|

市場調査レポート

商品コード

1643143

アジア太平洋のテレマティクス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)APAC Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のテレマティクス-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

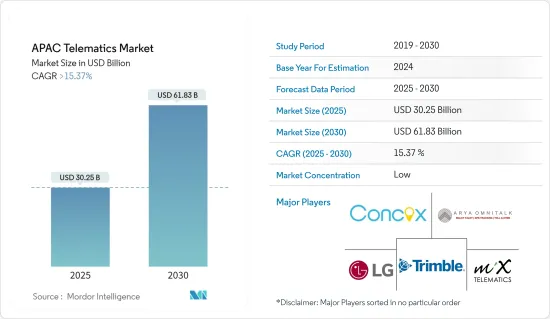

アジア太平洋のテレマティクス市場規模は2025年に302億5,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは15.37%を超え、2030年には618億3,000万米ドルに達すると予測されます。

テレマティクスは、車両管理会社や自動車保険会社に情報を提供し、車両の位置や行動をモニタリングすることで、利用ベースの保険(UBI)に役立っています。商用車や高度道路交通システム(ITS)のナビゲーション義務化による交通安全に対する政府の取り組み、EV需要の高まり、手頃な価格のセンサによる接続動向の高まりが、主にアジア太平洋のテレマティクス市場の成長を牽引しています。中国、日本、韓国などの国々における5Gインフラの開発もアジア太平洋のテレマティクス産業を後押しします。

主要ハイライト

- Qualcomm Technologies Inc.は、Snapdragon Car-to-Cloud Servicesの機能であるConnectivity-as-a-Serviceを発表しました。これは、すぐに使える接続性、統合された分析、新しい技術機能、コンテンツ、サービスを世界に提供することを目的としたクラウドとデバイス開発者環境をサポートする新しい技術連携をもたらすものです。コグニザントは、Qualcomm Technologies Inc.と協力して、自動車メーカー向けにSnapdragon Car-to-Cloud Servicesを統合し、カスタマイズします。これは、リッチで没入感のあるパーソナライズされた車載体験、新しい接続ソリューション、より優れたオンデマンドサービスを提供することを目的としています。

- コネクテッドカーサービスの利用増加が市場を牽引する中、各社は戦略的パートナーシップを結び、玄関先でサービスを提供しています。インドのAutoTech新興企業ReadyAssistは、テレマティクスソリューションの車両追跡と車両管理の技術プロバイダーであるiTriangle Infotechとの戦略的提携を発表しました。この提携により、両社のテレマティクスとサービスネットワークという既存の能力を相互活用し、IoT機器の設置、サービス、保証交換を顧客の目の前で行うことができるようになります。

- アジア太平洋では、都市化、生活水準の向上、経済成長により、自動車保有台数が大幅に増加しています。道路を走る車両が増えるにつれ、効率的な車両管理とメンテナンスソリューションに対するニーズが高まっています。IEAによると、2022年にアジア太平洋で最も電気自動車が販売されたのは中国で、約600万台の電気自動車が販売されました。テレマティクスは、電気自動車の性能を管理・モニタリングし、運転体験の最適化と効率を高める上で重要な役割を果たします。

- しかし、テレマティクスシステムのコストが高いこと、製品が標準化されていないこと、サイバーセキュリティの脅威が増大していることなどが、この市場の成長を抑制する主要要因となっています。さらに、個々の商用車/乗用車や小型車フリート事業者の認知度が低いことも、調査した市場の成長に課題となっています。

アジア太平洋のテレマティクス市場動向

乗用車セグメントが大きな市場シェアを占める見込み

- 乗用車セグメントは販売台数が多いため、アジアのテレマティクス市場を牽引すると予想されます。安全性と利便性の高いテレマティクスサービスに対する需要の高まりが、乗用車セグメントに拍車をかけています。過去10年間の大幅な技術開発により、コネクテッドカーが発売され、さらなる進化が期待されています。中国、インド、オーストラリア、日本といった国々は主要な乗用車市場を有しており、これらの国々では乗用車の安全規制がより厳しくなっているため、ハイエンドのテレマティクスサービスと接続性ソリューションに対する需要が高まっている

- インドの自動車部門には、2,000年 4月から2022年 9月までの間に約337億7,000万米ドルの株式FDIが流入しました。インド政府は、自動車産業が2023年までに80億~100億米ドルの外国・国内投資を誘致すると見込んでいます。

