欧州のDPaaS(Data Protection-as-a-Service)市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Europe Data Protection-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643205

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

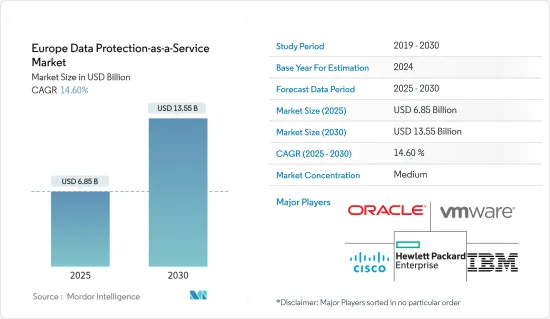

欧州のDPaaS(Data Protection-as-a-Service)市場規模は2025年に68億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.6%で、2030年には135億5,000万米ドルに達すると予測されます。

欧州のDPaaS(Data Protection-as-a-Service)市場を牽引している要因は、GDPRなどの厳しい規制と相まってサードパーティのリスク管理への注目が高まり、データ保護ソリューションの導入が促進されていることです。また、欧州を拠点とする市場ベンダーの多くは、競争優位性を獲得するためにさまざまな産業に参入し、製品提供を革新しており、市場の成長にさらに貢献しています。

主要ハイライト

- 欧州では、一般データ保護規則(GDPR)が個人データや情報の収集に関するガイドラインを定めた主要な法的枠組みとなっています。収集、アクセス、保管される個人情報に関連するGDPRの中核的な考え方の遵守は、企業にとって難しい課題です。そのため、データ保護サービスは、企業のガバナンスとコンプライアンスを確保しながら、ビジネスセルフサービス分析を可能にします。

- この地域のエンドユーザー産業では、クラウドへの移行も非常に進んでいます。より多くのモバイルデータが生成され、より多くのデータソースが追加される可能性があります。そのため、この地域ではより先進的データ準備ソリューションが必要とされています。

- 欧州のいくつかの国ではデータ漏洩やサイバー攻撃の件数が増加しているにもかかわらず、この地域の顧客や組織は第三者企業とのデータ共有に消極的です。さらに、2023年10月には、ドイツ最大の電力供給会社の1つであるイーオンのトップが、サイバー攻撃から重要な資産を保護するための十分な対策が講じられていないと述べ、その結果、欧州全域の当局に対してさらなる対策を講じるよう要請しました。欧州諸国ではこうした脅威の増加に伴い、データ保護サービスの導入が進んでいます。

- COVID-19パンデミックの発生率の増加に伴い、公的機関と医療専門家の間でデータ交換を行うための安全でシンプルな手段の必要性が、ウイルスとの闘いにおいて以前よりもはるかに透明化されました。しかし、欧州連合(EU)におけるブレグジットの影響により、市場は不確実性に直面しています。Googleは、英国の顧客のアカウントをEUのプライバシー規制当局の管理下から外し、米国の管轄下に置く計画です。英国の欧州連合(EU)離脱に伴うこの移行により、数百万人の顧客の機密情報は保護されなくなり、英国の法律がより届きやすい範囲に置かれることになります。

欧州のDPaaS(Data Protection-as-a-Service)市場動向

BFSI産業は予測期間を通じて大きな成長が見込まれる

- 銀行・金融サービス産業の参加者はデジタル化が進んでいるため、セキュリティ侵害から企業データを保護することが不可欠です。デジタル基盤技術に支えられたハイブリッドクラウドインフラを備え、自動運転オペレーションによって近代化された銀行のデータセンターは、顧客体験の大幅な向上を保証します。その一方で、近代化はさまざまなセキュリティの抜け穴を生み出し、データ漏洩やその他の情報損失を招いた。

- Eurobitsのような技術サービスプロバイダーは、銀行が連携して、顧客が複数の銀行プロバイダーで迅速に決済や銀行口座の管理を行えるように支援します。同社は、セキュアなバンキングアプリケーションをコンテナ化するため、2つのデータセンターでIBMのクラウド技術上のVMware vSphereに移行しました。

- 欧州の銀行の多くは、米国よりも高いセキュリティ基準を持つクラウドコンピューティング・プロバイダーを探しています。欧州の銀行は、米国の3大クラウドプロバイダー、Microsoft、Amazon、Googleを選んでいます。

