暗号化ソフトウェア:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Encryption Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644859

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

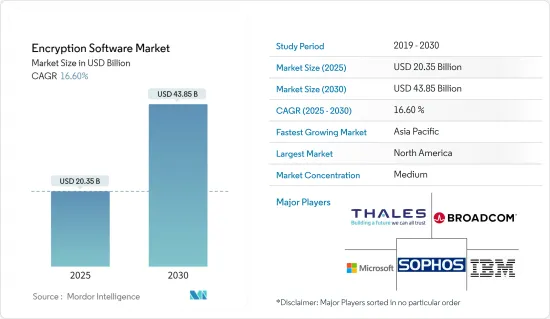

暗号化ソフトウェア市場規模は、2025年に203億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは16.6%で、2030年には438億5,000万米ドルに達すると予測されます。

暗号化ソフトウェア市場は、データ保護とプライバシーのニーズの高まりによって拡大するサイバーセキュリティの領域において極めて重要です。同市場は、高度な暗号化アルゴリズムによって機密情報を保護し、さまざまな業界でデータの完全性と機密性を確保するソリューションの数々をカバーしています。暗号化ソフトウェアは、機密データの保護が最優先事項である金融、ヘルスケア、政府などの分野で特に重要です。

暗号化アルゴリズム重要データの保護

主なハイライト

- 暗号化アルゴリズムは、ディスクに保存されているデータ、ネットワーク経由で送信されるデータ、電子メールで共有されるデータなど、データの安全性を確保する上で基本となるものです。ディスク暗号化ソフトウェア、ファイル暗号化ソフトウェア、モバイル暗号化ソフトウェアなどのソリューションは、不正アクセスからデータを保護する上で非常に重要です。クラウド・コンピューティングの普及により、クラウド暗号化とEaaS(Encryption as a Service)が最前線に登場し、クラウド環境でデータを保護するためのスケーラブルで柔軟なオプションが企業に提供されています。

市場セグメンテーションと採用状況

主なハイライト

- コンポーネント:市場はソフトウェアとサービスに分けられ、ソフトウェアが広く採用されているため、ソフトウェアが支配的な地位を占めています。暗号化ソフトウェアは、さまざまな業種の組織がデータを侵害や不正アクセスから保護するために不可欠なツールを提供します。

- 展開モデル:オンプレミスとクラウドベースのソリューションが主な展開モデルです。オンプレミス・ソリューションは厳格なセキュリティ要件を持つ組織に好まれ、クラウドベースのソリューションは柔軟性と拡張性を提供し、企業の進化するニーズに対応します。

- 企業規模:同市場は大企業と中小企業の両方にサービスを提供しているが、大企業は堅牢なサイバーセキュリティ対策に多額の投資を行っているため、大企業をリードしています。一方、中小企業はデータ保護の重要性を認識し、暗号化ソリューションの導入が進んでいます。

- 業界別:主な産業は、IT・通信、BFSI、ヘルスケア、政府機関などです。これらの業種は、サイバー脅威の高まりを背景に機密情報を保護する必要性から、暗号化ソフトウェアの最も重要なユーザーとなっています。

地域分析:主要市場

主なハイライト

- 北米:この地域は、厳しい規制要件と大手暗号化ソフトウェアプロバイダの存在に支えられ、暗号化ソフトウェア市場をリードしています。欧州ではGDPR、米国ではHIPAAのような規制が施行され、データセキュリティの維持における暗号化の必要性が強調されています。

- 欧州:GDPRに代表されるデータ保護に重点を置くこの地域は、暗号化ソフトウェアに対する大きな需要を牽引しています。欧州で事業を展開する企業は、コンプライアンス違反に対して厳しい罰則に直面するため、暗号化は極めて重要な投資となります。

- アジア太平洋:この地域は、デジタルトランスフォーメーションとサイバーセキュリティに対する意識の高まりにより、急成長を遂げようとしています。政府の取り組みや暗号化技術への投資が、中国、インド、日本といった国々での市場拡大をさらに後押ししています。