- OICAによると、2023年には中国がアジア太平洋の乗用車市場を独占し、2,600万台以上を販売します。第2位はインドで、販売台数は410万台に迫る。乗用車の生産と販売の拡大が、この地域の市場を牽引すると予想されます。

- 中国はアジア太平洋のテレマティクス市場の成長に大きく貢献しています。Nio、FutureMove、ThunderPower、Qorosのような中国の新しい自動車新興企業の中には、最新のポートフォリオにナビゲーションやリアルタイムの交通情報システムを採用しているところもあります。中国では車両盗難が増加しており、盗難車両追跡(SVT)技術の需要が着実に増加しています。

- 先進運転支援システム(ADAS)もアジア太平洋のテレマティクス市場を牽引する要因の一つです。日本は、ほとんどの自動車ADASを発明し、実装した最初の国の一つです。日本の自動車会社はテレマティクスと車両接続技術のための先進デバイスを開発しています。

中国市場は大幅な成長が見込まれる

- 中国のテレマティクス市場は著しく成長しており、同国の自動車産業は急速にテレマティクス技術を採用し、その結果、相当数のコネクテッドカーが路上を走るようになりました。コネクテッドカーは、ナビゲーション、遠隔診断、インフォテインメント、安全機能など様々なサービスを可能にします。

- 中国政府はテレマティクスの普及に重要な役割を果たしています。2022年1月、中国政府は自律走行の導入と適応を形成するために定期的に規則を変更しました。ADASやその他のコネクテッドカー機能を搭載した自動車には、自律走行システムを指示するすべての変数を記録する、バックボックスを持つ航空機に似た装置を装着しなければならないです。中国は自動車用マイクロコントローラとマイクロプロセッサで世界的に優位に立っているため、テレマティクス・コントロール・ユニット(TCU)の製造でも優位に立つことができます。また、最近の5Gインフラ市場への投資(COVID-19発生からの回復措置として)は、5G TCUの現地生産をさらに促進します。

- モノのインターネット(IoT)の普及と中国における5Gネットワークの展開は、テレマティクスシステムの能力を大幅に向上させました。より高速で信頼性の高い接続性により、リアルタイムのデータ伝送が可能になり、遠隔モニタリング、無線アップデート、V2X(Vehicle-to-Everything)通信などの先進的テレマティクスサービスが可能になります。

- 中国における基地局数の増加が市場を牽引し、より高速で信頼性の高いデータ通信を可能にし、可用途の範囲を拡大し、自動車・運輸産業のイノベーションを促進します。MIITによると、2023年末までに中国の5G基地局数は約338万局になります。大規模なインフラ投資と野心的な展開計画により、中国は5Gの大幅な普及を達成しています。基地局数は2024年までに約600万に達すると予測されています。

- テレマティクスが提供する車両管理ソリューションは、中国では特に物流、運輸、eコマースセグメントで高い需要があります。これらのソリューションは、企業が車両を最適化し、運用コストを削減し、燃料効率を向上させ、ドライバーの安全性を高めるのに役立っています。

アジア太平洋のテレマティクス産業概要

アジア太平洋のテレマティクス市場は非常にセグメント化されており、LG Corporation、MiX Telematics Ltd、Concox Information Technology、Trimble Inc.、Arya Omnitalk Wireless Solutions Private Limitedといった大手企業が存在します。市場の参入企業は、製品提供を強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2022年12月-OCTO Telematicsは、技術、ロボット工学、オートメーションの戦略的拠点での存在感を強化するため、日本の東京に拠点を開設すると発表しました。OCTOの日本法人は、日本と周辺諸国におけるコネクテッドモビリティ市場の開拓をさらに支援し、パートナーに技術と営業サポートを記載しています。

- 2022年10月-Asia MobilitiはTruck Itと提携し、広告バイヤーに対象を絞り、すべてのトラックのリアルタイムの追跡情報、ルートを提供し、彼らの選択に合ったトラックのタイプを表示する機能を提供する包括的なテレマティクスとジオマッピング技術を記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- コネクテッドカーサービスの利用増加

- 簡単な車両診断への需要の高まり

- 市場抑制要因

- データハッキングによるデータセキュリティへの脅威

第6章 市場セグメンテーション

- 車種別

- 商用車(トラック) LCV対M/HCV

- 乗用車

- チャネル別

- OEM

- 新聞

- アフターマーケット

- 国別

- 中国

- 日本

- 韓国

- 東南アジア

第7章 競合情勢

- 企業プロファイル

- LG Corporation

- MiX Telematics Ltd

- Concox Information Technology Co. Ltd

- Trimble Inc.

