|

市場調査レポート

商品コード

1910822

プロセス計装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Process Instrumentation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| プロセス計装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

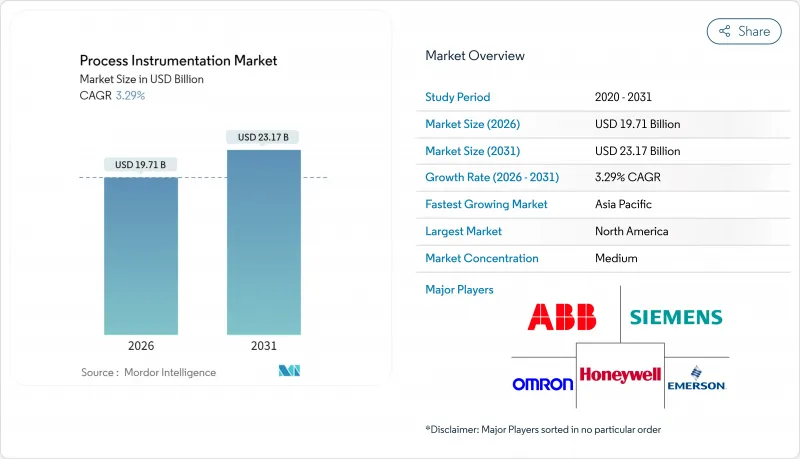

プロセス計装市場は2025年に190億8,000万米ドルと評価され、2026年の197億1,000万米ドルから2031年までに231億7,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは3.29%と見込まれます。

この緩やかな成長軌道は、デジタル化、脱炭素化の義務化、改修サイクルが交換需要を強化しているにもかかわらず、顧客基盤が成熟化していることを反映しています。サプライヤーはハードウェア、ソフトウェア、サービスを統合したソリューションを提供し続け、ライフサイクルコストの削減と排出量監視のコンプライアンス支援を実現しています。老朽化したプラントにおける改修プログラム、シングルペアイーサネットの導入、労働力不足が相まって、既存設備のアップグレード需要を安定的に支えています。同時に、グリーン水素および水再利用プロジェクトが新規需要を創出し、プロセス計装市場に対する堅調な需要見通しを支えています。顧客が測定精度、サイバーセキュリティ認証、サービス対応力を優先するため価格競争は限定的であり、ベンダーはデジタル技術を活用した差別化要素により利益率を維持することが可能です。

世界のプロセス計装市場の動向と洞察

脱炭素化に連動したプロセス最適化の要請

欧州連合の炭素国境調整メカニズム(CBAM)などの炭素削減規制により、継続的な排出量監視とエネルギー効率測定が中核的な運用指標として位置づけられています。プラントでは現在、高精度センシングと安全なデータパイプラインを組み合わせた計装機器が指定され、IEC 62443-2-1:2024サイバーセキュリティプログラム規格に基づく監査対応レポートの生成が可能となっています。化学、精製、セメント産業における需要が最も高く、リアルタイム分析により燃料消費量の削減とスコープ1およびスコープ2の排出量目標達成が図られています。これに対し、サプライヤーは自己診断機能、エッジベース検証、暗号化クラウド接続を統合したスマート分析装置を提供。コンプライアンス対応を、エネルギーコスト削減や炭素税負担軽減という測定可能な収益に変換します。こうした規制により、仕様要求は基本精度を超え、データ完全性とトレーサビリティまで拡大。プロセス計装市場全体でプレミアム価格設定が強化されています。

老朽化プラントにおける爆発検知器の改修サイクル

1980年代から1990年代に建設された施設では、校正費用の増加と予期せぬダウンタイムに直面しています。資産寿命延長プロジェクトでは、センサーの改修とデジタル化を同時に実施し、従来のトランスミッターをスマートモデルに置き換えることで、多変量データと予知診断機能を実現しています。エンドレスハウザーのコンパクトなステンレス製計装機器は、現代的な形状設計がCIP洗浄に耐え、デッドレッグの蓄積を最小限に抑えることで、プロセス停止を伴わないメンテナンスを可能にする好例です。プラント管理者は、最大20%のメンテナンスコスト削減と安全インシデントの減少を実証しており、これにより短期間での投資回収が可能となり、発注サイクルが加速しています。設置済みデバイスの60%以上が依然としてアナログ4-20mAループで稼働しているため、レトロフィットプログラムはプロセス計装市場における複数年にわたる成長エンジンであり続けています。

