|

|

市場調査レポート

商品コード

1644883

中国のサイバーセキュリティ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のサイバーセキュリティ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

中国のサイバーセキュリティ市場規模は2025年に276億米ドルと推計され、予測期間(2025~2030年)のCAGRは21.09%で、2030年には718億4,000万米ドルに達すると予測されます。

中国のサイバーセキュリティ市場は、デジタル化の進展とそれに伴うサイバー脅威の増加に伴い、急速に成長しています。中国政府は、重要インフラ、機密データ、企業をサイバー攻撃から守るため、サイバーセキュリティ対策を積極的に強化しています。

主なハイライト

- 中国では技術の進歩により、接続された機器の数が増加しています。デバイスの相互接続性も、5G対応デバイスによって飛躍的に高まっています。その結果、接続されるデバイスが増え、セキュリティ製品に対する市場のニーズが一気に高まる。

- 産業革命4.0は、IoTの台頭により、業界全体のセルラー接続を助ける。マシン・ツー・マシンの接続も市場を牽引しています。CNNICによると、2023年12月には、中国の約23億3,000万人のインターネットユーザーがセルラーIoTサービスにアクセスできるようになった。スマート公共事業、製造業、運輸業がIoTエンドユーザーの半分以上を占めています。

- サイバー攻撃の増加の主な原因の1つは、各業界における熟練したサイバーセキュリティ人材の不足です。中国では、経験豊富なサイバーセキュリティの専門家はセキュリティの専門家よりも少なく、金融機関、政府機関、民間企業/産業界のサイバー脅威に対処することが求められています。

- 大企業は、セキュリティと販売のために、より多くのデータに基づくAIソリューションを導入しています。サイバーセキュリティの専門家は、防衛線を補強するために地理空間データに注目しています。企業は、既存のセキュリティ・システムに地理空間データを導入することで、緊急管理、国家情報、インフラ保護、国防プラットフォームを強化することができます。

- COVID-19以降、中国を含め、さまざまな国の多くの組織がリモートワーク環境に切り替えています。マルウェアやランサムウェアを含むサイバー攻撃の増加により、組織はサイバーセキュリティ・ソリューションの導入を余儀なくされています。したがって、中国のサイバーセキュリティ市場は、在宅勤務の増加傾向の結果として大きな成長を遂げると予想されます。

中国のサイバーセキュリティ市場の動向

クラウド導入形態セグメントが大きな市場シェアを占める見込み

- クラウドベースのソリューションに対するニーズと、それに続くオンデマンドセキュリティ・サービスの利用拡大には、新たなデータ・ストレージを作成して維持するよりも、データをクラウドに移行する方がコストとリソースを節約できるという価値に対する企業の認識が高まっていることが背景にあります。こうした利点から、中国の大手企業や中小企業はクラウドベースのソリューションを頻繁に採用しています。

- 新たなデータ・ストレージを構築・維持するのではなく、データをクラウドに移行することでコストとリソースを節約することの重要性に対する企業の認識が高まっていることが、クラウドベースのソリューションに対する需要を後押ししています。複数の利点があるため、クラウドプラットフォームとエコシステムは、今後数年間でデジタル革新のペースと規模を爆発的に拡大させる発射台としての役割を果たすと予想されます。

- ITの提供がオンプレミスから社外へとシフトするにつれ、クラウド導入サイクルのあらゆる段階でセキュリティが極めて重要になっています。中小企業がクラウドの導入を好むのは、限られたサイバーセキュリティ資金をセキュリティ・インフラに投資するよりも、自社のコア・スキルに集中できるようになるためです。さらに、パブリック・クラウド・サービスを利用することで、組織の信頼性の境界が広がるため、セキュリティはクラウド・インフラストラクチャの不可欠な要素となっています。しかし、クラウドベースのソリューションの利用が増えたことで、企業のサイバーセキュリティ対策は大幅に簡素化されました。

