|

|

市場調査レポート

商品コード

1644321

中東の太陽光発電:市場シェア分析、産業動向、成長予測(2025年~2030年)Middle-East Solar Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東の太陽光発電:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

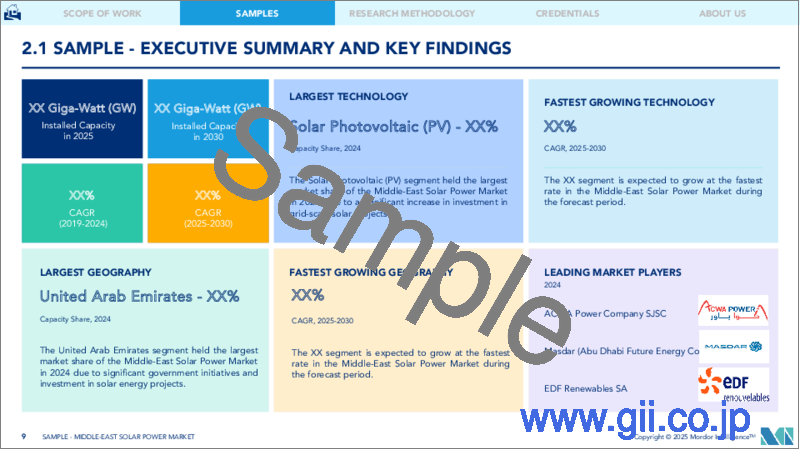

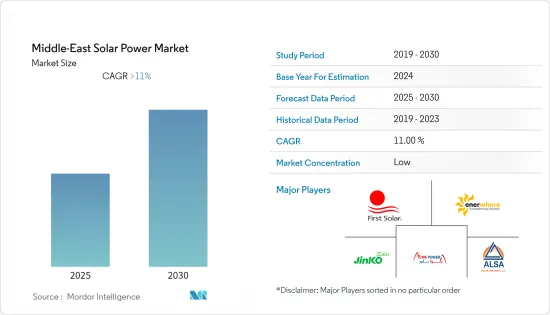

中東の太陽光発電市場は予測期間中に11%を超えるCAGRで推移すると予想されます。

2020年第1四半期にCOVID-19が発生し、中東の太陽光発電市場は中程度の影響を受けました。サウジアラビア、クウェート、カタールなど少数の国では、太陽電池モジュールの出荷が遅れたため、2020年の新規設置件数が大幅に減少しました。2021年には市場は回復しました。

主要ハイライト

- 政府の支援施策、再生可能エネルギー源を利用して電力需要を満たす取り組みの増加、化石燃料への依存度の低下といった要因が、市場を牽引する大きな要因になると予想されます。また、予測期間中には多くの野心的な太陽光発電プロジェクトが予定されており、今後数年間の太陽光発電市場の牽引役となることが期待されます。

- しかし、大規模太陽光発電プロジェクトの遅れや代替エネルギーへの注目の高まりといった要因が、市場の成長を妨げると予想されます。

- 今後予定されている太陽光発電プロジェクトは、この地域におけるハイブリッド電源ソリューションの利用とともに、近い将来、太陽光発電市場に計り知れない機会を生み出す可能性があります。

- サウジアラビアは、予測期間中に進行中と今後のプロジェクトが多数あるため、大きな需要が見込まれます。

中東の太陽光発電市場動向

太陽光発電(PV)プロジェクトが市場を牽引

- 太陽光発電(PV)セルは、太陽からの放射光やエネルギーを直流電力に変換する太陽光発電材料を含むセルのアレイです。太陽光発電(PV)ソーラーパネルは、2022年に設置された中東の太陽エネルギー全体の96.57%以上を占めています。

- 中東の太陽光発電設備容量は2022年に1,244万kWに増加し、2021年の923万9,000kWを上回りました。今後予定されているプロジェクトによって、予測期間中の容量はさらに増加すると予想されます。

- 2022年10月、Water Procurement Company(OPWP)とOman Powerは、オマーン北西部のイブリで2件目の大規模太陽光発電(PV)プロジェクトの入札を開始しました。新しいイブリIII太陽光独立発電プロジェクト(IPP)の太陽光発電容量は500MWです。この新しい施設は、2026年第4四半期に商業運転を開始する予定です。

