|

市場調査レポート

商品コード

1644489

米国の電気エンクロージャ:市場シェア分析、産業動向、統計、成長予測(2025~2030年)US Electrical Enclosures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の電気エンクロージャ:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 163 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

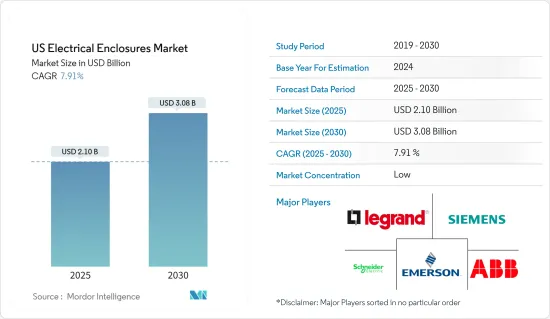

米国の電気エンクロージャ市場規模は2025年に21億米ドルと推定され、予測期間(2025-2030年)のCAGRは7.91%で、2030年には30億8,000万米ドルに達すると予測されます。

主なハイライト

- 電力および産業インフラの増加と、安全な労働力の必要性が相まって、産業界の設備に対する様々な安全基準が策定されています。これにより、電気エンクロージャは産業用および住宅用アプリケーションにおいて重要な要素となっています。日本では、特に石油・ガス、自動車、発電といった様々なエンドユーザー・セグメントからの電力消費が伸びているため、需要が増加しています。

- 米国バージニア州に本部を置く全米電機工業会(NEMA)は、カバー、耐腐食性、雨や水没から保護する能力などの規格を制定しました。また、その性能に基づいて電気エンクロージャを分類しています。エンクロージャー業界は、特定のエンドユーザー業界ごとの規制に従わなければならないです。例えば、石油・ガス産業は本質安全防火・防爆エンクロージャを使用しています。予測期間中、国家OCSリース・プログラムに起因する、同国におけるオフショアおよびオンショアの石油・ガス・プロジェクトの増加により、同国での事故発生を回避または抑制するための電気エンクロージャの需要が増加すると予想されます。

- 米国での石油生産は急速に拡大し続けています。例えば、米国有数の石油生産会社であるエクソンモービルは、テキサス州西部のパーミアン盆地での生産活動を拡大し、早ければ2024年までに石油換算で日産100万バレル(BPD)を超える生産を行う計画を発表しました。同様にシェブロンも、2023年までに石油換算生産量を90万BPDに増やす計画です。

- COVID-19の大流行でアメリカ人が家に閉じこもり、サービス業からの商品需要の変化がサプライチェーンにストレスを与えました。ウイルスは工場の労働力や、原材料供給業者や製造業者といった様々な利害関係者にも影響を及ぼし、その結果、電気筐体業界全体で原材料不足が発生しました。ISMによると、製造業の成長の可能性は、部品や労働力不足による労働者の欠勤や短期の操業停止によって妨げられています。

米国の電気エンクロージャー市場動向

商業スペースとビル産業が市場需要を牽引

- 商業ビルでは、電気パネルや電気機器専用のスペースが設けられるのが一般的です。多くの場合、商業ビルには主要な電気サービスルームがあり、他の階には小さな電気ルームがあります。米国電気工事規定では、過電流装置への容易なアクセスを確保し、保守点検のための十分なスペースを確保するため、盤の周囲に作業スペースと呼ばれる「クリアスペース」を設けることを義務付けています。作業スペースは、電気機器の電圧、周囲の機器や壁によって異なります。

- 米国国勢調査局によると、2008年から2020年にかけて米国で行われた商業プロジェクトに対する公共建設支出の額は、時系列で変化しています。2019年、公共部門は商業建設プロジェクトに約43億米ドルを支出しました。この数字は、翌年には約38億3,000万米ドルまで減少しました。現在、民間オフィス、倉庫、小売/ショッピングが主な主導権を握っています。しかし、ビル建設はスマート・ビルディングに移行しつつあり、商業プロジェクトが増加すると予想されます。