- グーグル・ドライブ、ドロップボックス、マイクロソフト・アジュールなどのクラウド・サービスの導入が進み、これらのツールがビジネス・プロセスの不可欠な部分として台頭してきたことで、企業は機密データの管理ができなくなるなどのセキュリティ問題に対処しなければならなくなった。そのため、オンデマンド・サイバーセキュリティ・ソリューションの導入が増加しています。

- クラウドベースのソリューションは、資本支出要件が低いというメリットもあるため、ビジネスの説得力が格段に増します。クラウドベースのサービスを導入すれば、企業はハードウェア・コンポーネントに投資する必要がないため、設備投資要件を大幅に削減できます。また、クラウド・ソリューションは、アプリケーションのコストをより正確に予測することができるため、企業はテクノロジーを導入するための初期費用をそれほど負担する必要がないです。ハードウェアとITサポートの節約により、クラウドベースのソリューションはより手頃な価格になっています。

- オンプレミスのソフトウェアからクラウドベースのソリューションへの移行を検討している企業は、主に、標準準拠、侵入防止、検出などの主要なセキュリティ機能に関する潜在的なソリューションの機能をチェックしています。

- CNNICが2023年6月に実施した調査によると、中国のインターネット・ユーザーの20%がオンライン詐欺の被害に遭っていることが判明しました。

データセキュリティ・オファリング・セグメントが大きな市場シェアを占める見込み

- 金融セクターは、適切な情報およびデータセキュリティ基準を導入するための規制的枠組みを採用する主要な企業として認識されています。これにより、商品やサービスの信頼できる提供、システムによる安全なデータ処理、個人データの責任ある利用が保証されます。

- データセキュリティは、機密データを脅威から保護することに伴うリスクを軽減し、組織がコンプライアンスを維持するのに役立ちます。データセキュリティ・プラットフォームは、データ・リスク分析、データ監視、保護ソリューション、データベースの脆弱性からの組織データの保護を提供します。各国政府はデータセキュリティに関する規制を強化し、企業にサイバーセキュリティソリューションの利用を義務付けています。ウイルス対策ソフトやスパイウェア対策ソフトの使用を含むこの動向は、今後数年間、サイバーソリューションの活況市場を生み出すと予想されます。コンプライアンスは、データ損失防止ソリューションの主要な原動力になると予想されます。しかし、企業のデジタルトランスフォーメーション戦略、特にクラウドの採用、ビッグデータ分析、IoTの実現は、この地域の企業セキュリティチームがこれらの製品を採用し、組織全体で重要なデータを特定・分類し、主に情報の重要性に基づいてデータセキュリティ管理を再配分する原動力にもなっています。

- 企業が業務のデジタル化を進め、複雑化するデータ保護の課題に対処していく中で、効果的なデータセキュリティ対策への投資は、機密情報の保護、規制遵守の維持、評判の保護に不可欠となります。

- デジタルトランスフォーメーションが加速し、データ保護の問題が複雑化する中、組織は機密データを保護し、規制要件を満たし、ブランドイメージを守るために、適切なセキュリティ対策に投資しなければならないです。データ量の増加、データ保護規制の変化、顧客の関連する懸念の必要性から、データセキュリティ・ソリューションに対する需要は旺盛になると予想されます。

- CNNICが2023年6月に実施した調査によると、オンライン詐欺は中国のインターネット・ユーザーが直面する最も一般的なインターネットセキュリティ問題です。回答者の約38%がオンラインで懸賞や宝くじの当選詐欺に遭遇しています。

中国のサイバーセキュリティ産業の概要

中国のサイバーセキュリティ市場は断片化されており、Palo Alto Networks、ThreatBook、IBM Corporation、QI-ANXIN Technology Group Inc.、Beijing Chaitin Future Technologyなどの大手企業が存在します。同市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。例えば

