マイクロプロセッサ:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Microprocessor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644543

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

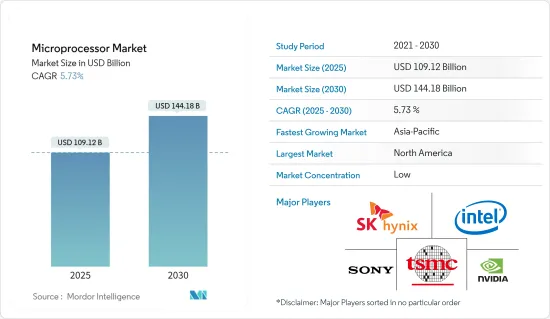

マイクロプロセッサの市場規模は2025年に1,091億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.73%で、2030年には1,441億8,000万米ドルに達すると予測されます。

5Gと高性能コンピューティングデバイスの普及、クラウドベースのソフトウェアとデータセンターの採用増加、人工知能と機械学習ソリューションの進歩、家電と自動車の需要増加により、マイクロプロセッサ市場の成長が促進される可能性が高いです。

主なハイライト

- マイクロプロセッサは、チップ上に構築されたマイクロコンピューターの制御ユニットであり、算術論理演算ユニット(ALU)演算を実行し、他のリンクデバイスと通信することができます。マイクロプロセッサは、制御ユニット、レジスタ・アレイ、ALUから構成されます。ALUは算術演算と論理演算を実行し、コントロール・ユニットはコンピュータを介したデータの流れと命令を監督し、レジスタ・アレイはアキュムレータとデータを格納します。マイクロプロセッサは、フェッチ、デコード、実行を所定の順序で実行します。

- モノのインターネットの急速な台頭は、マイクロプロセッサの利用を促進する重要な理由のひとつです。以前よりもはるかに広範なモノからデータを収集することが技術的にも経済的にも可能になったため、企業はIoT製品やプラットフォームから生成されるデータの複雑さと量を見誤ることが多く、現在収集しているすべてのデータの管理と解釈を支援するソリューションの導入が必要となっています。そのため、IoTインフラの主要コンポーネントの1つであるマイクロプロセッサは、需要の拡大が見込まれています。

- さらに、拡張現実(Augmented Reality)や仮想現実(Virtual Reality)のアプリやデバイス、デジタルカメラやゲーム機に対する需要の高まりが、世界のマイクロプロセッサ市場を前進させています。

- これとは別に、スマートホーム製品の普及が進んでいることも、マイクロプロセッサ需要を押し上げています。スマートロック、火災・煙警報システム、スマートスピーカーなどのデバイスは、ますます人々の生活に浸透しつつあります。特にインド、ブラジルなどの新興諸国では、中間層の消費能力が高まっていることも相まって、研究市場の成長をさらに後押しすると予想されます。

- また、ITインフラ、UPS(無停電電源装置)システム、配電ユニット(PDU)、冷却装置はすべて何らかの形でマイクロプロセッサを使用しているため、データセンター産業の拡大も市場成長に有利なシナリオを描くと予想されます。さらに、トランザクションコストの削減、高機能、大容量ストレージなど、マイクロデータセンターを採用することによる複数のメリットが、こうしたデータセンタータイプの需要を促進し、その過程で調査対象市場の成長を促進すると予想されます。

- しかし、半導体チップの不足、マイクロプロセッサ集積回路の生産に伴う複雑さ、回路設計費用、原材料価格の高騰、コンピュータシステムの出荷台数の減少、低価格モバイル機器の販売増加などの課題が、調査市場の成長を阻んでいます。

- マイクロプロセッサ市場では、COVID-19の影響が顕著です。COVID-19の影響はマイクロプロセッサ市場にも及んだが、パンデミック(世界的大流行)時には、特にコンシューマーエレクトロニクスとヘルスケア産業で需要が大幅に増加しました。ベンダーは、生産能力の制限や、各国での封鎖によるサプライチェーンの制約のため、需要に対応することが困難であると感じていました。