- フランスとドイツの政府関係者は、地域の技術・プロバイダー企業によって運営される競合大陸クラウドサービスを創設するため、技術、通信、金融の大手企業と協議を進めています。しかし、ドイツのコメルツ銀行(Commerzbank AG)のような銀行は、データ関連規制の柔軟性を高めるため、米国のプロバイダーに共同でクラウド要件を提示するために手を組んでいます。

- この市場で事業を展開する企業は、効率的に問題に取り組むため、革新的なソリューションに継続的に投資しています。例えば、サイバーセキュリティソリューションの大手プロバイダーであるフォーティネットは、FortiGate-VMの発売を発表し、VMware NSX-Tのネイティブサポートを拡大して東西トラフィックに先進的セキュリティを記載しています。

英国セグメントが大きなシェアを占める見込み

- 英国市場では、ビッグデータ、ブロックチェーン、その他の取り組みに対する嗜好が高まっており、市場の成長に寄与しています。

- SAS Instituteによると、英国のリテールバンキング組織はビッグデータ導入において80%という驚異的な伸びを示し、市場の成長にプラスに寄与すると予想されています。

- ファッション小売業のH&Mは最近、実店舗でのマーチャンダイジングミックスを調整するためにビッグデータの利用を開始しました。収益向上のため、このファッション小売業者はアルゴリズムとさまざまな顧客データソースを利用し、レシート、返品、ポイントカードのデータから洞察を得ています。

- 英国では、ブロックチェーンユーザーはフランスで開発されたガイダンスを参考にして、データ保護法を遵守することができます。英国のデータ保護当局は、暗号通貨マイニングや関連技術に関連する重要な法律を無視してきました。フランスのデータ保護当局であるCNILが開発したガイダンスは、ブロックチェーンセグメントで働く人々にとって効率的であると考えられています。

- さらに、サイバー脅威インシデントの増加も、今後数年間の英国国セグメントの成長を後押ししています。例えば、2023年2月に発表されたIBMのX-Force脅威インテリジェンスインデックスレポートによると、過去12ヶ月間に欧州全域で観測された脅威の43%は英国でした。2022年には、エネルギーと金融セクターの侵害件数が最も多く、英国におけるサイバー攻撃全体の16%を占めました。さらに、SurfSharkによると、2023年第2四半期に英国(英国)で約42万件のデータレコードが漏洩しました。2021年第1四半期の約1,500万件に比べ、大幅に減少しました。このようなデータ漏洩の大幅な減少は、全国的にデータ保護サービスがかなり採用されていることを示しているの可能性があります。

欧州のDPaaS(Data Protection-as-a-Service)産業概要

欧州のDPaaS(Data Protection-as-a-Service)市場は中程度の競争であり、複数の重要な参入企業が存在します。これらの参入企業はかなりの市場シェアを占めており、欧州全域での顧客基盤の拡大に注力しています。これらのベンダーは、予測期間中に大きなシェアを獲得するために、新しいソリューションを導入するための研究開発投資、戦略的提携、その他の有機的・無機的成長戦略に注力しています。

2023年10月、Amazonは、EUのデータ主権に関する懸念を最小限に抑えることを目的として、欧州向けのスタンドアロンクラウドサービスの提供を発表しました。Amazon Web Services(AWS)が提供するEuropean Sovereign Cloudは、特に公共部門の顧客や規制の厳しいセグメントの企業向けに提供されます。このクラウドは、ドイツをローンチパッドとして欧州のサーバーにインストールされ、その運用はEUで活動するAWSの担当者のみが管理します。

2023年6月、技術とセキュリティの世界的企業であるタレスは、企業が最も重要なデータを特定、分類、保護できるよう、AIを活用した生成的なデータセキュリティ機能を新たに構築するため、Googleクラウドとの新たな提携を発表しました。この提携はThalesの生成AI戦略の一環であり、同社のサイファートラスト・データセキュリティプラットフォームの顧客にAIを活用した新たな機能と体験を提供することを目的としています。

2023年3月、クラウドプロテクションを提供するAxis Securityは、間もなくHewlett Packard EnterpriseHPEに買収されます。さらに、統合セキュア・アクセスサービスエッジ(SASE)ソリューションを提供することで、エッジからクラウドへのセキュリティ機能を拡大しました。これにより、サービスとして提供されるネットワーキングとセキュリティの統合ソリューションに対する需要の高まりに応えることができるようになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- サードパーティリスク管理への注目の高まり

- データ保護ソリューションの採用を促すGDPRなどの厳しい規制

- EU機関における意識の高まり

- 市場課題

- ブレグジットによるデータ保護の不透明感

第6章 COVID-19が欧州のDPaaS(Data Protection-as-a-Service)市場に与える影響

第7章 市場セグメンテーション

- サービス

- SaaS(Storage-as-a-Service)

- BaaS(Backup-as-a-Service)

- DRaaS(Disaster Recovery-as-a-Service)

- 展開

- パブリッククラウド

- プライベートクラウド

- ハイブリッドクラウド

- エンドユーザー産業

- BFSI

- 医療

- 政府・防衛

- ITと電気通信

- その他

- 国名

- 英国

- ドイツ

- フランス

- その他の欧州

第8章 競合情勢

- 企業プロファイル

- IBM Corporation

- Amazon Web Services Inc.

