|

市場調査レポート

商品コード

1644320

インドの電池:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの電池:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

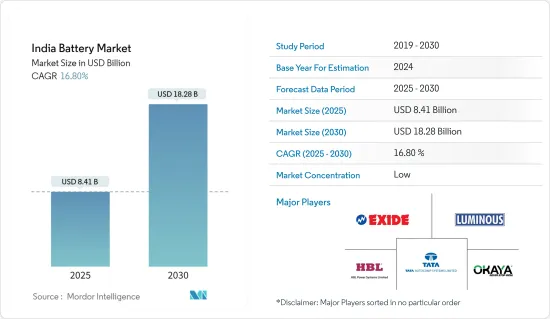

インドの電池市場規模は2025年に84億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.8%で、2030年には182億8,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、電気自動車や様々な用途の電池エネルギー貯蔵システムといった新しくエキサイティングな市場の出現や、電気自動車における自動車用電池の利用拡大といった要因が、予測期間中のインド電池市場を牽引すると考えられます。

- 一方、リチウムイオンの国内製造施設がないことが、予測期間中のインド電池市場の成長を妨げる可能性が高いです。

- しかし、インドにおけるリチウムイオン電池の国内製造計画は、予測期間中、インドの電池市場に有利な成長機会をもたらす可能性が高いです。

インドの電池市場動向

自動車セグメントが著しい成長を遂げる

- 政府の施策レベルの支援が製造業を後押ししているため、インドは今後数年間、電池企業にとって主要な投資ホットスポットになると予想されます。

- 中産階級と若年人口の増加により、二輪車セグメントが自動車市場を独占しています。組織企業は保証付きのブランド電池を販売しているが、非組織企業は保証やアフターサービスを提供せず、リサイクル電池を販売し、ブランド電池より30~35%安く製品を提供しています。インドの自動車用交換電池市場は鉛蓄電池市場をリードしています。

- 2022~2023年にかけて、同国最大の自動車メーカーであるMaruti Suzuki Indiaの卸売台数は最大で、2021~2022年の165万2,653台から19%増の196万6,164台となりました。国内出荷台数は、前年度の141万4,277台から2022~2023年度には170万6,831台と21%増加しました。

- Motor Vehicle Manufacturers(OICA)によると、インドの自動車生産台数は2109年度から2023年度まで着実に増加し、右肩上がりのグラフを示しています。自動車の販売台数はすべて電池の販売台数に比例することを考えると、これは市場関係者にとって将来の力強い成長を約束するものです。

- 2023年2月、世界トップクラスのVRLAとリン酸リチウムイオン電池製造会社であるOkaya Power Pvt.Ltdは、インド市場向けに新型電動二輪車E-Scooter Faast F3の発売を発表しました。新型EスクーターFaast F3は125kmの航続が可能で、防水・防塵仕様の3.53kWhリチウムイオンLFPデュアル電池を搭載し、電池寿命を延ばすスイッチング技術を採用しています。新型リチウム電池は4~5時間で充電できます。

- 人口の増加と利用しやすい融資制度により、自動車部門は予測期間中に大きく成長すると予想されます。電気自動車(EV)の販売は、このセグメントを下支えすると予想されます。

- 以上のような要因により、同国では自動車セグメントが大きな勢いを得ることが予想され、ひいては予測期間中の電池市場の成長にも貢献するものと考えられます。

電気自動車(EV)需要の増加が市場を牽引

- 電気自動車(EV)は、国連のサステイナブル開発目標の達成に中心的な役割を果たすと期待されています。インドでは、クリーンなエネルギー源に対する需要の増加に伴い、EVの採用が大きく伸びるとみられます。政府は、インドにおける二輪車、三輪車、商用車の電動化を主要原動力として、2030年までに電気自動車普及率30%という目標を達成する計画を立てています。

- インドでは、化石燃料を動力源とする乗用車が年間300万台以上販売されており、Mahindra & Mahindra Ltd、Tata Motors Ltd、Ashok Leyland Ltdなど数社の自動車メーカーが国内でEVを製造しています。Hyundai Motor Co.やSuzuki Motor Corp.などの海外企業も、2030年までに環境対応車を保有台数の約3分の1にすることを政府が計画していることから、この新セグメントに参入しています。