- しかし、半導体メーカーの大部分がマイクロプロセッサやその他の半導体製品の生産規模を拡大するための投資と努力を増やしているため、状況が正常に戻りつつある現在、市場は牽引力を増すと予想されます。さらに、自動化、コネクテッドカー、AI、ML、IoTなどの技術の浸透が進んでいることが、COVID後の期間における調査対象市場の成長に有利な市場シナリオを生み出しています。

マイクロプロセッサ市場動向

市場成長を牽引するコンシューマーエレクトロニクスセグメント

- マイクロプロセッサは、処理速度が速く、サイズが小さく、メンテナンスが容易なため、デスクトップPC、スマートフォン、タブレット、サーバーなどのコンシューマーエレクトロニクス・アプリケーションでますます使用されるようになっています。この多目的電子処理装置は、1秒間に約30億回の演算を行い、メモリ領域間でデータを迅速に転送し、浮動小数点演算などの高度な数学的計算を行うように構成することができます。コンシューマーエレクトロニクス分野の成長はマイクロプロセッサ市場に好影響を与え、当市場の成長と発展に貢献します。

- PC、ゲーム機、スマートフォンなどのゲーム機器には、特定の機能を果たす多数のコンポーネントからなる組み込みシステムが搭載されているため、ゲーム市場の成長は、スマートフォン、ゲーム機、VR/AR機器の成長に貢献し、最終的にマイクロプロセッサの世界の成長に影響を与えます。

- 近年のスマートフォンやタブレットの普及は、PCの需要に影響を与えています。マイクロプロセッサとGPU市場の成長は、新世代のスマートフォンやタブレットの携帯性と性能に影響を受けています。スマートフォンやタブレットに使用されるものと比較すると、PC用プロセッサやGPUは通常より高価です。より多くのユーザーが日常的な作業にスマートフォンやタブレットのような携帯デバイスを選ぶようになったため、デスクトップPCはPCカテゴリーで大幅に減少しました。さらに、PCはライフサイクルが長く、短期間で買い換えることができないため、すぐに改良された技術に簡単にアップグレードできるスマートフォン業界全体の需要が伸びています。

- さらに、5Gの登場により、低遅延で高速なネットワークが利用可能になるため、スマートフォンやその他のウェアラブルデバイスの普及が大幅に促進されると予想され、その過程でマイクロプロセッサの需要が生まれます。エリクソン社によると、世界のスマートフォン契約数は2021年の62億6,000万台から2028年には77億9,000万台に増加すると予想されています。

アジア太平洋地域が大きな市場シェアを占める

- アジア太平洋地域は大きな市場シェアを占めており、予測期間中に最も急速に成長すると予測されています。同地域では、ノートパソコン、携帯電話、デスクトップパソコン、タブレット端末など、スマートフォンやその他のデバイスの利用が増加していることがその要因となっています。急速なデジタル化、ハイテクガジェットの普及拡大、カーエレクトロニクスの進歩などの要因により、中国やインドなどの新興経済諸国も市場拡大に貢献しています。さらに、モノのインターネット(IoT)利用の増加、大規模な政府IT投資、クラウドベースのサービスに対する需要の高まりが、予測期間を通じてこの地域市場を牽引します。

- アジア太平洋地域では最近、高度な機能を備えた高級車の需要が増加しているため、自動車産業はマイクロプロセッサに大きな需要をもたらすと予想されます。さらに、乗客や車両の安全性に関する政府の規制が厳しいことも、アジア太平洋地域の市場成長にプラスに寄与しています。

- 中国は、大規模な家電および自動車製造産業が存在するため、調査市場において優位性を保つと予想されます。中国自動車工業協会によると、2022年4月、中国では約99万6,000台の乗用車と21万台の商用車が生産されました。さらに同月、中国の自動車産業は合計約120万台の自動車を生産しました。

