|

|

市場調査レポート

商品コード

1642123

ハイパーコンバージドインフラストラクチャ:市場シェア分析、産業動向、成長予測(2025年~2030年)Hyper-Converged Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ハイパーコンバージドインフラストラクチャ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

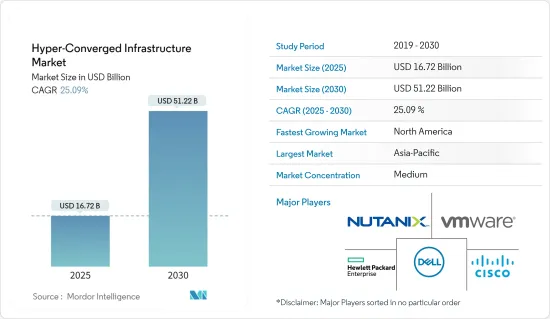

ハイパーコンバージドインフラストラクチャの市場規模は、2025年に167億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは25.09%で、2030年には512億2,000万米ドルに達すると予測されます。

主なハイライト

- ハイパーコンバージェンスインフラ(HCI)は、IT業界を変革するソリューションとして登場し、企業のデータセンター管理方法に革命をもたらしています。HCI市場は、企業がインフラの合理化、運用効率の向上、デジタルトランスフォーメーションの導入を目指す中で、著しい成長と普及を遂げています。

- ハイパーコンバージドインフラ市場の主な促進要因となっているのが、クラウドコンピューティングの採用拡大です。さまざまな業界の企業が、その拡張性、コスト効率、柔軟性を活用するため、ワークロードをクラウドに移行しています。HCIソリューションは、オンプレミスとクラウドのリソースをシームレスに統合することで、クラウド環境を補完します。HCIを利用することで、企業はプライベートクラウドとパブリッククラウド間でワークロードを容易に移行でき、両環境の利点を組み合わせたハイブリッドクラウドの展開が可能になります。このようなHCIとクラウド・コンピューティングの相乗効果が市場の成長を加速させており、今後もハイパーコンバージドインフラストラクチャ・ソリューションの需要を牽引していくと予想されます。

- データセンターの仮想化と統合は、ITインフラの最適化と運用コストの削減を目指す組織にとって不可欠なものとなっています。ハイパーコンバージドインフラストラクチャは、データセンター管理への統合アプローチを提供し、企業が複数のコンポーネントを単一の統合システムにまとめることを可能にします。仮想化技術を活用することで、HCIはコンピューティング・リソースの効率的な割り当てと利用を可能にし、パフォーマンスの向上とハードウェア・フットプリントの削減につながります。HCIが提供する拡張性と柔軟性は、データセンターの統合と仮想化構想にとって理想的なソリューションとなっています。その結果、ハイパーコンバージドインフラ市場は、効率的なデータセンター運用の需要に後押しされて大幅な成長を遂げています。

- ハイパーコンバージドインフラストラクチャの世界市場は、ITインフラストラクチャの効率化につながるさまざまなアプリケーションにより、需要が増加しています。この需要の急増は、ハイパーコンバージドインフラストラクチャシステムが、スナップショット、レプリケーション、暗号化などの機能を提供し、オンプレミスのデータセンター内のデータを保護する能力によって促進されています。その結果、さまざまな分野の組織がこうしたソリューションを求めています。

- しかし、HCIソリューションを導入するための初期投資コストが高いことが、市場の足かせとなっています。HCIは、管理の簡素化、スケーラビリティの向上、運用コストの削減など数多くのメリットを提供する一方で、これらのソリューションの導入に必要な初期投資は多額になります。特に、IT予算が限られている中小企業(SME)にとっては、ハードウェア、ソフトウェア・ライセンス、プロフェッショナル・サービスにかかるコスト負担が大きいです。初期投資コストの高さが導入の障壁となり、市場の成長を妨げています。しかし、市場が成熟し、技術が進歩するにつれて、HCIソリューションのコストは低下し、より広範な組織がHCIソリューションにアクセスできるようになると予想されます。

