|

市場調査レポート

商品コード

1643090

ロボットビジョン:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Robotic Vision - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ロボットビジョン:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

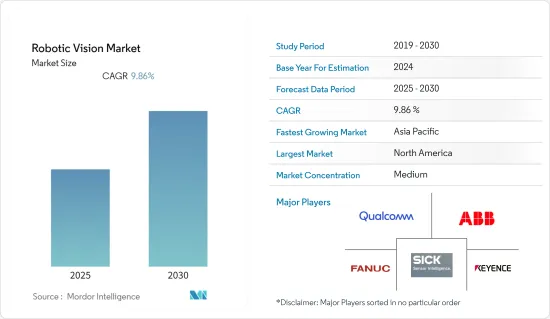

ロボットビジョン市場は予測期間中にCAGR 9.86%を記録する見込みです。

主なハイライト

- マシンガイダンスシステムは、2Dおよび3Dマシンビジョンシステムを使用して、組立ロボットや自動マテリアルハンドリング装置の精度と速度を向上させます。アプリケーションは、生産される車両やモデルによって異なりますが、一般的なカテゴリーとしては、ロボット工学、寸法計測機能、組立検証、欠陥検出、塗装作業検証、コード読み取りなどが観察されます。

- ロボットビジョンは、カメラと画像処理を使用して、手作業による検査作業を補完または代替するための視覚をロボットに提供します。その用途は、存在検知のような基本的な作業からリアルタイムの検査まで多岐にわたる。

- 特に検査のような冗長な作業を正確に行う必要がある分野では、世界中の製造企業がこうしたロボットビジョンシステムの利点を実感しています。高速の生産ラインや危険な環境では不可欠な役割を果たします。これらのシステムの大きな利点は、生産性の向上、機械のダウンタイムの削減、より厳密な工程管理などです。

- ビジョンセンサやビジョンソフトウェアなど、ロボットビジョンのコアコンポーネントの開発には多額の費用が必要です。また、ロボットビジョンの導入にかかる初期費用もやや大きく、市場拡大の妨げになる可能性があります。

- COVID-19の流行は、複数のエンドユーザー産業において、人との接触を減らすことができるビジョン誘導ロボットの成長を増加させると予想されます。例えば、米国のOrrbec社は中国のロボットメーカーと協働し、さまざまな病院用途のロボットに3Dカメラ製品を導入しました。フードデリバリーロボット、滅菌ロボット、マシンビジョンシステムを使用した方向案内ロボットが中国の多くの病院に導入されています。認知型ヒューマノイドロボットの採用増加に伴い、市場はパンデミック後に急拡大しています。

ロボットビジョン市場動向

自動車産業などエンドユーザーからの需要拡大が市場成長を牽引

- 品質問題に対処するため、自動車メーカーはビジョンシステムへの投資を増やしています。この技術は、接着剤ディスペンシング、ビンピッキング、エラー防止、インライン溶接分析、マテリアルハンドリング、ロボットガイダンス、表面検査、トレーサビリティなど、さまざまな用途で自動車メーカーや部品サプライヤーによってますます使用されるようになっています。カスタマイズ需要の高まり、労働力不足の増加、コスト圧力は、自動車産業で使用されるビジョンシステムの重要な促進要因です。

- ビジョン誘導ロボットは、エレクトロニクス、自動車、食品加工産業に革命を起こすと予測されています。アーク溶接、切断、パレタイジングなどのアプリケーションに対する技術需要が非常に大きいため、これらの産業では3Dビジョンガイド技術が主流となっています。

- 高度なマシンビジョン技術は、世界の様々な自動車工場の日常業務で重要な役割を果たしています。例えば、フォード・モーターのヴァン・ダイク・トランスミッション工場では、ギアやクラッチなどの重要部品の高品質な組み立てを保証するためにビジョンガイドロボットを使用しています。この工場では、エラー防止、ゲージング、複雑性の問題を解決するために、500以上のインライン・マシン・ビジョンアプリケーションを導入しています。

- 自動車におけるADASシステムの成長に伴い、カメラ主導の照明、ライダー、V2Xなどのコンポーネントの要件は、自動化とインテリジェンスのためにまもなく重要な役割を果たすと思われます。さらに、Neuromationによると、交通事故は世界の死者の2.2%を占めています。2Dおよび3Dマシンビジョンとインテリジェント交通システム(ITS)により、ドライバーはセーフティネットを利用できます。これらの技術は、自動車産業におけるヒューマンエラーを軽減することを可能にし、重大なミスや事故を起こさないためのツールや機能でハンドルを握るドライバーをサポートします。

- 非接触検査、高い再現性、最小限のコストにより、ロボットビジョンシステムは様々な分野での品質管理に普及しつつあります。従来の製品の品質管理方法は、すべて人の手による検査に頼っていました。一方、人間による検査は、疲弊と繰り返しにより、交代勤務の間にパフォーマンスが低下すると予測されています。些細な欠陥に気づかず、些細でないエラーを引き起こすこともあります。技術の進歩は、時間のかかる検査作業を人間から機械による自動化へと移行させつつあります。ハードウェアとソフトウェアの大幅な進歩により、すでに世界のさまざまな地域で、品質管理検査の労働力の大半が機械に移行しています。IFRによると、中国では新たに約16万8,000台の産業用ロボットが設置され、前年度に世界で最も多くのロボットが設置されました。