- 2024年4月、世界・サイバーセキュリティリーダーの一社であるパロアルトネットワークスとグーグル・クラウドは、10桁の複数年コミットメントによるパートナーシップの拡大を発表しました。パロアルトネットワークスは、Google CloudをAIとインフラのプロバイダーとして選択しました。Google Cloudは以前からパロアルトネットワークスを優先的な次世代ファイアウォール(NGFW)プロバイダーとみなしており、今回の契約拡大はその関係を強固なものにしました。この協業はまた、複数のソリューションを自動化・統合し、ほぼリアルタイムのセキュリティ解決を実現するために、AIを活用したプラットフォーム化が極めて重要であることを強調しています。

- IBMは2023年10月、アラートの最大85%を自動的にエスカレーションまたはクローズし、顧客のセキュリティ対応スケジュールを短縮するなど、AI技術を活用したマネージド検知・対応サービスの進化を発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- マクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 企業におけるフィッシングやマルウェアリスクの増加

- クラウドベースのサービス利用の増加

- 企業におけるサイバーセキュリティ強化が求められるM2M/IoT接続の増加

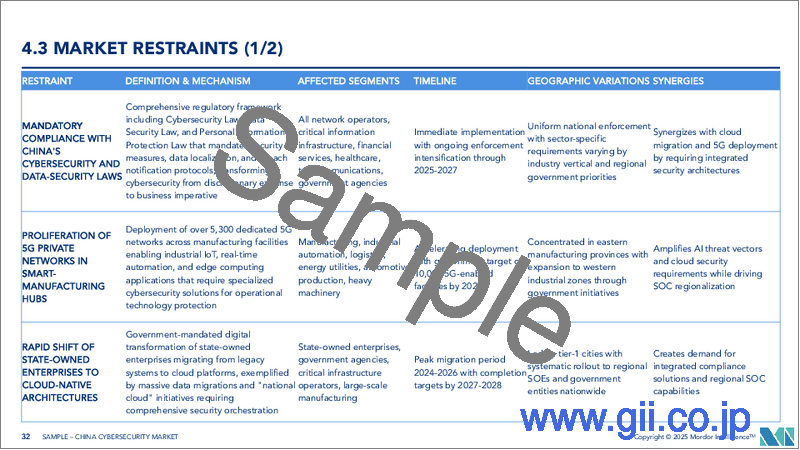

- 市場抑制要因

- サイバーセキュリティ専門家の不足と最新デバイスのセキュリティ課題

- 組織が直面する予算制限、準備不足、従来の認証方法への依存度の高さ

- 市場機会

- サイバーセキュリティにおけるIoT、BYOD、AI、機械学習の動向の高まり

- 従来のウイルス対策ソフトウェア業界の変革

第6章 市場セグメンテーション

- サービス別

- セキュリティタイプ

- クラウドセキュリティ

- データセキュリティ

- アイデンティティ・アクセス管理

- ネットワークセキュリティ

- コンシューマーセキュリティ

- インフラ保護

- その他のタイプ

- サービス別

- セキュリティタイプ

- 展開別

- クラウド

- オンプレミス

- エンドユーザー別

- BFSI

- ヘルスケア

- 製造業

- 政府・防衛

- IT・通信

- その他エンドユーザー

第7章 競合情勢

- 企業プロファイル

- Palo Alto Networks

- ThreatBook

- IBM Corporation

- QI-ANXIN Technology Group Inc.

- Beijing Chaitin Future Technology Co. Ltd

- CoreShield Times

- River Security

- Tophant Inc.

- iJiami

- IDsManager

第8章 投資分析

第9章 市場の将来展望

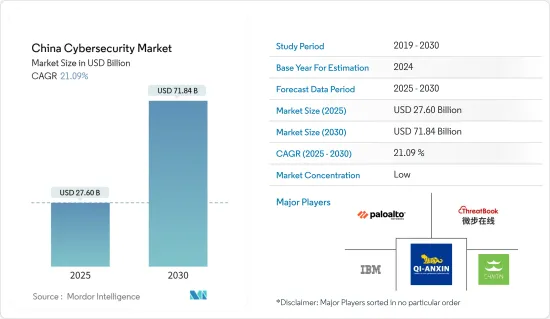

The China Cybersecurity Market size is estimated at USD 27.60 billion in 2025, and is expected to reach USD 71.84 billion by 2030, at a CAGR of 21.09% during the forecast period (2025-2030).