- 保護要件はそれほど厳しくないため、商用グレードのエンクロージャーが適しているかもしれないです。NEMA 1は屋内用に設計されており、偶発的な接触や汚れから保護します。例えば、米国でエンクロージャーを供給しているハモンド・エレクトロニクス社は、NEMA 3Rのフルラインを持っており、多くの屋外用途に最適です。

- さらに、米国エネルギー省(DOE)によると、HVACと照明だけで、平均的な商業ビルのエネルギー使用量の約50%を消費しています。スマート・ビルディング・オートメーション・システム、照明、HVACソリューションを取り入れることで、エネルギーコストを30%から50%削減することができます。米国エネルギー情報局によると、商業ビルは米国のエネルギー消費の約20%、温室効果ガス排出の12%を占めています。無駄を省き、エネルギーを節約することで、スマートビルは国際社会に利益をもたらします。スマートビルディングの増加に伴い、市場は大きな需要に応えることが期待されます。

最も高い市場シェアを占める産業用セグメント

- 機械や配線は、人間や他の外部体との直接的な接触から保護されるものであり、そうでなければ事故につながったり、人命や機械に危害を及ぼす可能性があります。これらのキャビネットは、内部に設置された重要な部品に十分な強度と安全性を提供するため、業界標準に従って製造されなければならないです。

- 環境規制、高い資本コスト、最新の認証要件のため、主に自社施設を使用していたパネルビルダーや機械メーカーは、経営が難しいと感じていました。

- 多くのメーカーは、電気エンクロージャの規格ファミリーを制定する国際電気標準会議(IEC)や、技術の進歩と人類の利益のために規格を制定する技術専門組織である電気電子学会(IEEE)を利用しています。産業用途のエンクロージャーを選ぶ際には、材質、保護、取り付け、気候制御、サイズ、モジュール性、汎用性などの要素が考慮されます。

- 全米電気機器工業会(NEMA)は、電気エンクロージャを使用できる環境の種類を指定するために、標準評価システムを採用しています。これは、特定の環境条件に耐える固定エンクロージャの能力を示すために広く使用されています。

- NEMAは、規格の使用はユーザーとメーカーの双方にメリットがあると考えています。それは、製造者と購入者の関係の安全性、経済性、コミュニケーションを高めます。NEMA規格は、製品の特性と能力を説明するものです。

米国の電気エンクロージャ産業の概要

米国の電気エンクロージャ市場は断片化されています。インダストリー4.0は、さまざまな地域でのエネルギー消費の増加とともに、電子エンクロージャ市場に機会を提供しています。既存の競合企業間の敵対関係は高いです。今後、大企業のイノベーション戦略が電子エンクロージャ市場を牽引します。

- 2021年2月-Legrand AV米国は、新しいOn-Q Dual-Purpose In-Wall Enclosuresを発表しました。このソリューションは、9インチ(ENP0900-NA)と17インチ(ENP1700-NA)のフォームファクターで提供され、テレビの背後のAVストレージや構造化配線用のエンクロージャーとして使用できます。デュアルパーパスインウォールエンクロージャーは、ケーブルボックスやストリーミングプレーヤーなどを便利に収納できるよう設計されています。

- 2020年12月-Innovation Summit North America 2020で、シュナイダーエレクトリックは米国の製造リソースをアップグレードする4,000万米ドルのプロジェクトによる米国での拡張計画を発表しました。また、産業用モノのインターネット(IIoT)をターゲットとした堅牢なデータセンター用エンクロージャの新セットを発表。屋内産業環境向けに設計されたEcoStruxure Micro Data Center R-Seriesは、工場フロアのような場所でエッジ・コンピューティング・インフラを迅速かつ簡単に導入・管理する方法を提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 産業バリューチェーン分析

- 電気エンクロージャーの規格

- COVID-19の業界バリューチェーンへの影響

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 再生可能エネルギーの消費と容量の増加

- 発電・配電網の老朽化

- 市場抑制要因

- 産業界の景気減速

第6章 市場セグメンテーション

- 材料タイプ別

- 金属

- 非金属

- 用途別

- 発電および配電

- 金属および鉱業

- 輸送

- 石油・ガス

- 商業スペースおよびビル

- プロセス産業

- その他の用途

- エンドユーザー別

- 産業

- 商業

- 住宅

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Legrand SA

- Hubbell Inc.