北米が急成長市場になる見込み

- ロボットの導入において、北米は重要な発明者であり先駆者であり、世界最大の市場のひとつです。さまざまな分野でロボット工学の導入が進んでいることが、市場成長の主な要因となっています。

- 国際ロボット連盟によると、北米における産業用ロボットの導入は、今年までに年間6万9,000台に達すると予測されています。Advancing Automationによると、昨年のロボット販売台数は前年比28%増と推定されています。生産性向上と労働力不足解消のため、より多くの分野でオートメーション化が進む中、昨年第4四半期のロボット販売台数は過去最高を記録し(前年同期比9%増)、この数ヶ月ですでに大きな勢いを見せています。

- 産業用ロボットは産業オートメーションに欠かせない存在であり、さまざまなロボットがさまざまな産業で重要な機能を担っています。エレクトロニクス、eコマース、自動車産業などは、この地域の多くの国々における景気拡大とともに成長しています。製品メーカーは、経済全体における需要の高まりを受けて、反復的な手順を自動化するロボットを急速に採用しています。

- 企業、大学、連邦政府に将来の自動化技術への投資を奨励することを目的とした先進製造パートナーシップのような政府の取り組みにより、マシンビジョンシステムはより頻繁に生産されるようになると思われます。

- MAPI(Manufacturers Alliance for Productivity and Innovation)によると、米国の工業生産は前年までに2.8%増加すると推定され、ロボットビジョン技術の使用を後押ししています。

ロボットビジョン産業概要

ロボットビジョン市場は、Qualcomm Technologies, Inc.、Keyence Corporation、FANUC Corporation、ABB Group、Sick AGなどの大手企業によって適度に断片化されています。市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、パートナーシップ、イノベーション、買収などの戦略を採用しています。

- 2022年10月-ABBは、米国を拠点とする新興企業Scalable Roboticsとの戦略的パートナーシップを発表し、ユーザーフレンドリーなロボット溶接ソリューションラインを拡大します。スケーラブル・ロボティクスのテクノロジーは、3Dビジョンと組み込みプロセス認識を利用し、ユーザーはコーディングなしで溶接ロボットをプログラムすることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

- ロボットビジョン一体型ロボットの分析(出荷台数ベース)

- 産業用ロボット

- モバイルロボット

第5章 市場力学

- 市場促進要因

- 認知ヒューマノイドロボットの採用増加

- 自動車産業などのエンドユーザーからの需要拡大

- 市場抑制要因

- 高額投資

第6章 市場セグメンテーション

- 技術別

- 2Dビジョン

- 3Dビジョン

- エンドユーザー産業別

- 自動車

- エレクトロニクス

- 航空宇宙

- 飲食品

- 製薬

- その他エンドユーザー産業

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Qualcomm Technologies, Inc.

- Keyence Corporation

- FANUC Corporation

- ABB Group

- Sick AG

- Teledyne Dalsa Inc.

- Cognex Corporation

- Omron Adept Technology, Inc.

- National Instruments Corporation

- Hexagon AB

第8章 投資分析

第9章 市場の将来

目次

Product Code: 69651

The Robotic Vision Market is expected to register a CAGR of 9.86% during the forecast period.

Key Highlights

- Machine guidance systems use 2D and 3D machine vision systems to improve the accuracy and speed of assembly robots and automated material handling equipment, which plays a crucial role in the engine chassis marriage operations. Although the applications vary depending on the vehicle or model being produced, the general categories of applications are observed in robotics, dimensional gaging functions, assembly verification, flaw detection, paint job verification, and code reading.

- Robotic vision provides the robots with a sight that helps them to complement or replace manual inspection tasks using cameras and image processing. The applications range from basic tasks, like presence detection, to real-time inspection.

- Manufacturing companies across the globe realize the benefits of these robotic vision systems, particularly in areas where redundant tasks, like inspection, should be performed with precision. They play an essential role in high-speed production lines and hazardous environments. These systems' significant benefits include increased productivity, reduced machine downtime, and tighter process control.

- Significant expenditures are required to develop the core components of robotic vision, such as vision sensors and the underlying vision software. The initial cost of implementing robotic vision is also slightly more significant, which may impede market expansion.

- The COVID-19 pandemic is expected to increase the growth of vision-guided robots that can reduce human contact in multiple end-user industries. For instance, Orrbec, a US-based company, collaborated with robot manufacturers in China to deploy its 3D camera products in robots for different hospital applications. Food delivery robots, sterilization robots, and directional guiding robots using machine vision systems have been deployed across many hospitals in China. With the increased adoption of cognitive humanoid robots, the market is proliferating after the pandemic.