China's cybersecurity market has been rapidly growing with the country's increasing digitization and the corresponding rise in cyber threats. The Chinese government has been actively enhancing its cybersecurity measures to protect critical infrastructure, sensitive data, and businesses against cyber attacks.

Key Highlights

- The number of connected devices has increased in China due to technological advancements. The interconnectivity of the devices also grows exponentially with 5G-enabled devices. As a result, there are more connected devices, which immediately increases the market's need for security products.

- Industrial Revolution 4.0 aids cellular connectivity throughout the industry with the rise of IoT. Machine-to-machine connections have also been instrumental in driving the market. According to CNNIC, in December 2023, approximately 2.33 billion internet users in China had access to cellular Internet of Things (IoT) services. Smart public utility, manufacturing, and transportation accounted for over half of the IoT end users.

- One of the major causes of growing cyberattacks is the lack of skilled cybersecurity personnel in each industry. In China, experienced cybersecurity professionals are less than security professionals, who are required to handle cyber threats for financial institutes, government organizations, and private sector/industrial businesses.

- Large businesses are implementing more data-based AI solutions for security and sales. Cybersecurity experts have turned to geospatial data to shore up the lines of defense. Companies can strengthen emergency management, national intelligence, infrastructure protection, and national defense platforms by implementing geospatial data into pre-existing security systems.

- Many organizations in various countries have switched to remote work environments after COVID-19, including China. The rising cyber-attacks involving malware and ransomware are forcing organizations to adopt cybersecurity solutions. Therefore, the Chinese cybersecurity market is anticipated to experience significant growth as a result of the growing work-from-home trend.

China Cyber Security Market Trends

Cloud Deployment Mode Segment is Expected to Hold Significant Market Share

- The need for cloud-based solutions and subsequent growth in the use of on-demand security services is driven by businesses' growing awareness of the value of saving money and resources by transferring their data to the cloud rather than creating and maintaining new data storage. Due to these advantages, major businesses and SMEs in China adopt cloud-based solutions more frequently.

- The increasing realization among enterprises about the importance of saving money and resources by moving their data to the cloud instead of building and maintaining new data storage drives the demand for cloud-based solutions. Owing to multiple benefits, cloud platforms and ecosystems are anticipated to serve as a launchpad for an explosion in the pace and scale of digital innovation over the next few years.

- As IT provision has shifted from on-premise to outside the boundaries of the business, security has been crucial at every stage of the cloud adoption cycle. SMEs prefer cloud deployment because it frees them up to concentrate on their core skills rather than investing their limited cybersecurity funds in security infrastructure. Furthermore, using public cloud services expands the organization's confidence boundary, making security an essential component of the cloud infrastructure. However, the increasing usage of cloud-based solutions has significantly simplified enterprises' adoption of cybersecurity practices.

- With the increased adoption of cloud services, such as Google Drive, Dropbox, and Microsoft Azure, and with these tools emerging as an integral part of business processes, enterprises must deal with security issues, such as losing control over sensitive data. This gives rise to the increased incorporation of on-demand cybersecurity solutions.

- Cloud-based solutions also benefit from lower capital expenditure requirements, thus making the business much more compelling. Deploying cloud-based services can significantly reduce the Capex requirement as the companies need not invest in hardware components. Cloud solutions also enable better prediction of the cost of an application, and companies do not need to incur as much upfront cost to incorporate the technology. The hardware and IT support savings make cloud-based solutions much more affordable.

- Companies considering moving from on-premise software to a cloud-based solution are primarily checking the potential solutions for their capabilities concerning key security features, including standards compliance, intrusion prevention, and detection.

- A CNNIC survey conducted in June 2023 found that a troubling 20% of internet users in China have been victims of online fraud.

Data Security Offering Segment is Expected to Hold Significant Market Share

- The financial sector has been recognized as a prime adopter of regulatory frameworks to implement adequate information and data security standards. These ensure a reliable provision of products and services, safe data processing by its systems, and responsible use of personal data.