市場を形成する規制基準

主なハイライト

- コンプライアンスの重要性:GDPR、HIPAA、PCI DSS、CCPAなどの規制基準は、暗号化ソフトウェア市場を形成する上で極めて重要です。企業が罰則を回避し、顧客の信頼を維持するためには、これらの基準を遵守することが不可欠です。これらの規制は厳格なデータ保護対策を義務付けており、さまざまな業界で暗号化ソリューションの採用を促進しています。

- 業界特有の要件:ヘルスケアや金融などの分野には、暗号化の重要性を強調する業界特有の規制があります。たとえば、HIPAAは患者データの保護を義務付けており、PCI DSSは決済情報の保護に重点を置いているため、暗号化ソフトウェアへの需要がさらに高まっています。

サイバー攻撃とモバイル盗難が暗号化導入に与える影響

主なハイライト

- サイバー脅威の増加:ランサムウェアやフィッシングを含むサイバー攻撃の増加と巧妙化は、暗号化ソフトウェア採用の主要な促進要因です。暗号化は重要な防御メカニズムを提供し、攻撃者がデータにアクセスしても、適切な復号キーがなければ読み取れないようにします。

- モバイル・デバイスのセキュリティ:特に職場におけるモバイル・デバイスの普及は、盗難や紛失によるデータ損失のリスクを増大させています。モバイル暗号化ソフトウェアは、スマートフォンやタブレットに保存されたデータを保護し、不正アクセスのリスクを軽減するために不可欠です。

- リモートワークの動向:パンデミック後のリモートワークの拡大により、安全な通信チャネルの必要性が高まっています。安全でない可能性のあるネットワーク上で共有される機密情報を保護するため、エンドツーエンドの暗号化とネットワーク暗号化の導入が進んでいます。

暗号化ソフトウェア市場動向

IT・通信が大きなシェアを占める

- IT・通信の優位性:データ・セキュリティ・ニーズの高まりから、IT・通信分野が暗号化ソフトウェア市場で大きなシェアを占めると予想されます。膨大な量の機密データが日々送信されるため、この分野の組織では、不正アクセスやデータ漏洩を防ぐために暗号化アルゴリズムの採用が進んでいます。

- クラウドとモバイル暗号化の成長:クラウド・コンピューティングの台頭により、クラウド暗号化とEaaSの需要が大幅に増加しています。IT部門がクラウド環境全体でデータを保護するために暗号化キー管理に注力することは、AES、PCI DSS、GDPRなどの世界暗号化標準に準拠するために極めて重要です。

- 技術革新:暗号化技術の絶え間ない進歩は、IT・通信セクターの進化するニーズに応えるために不可欠です。量子安全暗号化などの技術革新は、データセキュリティの新たなベンチマークを設定し、新たな脅威から機密情報を確実に保護します。

- データ漏洩の懸念:データ漏えいの急増は、暗号化対策の強化が急務であることを強調しています。ITを含むプロフェッショナル・サービス部門は、サイバー脅威に対して特に脆弱であり、包括的な暗号化ソリューションの重要性が浮き彫りになっています。

アジア太平洋地域の成長と政府の取り組み

- デジタルトランスフォーメーション:アジア太平洋地域は、さまざまな産業における急速なデジタル変革によって、暗号化ソフトウェア市場の大幅な成長が見込まれています。金融、ヘルスケア、政府などのセクターがデジタル技術を取り入れるにつれて、機密データを保護するための暗号化ソフトウェアに対する需要が高まっています。

- 政府投資:堅牢なサイバーセキュリティの枠組みを構築するためのアジア太平洋地域の政府による多額の投資が、高度な暗号化ソリューションの開発を促進しています。シンガポールの量子コンピューティングへの投資のようなイニシアチブは、この地域がサイバーセキュリティの脅威に対抗するために暗号化技術に注力していることを浮き彫りにしています。

