|

|

市場調査レポート

商品コード

1644493

インドの屋根:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの屋根:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

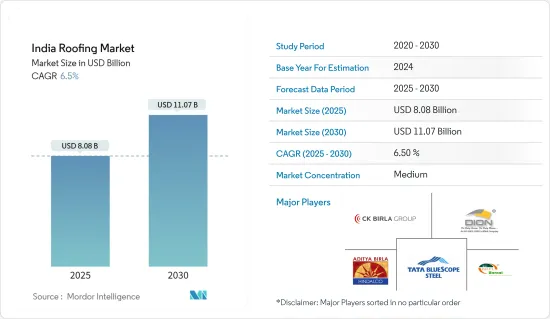

インドの屋根市場規模は2025年に80億8,000万米ドルと推定され、2030年には110億7,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.5%です。

インドの屋根材市場は、急速な都市化、産業の発展、大規模なインフラプロジェクトに後押しされ、力強い成長を遂げています。政府がスマートシティ、空港、高速道路などのイニシアチブを優先する中、住宅、商業、工業の各領域で高級屋根ソリューションの需要が急増しています。これを受け、メーカー各社は多様な市場の需要に合わせた革新的で耐久性が高く、エネルギー効率の高い製品を展開しています。

インドでは所得水準が上昇しているため、消費者は従来の屋根材からより信頼性の高い代替品へのシフトを促し、市場成長を大きく後押ししています。ポリカーボネート製屋根シートは、工業用建物や大規模な商業用建物への施工が容易なため、人気が高まっています。ポリカーボネート屋根材は耐候性に優れ、さまざまな質感やデザインがあり、メンテナンスコストも低いです。従来の用途にとどまらず、天窓、プール、歩道、表示看板などにも採用されています。ポリカーボネート屋根材は汎用性と耐久性に優れているため、様々な用途に使用され、市場での需要拡大に貢献しています。

ある産業レポートによると、技術革新、特に新しい屋根技術の出現がインドの屋根市場の成長を促進するといいます。特に、雨水の吸収、断熱、美観の向上といったメリットを提供するグリーン屋根は際立っています。緑化屋根はエネルギー効率を向上させるだけでなく、都市の生物多様性に貢献し、都市のヒートアイランド現象を抑制します。さらに、先進的機械設備によって屋根材のシームレスな施工と既存インフラのアップグレードが可能になるため、予測期間中に市場は勢いを増すと予想されます。最先端機械の統合により、屋根工事プロジェクトの精度と効率が確保され、市場拡大をさらに後押しします。

インドの屋根市場動向

活況を呈するインドの建設と都市開発:FDIの伸びと将来予測

不動産セグメントには、住宅、オフィス、店舗、ホテル、レジャーパークなどが含まれます。一方、都市開発セグメントでは、給水、衛生、都市交通、学校、医療などが含まれます。2023年の産業レポートによると、インドの人口は2047年までに16億4,000万人に達し、その51%が都市部に居住すると推定されています。2,000年4月から2024年3月までの間に、建設(インフラ)部門は総額339億1,000万米ドルの外国直接投資(FDI)流入を誘致し、同国におけるFDI受入額のトップクラスとなりました。

自動化ルートでは、タウンシップ、モール、複合ショッピングセンター、商業施設の運営・管理のための完成済みプロジェクトに100%のFDIが認められています。同様に、都市交通、上水道、下水道、汚水処理などの都市インフラについても、自動ルートで100%の直接投資が認められています。

予測では、2047年までにインドの人口の半分以上が都市部に居住するようになり、住宅、商業、インフラプロジェクトの需要が高まります。さらに、自動ルートによる100%の外国直接投資(FDI)を認めるなど、インド政府の有利な施策は、世界の投資家にとってこれらのセグメントの魅力を高めています。インフラと不動産の両セグメントへのFDIの着実な流入により、インドの建設産業は継続的な拡大と急成長の機会を迎えています。

政府主導の手ごろな価格の住宅:インド屋根材市場の重要な触媒

産業をリードする金融プラットフォームが報じたように、2022年の国家予算は住宅セクターへの政府のコミットメントを強調し、住宅都市開発省(MoHUA)に5,000億インドルピー(6兆1,114億3,000万米ドル)を割り当て、停滞している住宅プロジェクトを促進するために35億米ドルの基金を設立しました。インドの都市化率は2030年までに33%から40%以上に上昇すると予測されており、Invest Indiaは、2,500万戸の中規模と手頃な住宅ユニットの追加需要があると見込んでいます。

2023年には、首相の住宅計画としても知られるPradhan Mantri Awas Yojana(PMAY)のもと、都市部で540万戸の住宅が完成しました。しかし、2020年には、都市部の貧困層の住宅需要は約1,100万戸に達すると推定されています。

