|

市場調査レポート

商品コード

1643209

欧州の太陽光発電(PV)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Europe Solar Photovoltaic (PV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の太陽光発電(PV)-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

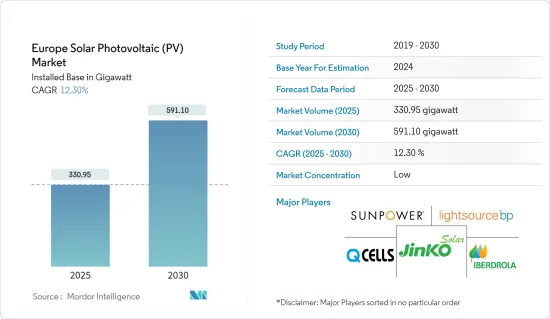

欧州の太陽光発電(PV)市場規模(設置ベース)は、2025年の330.95ギガワットから2030年には591.10ギガワットに成長し、予測期間(2025~2030年)のCAGRは12.3%と予測されます。

主要ハイライト

- 中期的には、地域全体の電力需要の増加、太陽エネルギープロジェクトへの投資の増加、再生可能エネルギーによる電力生産が市場の成長を牽引しています。

- その一方で、天然ガス発電が重視されるようになり、発電用の天然ガスが低価格で入手できるようになったことが、欧州の市場成長を抑制しています。

- しかし、太陽光発電の導入を促進するために実施されている野心的な太陽エネルギー目標は、予測期間中に市場に有利な機会を生み出すと期待されています。

- 太陽光発電の設置容量が最大のドイツは、予測期間中、欧州の太陽光発電(PV)市場を独占すると予想されます。

欧州の太陽光発電(PV)市場動向

大幅な市場成長が見込まれる屋上セグメント

- 欧州では予測期間中、屋上市場が大きく成長すると予測されています。欧州の屋根のほとんどは未使用であるため、欧州の屋上設置は大きな可能性を秘めています。欧州のいくつかの国では、報酬水準を評価するための施策の修正に取り組んでいます。

- ノルウェー、バルト地域、アイルランドなどは、屋上太陽光発電の設置に有利な地理的条件を備えています。このため、予測期間中、欧州では屋上太陽光発電の設置が増加すると予想されます。また、いくつかの国では、住宅所有者が電気代削減のために屋上PVモジュールの設置に積極的です。国際再生可能エネルギー機関(IRENA)によると、2023年の欧州の太陽光発電導入量は285.80GWに達し、前年比成長率は23.45%です。

- 2023年12月、欧州議会と欧州理事会は、建物のエネルギー性能を刺激し、新しい建物に太陽光発電への対応を義務付けることを目的とした、強化された「建物のエネルギー性能指令(EPBD)」に関する中間合意に達しました。EPBDはまた、EU加盟国に対し、新しい建物が屋上太陽光発電や熱利用設備の設置に適していることを保証するよう義務付けています。既存の公共建築物や非住宅建築物には、2027年から太陽光発電の設置が義務付けられます。

- 数カ国の政府は、同地域内での屋上太陽光発電アレイの展開を拡大するための支援施策を採用しています。例えば、欧州政府は2023年3月、2028年までにすべての新築建物に、また2032年までに住宅を改築する際に屋上太陽光発電システムの設置を義務付ける改正事業所エネルギー性能指令を採択しました。

- 2023年、ドイツは記録的な14GWの太陽光発電容量を導入し、マイルストーンを達成しました。この急増は、ドイツ太陽電池協会(BSW)が報告したように、前年と比較して容量が85%増加したことを反映しています。容量の急増は、主に住宅需要、特に屋根上太陽光発電システムによるものでした。BSWは大幅な増加を指摘しており、2023年第1四半期に稼働した太陽光発電システムは15万9,000件で、2022年同時期の2倍以上となっています。

- 以上のことから、予測期間中、欧州の太陽光発電市場では屋上設置型太陽光発電が大きく成長すると予想されます。

ドイツが市場を独占する見込み

- ドイツは、太陽光発電を含む再生可能エネルギー生産において、欧州で最も有利な市場の一つです。同国は二酸化炭素排出量削減を目標に掲げているため、太陽光発電の設置が大きく発展しており、今後も太陽光発電の設置が伸びると見られています。