- クラウド暗号化の需要:アジア太平洋地域ではクラウドベースのプラットフォームの採用が増加しており、クラウド暗号化の需要が高まっています。特にデータ保護が重要な金融分野では、クラウド環境でのデータ保護にEaaSがよく使われるようになっています。

- スキルギャップとコンサルティングサービス:アジア太平洋地域では有能なサイバーセキュリティの専門家が不足しているため、暗号化ソフトウェアを効果的に導入するためのコンサルティング・サービスへの需要が生じています。業界各社は専門的なコンサルティング・サービスを提供することで対応し、市場の成長に貢献しています。

暗号化ソフトウェア業界の概要

適度に統合された市場:暗号化ソフトウェア市場は適度に統合されており、IBM、Microsoft、Broadcom Inc.、Sophos Ltd.、Thalesなどの大手世界企業が市場を牽引しています。これらの企業は、包括的な製品ポートフォリオと確立された顧客基盤により、優位を占めています。

イノベーションへの戦略的注力:特に、量子耐性暗号やゼロトラスト・アーキテクチャの開発に力を入れています。暗号化と他のサイバーセキュリティ対策を組み合わせた統合セキュリティソリューションに対する需要も高まっており、今後の市場動向を形成します。

小規模ベンダーの役割:大企業が優位を占めているにもかかわらず、ニッチ市場や特定地域では、小規模な専門ベンダーが引き続き重要な役割を果たしており、特定の業界のニーズに対応したオーダーメイドの暗号化ソリューションを提供しています。

暗号化ソフトウェア市場は、IT・通信セクターのデータセキュリティへの取り組みとアジア太平洋地域の急速なデジタル変革に牽引され、力強い成長を遂げると思われます。暗号化技術の革新、規制上の要求の高まり、サイバー脅威の蔓延の高まりは、市場動向を形成する重要な要因です。企業が機密情報を保護するために暗号化を優先させる中、市場は拡大を続け、業界のリーダーや新規参入者に有利な機会を提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- データ転送とそのセキュリティに関する規制基準

- サイバー攻撃とモバイル盗難の増加

- 市場抑制要因

- 高価な暗号化ソフトウェアの導入と保守コスト

- オープンソースや海賊版暗号化製品の利用

第6章 市場セグメンテーション

- コンポーネント別

- ソフトウェア

- サービス

- 展開モデル別

- オンプレミス

- クラウド

- 企業規模別

- 大企業

- 中小企業

- 機能別

- ディスク暗号化

- 通信暗号化

- ファイル/フォルダ暗号化

- クラウド暗号化

- データベース暗号化

- 業界別

- IT・通信

- BFSI

- ヘルスケア

- 政府機関

- 小売

- 教育

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- 中東・アフリカ

- ラテンアメリカ

第7章 競合情勢

- 企業プロファイル

- IBM

- Microsoft

- Broadcom Inc.

- Sophos Ltd.

- Thales

- McAfee, LLC

- Trend Micro Incorporated

- Dell Inc.

- Check Point Software Technologies Ltd.

- Micro Focus International plc

第8章 投資分析

第9章 市場の将来展望

目次

The Encryption Software Market size is estimated at USD 20.35 billion in 2025, and is expected to reach USD 43.85 billion by 2030, at a CAGR of 16.6% during the forecast period (2025-2030).

The encryption software market is pivotal in the expanding domain of cybersecurity, driven by the escalating need for data protection and privacy. This market covers an array of solutions that secure sensitive information through advanced encryption algorithms, ensuring data integrity and confidentiality across various industries. Encryption software is particularly crucial in sectors such as finance, healthcare, and government, where the protection of sensitive data is a top priority.

Encryption Algorithms: Safeguarding Critical Data

Key Highlights

- Encryption algorithms are fundamental in securing data, whether stored on disks, transmitted over networks, or shared via email. Solutions like disk encryption software, file encryption software, and mobile encryption software are critical in protecting data from unauthorized access. The growing adoption of cloud computing has brought cloud encryption and Encryption as a Service (EaaS) to the forefront, offering businesses scalable and flexible options to secure their data in cloud environments.