Robotic Vision Market Trends

Growing Demand from End-User Segments like Automotive Industry Drives the Market Growth

- To address quality issues, Automotive manufacturers are increasingly investing in vision systems. The technology is increasingly being used by automakers and parts suppliers for various applications, including adhesive dispensing, bin picking, error-proofing, inline welding analysis, material handling, robotic guidance, surface inspection, and traceability. Growing demand for customization, increasing labor shortages, and cost pressures are some significant drivers of vision systems used in the auto industry.

- Vision-guided robots are projected to revolutionize the electronics, automotive, and food processing industries. Due to the tremendous technology demand for applications such as arc welding, cutting, and palletizing, these industries are dominated by 3D vision-guided technology.

- Advanced machine vision technology plays a significant role in the daily operation of various global automotive plants. Ford Motor Co.'s Van Dyke transmission plant, for instance, uses vision-guided robots to ensure the high-quality assembly of critical components like gears and clutches. The plant has deployed over 500 inline machine vision applications for error-proofing, gauging, and complexity issues.

- With the growth of the ADAS system in Automotives, the requirement of components like camera-led lighting, Lidar, and V2X, among others, would play a crucial role shortly for automation and intelligence. Further, according to Neuromation, traffic accidents account for 2.2% of global deaths. With 2D and 3D machine vision and intelligent transportation systems (ITS), drivers are provided with a safety net. These technologies make it possible to mitigate human error in the auto industry, assisting drivers at the wheel with tools and features that keep them from committing severe mistakes and accidents.

- Because of their noncontact inspection, high repeatability, and minimal cost, robotic vision systems are becoming more popular for quality control in various sectors. Traditional methods of product quality control rely entirely on human inspection. On the other hand, human inspection performance is projected to decline over a shift of work owing to weariness and repetition. Minor faults may go unnoticed, resulting in non-trivial errors. Technological breakthroughs are transferring the time-consuming inspection labor from humans to machine automation. Significant advances in hardware and software have already shifted most of the quality control inspection labor to machines in various regions of the globe. According to IFR, With approximately 168 thousand new industrial robot installations in China, it had set up the most robotics-worldwide in the previous year.

North America is Expected to become the Fastest Growing Market

- In robotics adoption, North America is one of the significant inventors and pioneers and one of the world's largest markets. The rising deployment of robotics across various sectors is the key driver of the market's growth.

- According to the International Federation of Robotics, North American industrial robot deployments are predicted to reach 69,000 annually by the current year. According to Advancing Automation, the number of robots sold last year was estimated to rise by 28% over before previous year. As more sectors resorted to automation to enhance productivity and reduce persistent labor shortages, record robot sales were recorded in the fourth quarter of the last year (up by 9% from the fourth quarter of before earlier year), demonstrating strong momentum already gained in the previous few months.

- Industrial robots are critical in industrial automation, with various robots managing many vital functions in multiple industries. Electronics, e-commerce, and automotive industries, among others, are growing in tandem with economic expansion in many countries in this region. Product manufacturers are rapidly employing robots to automate repetitive procedures in response to rising demand across economies.

- Machine vision systems would be produced more frequently due to government efforts such as the Advanced Manufacturing Partnership, which aims to encourage businesses, universities, and the federal government to invest in future automation technology.

- According to the MAPI (Manufacturers Alliance for Productivity and Innovation), industrial production in the United States was estimated to rise by 2.8% by the earlier year, boosting the country's use of robotic vision technologies.

Robotic Vision Industry Overview

The robotic vision market is moderately fragmented due to major players like Qualcomm Technologies, Inc., Keyence Corporation, FANUC Corporation, ABB Group, and Sick AG. Players in the market are adopting strategies such as partnerships, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2022 - ABB announced a strategic partnership with the US-based startup Scalable Robotics to expand its user-friendly robotic welding solutions line. Scalable Robotics technology, which uses 3D vision and embedded process awareness, enables users to program welding robots without coding.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Covid-19 on the Industry

- 4.5 Analysis of Robots Integrated with Robotic Vision (in terms of Volumes Shipped)

- 4.5.1 Industrial Robots

- 4.5.2 Mobile Robots

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Adoption of Cognitive Humanoid Robots

- 5.1.2 Growing Demand from End - User Segments like Automotive Industry

- 5.2 Market Restraints

- 5.2.1 High Investments

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 2D Vision

- 6.1.2 3D Vision

- 6.2 By End User Industry

- 6.2.1 Automotive

- 6.2.2 Electronics

- 6.2.3 Aerospace

- 6.2.4 Food and Beverage

- 6.2.5 Pharmaceutical

- 6.2.6 Other End User Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Technologies, Inc.

- 7.1.2 Keyence Corporation

- 7.1.3 FANUC Corporation

- 7.1.4 ABB Group

- 7.1.5 Sick AG

- 7.1.6 Teledyne Dalsa Inc.

- 7.1.7 Cognex Corporation

- 7.1.8 Omron Adept Technology, Inc.

- 7.1.9 National Instruments Corporation

- 7.1.10 Hexagon AB