スマートトランスミッター向けチップ供給のボトルネック

産業用マイクロプロセッサは依然として割り当て制の対象となっており、HARTおよびイーサネット対応トランスミッタのリードタイムは2025年までに最大32週間に延長される見込みです。ベンダー各社は代替部品を用いた基板の再設計を進めていますが、12~18カ月にも及ぶ認定サイクルにより量産回復は遅延しています。アジア太平洋地域の化学プラント複合施設におけるプロジェクトでは、緊急輸送や直前の設計変更により、最大150万米ドルのコスト超過が発生した事例が報告されています。この不足は、特殊なA/Dコンバーターを必要とする多変量分析装置に特に深刻な影響を与え、出荷の遅延やプロセス計装市場の短期的な勢いの鈍化を招いています。

セグメント分析

2025年時点で、トランスミッタはプロセス計装市場規模の37.62%を占め、レベル・圧力・温度制御ループの中核としての役割を確固たるものにしております。診断機能、サイバーセキュリティ対応ファームウェア、ホットスワップモジュラー性の継続的改善が、既存設備基盤を保護しております。ベンダー各社は現在、高度なドリフト補償アルゴリズムを組み込み、校正サイクルを年次から3年に1回へと延長し、24時間365日稼働における稼働時間を維持しております。マグネトロル社のジュピターJM4のような現場交換可能なヘッド設計により、プラントはプロセスシールを破ることなく電子部品を交換可能となり、保守作業とベントリスクを低減します。予測期間中、トランスミッタは安定した収益源であり続け、排出量測定規制の強化による需要増加が見込まれます。

分析機器は年平均CAGR3.62%で拡大し、リアルタイム分光分析、溶存酸素検知、多項目ガス分析を計測ツールキットに追加します。その台頭は、単純な状態監視から能動的なプロセス最適化への移行を反映しています。モジュラープラットフォームにより、単一シャーシで光学式、電気化学式、質量分析式カートリッジの装着が可能となり、設置面積の削減と予備部品在庫の最小化を実現します。分析機器の普及拡大は、追加のソフトウェアライセンシングやクラウドゲートウェイの機会をもたらし、ポイントあたりの生涯収益を高めます。この動きがプロセス計測機器市場全体の持続的成長を支えています。

PLC(プログラマブルロジックコントローラ)は、確定的なスキャン時間、フェイルセーフ冗長性、汎用的なサービスノウハウが評価され、2025年のプロセス計装市場で34.02%のシェアを占めました。アップグレードの焦点は、セキュアブートローディング、冗長ギガビットバックプレーン、上流データ共有を簡素化する組み込みOPC UAサーバーにあります。水素電解装置スキッドや水リサイクルモジュールにおけるコントローラの採用拡大が、PLCの出荷台数の安定性を強化しています。

製造実行システム(MES)は、生産スケジューリング、電子バッチ記録、リアルタイム品質分析を一元管理する「シングルペイン・オブ・グラス」を求める施設が増加し、3.76%という最高成長率(CAGR)で拡大しています。エマソンのDeltaV Edge 2.0は、コンテキスト化されたヒストリアンデータをノースバウンドで伝送可能とし、コントローラを双方向トラフィックに晒すことなくITセキュリティ監査を容易にします。MESと高度なプロセス制御の融合により意思決定の遅延が短縮され、センサーインテリジェンスが省エネルギーとスループット向上に転換されます。これによりプロセス計装市場全体で投資収益率が守られます。

地域別分析

2025年、北米はプロセス計装市場において29.12%のシェアを占めました。同地域では環境保護庁(EPA)の規制により、排出物と水質の継続的モニタリングが義務付けられており、これがレガシーアナログループの加速的な更新を促進しています。米国公益事業会社は、パーフルオロアルキル物質およびポリフルオロアルキル物質に対する厳格な規制基準への適合のため、スマートトランスミッターへの投資を進めています。一方、カナダのオイルサンド事業者は、研磨性スラリーに耐える多変量流量計を導入しています。国境を越えたサプライチェーンと現地サービスネットワークがアフターマーケットの回復力を強化し、ベンダーにとって高いスペアパーツ付帯率と安定したサービス収益を確保しています。