- 2023年2月には、Mobarakeh Steel Companyがイスファハン州Kouhpayeh郡で容量600MWの太陽光発電所に融資する見込みです。このプロジェクトには5億米ドルの投資が見込まれています。第一段階では、2023年7月までに国内の送電網に100MW近くが追加される見込みです。

- サウジアラビアやアラブ首長国連邦のような国々では、複数のプロジェクトが建設中または入札段階にあり、予測期間中、太陽光発電の大幅な成長が中東地域の太陽光発電市場を牽引すると予想されます。

市場を独占するサウジアラビア

- サウジアラビアでは、2030年までに35の再生可能プロジェクト、5,870万kWの設置容量を設置するという目標を掲げた国家再生可能エネルギー計画が、太陽光発電の設置容量増加の要因となっています。

- 2022年のサウジアラビアの太陽光発電設備容量は440MWであり、今後数年で増加すると予想されます。また、2022年のサウジアラビアの太陽光発電設備容量は390MWに増加し、2020年の59MWと比較して増加しました。

- 2022年11月、ACWA PowerはWater and Electricity Holding Company(Badeel)と、メッカ州Al Shuaibahに世界最大の単一サイト太陽光発電所を開発する契約を締結しました。2,060MWの発電能力を持つこの太陽光発電所は、2025年末までに運転を開始する予定です。

- さらに、産業鉱物資源省によると、サウジアラビアは2022年3月、グリーンエネルギーへの取り組みを支援し、原油への依存を減らすための新たな計画を打ち出しました。さらに同省は、再生可能エネルギーを発電する事業者に減税などの特典を提供する予定です。

- 従って、前述の事実に基づき、サウジアラビアは予測期間中、中東地域の太陽光発電市場で大きな需要を目の当たりにすることになると予想されます。

中東の太陽光発電産業概要

中東の太陽光発電市場は適度にセグメント化されています。この市場の主要企業には、JinkoSolar Holding、First Solar Inc.、Enerwhere Sustainable Energy DMCC、ACWA POWER BARKA SAOG、Alsa Solar Systems LLCなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 設置容量と2028年までの予測(単位:GW)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

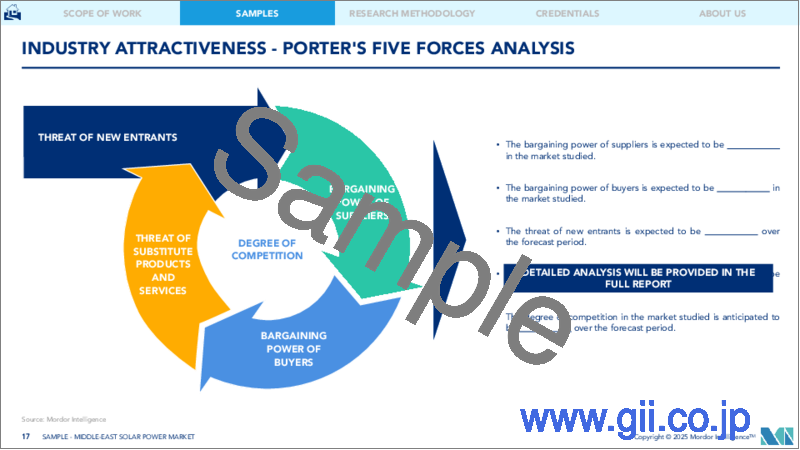

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術セグメント

- 太陽光発電(PV)

- 集光型太陽光発電(CSP)

- 地域

- サウジアラビア

- アラブ首長国連邦

- オマーン

- その他の中東地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- JinkoSolar Holding Co. Ltd.

- First Solar Inc

- Enerwhere Sustainable Energy DMCC

- ACWA POWER BARKA SAOG

- Alsa Solar Systems LLC

- Enviromena Power Systems

- Trina Solar Ltd.

- JA SOLAR Co. Ltd.

- Sungrow Power Supply Co. Ltd.

- Hitachi Energy Ltd.

- Canadian Solar Inc.

第7章 市場機会と今後の動向

The Middle-East Solar Power Market is expected to register a CAGR of greater than 11% during the forecast period.

With the COVID-19 outbreak in Q1 2020, the Middle Eastern solar power market was moderately impacted. Few countries like Saudi Arabia, Kuwait, and Qatar had significantly less number of new installations in 2020 due to delays in the shipping of solar modules. The market rebounded in 2021.

