|

市場調査レポート

商品コード

1642156

オールフラッシュアレイ:市場シェア分析、産業動向、成長予測(2025~2030年)All Flash Array - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オールフラッシュアレイ:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

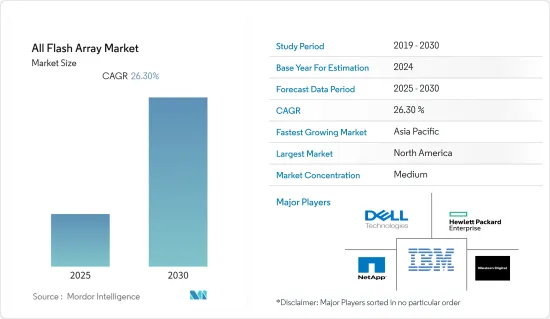

オールフラッシュアレイ市場は予測期間中にCAGR 26.3%を記録する見込みです。

主なハイライト

- 企業で生成されるデータの増加は、クラウド技術の採用増加と相まって市場を牽引すると予測されます。さらに、ビッグデータおよびアナリティクスに伴い、データアクセスおよび処理パターンには、より高いストレージ性能と並行性の向上が求められる(ビッグデータはデータモビリティ問題を悪化させる)。

- フラッシュ・ストレージの採用は主に、消費電力、性能の向上、メンテナンスの容易さなど、その有用性に依存しており、これが採用率を高めています。さらに、リアルタイム分析や要求の厳しいデータベースシステムを含むミッションクリティカルなアプリケーションは、フラッシュストレージシステムで容易に実現できます。

- SCMは、オールフラッシュアレイのキャッシング・レイヤーとして導入される可能性が高いです。これらの新しい進化は、ストレージコストを削減しながら、ワークロードのパフォーマンスを最適化することが期待されます。

- さらに、NVMe(Non-Volatile Memory Express)などの改良により、従来のプロトコルよりも高速なパフォーマンスと高密度を実現できるようになり、エンタープライズ向けオールフラッシュ・ストレージ業界は拡大しています。

- インドのような地域では、2022年にかけてヘルスケア、保険、通信の各業界からエンタープライズ向けフラッシュストレージのプラス成長が見込まれています。インドの成長は主にIoT、AI、ビッグデータ革新によるものです。組織は自動化技術と消費ベースの価格設定に期待しています。

オールフラッシュアレイ(AFA)市場動向

データセンターが大きなシェアを占める見込み

- 増大するデータセンターのワークロードは、ハードディスクドライブ(HDD)では対応が非常に困難な新たなストレージ性能要件を生み出します。永続的ストレージ技術としてフラッシュを使用することで、こうした課題が解決されます。

- NASSCOMによると、インドのデータセンター市場への投資額は2025年までに46億米ドルに達すると予想されています。主な理由は、インドのインターネット利用の拡大、クラウドコンピューティング需要の増加、政府によるデジタル化への取り組み、デジタルサービスプロバイダーによるローカライゼーションです。インドの開発・運用におけるコスト効率の高さは、より成熟した市場と比較して最大の利点です。

- さらに、CloudSceneによると、110カ国の情報が入手可能な2021年時点で、世界には約8,000のデータセンターが存在します。このうち、米国(全体の33%)、英国(5.7%)、ドイツ(5.5%)、中国(5.2%)、カナダ(3.3%)、オランダ(3.4%)の6カ国がデータセンターの過半数を占めています。

- WSTSによると、2021年のメモリ部品販売による売上高は約1,538億米ドルで、2020年に記録した1,175億米ドルから増加し、約31%の増収を示しています。

北米が主要市場シェアを占める見込み

- 複数の製品が発売されていることから、北米が大きな市場シェアを占めていることがうかがえます。さらに、米国は、Dell Inc.、IBM Corporation、Net App Inc.など、同市場の他の著名なプレイヤーの本社として機能しています。オールフラッシュアレイの採用は、ビッグデータおよび関連アプリケーションへの支出増に後押しされ、この地域の成長を高めています。

- この地域は、データセンターの数が最も多く、ヘルスケア、IT、BFSI、小売、メディア産業が急成長しているため、オールフラッシュアレイ市場で大きなシェアを占めています。Cloudsceneによると、米国とカナダのデータセンター数は3029で世界最多であり、オールフラッシュアレイ市場の需要を牽引すると期待されています。