Market Segmentation and Adoption

Key Highlights

- Components: The market is divided into software and services, with software taking a dominant position due to its widespread adoption. Encryption software provides essential tools for organizations across various sectors to protect their data from breaches and unauthorized access.

- Deployment Models: On-premise and cloud-based solutions are the primary deployment models. On-premise solutions are favored by organizations with stringent security requirements, while cloud-based solutions offer flexibility and scalability, catering to the evolving needs of businesses.

- Enterprise Size: The market serves both large enterprises and SMEs, with large enterprises leading due to their significant investments in robust cybersecurity measures. SMEs, however, are increasingly adopting encryption solutions as they recognize the importance of data protection.

- Industry Verticals: Key industries include IT & telecommunications, BFSI, healthcare, and government. These sectors are the most critical users of encryption software, driven by the need to secure sensitive information against a backdrop of rising cyber threats.

Regional Analysis: Leading Markets

Key Highlights

- North America: The region is a leader in the encryption software market, supported by stringent regulatory requirements and the presence of major encryption software providers. The enforcement of regulations like the GDPR in Europe and HIPAA in the U.S. underscores the necessity of encryption in maintaining data security.

- Europe: The region's focus on data protection, highlighted by the GDPR, drives significant demand for encryption software. Companies operating in Europe face severe penalties for non-compliance, making encryption a crucial investment.

- Asia-Pacific: This region is poised for rapid growth, driven by digital transformation and increasing awareness of cybersecurity. Government initiatives and investments in encryption technologies are further propelling market expansion in countries like China, India, and Japan.

Regulatory Standards Shaping the Market

Key Highlights

- Compliance Imperatives: Regulatory standards such as GDPR, HIPAA, PCI DSS, and CCPA are crucial in shaping the encryption software market. Compliance with these standards is essential for businesses to avoid penalties and maintain customer trust. These regulations mandate stringent data protection measures, driving the adoption of encryption solutions across various industries.

- Industry-Specific Requirements: Sectors like healthcare and finance have industry-specific regulations that emphasize the importance of encryption. For example, HIPAA mandates the protection of patient data, while PCI DSS focuses on securing payment information, further fueling the demand for encryption software.

Impact of Cyber Attacks and Mobile Theft on Encryption Adoption

Key Highlights

- Rising Cyber Threats: The increasing volume and sophistication of cyber attacks, including ransomware and phishing, are major drivers of encryption software adoption. Encryption provides a critical defense mechanism, ensuring that even if attackers access data, it remains unreadable without the appropriate decryption keys.

- Mobile Device Security: The proliferation of mobile devices, particularly in the workplace, has amplified the risk of data loss due to theft or loss. Mobile encryption software is essential in protecting data stored on smartphones and tablets, mitigating the risk of unauthorized access.

- Remote Work Trends: The expansion of remote work post-pandemic has heightened the need for secure communication channels. End-to-end encryption and network encryption are increasingly deployed to protect sensitive information shared over potentially unsecured networks.

Encryption Software Market Trends

IT & Telecommunication to Hold a Significant Share

- IT & Telecommunications Dominance: The IT & telecommunications sector is expected to hold a significant share of the encryption software market due to escalating data security needs. With vast amounts of sensitive data transmitted daily, organizations in this sector are increasingly adopting encryption algorithms to prevent unauthorized access and data breaches.

- Cloud and Mobile Encryption Growth: The rise of cloud computing has significantly increased the demand for cloud encryption and EaaS. The IT sector's focus on encryption key management to secure data across cloud environments is crucial for compliance with global encryption standards like AES, PCI DSS, and GDPR.

- Technological Innovations: Continuous advancements in encryption technology are vital for meeting the evolving needs of the IT & telecommunications sector. Innovations, such as quantum-safe encryption, are setting new benchmarks in data security, ensuring that sensitive information remains protected against emerging threats.

