パッドマウント変圧器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Pad Mounted Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643179

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

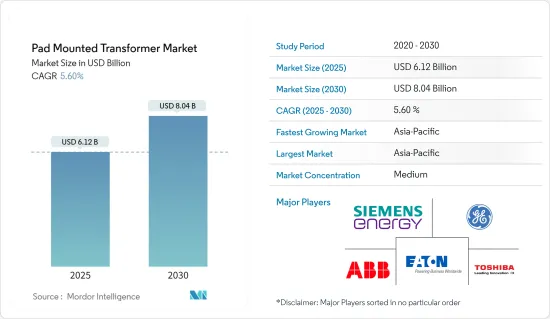

パッドマウント変圧器の市場規模は2025年に61億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.6%で、2030年には80億4,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、世界の発電容量の増加計画、老朽化した配電変圧器の交換/改修需要の増加、電力需要の増加といった要因が、予測期間中の市場を牽引すると見込まれます。

- その一方で、消費者側での分散型エネルギー発電の採用が増加していることが、市場の成長を妨げる可能性が高いです。

- とはいえ、中東・アフリカ、アジア太平洋地域における電化プロジェクトの増加や、いくつかの政府イニシアティブは、パッドマウント変圧器市場のプレーヤーにとって、今後数年間で十分な機会を創出すると予想されます。

- アジア太平洋地域が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。中国とインドが市場を牽引しているが、これはこれらの国々の電力インフラが成長しているためです。

パッドマウント変圧器市場動向

油入変圧器タイプが市場を席巻

- 油入変圧器は液体冷却を採用しており、屋外での使用に理想的で、効率の向上、耐用年数の延長、信頼性の高い過負荷機能を提供します。冷却媒体として液体を利用することで、これらの変圧器は乾式を上回り、より高い定格と過負荷を扱えるという特筆すべき利点があります。

- インドや中国などの国々では、都市化の進展による電力需要の増加に対応するため、送配電網を拡張しており、商業・産業拠点の設立が油入りパッドマウント変圧器市場を牽引すると予想されています。

- 例えば、インド政府の目標は、Pradhan Mantri Sahaj Bijli Har Ghar Yojanaを通じて全世帯の電化を実現し、Deendayal Upadhyaya Gram Jyoti Yojana(DDUGJY)を通じて農村部の電力供給品質を改善することであり、予測期間中にパッドマウント変圧器市場を押し上げると予想されています。

- 油入変圧器は通常キャビネットに収納されているため、公共スペースで使用する安全な変圧器として好まれています。これと同様に、多くの国々で電気自動車の充電インフラが整備されているため、油入りのパッドマウント変圧器の設置は間違いなく増加すると予想されます。

- 例えば、2023年5月、LNGエレクトリック社は米国内の13,000軒以上のホテルでEV充電インフラを開始すると発表しました。これに加え、LNGエレクトリックは40以上の集合住宅地域に充電ステーションを設置する可能性が高いです。これは間違いなく米国のパッドマウント変圧器市場に弾みをつけると思われます。

- さらに、世界中で発電量が増加傾向にあるため、電力会社は送電線の安全で信頼性の高い運用のために計器用変圧器を導入する必要があります。2022年現在、発電量は29,165 TWhで、2021年から約2%増加しています。発電量の緩やかな増加は、パッドマウント変圧器市場の今後の成長を後押しすると思われます。

- したがって、上記の要因から、予測期間中、油入変圧器が世界のパッドマウント変圧器市場を独占すると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、発電能力の拡大、老朽化した配電用変圧器の交換・改修ニーズの急増、電力需要の増加に牽引され、急速な成長が見込まれています。この成長は、産業インフラの開発加速によって拍車がかかり、特に中国とインドで顕著です。

- この地域のさまざまな国々が、工業や商業部門の増加など、地域の開発活動の拡大に重点を移しており、それが電力需要の原動力となって、より効率的な電気インフラに対する需要が高まっています。

