|

市場調査レポート

商品コード

1644384

ゲーミングGPU:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゲーミングGPU:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

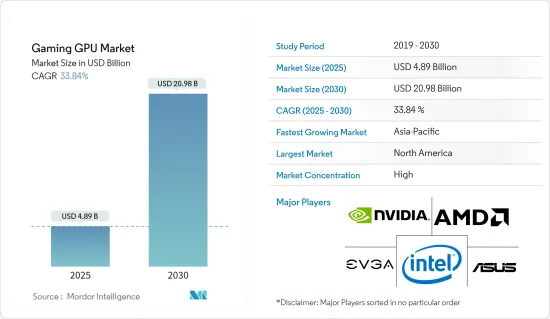

ゲーミングGPUの市場規模は2025年に48億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは33.84%で、2030年には209億8,000万米ドルに達すると予測されます。

ミレニアル世代におけるゲーミフィケーション傾向の高まりにより、ビデオゲーマー向けの仮想世界の導入が進んでいます。ゲーム機もまた、レストラン、ゲームセンター、バーで見られる強力な位置情報機器から、ゲーム機、そしてPCという形の家庭内機器へと進化してきました。ムーアの法則によってチップの価格が下がり、性能が向上するにつれて、人々は家庭用のゲーム機を買い増し、これはロケーションベースのゲーム機を犠牲にする正の価格弾力性効果をもたらしました。ここ数年、ゲーム機の販売台数が増加しているため、ゲーミングGPUの需要も大きく伸びています。

主なハイライト

- スマートフォン、タブレット、PC、ゲーム機のゲーム用途への普及に伴い、グラフィックスを多用するゲーム用途のハイエンド・コンピューティング・システムに対する需要が増加しています。ゲームに必要な2Dおよび3Dグラフィックスに関連する複雑な数学的計算を処理できる専用プロセッサに対する需要の高まりが、GPU市場の需要を牽引しています。

- また、高性能コンピューティングの技術的進歩も、GPUベンダーにチャンスをもたらす可能性があります。例えば、今年4月、Nvidiaは、研究者がNVIDIA GPUを搭載したスーパーコンピュータを使用して、4月25日にハッブルのデータの動向を発見したと発表しました。また、ハイパフォーマンス・コンピューティングは、NVIDIA GPUを使用して、すべての惑星の理解を深め、その苛酷な大気を分析しています。

- 市場のその他の促進要因としては、自動車、製造、不動産、ヘルスケアなどの産業が挙げられ、グラフィックス・アプリケーションや3Dコンテンツをサポートするプロセッサの利用が増加しています。例えば、自動車分野の製造・設計アプリケーションでは、CADやシミュレーション・ソフトウェアがGPUを使用して、重要なアプリケーション用のリアルな画像やアニメーションを作成します。

- ゲーミングGPUは高度な技術と素材を使用しています。現在のGPUが高価格である主な要因のひとつは、製造コストが高いことです。生産者は余裕のある材料しか生産できません。生産者は、製造コストの上昇によって製品の質や量を犠牲にすることなく利益を最大化しようと考えており、それがGPUの販売価格の上昇を引き起こしています。このような莫大な初期投資のため、消費者は最新のゲーミングGPU以外のものを機器に搭載することを好み、これが市場成長の課題となっています。

- 現代のゲーム機やサーバーは、ゲーミングGPU回路を含む多くの部品を利用しています。COVID-19は、サプライチェーンの問題により、これらの部品の多くの平均的な生産を脅かしました。しかし、半導体鋳造所が生産を再開し始めたため、市場のメーカー各社はやる気を取り戻しました。クラウドコンピューティング、ゲーム、データセンターサーバー、自動化、AI技術の需要は、GPUメーカーがパンデミックの後半に成長を復活させるのに役立つ可能性があります。

ゲーミングGPU市場動向

ゲームコンソール、拡張現実(AR)、仮想現実(VR)の需要増加が市場を牽引

esportsやその他のオンラインゲームの普及に伴い、コンソールでのビデオゲームは増加傾向にあり、今後数年でさらなる成長機会を示すと思われます。この動向の結果、接続プロバイダーやエンターテインメントプロバイダーは、高速ブロードバンドやライブスポーツなど、コンソール関連のビデオサービスを提供し、OTTサービスを通じて視聴者を最適に収益化することで、コンソールゲーマーをターゲットにすることができます。ビデオゲーム開発会社は、esportsイベントやオリジナルコンテンツへのアクセスなど、ゲーム配信サービスのプレミアム価格を提供することができます。