- Hewlett Packard Enterprise Company

- Dell Technologies

- Cisco Inc.

- Oracle Corporation

- VMware Inc.

- Commvault Systems Inc.

- Veritas Technologies UK Ltd

- Quantum Corporation

- Quest Software UK Ltd

- Hitachi Vantara Corporation

第9章 投資分析

第10章 投資分析市場の将来

目次

The Europe Data Protection-as-a-Service Market size is estimated at USD 6.85 billion in 2025, and is expected to reach USD 13.55 billion by 2030, at a CAGR of 14.6% during the forecast period (2025-2030).

The factors driving the European market for data protection-as-a-service are increased focus on third party risk management coupled with stringent regulations, such as GDPR, prompting the adoption of data protection solutions. Many Europe-based market vendors are also innovating their product offerings by penetrating various industries to gain a competitive advantage, further contributing to the market's growth.

Key Highlights

- In Europe, the General Data Protection Regulation (GDPR) is the primary legal framework that structures guidelines for collecting personal data and information. Compliance with the core tenets of GDPR, relating to personal information collected, accessed, and stored, is a hard take for companies. Therefore, data protection services can enable business self-service analytics while ensuring enterprise governance and compliance.

- Cloud migration is also very high among the end-user industries in the region. With more mobile data generated, more data sources are likely to be added. Hence, the region requires more advanced data preparation solutions.

- Even though the number of data breaches and cyberattacks is increasing in several European countries, customers and organizations in this region have been reluctant to share their data with third-party companies. Moreover, in October 2023, the head of Eon, one of the largest power providers in Germany, stated that the country failed to do strong enough to secure critical assets from cyberattacks and, as a result, called on authorities throughout Europe to take more action. With these increasing numbers of threats in European countries are driving the adoption of data protection services.

- With the increasing incidence of the COVID-19 pandemic, the necessity for safe, simple avenues for data exchange between public bodies and healthcare professionals made its way much more transparent than previously in to fight against the virus. However, the market is facing uncertainties owing to the Brexit effect in the European Union. Google plans to move its British customer's accounts out of EU privacy regulators' control and place them under the United States jurisdiction. The shift, prompted by Britain's exit from the European Union, will leave the sensitive information of millions of customers with less protection and within more comfortable reach of British law.

Europe Data Protection-as-a-Service Market Trends

BFSI Industry is Expected to Grow at a Significant Rate Throughout the Forecast Period

- The banking and financial services industry participants are becoming more digitally sophisticated, so safeguarding corporate data from security breaches is essential. Modernized bank data centers with hybrid cloud infrastructure backed by a digital foundation technology and powered by self-driving operations ensure significantly improved customer experiences. On the other hand, modernization created different security loopholes, resulting in data breaches and other information losses.

- Technology service providers, such as Eurobits, help banks work together so that their customers can quickly pay and manage their bank accounts at multiple banking providers. The company migrated to VMware vSphere on IBM's cloud technology in two data centers to containerize its secure banking applications.

- Many European banks are looking for cloud computing providers with higher security standards than they can find in the United States. The European banks are opting for three major United States cloud providers, Microsoft, Amazon, and Google.

- French and German government officials are in talks with major technology, telecommunications, and finance players to create a competitive continental cloud service run by regional technology provider companies. However, banks, like Germany's Commerzbank AG, have teamed up to present joint cloud requirements to the United States providers to increase the flexibility of data-related regulations.

- Players operating in the market continually invest in innovative solutions to tackle problems efficiently. For instance, Fortinet, a significant cybersecurity solutions provider, announced the launch of FortiGate-VM, extending its native support of VMware NSX-T to provide advanced security for East-West traffic.

United Kingdom Country Segment is Expected to Hold a Significant Share

- The increasing preferences for big data, blockchain, and other initiatives across the UK market landscape have contributed to market growth.