- 同市場は、主に旅客運送業者が使用する電気自動車が支配的となると考えられます。Eリキシャや個人所有の小型三輪タクシー用の電池需要は、予測期間中に20%以上の成長が見込まれます。

- インド道路交通高速道路省(MORTH)の2023年12月のプレスリリースによると、2023年のEV登録台数は2022年比で13万4,434台増加しました。2年間の総販売台数は150万4,012台となりました。インドの電池とプラグインハイブリッド車市場の活況を考慮すると、これはインドの電池市場参入企業に強い将来性をもたらすと考えられます。

- 2023年2月、RenaultとNissanは、生産と研究開発活動の拡大、電気自動車の採用、カーボンニュートラル製造への移行を含む、インドにおける新たな長期ビジョンを明らかにしました。両社はチェンナイを拠点に、2台の完全電気自動車を含む6台の新型生産車を共同開発します。両社は新プロジェクトを支援するために約6億米ドルを投資する予定です。

- 2023年6月、Tata Groupの子会社であるAgratas Energy Storage Solutions Private Limitedは、グジャラート州政府とインド初のリチウムイオン電池のギガファクトリーを設立する契約を締結しました。同社は当初、20ギガワット(GW)のユニットに15億7,000万米ドルを投資します。

- このため、電気自動車の普及拡大が予測期間中のインドの電池市場を牽引するとみられます。

インドの電池産業概要

インドの電池市場はセグメント化されています。市場の主要企業(順不同)には、Exide Industries LtdとLuminous Power Technologies Pvt.Ltd、HBL Power Systems Ltd、TATA AutoComp GY Batteries Pvt.Ltd、Okaya Power Pvt.Ltdなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車とさまざまな用途の蓄電池システムという、新しくエキサイティングな市場の出現

- 電気自動車における自動車用電池の利用拡大

- 抑制要因

- リチウムイオン国内製造施設の不在

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- 技術

- リチウムイオン電池

- 鉛蓄電池

- その他

- 用途

- SLI電池

- 産業用電池(動力用、据置型(電気通信、UPS、エネルギー貯蔵システム(ESS)など))

- ポータブル(民生用電子機器製品など)

- 自動車用電池(HEV、PHEV、EV)

- その他

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Exide Industries Ltd.

- Luminous Power Technologies Pvt. Ltd

- HBL Power Systems Ltd

- TATA AutoComp GY Batteries Pvt. Ltd

- Okaya Power Pvt. Ltd

- Amara Raja Batteries Ltd

- Su-Kam Power Systems Ltd

- Base Corporation Ltd

- Southern Batteries Pvt. Ltd

- Evolute Solutions Pvt. Ltd

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- インドにおけるリチウムイオン電池の現地生産計画

目次

Product Code: 71016

The India Battery Market size is estimated at USD 8.41 billion in 2025, and is expected to reach USD 18.28 billion by 2030, at a CAGR of 16.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the emergence of new and exciting markets, i.e., electric vehicles and battery energy storage systems for different applications and the growing usage of automotive batteries in electric vehicles, will likely drive the Indian battery market during the forecast period.

- On the other hand, the absence of lithium-ion domestic manufacturing facilities will likely hinder the growth of the Indian battery market during the forecast period.

- However, plans for local manufacturing of lithium-ion batteries in India will likely create lucrative growth opportunities for the Indian battery market during the forecast period.

India Battery Market Trends

The Automotive Segment to Witness Significant Growth

- India is expected to be a major investment hotspot for battery companies in the coming years because government policy-level support encourages the manufacturing sector.

- The two-wheeler segment dominates the automotive market owing to a growing middle class and a young population. Organized companies sell branded batteries with warranties, while unorganized companies provide no warranty or after-sales, sell recycled batteries, and offer products at a 30-35% discount to branded ones. The Indian automotive replacement battery market is leading the lead-acid battery market.

- During 2022-2023, Maruti Suzuki India, the country's largest automaker, had its greatest wholesales, up 19% from 165,265,3 units in 2021-2022 to 196,616,4 units. Domestic shipments climbed by 21% during 2022-2023 to 170,683,1 units from 141,427,7 units the previous fiscal year.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), automotive production in India increased steadily from FY 2109 to FY 2023, showing an upward graph. Considering that every automotive vehicle sale is directly proportional to battery sales, this promises strong future growth for the market players.