- 半導体チップの需要の高まりと米国との継続的な問題を考慮し、アリババやバイドゥをはじめとするさまざまな中国企業が自社チップの製造に投資しています。中国は第14次5カ年計画で、人工知能、量子コンピューター、半導体、宇宙など7つの技術分野を重点分野としており、これが研究市場の機会を促進すると期待されています。

- 同様の動向は他の国々でも見られ、それぞれの地域で半導体産業の成長を促進するためのイニシアチブを継続的に打ち出しています。例えば、インドのDIR-Vプログラムは、次世代マイクロプロセッサを大量生産することで同国の半導体エコシステムを加速させることを目的としており、最近明らかになった。インド政府は2023年12月までに、ヘビーグレードの商用シリコン生産と設計の勝利を達成したいと考えています。同様に、政府はソニー・インディア、ISRO、BELなどの企業と5つの覚書を締結し、自社で開発したShaktiおよびVega RISC-Vマイクロプロセッサの利用を促進しています。

マイクロプロセッサ産業の概要

マイクロプロセッサ市場は、初期投資の高さから少数の大手企業に集中しています。しかし、市場需要の拡大と安定した収益性により、新たなプレーヤーが市場に参入し、競争が激化することが予想されます。同市場の主要企業には、インテル、Nvidia、クアルコムなどがあります。

2023年2月、インドの先進コンピューティング開発センター(Centre for Development of Advanced Computing:C-DAC)は、同国初の独自設計のマイクロプロセッサ・ファミリーの開発に取り組んでいると発表しました。同センターのプロセッサのロードマップは、同国がマイクロプロセッサで自立することを目的としています。C-DACは、2024年末までに国全体で累積演算能力64ペタフロップス(PF)を達成することを目標としています。

2023年1月、インテルはCES 2023で最新の第13世代HおよびHXシリーズのラップトップ・プロセッサを発表しました。同社によると、これらの高性能ラップトップ・プロセッサは、最大24コアのCPU、DDR5のサポート、PCIe Gen5などを提供します。同社はまた、改良されたIris Xeオンボード・グラフィックスと最大14コアのCPU設計を備えた第13世代インテルCore PおよびUシリーズ・プロセッサも発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- マクロ動向が業界に与える影響

第5章 市場力学

- 市場促進要因

- 高性能でエネルギー効率に優れたプロセッサに対する需要の増加

- 市場抑制要因

- PC需要の減少

第6章 市場セグメンテーション

- タイプ別

- APU

- CPU

- GPU

- FPGA

- 用途別

- コンシューマーエレクトロニクス

- エンタープライズ-コンピュータとサーバー

- 自動車

- 産業

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- TSMC

- SK Hynix Inc.

- Sony Corporation

- Nvidia Corporation

- Samsung Electronics Co. Ltd.

- Qualcomm Technologies

- Broadcom Inc.

- Micron Technology

第8章 投資分析

第9章 市場の将来

目次

The Microprocessor Market size is estimated at USD 109.12 billion in 2025, and is expected to reach USD 144.18 billion by 2030, at a CAGR of 5.73% during the forecast period (2025-2030).

Due to the growing popularity of 5G and high-performance computing devices, increasing adoption of cloud-based software and data centers, advancements in artificial intelligence and machine learning solutions, and the increasing demand for household appliances and automobiles will likely fuel the microprocessor market growth.

Key Highlights

- A microprocessor is a microcomputer's controlling unit, built on a chip, capable of performing Arithmetic Logic Unit (ALU) operations and communicating with other linked devices. A microprocessor comprises a Control Unit, a Register Array, and an ALU. The ALU performs arithmetic and logical operations; the Control Unit supervises data flow and instructions through the computer, and the Register Array stores accumulators and data. The microprocessor performs Fetch, Decode, and Execute in the provided sequence.