- According to the SAS Institute, retail banking organizations in the United Kingdom are expected to lead in Big Data adoption by a staggering 80%, likely contributing to the market's growth positively.

- The fashion retailer H&M recently started using Big Data to tailor its merchandising mix in its brick-and-mortar stores. To enhance its bottom line, the fashion retailer uses algorithms and different customer data sources to gain insights from receipts, returns, and data from loyalty cards.

- In the United Kingdom, blockchain users can refer to the guidance developed in France to help them comply with data protection laws. The United Kingdom's data protection authority has ignored the significant legislation related to cryptocurrency mining and related technologies. The guidance developed by CNIL, the French data protection authority, has been considered efficient for people working in the blockchain field.

- Furthermore, the increasing number of cyber-threat incidents is also driving the growth of the United Kingdom country segment in the coming years. For instance, according to IBM's X-Force Threat Intelligence Index report, published in February 2023, 43% of threats observed throughout Europe during the previous 12 months were in the UK. In 2022, the energy and financial sectors experienced the highest number of breaches, accounting for 16% of all cyberattacks in the UK. Moreover, according to SurfShark, approximately 420 thousand data records in the United Kingdom (UK) were compromised in the second quarter of 2023. The number dropped significantly compared to about 15 million in the first quarter of 2021. Such a significant drop in data compromises might indicate the considerable adoption of data protection services nationwide.

Europe Data Protection-as-a-Service Industry Overview

The European data protection-as-a-service market is moderately competitive and has several significant players. These players account for a substantial market share and are focusing on expanding their customer base across the European region. These vendors focus on research and development investment to introduce new solutions, strategic alliances, and other organic and inorganic growth strategies to capture a significant share during the forecast period.

In October 2023, Amazon announced the availability of standalone cloud services for Europe, aiming to minimize concerns regarding EU data sovereignty. The European Sovereign Cloud from Amazon Web Services (AWS), particularly for public sector clients and business enterprises in highly regulated sectors, will be made available by the company. The cloud will be installed on European servers, with Germany serving as the launchpad, and its operation will be governed solely by AWS personnel operating in the EU.

In June 2023, Thales, a global player in technology and security, announced a new partnership with Google Cloud to create new generative AI-powered data security capabilities to help businesses identify, categorize, and safeguard their most critical data. The association is a component of Thales' generative AI strategy, which aims to provide customers of the company's CipherTrust data security platform with new AI-powered capabilities and experiences.

In March 2023, Axis Security, a company that offers cloud protection, will soon be acquired by Hewlett-Packard Enterprise HPE. Additionally, it expanded its edge-to-cloud security capabilities by providing a unified Secure Access Services Edge (SASE) solution. It will now be able to satisfy the increasing demand for integrated networking and security solutions that are provided as a service.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Focus on Third-party Risk Management

- 5.1.2 Stringent Regulations, such as GDPR Prompting the Adoption of Data Protection Solutions

- 5.1.3 Increasing Awareness among EU Institutions

- 5.2 Market Challenges

- 5.2.1 Uncertainty Regarding Data Protection Landscape due to Brexit

6 IMPACT OF COVID-19 ON THE EUROPE DATA PROTECTION-AS-A-SERVICE MARKET

7 MARKET SEGMENTATION

- 7.1 Service

- 7.1.1 Storage-as-a-Service

- 7.1.2 Backup-as-a-Service

- 7.1.3 Disaster Recovery-as-a-Service

- 7.2 Deployment

- 7.2.1 Public Cloud

- 7.2.2 Private Cloud

- 7.2.3 Hybrid Cloud

- 7.3 End-user Industry

- 7.3.1 BFSI

- 7.3.2 Healthcare

- 7.3.3 Government and Defense

- 7.3.4 IT and Telecom

- 7.3.5 Other End-user Industries

- 7.4 Country

- 7.4.1 United Kingdom

- 7.4.2 Germany

- 7.4.3 France

- 7.4.4 Rest of Europe

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 IBM Corporation

- 8.1.2 Amazon Web Services Inc.

- 8.1.3 Hewlett Packard Enterprise Company

- 8.1.4 Dell Technologies

- 8.1.5 Cisco Inc.

- 8.1.6 Oracle Corporation

- 8.1.7 VMware Inc.

- 8.1.8 Commvault Systems Inc.

- 8.1.9 Veritas Technologies UK Ltd

- 8.1.10 Quantum Corporation

- 8.1.11 Quest Software UK Ltd

- 8.1.12 Hitachi Vantara Corporation

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日