- 例えば、中国で最も重要な電力会社である中国国家電網公司によると、送電網インフラと関連産業への投資は、送電、電気自動車充電器、新しいデジタルインフラを中心に、2021-2025年に約8,960億米ドルを超えると予想されています。このことは、同国におけるパッドマウント変圧器市場開拓の見込みが高いことを示しています。

- 同様に、2022年8月、パンジャブ州政府は、消費者向け電力供給の口径と信頼性を強化するため、3,080億米ドルの行動計画を承認しました。この計画の一環として、89基と382基の66/11kV変圧器の建設と増強、94基の新しい66KV変電所の試運転など、さまざまなインフラ・プロジェクトが実施されます。また、2万3,687台の11KV配電変圧器の設置、15,859回路kmのHT/LT送電線の敷設、2,015回路kmの66kV送電線の敷設も計画されています。従って、これは同国におけるパッドマウント変圧器の配備範囲が広いことを示しています。

- さらに、長年にわたる再生可能エネルギー発電の成長により、アジア太平洋地域は最前線に位置しています。2022年の発電量は2003TWhで、前年から約18%増加しました。再生可能エネルギー発電の成長と関連プロジェクトは、アジア太平洋地域の計器用変圧器市場を増加させると思われます。

- したがって、上記の要因は、予測期間中、アジア太平洋地域全体のパッドマウント変圧器の需要を補う可能性が高いです。

パッドマウント変圧器産業の概要

パッドマウント変圧器市場は半分断されています。主な企業(順不同)は、ABB Ltd、Siemens Energy AG、Eaton Corporation PLC、Toshiba Corporation、General Electric Companyです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 世界の発電能力の増加

- 産業・インフラ開発による電力需要の増加

- 抑制要因

- 分散型エネルギー発電の増加

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- オイル充填

- 乾式

- フェーズ別

- 単相

- 三相

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- マレーシア

- オーストラリア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- コロンビア

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

- ナイジェリア

- カタール

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- ABB Ltd

- Eaton Corporation PLC

- General Electric Company

- Mitsubishi Electric Corporation

- Schneider Electric SE

- Siemens Energy AG

- Toshiba Corporation

- CG Power and Industrial Solutions Limited

- Olsun Electrics Corporation

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 変圧器技術における技術進歩の高まり

目次

Product Code: 70164

The Pad Mounted Transformer Market size is estimated at USD 6.12 billion in 2025, and is expected to reach USD 8.04 billion by 2030, at a CAGR of 5.6% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as plans for increasing power generation capacity worldwide, growing demand for replacing/refurbishing aging distribution transformers, and increasing electricity demand are expected to drive the market during the forecast period.

- On the other hand, the increase in adoption of distributed energy generation at the consumer's end is likely to hamper the market's growth.

- Nevertheless, increasing electrification projects in the Middle East & Africa, Asia-Pacific, and several government initiatives are expected to create ample opportunities for pad-mounted transformer market players over the coming years.

- The Asia-Pacific region is expected to dominate the market and will likely register the highest CAGR during the forecast period. China and India drive it due to these countries' growing electricity infrastructure.

Pad Mounted Transformer Market Trends

Oil-filled Transformer Type to Dominate the Market

- Oil-filled transformers employ liquid cooling and prove ideal for outdoor use, offering increased efficiency, prolonged service life, and dependable overload capabilities. Utilizing liquid as a cooling medium, these transformers surpass dry types, with the notable advantage of handling higher ratings and overloads.

- Countries such as India and China are expanding their transmission & distribution network to cater to the rise in electricity demand due to increased urbanization and establishing commercial & industrial hubs, which is expected to drive the oil-filled pad-mounted transformer market.

- For Instance, the Indian government's goal is to electrify every household through the Pradhan Mantri Sahaj Bijli Har Ghar Yojana and improve power supply quality in rural areas via the Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY) is expected to boost the market for pad-mounted transformers in the forecasted period.