- 同国の太陽光発電設備容量は、近年大幅な伸びを示しています。2023年の太陽光発電設備容量は約81.73GWで、2022年の67.47GWと比べ、CAGRは21%を超えており、太陽光発電システムの普及が進んでいることを示しています。

- 同国は、都市部での太陽電池モジュールの設置を促進するため、いくつかの規制や奨励制度を実施しています。2023年6月、ドイツ経済省は同国の太陽光発電産業再建のための新たな政府資金拠出を発表しました。経済省は近く新たな資金調達手段を提示する予定で、将来的にはEUの新たな補助金枠組みに沿った入札を準備しています。

- ドイツのいくつかの都市では、新築建物への太陽光発電設置が義務付けられており、ドイツ国内の市場拡大に貢献しています。2022年12月、EUはドイツの再生可能エネルギー計画280億ユーロを承認しました。この施策は、太陽光発電を含む自然エネルギーの利用を急速に拡大することを目的としています。これは、2030年までに電力の80%を再生可能エネルギーで生産するというドイツの目標を実現するためのものです。

- したがって、上記の点から、予測期間中はドイツの太陽光発電が欧州の太陽光発電市場を独占することになります。

欧州の太陽光発電産業概要

欧州の太陽光発電市場はセグメント化されています。同市場の主要企業(順不同)には、Hanwha Q CELLS Technology、Iberdrola SA、SunPower Corporation、JinkoSolar Holding、Lightsource BP Renewable Energy Investments Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの設置容量と予測(単位:GW)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 地域全体の電力需要の増加

- 太陽エネルギープロジェクトへの投資の増加

- 抑制要因

- 天然ガス発電重視の高まり

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- タイプ

- 薄膜

- 結晶シリコン

- エンドユーザー

- 住宅用

- 商業と産業(中小企業を含む)

- 展開

- 地上設置型

- 屋上設置型

- 2029年までの市場規模・需要予測(地域別)

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- ベルギー

- 北欧

- トルコ

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- First Solar Inc.

- Electricite de France S.A.(EDF)

- Hanwha Q CELLS Technology Co. Ltd

- Iberdrola SA

- JinkoSolar Holding Co. Ltd

- SunPower Corporation

- Lightsource bp Renewable Energy Investments Limited

- Enel SpA

- Centrotherm International AG

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 野心的な太陽エネルギー目標

The Europe Solar Photovoltaic Market size in terms of installed base is expected to grow from 330.95 gigawatt in 2025 to 591.10 gigawatt by 2030, at a CAGR of 12.3% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising demand for electricity across the region, increasing investments in solar energy projects, and producing most of the electricity from renewable sources have driven the growth of the market.

- On the other hand, the rising emphasis on natural gas power generation and the availability of natural gas at lower prices for power generation restrain the market growth in the European region.

- However, the ambitious solar energy targets implemented to boost solar PV installation are expected to create lucrative opportunities for the market during the forecast period.

- Germany, with the largest installed capacity of solar photovoltaics, is expected to dominate the European solar photovoltaics (PV) market during the forecast period.

Europe Solar Photovoltaic (PV) Market Trends

The Rooftop Segment Anticipated to Witness Significant Market Growth

- The rooftop segment is estimated to witness significant growth during the forecast period in Europe. The European region's rooftop installation has lots of potential as most of Europe's roof surfaces are unused. Several countries in Europe are working on modifying their policies to assess remuneration levels.

- Norway, the Baltic region, Ireland, and others have geographical conditions favorable to rooftop PV installation. This is expected to increase rooftop solar PV installation in Europe during the forecast period. Also, in several countries, homeowners are willing to install rooftop PV modules to reduce their electricity bills. According to the International Renewable Energy Agency (IRENA), in 2023, Europe's solar PV installed reached 285.80 GW, with a growth rate of 23.45% over the previous year.