- Emerson Electric Co.

- ABB Ltd

- Eaton Corporation

- Hammond Manufacturing Ltd

- AZZ Inc.

- Austin Electrical Enclosures

- Siemens AG

- Nvent Electric PLC

- Rittal GmbH & Co. Kg

- Adalet(Scott Fetzer Company)

第8章 投資分析

第9章 市場の将来

The US Electrical Enclosures Market size is estimated at USD 2.10 billion in 2025, and is expected to reach USD 3.08 billion by 2030, at a CAGR of 7.91% during the forecast period (2025-2030).

Key Highlights

- The increasing power and industrial infrastructure, combined with the need for a safe workforce, has led to various safety standards for the equipment in the industries. This has made electrical enclosures a crucial element in industrial and residential applications. The country has increased demand, owing to the growing electric consumption from various end-user segments, especially from the oil and gas, automotive, and power generation segments.

- The National Electrical Manufacturers Association (NEMA), based out of Virginia, United States, established the standards, such as cover, corrosion resistance, ability to protect from rain and submersion, etc. It also classified electrical enclosures based on their performance. The enclosure industry has to follow the regulations as per a specific end-user industry. For instance, the oil and gas industry uses intrinsically safe, fire and explosion-proof enclosures. Over the forecast period, the increasing offshore and onshore oil and gas projects in the country, owing to the National OCS leasing program, are expected to increase the demand for electrical enclosures to avoid or control any incidents from further taking place in the country.

- Oil production in the United States continues to expand rapidly. For instance, ExxonMobil, one of the prominent oil producers in the country, announced its plans to increase the production activity in the Permian Basin of West Texas by producing more than 1 million barrels per day (BPD) oil-equivalent by as early as the year 2024. Similarly, Chevron plans to increase its net oil-equivalent production to reach 900,000 BPD by 2023.

- As the COVID-19 pandemic kept Americans at home, a change in demand for commodities from services stressed supply chains. The virus also affects labor at factories and various stakeholders such as raw material suppliers and manufacturers, resulting in raw material shortages across the electrical enclosure industry. According to the ISM, manufacturing's growth potential has been hampered by worker absenteeism and short-term shutdowns due to component and labor shortages.

US Electrical Enclosures Market Trends

Commercial spaces and buildings industry to drive the market demand

- It is typical for space to be dedicated to electrical panels and equipment in a commercial building. Often, commercial buildings will have a leading electrical service room and smaller electrical rooms on the other floors. The National Electrical Code requires "clear space," referred to as working space around panelboard, to ensure easy access to overcurrent devices and provide adequate space for maintenance and inspection. The working space will vary as a function of the voltage of the electrical equipment and the surrounding equipment and walls.

- According to US Census Bureau, the value of public construction spending on commercial projects in the United States between 2008 and 2020 varied over time. In 2019, the public sector spent approximately USD 4.3 billion on commercial construction projects. This number had dropped to around USD 3.83 billion by the following year. Currently, private offices, warehouses, and retail/shopping take the primary lead. However, the building construction is moving toward the smart building, which is expected to increase the commercial projects.

- As protection requirements are less severe, a commercial-grade enclosure might be suitable. NEMA 1 is designed for indoor use and protects against incidental contact and dirt. For instance, Hammond Electronics Limited, which supply its enclosure in the United States, has a full NEMA 3R line and is ideal for many outdoor applications.