- Data Breach Concerns: The sharp increase in data breaches emphasizes the urgent need for enhanced encryption measures. The professional services sector, including IT, is particularly vulnerable to cyber threats, underscoring the importance of comprehensive encryption solutions.

Asia-Pacific Growth and Government Initiatives

- Digital Transformation: Asia-Pacific is expected to witness substantial growth in the encryption software market, driven by rapid digital transformation across various industries. As sectors like finance, healthcare, and government embrace digital technologies, the demand for encryption software to secure sensitive data is rising.

- Government Investments: Significant investments by governments in Asia-Pacific to build robust cybersecurity frameworks are driving the development of advanced encryption solutions. Initiatives like Singapore's investment in quantum computing highlight the region's focus on encryption technology to counter cybersecurity threats.

- Cloud Encryption Demand: The increasing adoption of cloud-based platforms in Asia-Pacific is fueling demand for cloud encryption. EaaS is becoming a popular choice for securing data in cloud environments, particularly in the financial sector, where data protection is critical.

- Skill Gap and Consulting Services: The shortage of qualified cybersecurity professionals in Asia-Pacific is creating demand for consulting services to implement encryption software effectively. Industry players are responding by offering specialized consultancy services, contributing to market growth.

Encryption Software Industry Overview

Moderately Consolidated Market: The encryption software market is moderately consolidated, with major global players like IBM, Microsoft, Broadcom Inc., Sophos Ltd., and Thales leading the landscape. These companies dominate due to their comprehensive product portfolios and established customer bases.

Strategic Focus on Innovation: Leading players are increasingly focusing on innovation, particularly in developing quantum-resistant encryption and zero-trust architecture. The demand for integrated security solutions that combine encryption with other cybersecurity measures is also rising, shaping future market trends.

Role of Smaller Vendors: Despite the dominance of large firms, smaller, specialized vendors continue to play a crucial role in niche markets or specific regions, offering tailored encryption solutions that address specific industry needs.

The encryption software market is set for robust growth, driven by the IT & telecommunications sector's commitment to data security and the rapid digital transformation in the Asia-Pacific region. Innovations in encryption technology, increasing regulatory demands, and the rising prevalence of cyber threats are key factors shaping market trends. As organizations prioritize encryption to safeguard sensitive information, the market will continue to expand, offering lucrative opportunities for industry leaders and new entrants alike.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Regulatory Standards Related to Data Transfer and its Security

- 5.1.2 Growing Volume of Strength of Cyber Attacks and Mobile Theft

- 5.2 Market Restraints

- 5.2.1 Expensive Encryption Software Deployment and Maintenance costs

- 5.2.2 Utilization of Open-Source and Pirated Encryption Products

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Service

- 6.2 By Deployment Model

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Enterprise Size

- 6.3.1 Large Enterprises

- 6.3.2 Small & Medium Enterprises

- 6.4 By Function

- 6.4.1 Disk Encryption

- 6.4.2 Communication Encryption

- 6.4.3 File/Folder Encryption

- 6.4.4 Cloud Encryption

- 6.4.5 Database Encryption

- 6.5 By Industry Vertical

- 6.5.1 IT & Telecommunication

- 6.5.2 BFSI

- 6.5.3 Healthcare

- 6.5.4 Government

- 6.5.5 Retail

- 6.5.6 Education

- 6.5.7 Others

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia

- 6.6.4 Australia and New Zealand

- 6.6.5 Middle East and Africa

- 6.6.6 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM

- 7.1.2 Microsoft

- 7.1.3 Broadcom Inc.

- 7.1.4 Sophos Ltd.

- 7.1.5 Thales

- 7.1.6 McAfee, LLC

- 7.1.7 Trend Micro Incorporated

- 7.1.8 Dell Inc.

- 7.1.9 Check Point Software Technologies Ltd.

- 7.1.10 Micro Focus International plc

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日