- In February 2023, Okaya Power Pvt. Ltd, a world-class VRLA and lithium-ion phosphate battery manufacturing company, announced the launching of a new electric two-wheeler, E-Scooter Faast F3, for the Indian market. The new E-Scooter Faast F3 is capable of providing a range of 125 km and is equipped with waterproof and dust-resistant 3.53 kWh lithium-ion LFP dual batteries with switchable technology to extend battery life. The new lithium battery can be charged in 4 to 5 hours.

- With an increasing population and accessible financing facilities, the automobile sector is expected to grow significantly during the forecast period. Electric vehicle (EV) sales are expected to support the segment.

- The factors above are expected to help the automotive segment gain significant momentum in the country, which, in turn, will help the battery market grow during the forecast period.

Increasing Demand for Electric Vehicles (EVs) to Drive the Market

- Electric vehicles (EVs) are expected to play a central role in achieving the UN Sustainable Development Goals. In India, the adoption of EVs is likely to grow significantly with the increasing demand for clean energy sources. The government has plans to achieve a target of 30% electric vehicle adoption by 2030, powered primarily by the electrification of two-wheeler, three-wheeler, and commercial vehicles in India.

- In India, more than 3 million fossil fuel-powered passenger vehicles are sold annually, and a few automakers, including Mahindra & Mahindra Ltd, Tata Motors Ltd, and Ashok Leyland Ltd, are making EVs domestically. Overseas companies such as Hyundai Motor Co. and Suzuki Motor Corp. are also entering the new segment as the government plans to have green vehicles comprise about a third of its fleet by 2030.

- The market will likely be dominated by electric vehicles mainly used by passenger carriers. The demand for batteries for e-rickshaws and small privately owned three-wheeler taxis is expected to grow by more than 20% during the forecast period.

- According to a December 2023 press release from the Indian Ministry of Road Transport and Highways (MORTH), the registration of EVs in 2023 increased by 1,34,434 units compared to 2022. The total sales in two years stood at 15,04,012 units. Considering India's battery and plug-in hybrid vehicle market boom, this will offer strong future potential to the Indian battery market players.

- In February 2023, Renault and Nissan revealed a new long-term vision for India, including increased production and R&D activities, the introduction of electric vehicles, and a shift to carbon-neutral manufacturing. From their base in Chennai, the firms will collaborate on six new production vehicles, including two fully electric cars. They are expected to invest approximately USD 600 million to support the new projects.

- In June 2023, Tata Group subsidiary Agratas Energy Storage Solutions Private Limited signed an agreement with the Gujarat government to establish India's first gigafactory for lithium-ion batteries. The company will initially invest USD 1.57 billion in the 20 gigawatts (GW) unit.

- Therefore, the increase in the adoption of electric vehicles is expected to drive the battery market in India during the forecast period.

India Battery Industry Overview

The Indian battery market is fragmented. Some of the major players in the market (in no particular order) include Exide Industries Ltd and Luminous Power Technologies Pvt. Ltd, HBL Power Systems Ltd, TATA AutoComp GY Batteries Pvt. Ltd, and Okaya Power Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Emergence of New and Exciting Markets, i.e., Electric Vehicles and Battery Energy Storage Systems for Different Applications

- 4.5.1.2 The Growing Usage of Automotive Batteries in Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 The Absence of Lithium-Ion Domestic Manufacturing Facilities

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-acid Battery

- 5.1.3 Other Technologies

- 5.2 Application

- 5.2.1 SLI Batteries

- 5.2.2 Industrial Batteries (Motive, Stationary (Telecom, UPS, Energy Storage Systems (ESS)), Etc.)

- 5.2.3 Portable (Consumer Electronics, Etc.)

- 5.2.4 Automotive Batteries (HEV, PHEV, and EV)

- 5.2.5 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Exide Industries Ltd.

- 6.3.2 Luminous Power Technologies Pvt. Ltd

- 6.3.3 HBL Power Systems Ltd

- 6.3.4 TATA AutoComp GY Batteries Pvt. Ltd

- 6.3.5 Okaya Power Pvt. Ltd

- 6.3.6 Amara Raja Batteries Ltd

- 6.3.7 Su-Kam Power Systems Ltd

- 6.3.8 Base Corporation Ltd

- 6.3.9 Southern Batteries Pvt. Ltd

- 6.3.10 Evolute Solutions Pvt. Ltd

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Plans for Local Manufacturing of lithium-Ion Batteries in India