- COVID-19の大流行は、業界全体のデジタルトランスフォーメーションの取り組みを大幅に加速させました。世界中の組織が、リモートワーク、オンラインコラボレーション、デジタルサービスをサポートするための俊敏で弾力性のあるITインフラの重要性に気づいた。ハイパーコンバージドインフラは、拡張性と柔軟性に優れたインフラ基盤を提供することで、こうした変革を可能にしました。パンデミック(世界的大流行)は、企業が俊敏性と適応性を備える必要性を浮き彫りにし、HCIソリューションの採用拡大につながりました。その結果、COVID-19後の時代は、企業がデジタル能力を強化するテクノロジーへの投資を継続することで、ハイパーコンバージドインフラストラクチャ市場がさらに活性化すると予想されます。

ハイパーコンバージドインフラストラクチャ市場の動向

データ保護強化へのニーズの高まりが市場成長を牽引

- 今日の組織は、信頼性が高く高性能なストレージに対するニーズが高まっています。ハイパーコンバージドインフラ(HCI)は、ネットワーキング、ストレージ、コンピューティングを単一のシステムに統合することで、安全かつ効率的なソリューションを提供します。このリソースの統合は、管理を合理化し、コストを削減し、多くの企業にとって戦略的IT優先事項にとって極めて重要であると考えられています。

- HCI市場は、特にデータ・セキュリティやディザスタ・リカバリなどの分野でHCIソリューションの採用が増加していることから拡大しています。ソーシャルメディアやナレッジ・プラットフォームのようなデジタル技術プラットフォームの普及も、HCIの需要拡大に寄与しています。IBM Data Breachの最新レポートによると、データ漏洩の平均コストは2.6%増の435万米ドル(罰則を含む)です。HCIシステムは、そのコンポーネントとアプリケーションを通じてデータ・セキュリティ侵害のリスクを軽減し、多くの場合、セキュリティ機能を備えた高セキュリティのAMDプロセッサを組み込んでいます。

- さらに、HCIは従来のストレージ・ソリューションに比べてデータ・セキュリティと拡張性が向上しています。コネクテッド・デバイスとモノのインターネット(IoT)の数が増加し続ける中、集中管理システムにアナリティクスを収集・保存するHCIの機能は、ますます価値が高まっています。この機能は、HCIが統一されたインターフェイスを通じて収集したデータを表示する能力が有利であることを証明する5Gネットワークの将来とよく一致しています。GSMAによると、5G接続は今年10億を突破し、2025年には20億に達する見込みで、HCI市場をさらに牽引します。

- HCIは、パブリック・クラウド・ベースのサービスと同様に、仮想ワークロード向けに最適化されており、柔軟で消費ベースのインフラ経済性を提供します。企業は、HCIビルディングブロックを追加することで、リソースを迅速に拡張することができ、ビジネスの需要に迅速に対応し、ITサービスの俊敏性を高めることができます。集中管理、計算、ストレージ、データ・セキュリティといったクラウド・コンピューティングに不可欠なサービスをハイパーコンバージドシステムに組み込むことで、HCIは包括的なソリューションとなります。

- 自動化と機械学習は、アプリケーション・パフォーマンスの向上と大量のデータ処理を可能にし、企業の生産性を高めるものとして広く認知されています。HCIはAIを活用してワークロードの需要に対応し、アプリケーションのワークロードを最適化し、ストレージを最適化します。オンプレミスのプライベート・クラウド、パブリック・クラウド、既存のデータセンター・インフラ間のギャップを埋めることで、ハイブリッド・マルチクラウド・モデルにおけるHCIは、企業がエンドツーエンドのデータ・ワークフローを管理し、AIアプリケーションのためのデータへの容易なアクセスを確保することを可能にします。前年の人工知能指数(Artificial Intelligence Index)レポートでも強調されているように、AIに対する企業の投資の増加もHCI市場を牽引しており、昨年の世界投資額は約940億米ドルに達し、前年の678億5,000万米ドルから大幅に増加しました。

北米が最速の成長を記録する見込み

- 北米におけるHCI市場の成長を牽引しているのは、主に同地域におけるハイパースケールクラウドサービスプロバイダーの拡大です。また、コロケーションサービスもホールセールとリテールの両分野で成長を遂げています。モバイルデータ利用の増加やBYOD(Bring-Your-Own-Device)規制の導入により、仮想デスクトップをサポートするインフラに対する需要が高まっています。その結果、北米ではHCIの市場シェアが拡大すると予想されます。

- 複数のデータセンター企業が、ハイパースケールデータセンターに大規模な投資を行っています。例えばエクイニクスは、世界の主要市場に32のハイパースケールデータセンターを建設する計画を発表しています。69億米ドル超の巨額投資と600メガワットの総容量により、エクイニクスはそのプレゼンスを拡大し、成長するハイパースケールデータセンターの状況を活用することを目指しています。地域データセンターの増加は、HCI市場をさらに牽引すると思われます。