- Arya Omnitalk Wireless Solutions Private Limited

- iData Kft(iTrack)

- Bright Box Hungary Kft

- Tata Consultancy Services Ltd

- Efkon India Pvt Ltd

- Tech Mahindra Limited

- Meitrack Group

- Octo Group S.p.A

- Asia Mobility Technologies Sdn Bhd

第8章 投資分析

第9章 市場の将来

The APAC Telematics Market size is estimated at USD 30.25 billion in 2025, and is expected to reach USD 61.83 billion by 2030, at a CAGR of greater than 15.37% during the forecast period (2025-2030).

Telematics helps in usage-based insurance (UBI) by providing information to fleet management companies and automobile insurance companies to monitor the location and behavior of vehicles. Government initiatives towards road safety with mandatory navigation for commercial vehicles and Intelligent Transport System (ITS), rising demand for EVs, and increasing trend of connectivity with affordable sensor prices are mainly driving the growth in the Asia-Pacific telematics market. The development of 5G infrastructure in countries such as China, Japan, and South Korea will also boost the telematics industry in the Asia Pacific.

Key Highlights

- Qualcomm Technologies introduced a feature for Snapdragon Car-to-Cloud Services - Connectivity-as-a-Service - that brings new technology collaborations to support out-of-the-box connectivity, integrated analytics, and a cloud and device developer environment aimed to deliver new technology features, content, and services globally. Cognizant will work with Qualcomm Technologies to integrate and tailor Snapdragon Car-to-Cloud Services for automakers, with the goal of delivering rich, immersive, personalized in-vehicle experiences, new connected solutions, and better on-demand services.

- With the increase in usage of connected car services driving the market, companies are making strategic partnerships to offer services at the doorstep. Indian AutoTech startup ReadyAssist announced its strategic partnership with iTriangle Infotech, a technology provider for vehicle tracking and fleet management for telematics solutions. The partnership will cross-leverage the companies' existing capabilities of telematics and service networks to bring installation, service, and warranty replacements of IoT devices to their customers at the doorstep.

- The Asia Pacific region has witnessed a substantial increase in vehicle ownership due to urbanization, improved living standards, and economic growth. With more vehicles on the road, there is a growing need for efficient vehicle management and maintenance solutions. According to IEA, in 2022, China witnessed the highest number of electric car sales across the Asia Pacific region, with around six million electric car sales, and nearly 28,000 electric cars were sold in 2022 in New Zealand. The growth in EVs is anticipated to drive the telematics market, as these advanced systems play a crucial role in managing and monitoring EV performance, enhancing optimization and efficiency of the driving experience.

- However, the higher cost of telematics systems, lack of standardization of products, and increasing cybersecurity threats are among the major factors restraining the growth of the market studied. Additionally, a lower awareness among individual commercial/passenger vehicles and small vehicle fleet operators also challenges the growth of the market studied.

APAC Telematics Market Trends

Passenger Type of Vehicles Segment is Expected to Hold Significant Market Share

- The passenger car segment is expected to drive the Asian telematics market owing to a high sales rate. Increased demand for safety and convenience telematics services is fueling the passenger car segment. Significant technological developments over the last decade have resulted in the launch of connected cars, which are expected to evolve further. Countries like China, India, Australia, and Japan have major passenger vehicle markets, and the safety regulations for these vehicles are more stringent in these countries, leading to the demand for high-end telematics services and connectivity solutions.

- The automobile sector in India got a cumulative equity FDI inflow of around USD 33.77 billion between April 2000 and September 2022. The Indian government expects the automobile industry to attract USD 8-10 billion in foreign and local investments by 2023.

- According to OICA, in 2023, China dominated the Asia-Pacific passenger car market, selling over 26 million units. India followed as the second-largest market, with sales nearing 4.1 million units.. The growing production and sale of passenger vehicles are expected to drive the market in the region.