アジア太平洋地域は最も成長が著しい地域であり、2031年までの年間平均成長率(CAGR)は3.81%と予測されています。これは、急速な工業化、グリーン水素電解装置の導入、中国・インド・東南アジアにおける製造業の回帰(リショアリング)が主な要因です。中国の化学産業拠点では揮発性有機化合物の管理に高周波レーダー式レベル計が活用され、インドの製薬クラスターでは米国FDA輸出要件を満たすため分光法を活用したPATフレームワークが導入されています。日本と韓国の半導体工場向け政府支援策は、超純水計装機器やサブppm級ガス分析装置の需要を促進しています。新規設備投資の広がりにより、アジア太平洋地域はプロセス計装市場において現地生産・サポートセンターを拡大する世界のベンダーにとって優先地域となっています。

欧州は脱炭素化法規制とインダストリー4.0導入により安定した成長を維持しております。ドイツの特殊化学品複合施設では、ATEXとIEC 62443の双方の要求を満たす統合安全・サイバーセキュリティ認証を活用し、イーサネットAPLフィールドネットワークへのアップグレードが進められております。英国では排出規制強化に対応するため、アンモニアスリップ監視システムによる水道事業近代化が推進され、フランスでは冗長性クラス伝送器を必要とする水素電解装置実証プラントへの投資が行われております。大陸全体では、各国の復興基金が効率化アップグレードに資本を投入し、経済的な逆風にもかかわらずベースライン需要を保護しています。中東・アフリカ地域では、石油化学統合プロジェクト、海水淡水化プラント、鉱業拡張が計装機器の受注を刺激し、プロセス計装市場における世界と地域プレイヤーの事業範囲を拡大する成長隣接領域を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場環境

- 市場概要

- 市場促進要因

- 脱炭素化に関連するプロセス最適化の義務化

- 老朽化プラントにおける爆発検知器の改修サイクル

- イーサネット-APLシングルペアイーサネットの展開

- バンドル型O&M契約(計器サービスとしての提供)

- コロナ禍後の労働力不足が無人自動化を推進

- グリーン水素メガプロジェクトが計測機器需要を牽引

- 市場抑制要因

- スマートトランスミッター向けチップ供給のボトルネック

- マルチプロトコルレガシーのロックインコスト

- 校正ラボの容量不足

- IIoT接続におけるサイバーセキュリティ保険の割増料金

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場におけるマクロ経済動向の評価

第5章 市場規模と成長予測

- 機器別

- 送信機

- レベルトランスミッター

- 温度トランスミッター

- 圧力トランスミッター

- 制御弁

- 分析機器

- フィールドコントローラー(RTU/PLC)

- プロセス分析装置

- ガス分析装置

- 液体分析装置

- その他の機器

- 送信機

- 技術別

- 分散制御システム(DCS)

- プログラマブルロジックコントローラ(PLC)

- 監視制御およびデータ収集(SCADA)

- 製造実行システム(MES)

- その他の制御技術

- エンドユーザー産業別

- 水処理・廃水処理

- 石油・ガス採掘

- 化学製造業

- エネルギー・公益事業

- 医薬品

- 金属・鉱業

- 食品・飲料

- 紙・パルプ

- その他のプロセス産業

- 測定パラメータ別

- フロー

- 圧力

- レベル

- 気温

- 湿度

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- シンガポール

- 韓国

- オーストラリア

- その他アジア太平洋

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Endress+Hauser AG

- Yokogawa Electric Corporation

- Emerson Electric Co.

- ABB Ltd.

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation Inc.

- Azbil Corporation

- KROHNE Messtechnik GmbH

- Pepperl+Fuchs SE

- Brooks Instrument LLC

- Mettler-Toledo International Inc.

- Badger Meter Inc.

- Spirax-Sarco Engineering plc

- AMETEK Inc.(Process Instruments)

- Omron Corporation

- Valmet Flow Control Oy

- HIMA Paul Hildebrandt GmbH

- Omega Engineering Inc.

- Samson AG