- Additionally, according to the US Department of Energy (DOE), HVAC, lighting alone consume about 50% of energy use in the average commercial building. Incorporating smart building automation systems, lighting, and HVAC solutions can decrease energy costs between 30% and 50%. According to the United States Energy Information Administration, commercial buildings account for nearly 20% of United States energy consumption and 12% of greenhouse gas emissions. By reducing waste and conserving energy, smart buildings create benefits for the global community. With increasing smart buildings, the market is expected to cater to significant demand.

Industrial segment to hold the highest market share

- Machine and wiring are protected from direct contact with humans and other external bodies, which could otherwise result in an accident or harm human life or the machine. These cabinets must be built according to industry standards to offer enough strength and safety for vital components installed inside.

- Due to environmental regulations, high capital costs, and the latest certification requirements, panel builders and machine manufacturers who predominantly used their facilities found it difficult to run.

- Many manufacturers use the International Electrotechnical Commission (IEC), which establishes a family of electrical enclosure standards, and the Institute of Electrical and Electronics Engineers (IEEE), a technical professional organization that establishes standards to advance technology and benefit humanity. When choosing an enclosure for industrial applications, factors such as material, protection, mounting, climate control, size, modularity, and versatility are considered.

- The National Electrical Manufacturers Association (NEMA) employs a standard rating system to specify the types of settings in which an electrical enclosure can be utilized. It is widely used to indicate a fixed enclosure's ability to tolerate specific environmental conditions.

- NEMA believes that using standards benefits both the user and the manufacturer. It increases the manufacturer-purchaser relationship's safety, economics, and communication. A NEMA standard describes a product in terms of its characteristics and capabilities.

US Electrical Enclosures Industry Overview

The United States Electrical Enclosures Market is fragmented. Industry 4.0, along with the increasing energy consumption in different regions, provides opportunities in the electronic enclosures market. The competitive rivalry among existing competitors is high. Moving forward, the innovation strategies of large companies are driving the electronic enclosures market.

- February 2021 - Legrand AV United States announced its new On-Q Dual-Purpose In-Wall Enclosures. The solutions are offered in 9-inch (ENP0900-NA) and 17-inch (ENP1700-NA) form factors and can be used for AV storage behind a TV or as enclosures for structured wiring. The Dual-Purpose In-Wall Enclosures are designed to house cable boxes, streaming players, and more conveniently.

- December 2020 - At the Innovation Summit North America 2020, Schneider Electric shared its plans for expansion in the United States with USD 40 million projects to upgrade its US manufacturing resources. The company also unveiled a new set of ruggedized data-center enclosures targeting the Industrial Internet of Things (IIoT). Designed for indoor industrial environments, the EcoStruxure Micro Data Center R-Series offers a fast and straightforward way to deploy and manage edge computing infrastructure in a place like a factory floor.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Electrical Enclosure Standards

- 4.5 COVID-19 Impact on Industry Value Chain

- 4.6 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Consumption and Capacity of Renewable Energy

- 5.1.2 Aging Power Generation and Distribution Network

- 5.2 Market Restraints

- 5.2.1 Economic Slowdown in Industries

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Metallic

- 6.1.2 Non-metallic

- 6.2 By Application

- 6.2.1 Power Generation and Distribution

- 6.2.2 Metal and Mining

- 6.2.3 Transportation

- 6.2.4 Oil and Gas

- 6.2.5 Commercial Spaces and Buildings

- 6.2.6 Process Industries

- 6.2.7 Other Applications

- 6.3 By End-User

- 6.3.1 Industrial

- 6.3.2 Commercial

- 6.3.3 Residential

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Legrand SA

- 7.1.3 Hubbell Inc.

- 7.1.4 Emerson Electric Co.

- 7.1.5 ABB Ltd

- 7.1.6 Eaton Corporation

- 7.1.7 Hammond Manufacturing Ltd

- 7.1.8 AZZ Inc.

- 7.1.9 Austin Electrical Enclosures

- 7.1.10 Siemens AG

- 7.1.11 Nvent Electric PLC

- 7.1.12 Rittal GmbH & Co. Kg

- 7.1.13 Adalet (Scott Fetzer Company)