- Oil-filled transformers are preferred as a safe and secure transformer for use in public spaces as they are usually enclosed in a cabinet. Along the same line, due to the roll-out of electric vehicle charging infrastructures in many countries, the installation of oil-filled pad-mounted transformers is undoubtedly expected to increase.

- For instance, in May 2023, LNG Electric announced the launch of an EV charging infrastructure for over 13,000 hotels in the United States. In addition to it, LNG Electric would likely install charging stations in more than forty multifamily community areas. This would undoubtedly give a thrust to the pad-mounted transformers market in the United States.

- Moreover, the rising trend of electricity generation across the globe would also necessitate power utilities to deploy instrument transformers for the safe and reliable operation of transmission lines. As of 2022, the electricty generation was 29,165 TWh, about a 2 % increase from 2021. The gradual growth in electricity generation would help the pad-mounted transformer market grow in the future.

- Hence, owing to the above factors, oil-filled type transformers are expected to dominate the global pad-mounted transformer market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is anticipated to experience rapid growth, driven by expanding power generation capacities, a surging need to replace/refurbish aging distribution transformers, and rising electricity demand. This growth, spurred by the accelerated development of industrial infrastructure, is notably prominent in China and India.

- Various countries in the region have shifted their focus on increasing the developmental activities in their region, such as increasing the industrial and commercial sectors, which in turn drives the demand for electricity, raising the demand for more efficient electrical infrastructure.

- For instance, according to the State Grid Corp. of China, the country's most significant power utility, investments in power grid infrastructure and related industries are expected to surpass approximately USD 896 billion in 2021-2025, focusing on power transmission, electric vehicle chargers, and new digital infrastructure. This indicated high prospects for developing the pad-mounted transformers market in the country.

- Similarly, in August 2022, the Punjab government approved a USD 308 billion action plan to enhance the caliber and dependability of consumer electricity supply. Various infrastructure projects, including the construction and augmentation of 89 and 382 66/ 11 kV power transformers and the commissioning of 94 new 66 KV sub-stations, will be carried out as part of the plan. The plan also calls for installing 23,687 11KV distribution transformers, laying 15,859 circuit km of HT/LT lines, and laying 2,015 circuit km of 66 kV transmission lines. Hence, this indicates a broad scope for the deployment of pad-mounted transformers in the country.

- Moreover, the growth in renewable energy generation over the years has put the Asia-Pacific region at the forefront. In 2022, the electricity generation was 2003 TWh, an increase of about 18% from the previous year. Renewable energy generation growth and the associated projects would likely increase the instrument transformer market in the Asia-Pacific region.

- Hence, the above factors are likely to supplement the demand for pad-mounted transformers across the Asia-Pacific region during the forecast period.

Pad Mounted Transformer Industry Overview

The pad-mounted transformer market is semi-fragmented. Some of the major companies (in no particular order) are ABB Ltd, Siemens Energy AG, Eaton Corporation PLC, Toshiba Corporation, and General Electric Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Power Generation Capacity Worldwide

- 4.5.1.2 Rise In Electricity Demand Due Increase Industrial And Infrastructural Development Activities

- 4.5.2 Restraints

- 4.5.2.1 Growth In Distributed Energy Generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Oil-filled

- 5.1.2 Dry Type

- 5.2 Phase

- 5.2.1 Single-phase

- 5.2.2 Three-phase

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 NORDIC Countries

- 5.3.2.7 Turkey

- 5.3.2.8 Russia

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Malaysia

- 5.3.3.5 Australia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Argentina

- 5.3.4.2 Brazil

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd

- 6.3.2 Eaton Corporation PLC

- 6.3.3 General Electric Company

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 Schneider Electric SE

- 6.3.6 Siemens Energy AG

- 6.3.7 Toshiba Corporation

- 6.3.8 CG Power and Industrial Solutions Limited

- 6.3.9 Olsun Electrics Corporation

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Technological Advancements in the Transformer Technology

パッドマウント変圧器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日