- クラウドゲーミングの台頭により、GPU市場は近年上昇傾向にあります。Shadowを運営するフランスの新興企業Bladeは、ゲーマー向けのクラウド・コンピューティング・サービスで、プレイヤーは月額利用料でデータセンター内のゲーミングPCにアクセスできます。同社は、他のクラウドゲーミングサービスと比較して、Windows 11のフル機能を提供しています。同社は現在、Intel Xeon 2620プロセッサ、Nvidia Quadro P5000 GPU、Nvidia GeForce GTX 1080の8スレッド、12GBのRAM、256GBのストレージを搭載したシングル構成を月額35米ドルで提供しています。

- さらに、大手ゲーム開発会社も、高いグラフィック品質を持つコンソールベースのゲーム開発に注力しており、ゲーム分野の成長に貢献しています。ソニーとマイクロソフトは、ゲーム機を8K対応として売り込むのではなく、120fpsまでのリフレッシュレートを優先し、ゲーム体験をシームレスなものにしています。Nvidiaは、PC向けに8Kゲームを実現するモンスターRTX 3090グラフィックカードで4Kを超えようとしています。

- ゲーム機開発メーカーも、市場競争のハードルを上げるために新製品開発に注力しています。ソニーは10.28テラフロップスの性能を目指しているが、これはXboxシリーズXより15%近く低いです。また、冷却とアーキテクチャの根本的な違いもあり、ソニーはGPUとCPUの速度を可変にできるのに対し、マイクロソフトはより伝統的な固定速度にこだわり、4K性能ではソニーに非常に近いです。

- 様々なアプリケーションでARやVRの導入が進んでいることから、GPUの採用が進むと予想されます。グラフィックス技術の向上により、真のARやVRを実現し、魅力的なユーザー体験を生み出すことが可能になった。多くの企業は、主に人々がコンピューティングやゲームを体験する方法を再定義するためにVRソリューションを開発しており、各社はARやVRアプリケーション用のGPUシステムも開発しています。

北米が大きなシェアを占める見込み

北米地域のミレニアル世代におけるゲームの増加は、ここ数年で劇的かつ急速に進んでいます。ライムライト・ネットワークスによると、米国では30%以上のビデオゲーマーがゲーム配信サービスに料金を支払っており、35%以上が週に1回以上オンラインゲームをプレイしています。

- 大手テクノロジー開発企業は北米ゲーム市場のオンラインゲームに投資しており、この地域の市場成長をさらに後押ししています。今年1月、アメリカの多国籍企業であるマイクロソフト社は、ゲーム開発とインタラクティブ・エンターテインメント・コンテンツ出版で著名なアクティビジョン・ブリザード社を買収する計画を発表しました。この買収により、マイクロソフトのモバイル、PC、コンソール、クラウドにわたるゲーム事業の成長が加速する可能性があり、同社が提供するXboxの需要が高まることが期待されます。

- さらに、インテルは今年3月、ノートPCおよびデスクトップPC向けのグラフィックス・プロセッシング・ユニット(GPU)Arcシリーズを発表しました。ゲームやコンテンツ制作の強化向けに設計されたArc 3 GPUを搭載したノートパソコンは予約受付中で、高度で高性能なゲーム向けに設計されたArc 5 GPUとArc 7 GPUを搭載したノートパソコンは今年後半に登場する予定です。

- クラウドゲーミング企業は、通信事業者と協力してより優れたエンドツーエンドのネットワークを開発し、同地域での5G導入を促進することで利益を得ています。通信事業者がesportsプレーヤーの需要を満たすために上流の容量を増やす必要性はさらなる原動力であり、さまざまなベンダーがゲーミングニーズを満たすために協力しています。

同地域のゲーミングGPUメーカーもGPU製品の開発に注力しており、同地域の成長をさらに後押ししています。例えば、AMDは昨年7月にAMD Radeon RX 6600XTシリーズグラフィックス製品を発表し、AMD RDNAアーキテクチャのパワーを活用しながら、9.6テラフロップスのRDNA 2テクノロジーと8GBのGDDR6 RAMでより優れたパフォーマンスを提供しています。

ゲーミングGPU業界の概要

ゲーミングGPU市場は著しく統合されており、少数の世界的・地域的プレーヤーで構成されています。これらのプレーヤーは大きな市場シェアを占めており、顧客基盤を世界に拡大することに注力しています。これらのベンダーは、新ソリューション導入のための研究開発投資、戦略的提携、その他の有機的・無機的成長戦略に注力し、予測期間における競争力を獲得しています。

