budgets.

- Furthermore, deploying public cloud services extends the boundary of trust beyond the organization, making security a vital part of the cloud infrastructure. However, the increasing usage of cloud-based solutions has significantly simplified enterprises' adoption of cybersecurity practices.

- With the increased adoption of cloud services, such as Google Drive, Dropbox, and Microsoft Azure, and with these tools emerging as an integral part of business processes, enterprises must deal with security issues, such as losing control over sensitive data. This increases the incorporation of on-demand cybersecurity solutions in the country.

- Additionally, the increased adoption of cloud-based email security services is driving the adoption of services integrated with other security platforms, such as IPS and NGFW. This trend demotes enterprises to spend on on-premise and dedicated email or web security solutions.

- Cloud-based solutions also benefit from lower capital expenditure requirements, thus making the business much more compelling. Deploying cloud-based services can significantly reduce the Capex requirement as the companies need not invest in hardware components, driving the growth of cloud-based solutions in the country.

BFSI Segment to hold significant share in the market

- The BFSI industry is one of the critical infrastructure segments that face multiple data breaches and cyber-attacks, owing to the massive customer base that the sector serves and the financial information that is at stake.

- Being a highly lucrative operation model with phenomenal returns and the added upside of relatively low risk and detectability, cybercriminals are optimizing a plethora of diabolical cyberattacks to immobilize the financial sector. These attacks' threat landscape ranges from Trojans, malware, ATM malware, ransomware, mobile banking malware, data breaches, institutional invasion, data thefts, fiscal breaches, etc.

- Various public and private banking institutes are focusing on implementing the latest technology to prevent cyber attacks with a strategy to secure their IT processes and systems, secure customer critical data, and comply with government regulations. Besides, with greater customer expectations, rising technological capabilities, and regulatory requirements, banking institutions are pushed to adopt a proactive security approach.

- With the growing technological penetration and digital channels, such as mobile banking, Internet banking, etc., online banking has become customers' preferred choice for banking services. There is a significant need for banks to leverage advanced authentication and access control processes.

- In 2022, financial firms worldwide were impacted by innovative new ransomware tactics that maximized ROI for the threat actors. While financial firms represent a small percentage of victims directly targeted by ransomware attacks, they can and have been impacted by attacks on third parties, who are prime targets. Such threats are poised to increase the usage of cybersecurity solutions in the BFSI sector in the country.

UK Cyber Security Industry Overview

UK Cybersecurity Market is semi-fragmented and has some major players who have adopted various growth strategies, such as mergers and acquisitions, new product launches, expansions, joint ventures, partnerships, and others, to strengthen their position in this market. The major players in the market are IBM Corporation, Cisco Systems Inc., Trend Micro Incorporated (UK), Broadcom Limited, and BAE Systems Inc., among others.

In October 2022 - Simplex Services, a Brighton-based digitalization services provider, partnered with NovigoSolutions, a technology solutions vendor based in Dallas. The cooperation will benefit from Simplex Services' Microsoft Cloud capabilities, which include Power Platform, SharePoint, Dynamics, Microsoft 365, Robotic Process Automation with UiPath, and Cybersecurity. Simplex will be able to support its clients by using Novigo's resource pool, boosting its market reach, increasing growth possibilities, and addressing challenges across many sectors.

In July 2022, The Cybersecurity and Infrastructure Security Agency (CISA) announced its first Attache Office in London. The Attache Office will serve for international collaboration between CISA, UK government officials, and other federal agency officials. thereby advancing CISA's missions in cybersecurity, critical infrastructure protection, and emergency communications and leveraging the agency's global network.

In April 2022, India and the United Kingdom partnered to increase their mutual cyber resilience, taking a holistic and whole-of-society approach to Vision 2030. The countries outlined their commitment to a joint cooperation program to deliver the partnership, focused on cyber governance, deterrence, resilience, and capacity building.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Digitalization and Scalable IT Infrastructure

- 5.1.2 Need to tackle risks from various trends such as third-party vendor risks, the evolution of MSSPs, and adoption of cloud-first strategy

- 5.2 Market Restraints

- 5.2.1 Lack of Cybersecurity Professionals

- 5.2.2 High Reliance on Traditional Authentication Methods and Low Preparedness

- 5.3 Trends Analysis

- 5.3.1 Organizations in Thailand increasingly leveraging AI to enhance their cyber security strategy

- 5.3.2 Exponential growth to be witnessed in cloud security owing to shift toward cloud-based delivery model.

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Security Type

- 6.1.1.1 Cloud Security

- 6.1.1.2 Data Security

- 6.1.1.3 Identity Access Management

- 6.1.1.4 Network Security

- 6.1.1.5 Consumer Security

- 6.1.1.6 Infrastructure Protection

- 6.1.1.7 Other Security Types

- 6.1.2 Services

- 6.1.1 Security Type

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 Healthcare

- 6.3.3 Manufacturing

- 6.3.4 Government & Defense

- 6.3.5 IT and Telecommunication

- 6.3.6 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Cisco Systems Inc

- 7.1.3 Trend Micro Incorporated (UK)

- 7.1.4 Broadcom Limited

- 7.1.5 BAE Systems Inc.

- 7.1.6 Dell Technologies Inc.

- 7.1.7 Fortinet Inc.

- 7.1.8 Palo Alto Networks

- 7.1.9 Mcafee, LLC

- 7.1.10 Intel Security (Intel Corporation)