- パートナーシップや提携も北米のHCI市場を形成しています。例えば、レノボとキンドリルは、スケーラブルなハイブリッドコンピューティングや高度なコンピューティングの実装、クラウドソリューションの開発・提供に向けて協業を拡大しました。LenovoのPC、ストレージ、サーバー性能に関する専門知識とKyndrylのITインフラ・サービスを活用することで、このパートナーシップは、ハイブリッド・クラウド、HCI、高度なコンピューティング・アプリケーションにわたる包括的なソリューションを顧客に提供することを目指しています。

- さらに、企業におけるHCI導入の急増により、ソフトウェア定義ストレージに対する需要が高まっています。この動向に対応するため、DataCore SoftwareはオブジェクトストレージのスペシャリストであるCaringo Inc.を買収しました。この買収により、DataCore Softwareはブロック、ファイル、オブジェクトの統合ストレージパッケージを提供できるようになった。Caringo社のSwarmプラットフォームは、ハイパースケールのデータアクセスとストレージ用に設計されており、データガバナンスのニーズに対応し、ハードウェアへの依存を軽減します。DataCoreのデータ管理ソリューションの最新バージョンは、分散ストレージ・リソース全体のデータ・アクセス機能を拡張します。

ハイパーコンバージドインフラストラクチャ業界の概要

ハイパーコンバージドインフラストラクチャ市場の競争は中程度で、主要企業は少数です。現在、一部のプレーヤーが市場シェアで市場を独占しています。しかし、クラウドプラットフォームを利用したインフラサービスの進歩に伴い、新たなプレーヤーが市場での存在感を高め、新興国での事業展開を拡大しています。市場の主要企業は、市場での地位を維持するために、提携、合併、投資を継続的に行っています。

2023年2月、ファーウェイはビッグデータ、人工知能、エッジコンピューティング、インテリジェント・マニュファクチャリングなどの先進技術を導入することで、企業のデジタルトランスフォーメーションを加速する計画を発表しました。その中で、ハイパーコンバージドインフラは急速に進化しており、従来のデータセンターからエッジへ、構造化データから非構造化データへ、単一の汎用コンピューティング能力から多様なコンピューティング能力へとシフトしています。この進化は、データセンター構築の主流アプローチの1つとなっています。

さらに、この動向をサポートするため、ファーウェイはハイパーコンバージェンス戦略と、Kunpengハイパーコンバージェンス、Blue Whaleアプリケーションモール、ハイパーコンバージェンスソフトウェア、サポートツールなどの新製品の発売を準備しています。これらの製品は、エコシステムの開発、ユーザーエクスペリエンス、ビジネス能力を包括的にアップグレードします。

2022年4月、エクイニクスとデルはパートナーシップを拡大し、ハイパーコンバージドデータセンターの提供を開始しました。この拡張の一環として、エクイニクスはベアメタルアプライアンスのEquinix Metal製品ラインを拡張しました。さらに、「Dell PowerStore on Equinix Metal」、「Dell VxRail on Equinix Metal」、「Dell EMC PowerProtect DDVE on Equinix Metal」など、複数の新サービスの導入も含まれています。これらの新しいソリューションは、デルの高度なハードウェアとエクイニクスの堅牢なベアメタルインフラストラクチャを組み合わせることで、機能とパフォーマンスを強化することを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が市場に与える影響

第5章 市場力学

- 市場促進要因

- データ保護強化のニーズの高まり

- クラウドプラットフォーム上での統合需要の高まり

- 市場抑制要因

- ビジネスエコシステムにおけるデータプライバシーの喪失

第6章 市場セグメンテーション

- サービス別

- プロフェッショナル

- マネージド

- 組織タイプ別

- 大企業

- 中小企業

- エンドユーザー業界別

- IT・通信

- BFSI

- ヘルスケア

- 小売

- 政府・防衛

- その他のエンドユーザー産業

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Nutanix Inc.

- Dell Inc.

- VMware Inc.

- Hewlett Packard Enterprise Development LP

- Cisco System Inc.

- Oracle Corp.

- Microsoft Corp.

- NetApp Inc.

- IBM Corp.(Red Hat Inc.)

- Huawei Technologies Co. Ltd

- StarWind Software Inc.

- Datacore Software Corp.