2022年11月、ASUSはTUF Gaming GeForce RTX 3060 TiおよびDual GeForce RTX 3060 Tiグラフィックスカードを更新し、より優れたパフォーマンスを実現するGDDR6Xメモリを搭載しました。GDDR6X RAMの追加により3060 Tiの能力が向上し、目の肥えたPC DIYビルダーが利用できる選択肢が広がった。ASUSは、GDDR6 VRAM 8GBを搭載した新しいGeForce RTX 3060を製造し、カスタマイズと組み立てのためにGPUの容量を増やしました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

- 市場促進要因

- 業界におけるゲーム機、拡張現実(AR)、仮想現実(VR)の需要増加

- より高いリフレッシュレートを持つ高度なディスプレイに対する需要の増加

- 市場抑制要因

- 高い初期投資

第5章 市場セグメンテーション

- タイプ別

- 専用グラフィックカード

- 統合グラフィックス・ソリューション

- その他の市場タイプ

- デバイス別

- モバイル機器

- PCおよびワークステーション

- ゲーム機

- 自動車

- その他のデバイス

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Intel Corporation

- Advanced Micro Devices Inc.

- Nvidia Corporation

- ASUSTEK Computer Inc

- GIGA-BYTE Technology Co., Ltd.

- Arm Limited

- Qualcomm Technologies Inc.

- Imagination Technologies Group

- EVGA Corporation

- SAPPHIRE Technology Limited

第7章 投資分析

第8章 市場の将来

The Gaming GPU Market size is estimated at USD 4.89 billion in 2025, and is expected to reach USD 20.98 billion by 2030, at a CAGR of 33.84% during the forecast period (2025-2030).

The rising gamification trend among millennials has led to the increasing adoption of a virtual world for video gamers. Gaming machines have also evolved from powerful location-based devices found in restaurants, arcades, and bars to in-home machines in the form of gaming consoles and then PCs. As Moore's Law drove down chip prices and increased performance, people bought more gaming machines for the home, which has a positive price elasticity effect at the expense of location-based gaming machines. As gaming machine sales have increased in the last few years, the demand for gaming GPUs has grown significantly.

Key Highlights

- The demand for high-end computing systems for graphics-intensive gaming applications has increased with the rising adoption of smartphones, tablets, PCs, and consoles for gaming purposes. The growing demand for specialized processors that can handle complex mathematical calculations related to the 2D and 3D graphics required for gaming drives the GPU market demand.

- Technological advancement in high-performing computing may also develop an opportunity for GPU vendors. For instance, in April this year, Nvidia stated that researchers discovered trends in Hubble data on April 25 using a supercomputer with NVIDIA GPUs. Also, high-performance computing is used with NVIDIA GPUs to increase the understanding of all planets and analyze their torrid atmospheres.

- Other drivers for the market include industry verticals such as automotive, manufacturing, real estate, and healthcare, with the rising usage of processors to support graphics applications and 3D content. For instance, in manufacturing and design applications in the automotive sector, CAD and simulation software uses GPUs to create realistic images and animations for critical applications.

- Gaming GPUs use advanced technologies and materials. One of the primary factors contributing to the high price of current GPUs is higher manufacturing expenses. Only the materials that producers can afford can be produced. Producers are thinking of maximizing their profits without sacrificing a product's quality or quantity due to rising manufacturing costs, which cause a rise in the selling price of the GPU. Due to this huge initial investment, consumers prefer to use something other than the latest gaming GPU in their devices, which is a challenge for market growth.

- Modern-day video game consoles and servers utilize many components, including gaming GPU circuits. COVID-19 threatened the average production of many of these components due to supply chain problems. However, semiconductor foundries started resuming production, which motivated manufacturers in the market. Demand in cloud computing, gaming, data center servers, automation, and AI technologies could help GPU manufacturers revive growth in the later part of the pandemic.

Gaming GPU Market Trends

Rising Demand for Gaming Consoles, Augmented Reality (AR), and Virtual Reality (VR) in the industry are Driving the Market

With the increasing adoption of esports and other types of online gaming, video games on consoles are rising and will show more growth opportunities in the coming years. As a result of this trend, connectivity and entertainment providers could target console gamers by offering console-related video services offerings, like fast broadband and live sports, and optimally monetizing the audience through OTT services. Video game developers could provide premium pricing for gaming subscription services, including access to esports events and original content.

- With the rising trend of cloud gaming, the GPU market has seen an upward trend in recent years. Blade, the French startup behind Shadow, is a cloud computing service for gamers that allows a player to access a gaming PC in a data centre for a monthly subscription fee. The company provides full Windows 11 features compared to other cloud gaming services. The company currently offers a single configuration for USD 35 per month with eight threads on an Intel Xeon 2620 processor, an Nvidia Quadro P5000 GPU, and an Nvidia GeForce GTX 1080, 12GB of RAM, and 256GB of storage.