- The rapid rise of the Internet of Things is one significant reason for promoting microprocessor usage. As collecting data from a far wider range of things is now technically and economically feasible than before, companies frequently misjudge the complexity and volume of data generated by IoT products and platforms, necessitating the deployment of solutions to help them manage and interpret all of the data they are now collecting. Microprocessors which are among the major component of IoT infrastructure, are thus expected to grow in demand.

- In addition, the growing demand for Augmented Reality and Virtual Reality apps and devices, as well as digital cameras and gaming consoles, is propelling the worldwide microprocessor market forward.

- Apart from this, the increasing penetration of smart home products is also driving the demand for microprocessors. Devices like smart locks, fire, and smoke alarm systems, smart speakers, etc., are increasingly taking their place in the lives of people. Coupled with the increasing spending capacity of the middle class, especially across developing countries such as India, Brazil, etc., are expected to support the growth of the studied market further.

- The expanding data center industry is also expected to create a favorable scenario for the studied market's growth, as IT infrastructure, UPS (uninterruptible power supply) systems, power distribution units (PDUs), and cooling units all use microprocessors in some form or other. Furthermore, the multiple benefits of adopting micro-data centers, such as decreased transactional costs, high functionality, and high storage, are expected to propel the demand for such data center types, driving the studied market's growth in the process.

- However, the factors such as the shortage of semiconductor chips, the complexity involved in the production of microprocessor integrated circuits, circuit design expenses, escalating raw material prices, decreased shipment of computer systems, and increased sales of low-cost mobile devices are challenging the growth of the studied market.

- A notable impact of COVID-19 was observed on the microprocessors market. Although, the demand increased significantly during the pandemic, especially across the consumer electronics and healthcare industry. The vendors felt it hard to match the demand owing to limited production capabilities and supply chain constraints due to widespread lockdowns imposed across various countries.

- However, with the conditions returning to normalcy, the market is expected to gain traction as a significant portion of the semiconductor manufacturers is increasing their investment and efforts to scale up the production of microprocessors and other semiconductor products. Furthermore, the increasing penetration of technologies such as automation, connected cars, AI, ML, and IoT are creating a favorable market scenario for the growth of the studied market in the post-COVID period.

Microprocessor Market Trends

Consumer Electronics Segment to drive the Market Growth

- Microprocessors are increasingly used in consumer electronics applications such as desktop PCs, smartphones, tablets, and servers because of their fast processing speed, small size, and ease of maintenance. This multipurpose electronic processing device may be configured to accomplish about 3 billion activities per second, transport data swiftly between memory regions, and conduct sophisticated mathematical calculations such as floating-point operations. The rising consumer electronic segment will favor the Microprocessor Market, contributing to market growth and progress for the market under consideration.

- The gaming industry has grown significantly in recent years, rather more dramatically since the outbreak of the pandemic, as gaming devices such as PC, game consoles, smartphones, etc., contain embedded systems comprising many components all serving a specific function, the growing gaming market will contribute to the growth of smartphones, Gaming consoles, and VR/AR devices, ultimately influencing the growth of microprocessors globally.

- The popularity of smartphones and tablets in recent years has influenced PC demand. Microprocessor and GPU market growth have been impacted by the portability and performance of new-generation smartphones and tablets. When compared to those utilized in smartphones and tablets, PC processors and GPUs are usually more expensive. Desktop PCs have significantly declined in the PC category as more users chose portable devices such as smartphones and tablets for day-to-day tasks. Furthermore, because PCs have a long lifecycle and cannot be replaced in a short time, there is a growth in overall demand for the smartphone industry, which can be easily upgraded to improved technology quickly.

- Furthermore, the arrival of 5G is expected to significantly expedite the adoption of smartphones and other wearable devices owing to the availability of a low latency and high-speed network, creating the demand for microprocessors in the process. According to Ericsson, global smartphone subscriptions are expected to grow from 6,260 million in 2021 to 7,790 million by 2028.