政府のコミットメントは、多額の財政投資やPMAYのようなプログラムを通じて明らかであり、住宅不足に取り組む決意を強調しています。都市化が加速し、中級住宅や手頃な価格の住宅への需要が高まるにつれ、このセグメントは投資と開発にとって有利な手段となっています。しかし、急増する都市住民の住宅ニーズに真に応えるには、既存の不足を埋める持続的な取り組みが不可欠です。

インドの屋根産業概要

Saint-Gobain、Mongia Roofing、JSW Steel、Boral Roofing、Etex、Visaka Industriesなどの主要企業が、国内外で圧倒的なシェアを誇っています。これらの企業は、一貫して高品質の屋根材ソリューションを提供し、市場での存在感を高めることで、主要企業としての地位を確立しています。

金属屋根材、アスファルトシングル、粘土瓦、コンクリート屋根材、瀝青膜、緑化屋根材など、多様な屋根材が市場を牽引しています。各材料は、耐久性、費用対効果、環境持続可能性といった独自のメリットを提供し、消費者の多様な嗜好やニーズに対応しています。

屋根材市場は細分化が進んでおり、大規模メーカーと地元サプライヤーの両方が存在します。これらのメーカーは、高級品から手頃な価格の屋根材まで、さまざまなセグメントに対応しています。このように細分化されているため、競合情勢は技術革新と顧客中心のソリューションが盛んで、消費者は特定の要件を満たす幅広い選択肢を利用できます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 屋根セグメントにおける技術革新

- 産業のバリューチェーン/サプライチェーン分析

- 建設産業における政府規制とイニシアチブの影響

- 政府のインフラ開発計画に関するレビューと解説

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- 市場促進要因

- 可処分所得の増加と中間層の拡大

- 屋根材ソリューションに対する意識の高まり

- 市場抑制要因

- 偽造品や規格外の屋根材の存在が大きな課題

- 屋根産業は熟練労働者の不足に直面している

- 市場機会

- 急速な都市化と建設ブーム

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第6章 市場セグメンテーション

- セクター別

- 商業用建設

- 住宅用建設

- 工業用建設

- 材料別

- アスファルト

- タイル

- 金属

- その他

- 屋根タイプ別

- 平屋根

- 傾斜屋根

第7章 競合情勢

- 企業プロファイル

- Tata Bluescope Steel

- CK Birla Group

- Hindalco Ind Ltd

- Bansal Roofing Products Limited

- Dion Incorporation

- Everest Industries Limited

- Moon Pvc Roofing

- Aqua Star

- Indian Roofing Industries Pvt. Ltd

- Metecno India Pvt. Limited*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

The India Roofing Market size is estimated at USD 8.08 billion in 2025, and is expected to reach USD 11.07 billion by 2030, at a CAGR of 6.5% during the forecast period (2025-2030).

The Indian roofing market is experiencing robust growth, propelled by swift urbanization, industrial growth, and extensive infrastructure projects. As the government prioritizes initiatives like smart cities, airports, and highways, the demand for premium roofing solutions surges across residential, commercial, and industrial domains. In response, manufacturers are rolling out innovative, durable, and energy-efficient products tailored to diverse market demands.

In India, rising income levels are prompting consumers to shift from traditional roofing materials to more reliable alternatives, significantly driving market growth. Polycarbonate roofing sheets, favored for their easy installation in industrial and large-scale commercial buildings, are becoming increasingly popular. These sheets are weather-resistant, come in various textures and designs, and boast low maintenance costs. Beyond traditional uses, they're also employed in skylights, swimming pools, walkways, and display signboards. The versatility and durability of polycarbonate roofing sheets make them a preferred choice for various applications, contributing to their growing demand in the market.

According to an industry report, technological innovations, especially the emergence of new roofing technologies, are set to propel the growth of the roofing market in India. Notably, green roofing stands out, offering benefits like rainwater absorption, insulation, and enhanced aesthetic appeal. Green roofing systems not only improve energy efficiency but also contribute to urban biodiversity and reduce the urban heat island effect. Furthermore, the market is expected to gain momentum during the forecast period, thanks to the seamless installation of roofing components and upgrades to existing infrastructure, facilitated by advanced machinery. The integration of cutting-edge machinery ensures precision and efficiency in roofing projects, further driving market expansion.