- China is a major contributor to the growth of the APAC telematics market. Some of the new automotive start-ups in China, like Nio, FutureMove, ThunderPower, and Qoros, use navigation and real-time traffic information systems in their latest portfolios. There is a steady increase in the demand for Stolen Vehicle Tracking (SVT) technology as vehicle thefts rise in China.

- The Advanced Driver Assistance System (ADAS) is another factor driving the APAC telematics market. Japan was one of the first countries to invent and implement most car ADAS. Japanese automotive companies are developing advanced devices for telematics and vehicle connectivity technologies.

China Expected to Witness Significant Growth in the Market

- The telematics market in China is significantly growing, and the country's automotive industry has quickly adopted telematics technology, resulting in a substantial number of connected vehicles on the road. Connected cars enable various services such as navigation, remote diagnostics, infotainment, and safety features.

- The Chinese government has played a crucial role in promoting telematics adoption. In January 2022, the Chinese government changed the rules regularly to shape the country's introduction and adaptation of autonomous driving. The cars with ADAS and other connected car features must be fitted with devices similar to aircraft having back boxes, recording all the variables directing the autonomous driving systems. China's dominance in global automotive microcontrollers and microprocessors also gives them the upper hand in manufacturing telematics control units (TCU). Also, the country's recent investment in the 5G infrastructure market (as a recovery step from the COVID-19 outbreak) further promotes the local production of 5G TCUs.

- The proliferation of the Internet of Things (IoT) and the deployment of 5G networks in China have significantly enhanced the capabilities of telematics systems. Faster and more reliable connectivity allows for real-time data transmission, enabling advanced telematics services such as remote monitoring, over-the-air updates, and vehicle-to-everything (V2X) communication.

- The increasing number of base stations in China drives the market, enabling faster and more reliable data communication, expanding the range of possible applications, and fostering innovation in the automotive and transportation industries. According to MIIT, by the end of 2023, the number of 5G base stations in China is approximately 3.38 million. With extensive infrastructure investments and ambitious rollout plans, China has achieved significant 5G coverage. The forecasted number of base stations was projected to reach about six million by 2024.

- Fleet management solutions offered by telematics are in high demand in China, particularly in the logistics, transportation, and e-commerce sectors. These solutions help companies optimize their fleets, reduce operating costs, improve fuel efficiency, and enhance driver safety.

APAC Telematics Industry Overview

The Asia Pacific Telematics market is highly fragmented, with the presence of major players like LG Corporation, MiX Telematics Ltd, Concox Information Technology Co. Ltd, Trimble Inc., and Arya Omnitalk Wireless Solutions Private Limited. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022 - OCTO Telematics announced an opening in Tokyo, Japan, to strengthen its presence in a strategic hub for technology, robotics, and automation. The Japanese subsidiary of OCTO will further help the development of the connected mobility market throughout Japan and surrounding countries, providing technical and sales support to partners.

- October 2022 - Asia Mobiliti collaborated with Truck It to provide comprehensive telematics and geo-mapping technologies that would offer advertisement buyers the capability to target their customers, offer them real-time tracking information of all trucks, routes, and display the type of truck that suits their choice.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Connected Cars Services

- 5.1.2 Growing Demand for Easy Vehicle Diagnostics

- 5.2 Market Restraints

- 5.2.1 Threats to Data Security in the form of Data Hacking

6 MARKET SEGMENTATION

- 6.1 By Type of Vehicle

- 6.1.1 Commercial (Truck) LCV Vs. M/HCV

- 6.1.2 Passenger (Car)

- 6.2 By Channel

- 6.2.1 OEM

- 6.2.2 Newsprint

- 6.2.3 Aftermarket

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 South Korea

- 6.3.4 South East Asia

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 LG Corporation

- 7.1.2 MiX Telematics Ltd

- 7.1.3 Concox Information Technology Co. Ltd

- 7.1.4 Trimble Inc.

- 7.1.5 Arya Omnitalk Wireless Solutions Private Limited

- 7.1.6 iData Kft (iTrack)

- 7.1.7 Bright Box Hungary Kft

- 7.1.8 Tata Consultancy Services Ltd

- 7.1.9 Efkon India Pvt Ltd

- 7.1.10 Tech Mahindra Limited

- 7.1.11 Meitrack Group

- 7.1.12 Octo Group S.p.A

- 7.1.13 Asia Mobility Technologies Sdn Bhd