- 北米は、著名な情報技術産業や主要ベンダー企業の存在により、ITインフラに多額の投資を行っています。この地域はBFSI産業が盛んであり、組織は顧客のニーズに応えるためにITインフラに支出する用意があります。

- この地域はまた、クラウド・ソリューションに対する世界の支出も大きいです。経済戦略研究所(ESI)によると、米国経済はクラウド・サービス(クラウド・コンピューティング、データ分析、モノのインターネット)に対する企業の支出から恩恵を受ける。2025年までに1兆7,000億米ドルの新規支出、GDPへの3兆米ドルの追加、米国経済への800万人の雇用創出が見込まれています。

オールフラッシュアレイ(AFA)産業の概要

オールフラッシュアレイ市場は、多くの地域および世界プレーヤーが存在し、競争は中程度です。製品提供の革新が市場を牽引し、各ベンダーは技術革新に投資しています。主なプレーヤーは、Dell Technologies、Western Digital Corporation、Hewlett Packard Enterprise、NetApp Inc.、IBM Corporationなど。

- 2022年2月-IBMは、ランサムウェアやその他のサイバー攻撃の検出と迅速な復旧をサポートするIBM FlashSystem Cyber Vaultを発表しました。さらに、IBM Spectrum VirtualizeをベースとしたFlashSystemストレージの新モデルを発表し、ハイブリッド・クラウド環境におけるサイバー耐障害性とアプリケーション・パフォーマンスの向上を目的とした、単一で一貫性のある運用環境を提供。

- 2022年3月- ネットアップとシスコは、FlexPod XCSのイントロダクションよりFlexPodを進化させ、最新のアプリケーション、データ、ハイブリッドクラウドサービスに対応する1つの自動化プラットフォームを提供すると発表しました。FlexPodは、CiscoとNetAppが事前に検証したストレージ、ネットワーク、サーバのテクノロジで構成されています。さらに、新しいFlexPod XCSプラットフォームは、ハイブリッド・クラウド環境における最新のアプリケーションとデータの提供を加速するように設計されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- オールフラッシュアレイを選択するための前提条件/考慮事項

- COVID-19が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- データセンター数の増加

- 管理とメンテナンスの容易さ

- 市場抑制要因

- 初期コスト

- 書き込みサイクルの低下

第6章 市場セグメンテーション

- タイプ別

- 従来型

- カスタム

- エンドユーザー用途別

- IT・通信業界

- BFSI

- ヘルスケア

- 政府機関

- その他のエンドユーザー用途

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- その他アジア太平洋地域

- 世界のその他の地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Silk Platform

- Dell Inc.

- Hewlett Packard Enterprise Development LP

- NetApp Inc.

- Violin Systems LLC

- IBM Corporation

- Fujitsu Ltd.

- Pure Storage, Inc.

- Western Digital Corporation

- Huawei Technologies Co., Ltd.

第8章 投資分析

第9章 市場の将来

目次

Product Code: 66997

The All Flash Array Market is expected to register a CAGR of 26.3% during the forecast period.

Key Highlights

- The gain in data generated by the enterprise, coupled with the increasing adoption of cloud technology, is anticipated to drive the market. Moreover, with big data and analytics, data access and processing patterns demand a higher storage performance and improved concurrency (Big Data aggravates the data mobility issues).

- Flash storage adoption mainly depends on its usefulness, such as power consumption, improving performance, and ease of maintenance, which have raised the adoption rate. Moreover, mission-critical applications, including real-time analytics and demanding database systems, can be achieved easily with flash storage systems.

- SCMs will likely be deployed as a caching layer for an all-flash array. These new evolutions are expected to provide optimized workload performance while decreasing storage costs.

- Furthermore, improvements such as Non-Volatile Memory Express (NVMe) have increased the enterprise all-flash storage industry, allowing faster performance and more density than conventional protocols.

- Territories like India anticipate positive growth for enterprise flash storage from healthcare, insurance, and telecommunications verticals across 2022. India's growth is primarily due to IoT, AI, and big data innovation. Organizations are looking ahead to automation technologies and consumption-based pricing.

All-flash Array (AFA) Market Trends

Data centers is Expected to Hold Significant Share

- Growing data center workloads create new storage performance requirements that are very difficult to address with hard disk drives (HDDs). Using flash as a persistent storage technology resolves these challenges.