Asia Pacific to Account for a Significant Market Share

- The Asia-Pacific region commands a significant market share and is predicted to grow the fastest over the forecast period. The increased use of smartphones and other devices in the region, such as laptops, mobile phones, desktop computers, and tablets, is credited with the increase. Due to factors such as fast digitalization, increased penetration of high-tech gadgets, and progress of automotive electronics, developing economies such as China and India are also helping market expansion. Furthermore, increased Internet of Things (IoT) usage, large government IT investment, and rising demand for cloud-based services will drive the regional market throughout the projection period.

- The automotive industry is expected to generate considerable demand for microprocessors as the demand for luxury cars with advanced functionalities has been increasing lately in the Asia Pacific region. Furthermore, stringent government regulations regarding passenger and vehicle safety also contribute positively to the studied market's growth in Asia Pacific.

- China is expected to remain dominant in the studied market due to the presence of a large consumer electronics and automotive manufacturing industry. According to the China Association of Automobile Manufacturers, in April 2022, around 996,000 passenger cars and 210,000 commercial vehicles were produced in China. Additionally, during the month, China's automotive industry produced a total of about 1.2 million vehicles.

- Considering the growing demand for semiconductor chips, and ongoing issues with the United States, various Chinese firms, including Alibaba and Baidu, among others, have been making investments in manufacturing their own chips, a move considered progress toward China's goal of increasing local capabilities in a crucial technology. China has outlined seven technology fields in its 14th five-year plan, including artificial intelligence, quantum computing, semiconductors, and space, as its priority which is expected to drive opportunities in the studied market.

- A similar trend has been observed across other countries as well, which are continuously launching initiatives to drive the semiconductor industry's growth in their respective regions. For instance, India's DIR-V program, which aims to accelerate the country's semiconductor ecosystem by mass-producing next-generation indigenous microprocessors, was recently revealed. By December 2023, the Indian government hopes to have achieved heavy-grade commercial silicon production and design victories. In the same vein, the government has inked five Memorandums of Understanding with companies such as Sony India, ISRO, BEL, and others to promote the usage of the Shakti and Vega RISC-V microprocessors, which were created in-house.

Microprocessor Industry Overview

The Microprocessor Market is concentrated due to the high initial investments and is dominated by a few major players. However, the growing market demand and stable profitability are expected to drive new players into the market, making it more competitive. Some of the key players in the market are Intel, Nvidia, Qualcomm, etc.

In February 2023, India's Centre for Development of Advanced Computing (C-DAC) announced they are working on the country's first indigenously designed family of microprocessors. The organization's roadmap for processors is aimed at helping the country become self-reliant in microprocessors. C-DAC targets to achieve 64 PetaFlops (PF) of cumulative compute power across the country by the end of 2024.

In January 2023, Intel unveiled its latest 13th Gen H and HX series of laptop processors at CES 2023. According to the company, these high-performance laptop processors offer up to 24-core CPU, DDR5 support, PCIe Gen5, and more. The company also announced the 13th Gen Intel Core P and U series of processors with improved Iris Xe onboard graphics and up to 14 core CPU designs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in demand for high performance and energy-efficient processors

- 5.2 Market Restraints

- 5.2.1 Decrease in demand for PCs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 APU

- 6.1.2 CPU

- 6.1.3 GPU

- 6.1.4 FPGA

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Enterprise - Computer and Servers

- 6.2.3 Automotive

- 6.2.4 Industrial

- 6.2.5 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 TSMC

- 7.1.3 SK Hynix Inc.

- 7.1.4 Sony Corporation

- 7.1.5 Nvidia Corporation

- 7.1.6 Samsung Electronics Co. Ltd.

- 7.1.7 Qualcomm Technologies

- 7.1.8 Broadcom Inc.

- 7.1.9 Micron Technology

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日