- Data security helps reduce risks associated with protecting sensitive data from threats and helps organizations maintain compliance. The data security platforms provide data risk analytics, data monitoring, protection solutions, and protection of the organization's data from database vulnerability. Governments are tightening the mandates on data security, requiring companies to use cybersecurity solutions. This trend, including the use of antivirus and antispyware software, is expected to create a booming market for cyber solutions in the coming years. Compliance is expected to be the key driver of data loss prevention solutions. However, an enterprise's digital transformation strategies, most notably cloud adoption, Big Data analytics, and IoT enablement are also driving enterprise security teams in the region to adopt these products to identify and classify crucial data throughout the organization and reallocate data security controls primarily based on the criticality of the information.

- As organizations continue to digitize their operations and deal with increasingly complex data protection challenges, investment in effective data security measures will be essential to safeguard sensitive information, maintain regulatory compliance, and protect their reputation.

- As digital transformation accelerates and data protection issues become more complex, organizations must invest in adequate security measures to protect sensitive data, meet regulatory requirements, and save their brand image. Increasing data volumes, changing data protection regulations, and the necessity of customers' related concerns are expected to create robust demand for data security solutions.

- A CNNIC survey conducted in June 2023 found that online fraud is the most common internet security issue faced by internet users in China. Around 38% of respondents encountered prize or lottery-winning scams online.

China Cyber Security Industry Overview

The Chinese cybersecurity market is fragmented, with the presence of major players like Palo Alto Networks, ThreatBook, IBM Corporation, QI-ANXIN Technology Group Inc., and Beijing Chaitin Future Technology Co. Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage. For instance,

- In April 2024, Palo Alto Networks, one of the global cybersecurity leaders, and Google Cloud announced the expansion of their partnership with a ten-figure, multi-year commitment. Palo Alto Networks named Google Cloud its AI and infrastructure provider of choice. Google Cloud has long considered Palo Alto Networks its preferred next-generation firewall (NGFW) provider and the expanded agreement solidified that relationship. The collaboration also underscores the critical importance of platformization fueled by AI to automate and consolidate multiple solutions and deliver near-real-time security resolutions.

- In October 2023, IBM unveiled the evolution of its managed detection and response service offerings with AI technologies, including automatically escalating or closing up to 85% of alerts and accelerating security response timelines for clients.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Phishing and Malware Risks among Businesses

- 5.1.2 Rising Utilization of Cloud-Based Services

- 5.1.3 Rising M2M/IoT Connections Requiring Enhanced Cybersecurity in Businesses

- 5.2 Market Restraints

- 5.2.1 Lack of Cybersecurity Experts and Security Challenges with Modern Devices

- 5.2.2 Budgetary Restrictions faced by Organizations, Low Preparedness, and High Reliance on Traditional Authentication Methods

- 5.3 Market Opportunities

- 5.3.1 Growing Trends in IoT, BYOD, AI, and Machine Learning in Cybersecurity

- 5.3.2 Traditional Antivirus Software Industry Transformation

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Security Type

- 6.1.1.1 Cloud Security

- 6.1.1.2 Data Security

- 6.1.1.3 Identity Access Management

- 6.1.1.4 Network Security

- 6.1.1.5 Consumer Security

- 6.1.1.6 Infrastructure Protection

- 6.1.1.7 Other Types

- 6.1.2 Services

- 6.1.1 Security Type

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-premise

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 Healthcare

- 6.3.3 Manufacturing

- 6.3.4 Government & Defense

- 6.3.5 IT and Telecommunication

- 6.3.6 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Palo Alto Networks

- 7.1.2 ThreatBook

- 7.1.3 IBM Corporation

- 7.1.4 QI-ANXIN Technology Group Inc.

- 7.1.5 Beijing Chaitin Future Technology Co. Ltd

- 7.1.6 CoreShield Times

- 7.1.7 River Security

- 7.1.8 Tophant Inc.

- 7.1.9 iJiami

- 7.1.10 IDsManager