Key Highlights

- Factors such as supportive government policies and increasing efforts to meet power demand using renewable energy sources, and decreased dependency on fossils are expected to be significant contributors to driving the market. Besides, many ambitious photovoltaic projects are lined up in the forecast period and are expected to drive the solar market in the coming years.

- However, factors such as delays in large-scale solar projects and increasing focus on alternative energy sources are expected to hinder the market's growth.

- The upcoming solar power projects, along with the use of hybrid power solutions in this region, can create immense opportunities for the solar power market in the near future.

- Saudi Arabia is expected to witness significant demand due to the number of ongoing and upcoming projects over the forecast period.

Middle East Solar Power Market Trends

Solar Photovoltaic (PV) Projects to Drive the Market

- Photovoltaic (PV) cells are arrays of cells containing a solar photovoltaic material that converts solar radiation or energy from the sun into direct current electricity. Photovoltaic (PV) solar panels held a share of more than 96.57% of the total Middle Eastern solar energy installed in 2022.

- The solar PV installed capacity of the Middle East grew to 12.440 GW in 2022, which is higher compared to the 9.239 GW installed in 2021. Upcoming projects are expected to increase capacity during the forecast period even further.

- In October 2022, the Water Procurement Company (OPWP) and Oman Power initiated bidding for the second large-scale solar photovoltaic (PV) project at Ibri in northwest Oman. The new Ibri III Solar Independent Power Project (IPP) has a solar PV capacity of 500 MW. The new facility is anticipated to begin commercial operations in the fourth quarter of 2026.

- In February 2023, Mobarakeh Steel Company was anticipated to finance the solar photovoltaic power plant in Kouhpayeh County, Isfahan Province, with a capacity of 600 MW. The project is expected to receive an investment of USD 500 million. The first phase will likely add nearly 100 MW to the nation's power grid by July 2023.

- With several projects under construction or in the tender phase in countries like Saudi Arabia and the United Arab Emirates, considerable growth in solar PV is expected to drive the solar power market in the Middle Eastern region over the forecast period.

Saudi Arabia to Dominate the Market

- In Saudi Arabia, the solar energy installed capacity growth can be attributed to the National Renewable Energy Program, which had a target of installing 35 renewable projects with 58.7 GW of installed capacity by 2030.

- The installed solar power capacity for Saudi Arabia in 2022 was 440 MW, which is expected to increase in the coming years. Also, the solar PV installed capacity for Saudi Arabia increased to 390 MW in 2022, which was higher compared to 59 MW in 2020.

- In November 2022, ACWA Power signed an agreement with Water and Electricity Holding Company (Badeel) to develop the world's largest single-site solar-power plant in Al Shuaibah, Mecca province. With a 2,060 MW generation capability, the solar power plant is anticipated to begin operations by the end of 2025.

- Moreover, in March 2022, according to the Ministry of Industry and Mineral Resources, Saudi Arabia launched a new plan to support green energy initiatives and reduce its reliance on crude oil. Additionally, the ministry would provide tax breaks and other benefits to businesses that generate renewable energy.

- Therefore, based on the aforementioned facts, Saudi Arabia is expected to witness significant demand for the solar power market in the Middle Eastern region over the forecast period.

Middle East Solar Power Industry Overview

The Middle Eastern solar power market is moderately fragmented. Some of the key players in this market include (not in particular order) JinkoSolar Holding Co. Ltd, First Solar Inc., Enerwhere Sustainable Energy DMCC, ACWA POWER BARKA SAOG, and Alsa Solar Systems LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast in GW, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Concentrated Solar Power (CSP)

- 5.2 Geography

- 5.2.1 Saudi Arabia

- 5.2.2 United Arab Emirates

- 5.2.3 Oman

- 5.2.4 Rest of the Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 JinkoSolar Holding Co. Ltd.

- 6.3.2 First Solar Inc

- 6.3.3 Enerwhere Sustainable Energy DMCC

- 6.3.4 ACWA POWER BARKA SAOG

- 6.3.5 Alsa Solar Systems LLC

- 6.3.6 Enviromena Power Systems

- 6.3.7 Trina Solar Ltd.

- 6.3.8 JA SOLAR Co. Ltd.

- 6.3.9 Sungrow Power Supply Co. Ltd.

- 6.3.10 Hitachi Energy Ltd.

- 6.3.11 Canadian Solar Inc.