- Further, major game developers are also focusing on developing console-based games with high graphic quality, contributing to the gaming segment's growth. Sony and Microsoft prioritize refresh rates up to 120 fps instead of trying to market the consoles as 8K capable, making the gaming experience seamless. Nvidia is trying to move beyond 4K with its monster RTX 3090 graphics card, which delivers 8K gaming for PCs.

- Console developers are also focusing on new product development to raise the bar for the competition in the market. Sony is aiming for 10.28 teraflops of performance, which is almost 15% less than the Xbox Series X. There are also some fundamental differences in cooling and architecture that allow Sony to offer variable GPU and CPU speeds, while Microsoft sticks to the more traditional fixed speeds and is very close to Sony in terms of 4K performance.

- The increasing incorporation of AR and VR in various applications is expected to drive the adoption of GPUs. Due to improvements in graphics technology, it is now possible to achieve true AR or VR and create a compelling user experience. Many companies are developing VR solutions primarily to redefine the way people experience computing and gaming, and the companies are also developing GPU systems for AR and VR applications.

North America is Expected to Hold a Significant Share

The rise in gaming among millennials in the North American region has been dramatic and swift in the past few years. In the United States, over 30% of video gamers pay for gaming subscription services, and more than 35% play online video games at least once a week, according to Limelight Networks.

- Major technology developers are investing in online gaming in the North American gaming market, further bolstering the region's market growth. In January of this year, Microsoft, an American MNC, announced plans to acquire Activision Blizzard Inc., a prominent player in game development and interactive entertainment content publishing. This acquisition may accelerate the growth of Microsoft's gaming business across mobile, PC, console, and cloud and is expected to drive demand for the company's Xbox offerings.

- Additionally, in March of this year, Intel launched the Arc series of Graphics Processing Units (GPU) for laptops and desktop PCs. Laptops with the Arc 3 GPU, designed for enhanced gaming and content production, are available for pre-order, while laptops with the Arc 5 and Arc 7 GPUs, designed for advanced and high-performance gaming, will come later in the current year.

- Cloud gaming companies benefit from collaborating with telecoms to develop better end-to-end networks and encourage 5G adoption in the region. The need for telecoms to increase their upstream capacity to meet the demands of esports players is a further driving force, and various vendors are collaborating to meet their gaming needs.

Gaming GPU players in the region also focus on developing GPU products, further driving the region's growth. For instance, in July last year, AMD introduced the AMD Radeon RX 6600XT series graphics products, harnessing the power of the AMD RDNA architecture while providing better performance with its 9.6 teraflops of RDNA 2 technology and 8 GB of GDDR6 RAM.

Gaming GPU Industry Overview

The gaming GPU market is significantly consolidated and consists of fewer global and regional players. These players account for a significant market share and focus on expanding their customer base globally. These vendors focus on research and development investment in introducing new solutions, strategic alliances, and other organic & inorganic growth strategies to earn a competitive edge over the forecast period.

In November 2022, ASUS updated its TUF Gaming GeForce RTX 3060 Ti and Dual GeForce RTX 3060 Ti graphics cards to include GDDR6X memory for better performance. The 3060 Ti's capabilities have been improved by the addition of GDDR6X RAM, which expands the options available to discerning PC DIY builders. ASUS has produced a new GeForce RTX 3060 with 8 GB of GDDR6 VRAM to increase the GPU's capacity for customization and assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Market Drivers

- 4.5.1 Rising Demand for Gaming Consoles, Augmented Reality (AR), and Virtual Reality (VR) in the industry

- 4.5.2 Increasing Demand for Advanced Displays with Higher Refresh Rates

- 4.6 Market Restraints

- 4.6.1 High Initial Investment

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Dedicated Graphic Cards

- 5.1.2 Integrated Graphics Solutions

- 5.1.3 Other Market Types

- 5.2 Device

- 5.2.1 Mobile Devices

- 5.2.2 PCs and Workstations

- 5.2.3 Gaming Consoles

- 5.2.4 Automotive

- 5.2.5 Other Devices

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Intel Corporation

- 6.1.2 Advanced Micro Devices Inc.

- 6.1.3 Nvidia Corporation

- 6.1.4 ASUSTEK Computer Inc

- 6.1.5 GIGA-BYTE Technology Co., Ltd.

- 6.1.6 Arm Limited

- 6.1.7 Qualcomm Technologies Inc.

- 6.1.8 Imagination Technologies Group

- 6.1.9 EVGA Corporation

- 6.1.10 SAPPHIRE Technology Limited