- In December 2023, the European Parliament and the European Council reached an interim agreement on the strengthened Energy Performance of Buildings Directive (EPBD), aspiring to stimulate the energy performance of buildings and requiring new buildings to be solar-ready. The EPBD also mandates that EU member states ensure new buildings are fit to host rooftop solar PV or thermal installations. Existing public and non-residential building solar will require to be installed commencing from 2027.

- Governments in several countries have adopted supportive policies to increase the deployment of rooftop PV arrays within the region. For instance, in March 2023, the European government adopted the revised Energy Performance of Business Directive mandating rooftop solar systems for all new buildings by 2028 and renovating residential buildings by 2032.

- In 2023, Germany achieved a milestone by installing a record 14GW of solar energy capacity, facilitated by adding over a million new solar power systems, a significant portion of which were residential rooftop installations. This surge reflects an impressive 85% increase in capacity compared to the previous year, as the German Solar Association (BSW) reported. The surge in capacity was primarily fueled by residential demand, particularly for rooftop solar power systems. The BSW noted a substantial increase, with 159,000 PV systems operational in the first quarter of 2023, more than double the number recorded during the same period in 2022.

- Therefore, from the above points, the rooftop solar photovoltaic segment is anticipated to witness significant growth in the European solar photovoltaic market during the forecast period.

Germany Expected to Dominate the Market

- Germany is one of the most lucrative markets in the European region for renewable energy production, including solar. The country has experienced significant developments in solar PV installation due to its target of reducing carbon emissions, and it is likely to continue witnessing growth in solar installation.

- The country's solar PV installed capacity has witnessed massive growth in recent years. In 2023, the installed solar PV was around 81.73 GW compared to 67.47 GW in 2022, registering a CAGR of over 21%, signifying the country's growing penetration of solar PV systems.

- The country has implemented several regulations and incentive schemes to promote the installation of solar modules in cities. In June 2023, Germany's economy ministry announced new government funding to rebuild the country's solar industry. The economy ministry is expected to present the new funding instrument soon and is preparing a tender in line with a new EU subsidy framework in the future.

- The mandates for solar photovoltaic installation on new buildings in a few German cities have helped expand the market in Germany. In December 2022, the European Union approved a EUR 28 billion German renewable energy scheme. The policy aims to increase the use of renewables, including solar power rapidly. It is designed to deliver Germany's target of producing 80% of its electricity from renewable sources by 2030.

- Therefore, based on the above points, solar photovoltaic in Germany will dominate the European solar photovoltaic market during the forecast period.

Europe Solar Photovoltaic (PV) Industry Overview

The European solar photovoltaic (PV) market is fragmented. Some of the major companies in the market (in no particular order) include Hanwha Q CELLS Technology Co. Ltd, Iberdrola SA, SunPower Corporation, JinkoSolar Holding Co. Ltd, and Lightsource BP Renewable Energy Investments Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Market Definiton

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, in GW, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Rising Demand for Electricity across the Region

- 4.5.1.2 Increasing Investments on Solar Energy Projects

- 4.5.2 Restraints

- 4.5.2.1 Rising Emphasis on Natural Gas Power Generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thin Film

- 5.1.2 Crystalline Silicon

- 5.2 End User

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial (including SMEs)

- 5.3 Deployment

- 5.3.1 Ground-Mounted

- 5.3.2 Rooftop Solar

- 5.4 Geography Regional Market Analysis {Market Size and Demand Forecast till 2029 (for regions only)}

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Belgium

- 5.4.8 Nordic

- 5.4.9 Turkey

- 5.4.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 First Solar Inc.

- 6.3.2 Electricite de France S.A. (EDF)

- 6.3.3 Hanwha Q CELLS Technology Co. Ltd

- 6.3.4 Iberdrola SA

- 6.3.5 JinkoSolar Holding Co. Ltd

- 6.3.6 SunPower Corporation

- 6.3.7 Lightsource bp Renewable Energy Investments Limited

- 6.3.8 Enel SpA

- 6.3.9 Centrotherm International AG

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Solar Energy Targets