India Roofing Market Trends

Booming Construction and Urban Development in India: FDI Growth and Future Projections

The real estate segment includes residential properties, offices, retail spaces, hotels, and leisure parks. In contrast, the urban development segment covers areas such as water supply, sanitation, urban transport, schools, and healthcare. As per industry reports from 2023, India's population was expected to reach 1.64 billion by 2047, with an estimated 51% residing in urban centers. From April 2000 to March 2024, the construction (infrastructure) sector attracted foreign direct investment (FDI) inflows totaling USD 33.91 billion, making it one of the top recipients of FDI in the country.

Under the automatic route, 100% FDI is permitted in completed projects for the operations and management of townships, malls, shopping complexes, and business constructions. Similarly, 100% FDI is also allowed for urban infrastructures, including urban transport, water supply, sewerage, and sewage treatment, all under the automatic route.

Projections indicate that by 2047, more than half of India's populace will reside in urban locales, amplifying the demand for residential, commercial, and infrastructural projects. Furthermore, the Indian government's favorable policies, such as permitting 100% Foreign Direct Investment (FDI) through the automatic route, enhance the allure of these sectors for global investors. With a steady influx of FDI into both infrastructure and real estate, India's construction landscape is primed for ongoing expansion and burgeoning opportunities.

Government-Driven Growth in Affordable Housing: A Key Catalyst for the Roofing Market in India

As reported by an industry-leading financial platform, the 2022 national budget underscored the government's commitment to the housing sector, allocating INR 50,000 crore (USD 6111.43 billion) to the Ministry of Housing and Urban Development (MoHUA) and establishing a USD 3.5 billion fund to expedite stalled housing projects. With urbanization in India projected to rise from 33% to over 40% by 2030, Invest India estimates a demand for an additional 25 million mid-range and affordable housing units.

In 2023, under the Pradhan Mantri Awas Yojana (PMAY), also known as The Prime Minister's Housing Plan, India saw the completion of 5.4 million houses in urban areas. However, in 2020, the demand for housing among the urban poor was estimated at around 11 million housing complexes.

The government's commitment is evident through substantial financial investments and programs like PMAY, underscoring its determination to address the housing shortage. As urbanization accelerates and the demand for mid-range and affordable housing intensifies, the sector emerges as a lucrative avenue for investment and development. Yet, to truly cater to the housing needs of India's burgeoning urban populace, sustained efforts are essential to bridge the existing deficit.

India Roofing Industry Overview

Leading companies, including Saint-Gobain, Mongia Roofing, JSW Steel, Boral Roofing, Etex, and Visaka Industries, hold a dominant position in the market, boasting both national and international reach. These companies have established themselves as key players by consistently delivering high-quality roofing solutions and expanding their market presence.

Diverse roofing materials, including metal roofing, asphalt shingles, clay tiles, concrete roofing, bituminous membranes, and green roofing solutions, drive the market. Each material offers unique benefits, such as durability, cost-effectiveness, and environmental sustainability, catering to the varied preferences and needs of consumers.

The roofing market exhibits high fragmentation, accommodating both large-scale manufacturers and local suppliers. These players cater to a spectrum of segments, ranging from premium to budget-friendly roofing materials. This fragmentation allows for a competitive landscape where innovation and customer-centric solutions thrive, ensuring that consumers have access to a wide range of options to meet their specific requirements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Innovations in the Roofing Sector

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of Government Regulations and Initiatives taken in the Construction Industry

- 4.5 Review and Commentary on the Extent of Government Infrastructure Development Schemes

- 4.6 Impact of Geopolitics and Pandemics on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Disposable Income and Middle-Class Expansion

- 5.1.2 Increased Awareness of Roofing Solutions

- 5.2 Market Restraints

- 5.2.1 The presence of counterfeit or substandard roofing materials in the market poses a significant challenge

- 5.2.2 The roofing industry faces a shortage of skilled labor

- 5.3 Market Opportunities

- 5.3.1 Rapid Urbanization and Construction Boom

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitutes

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Sector

- 6.1.1 Commercial Construction

- 6.1.2 Residential Construction

- 6.1.3 Industrial Construction

- 6.2 By Material

- 6.2.1 Bituminous

- 6.2.2 Tiles

- 6.2.3 Metal

- 6.2.4 Other Materials

- 6.3 By Roofing Type

- 6.3.1 Flat Roof

- 6.3.2 Slope Roof

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Tata Bluescope Steel

- 7.1.2 CK Birla Group

- 7.1.3 Hindalco Ind Ltd

- 7.1.4 Bansal Roofing Products Limited

- 7.1.5 Dion Incorporation

- 7.1.6 Everest Industries Limited

- 7.1.7 Moon Pvc Roofing

- 7.1.8 Aqua Star

- 7.1.9 Indian Roofing Industries Pvt. Ltd

- 7.1.10 Metecno India Pvt. Limited*

- 7.2 Other Companies