- According to NASSCOM, India's data center market investment is expected to reach USD 4.6 billion by 2025, mainly due to India's growing internet usage, increased cloud computing demands, digitalization initiatives by the government, and localization by digital service providers. India's higher cost efficiency in development and operation is its biggest advantage compared to more mature markets.

- Moreover, as per CloudScene, with 110 countries' available information, as of 2021, there were around 8,000 data centers globally. Among these, six countries hold a majority of data centers: the United States (33% of total), the UK (5.7%), Germany (5.5%), China (5.2%), Canada (3.3%), and the Netherlands (3.4%).

- According to WSTS, in 2021, revenue from memory component sales was about USD 153.8 billion, an increase from the USD 117.5 billion in revenue recorded in 2020, which shows an approximately 31% increase in revenue.

North America is Expected to Hold Major Market Share

- Multiple product launches suggest that North America holds a significant market share. Moreover, the United States acts as headquarters for other prominent players in the market, such as Dell Inc., IBM Corporation, Net App Inc., etc. Adopting the all-flash array enhances the growth of this region, fueled by increased expenditures in big data and related applications.

- The region holds a significant share of the all-flash array market due to the presence of the highest number of data centers and booming healthcare, information technology, BFSI, retail, and media industries. According to Cloudscene, the number of data centers in the US and Canada is 3029, the highest in the world, and expected to drive the demand for the all-flash array market.

- North America spends a significant amount on IT infrastructure, owing to the presence of prominent information technology industry and key vendors' companies. The region is home to a thriving BFSI industry where organizations are ready to spend on IT infrastructure to cater to the needs of their customers.

- The region also accounts for significant global spending on cloud solutions. According to Economic Strategy Institute (ESI), the US economy will benefit from corporation spending on cloud services (cloud computing, data analysis, and the Internet of Things). It is expected to contribute USD 1.7 trillion in new spending, add USD 3 trillion to GDP, and create 8 million jobs for the US economy by 2025.

All-flash Array (AFA) Industry Overview

The All Flash Array Market is moderately competitive, with many regional and global players. Innovation drives the market in product offerings, and each vendor invests in innovation. Key players include Dell Technologies, Western Digital Corporation, Hewlett Packard Enterprise, NetApp Inc., and IBM Corporation.

- February 2022 - IBM introduced IBM FlashSystem Cyber Vault to support companies in better detecting and recovering quickly from ransomware and other cyberattacks. In addition, the company also revealed new FlashSystem storage models, based on IBM Spectrum Virtualize, to deliver a single and consistent operating environment designed to improve cyber resilience and application performance within a hybrid cloud environment.

- March 2022 - NetApp and Cisco announced the evolution of FlexPod with the introduction of FlexPod XCS, providing one automated platform for modern applications, data, and hybrid cloud services. FlexPod comprises pre-validated storage, networking, and server technologies from Cisco and NetApp. Moreover, the new FlexPod XCS platform is designed to accelerate the delivery of modern applications and data in a hybrid cloud environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Industry Attractiveness - Porter's Five Force Analysis

- 4.1.1 Bargaining Power of Suppliers

- 4.1.2 Bargaining Power of Consumers

- 4.1.3 Threat of New Entrants

- 4.1.4 Intensity of Competitive Rivalry

- 4.1.5 Threat of Substitute Products

- 4.2 Pre-requisites/Consideration for choosing All-Flash Array

- 4.3 Assessment of covid -19 impact on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Centers

- 5.1.2 Ease of Management and Maintenance

- 5.2 Market Restraints

- 5.2.1 Initial Cost Involved

- 5.2.2 Lower Write Cycles

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Traditional

- 6.1.2 Custom

- 6.2 By End-User Application

- 6.2.1 IT and Telecom Industry

- 6.2.2 BFSI

- 6.2.3 Healthcare

- 6.2.4 Government

- 6.2.5 Other End-User Applications

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 South Korea

- 6.3.3.4 India

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle-East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Silk Platform

- 7.1.2 Dell Inc.

- 7.1.3 Hewlett Packard Enterprise Development LP

- 7.1.4 NetApp Inc.

- 7.1.5 Violin Systems LLC

- 7.1.6 IBM Corporation

- 7.1.7 Fujitsu Ltd.

- 7.1.8 Pure Storage, Inc.

- 7.1.9 Western Digital Corporation

- 7.1.10 Huawei Technologies Co., Ltd.