- Maxta Inc.

- Pivot3 Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Hyper-Converged Infrastructure Market size is estimated at USD 16.72 billion in 2025, and is expected to reach USD 51.22 billion by 2030, at a CAGR of 25.09% during the forecast period (2025-2030).

Key Highlights

- Hyper-convergence infrastructure (HCI) has emerged as a transformative solution within the IT industry, revolutionizing the way organizations manage their data centers. The market for HCI has experienced significant growth and adoption as businesses seek to streamline their infrastructure, enhance operational efficiency, and embrace digital transformation.

- The increasing adoption of cloud computing has been a major driving factor for the hyper-converged infrastructure market. Enterprises across various industries are shifting their workloads to the cloud to leverage its scalability, cost-effectiveness, and flexibility. HCI solutions complement cloud environments by seamlessly integrating on-premises and cloud resources. With HCI, organizations can easily migrate workloads between private and public clouds, enabling hybrid cloud deployments that combine the benefits of both environments. This synergy between HCI and cloud computing has accelerated the market growth and is expected to continue driving the demand for hyper-converged infrastructure solutions.

- Data center virtualization and consolidation have become imperative for organizations seeking to optimize their IT infrastructure and reduce operational costs. Hyper-converged infrastructure offers a consolidated approach to data center management, enabling organizations to combine multiple components into a single, unified system. By leveraging virtualization technologies, HCI enables the efficient allocation and utilization of computing resources, leading to improved performance and reduced hardware footprint. The scalability and flexibility offered by HCI make it an ideal solution for data center consolidation and virtualization initiatives. As a result, the market for hyper-converged infrastructure is experiencing substantial growth driven by the demand for efficient data center operations.

- The global hyper-converged infrastructure market is experiencing increasing demand due to various applications, leading to greater efficiency in IT infrastructure. This surge in demand is fueled by the ability of hyper-converged infrastructure systems to safeguard data within on-premises data centers, offering features such as snapshots, replication, and encryption. Consequently, organizations across various sectors are seeking these solutions.

- However, the high initial investment cost of implementing HCI solutions is hampering the market. While HCI offers numerous benefits, including simplified management, improved scalability, and reduced operational costs, the upfront investment required to deploy these solutions can be significant. The costs of hardware, software licenses, and professional services can be challenging, particularly for small and medium-sized enterprises (SMEs) with limited IT budgets. The high initial investment cost is a barrier to adoption, hindering market growth. However, as the market matures and technology advancements occur, the cost of HCI solutions is expected to decline, making them more accessible to a broader range of organizations.

- The COVID-19 pandemic significantly accelerated digital transformation initiatives across industries. Organizations worldwide realized the importance of agile and resilient IT infrastructure to support remote work, online collaboration, and digital services. Hyper-converged infrastructure enabled these transformations by providing a scalable and flexible infrastructure foundation. The pandemic highlighted the need for businesses to be agile and adaptable, leading to increased adoption of HCI solutions. As a result, the post-COVID-19 era is expected to witness a further boost in the hyper-converged infrastructure market as organizations continue to invest in technologies that enhance their digital capabilities.

Hyper converged Infrastructure Market Trends

Growing Need for Enhanced Data Protection Driving the Market Growth

- Organizations today have a growing need for reliable and high-performance storage. Hyperconverged infrastructure (HCI) provides a secure and efficient solution by integrating networking, storage, and computation into a single system. This consolidation of resources streamlines management, reduces costs, and is considered crucial by many enterprises for their strategic IT priorities.

- The market for HCI is expanding due to the increasing adoption of HCI solutions, particularly in areas such as data security and disaster recovery. The widespread use of digital technology platforms like social media and knowledge platforms has also contributed to the growing demand for HCI. According to the IBM Data Breach's recent report, the average cost of data breaches has increased by 2.6% to USD 4.35 million, with penalties included. HCI systems mitigate the risk of data security breaches through their components and applications, and they often incorporate high-security AMD processors with security capabilities.

- Furthermore, HCI offers improved data security and scalability compared to traditional storage solutions. As the number of connected devices and the Internet of Things (IoT) continue to rise, the ability of HCI to gather and store analytics in a centralized management system becomes increasingly valuable. This feature aligns well with the future of 5G networks, where HCI's ability to view collected data through a unified interface proves advantageous. According to the GSMA, 5G connections are expected to surpass 1 billion this year and reach 2 billion by 2025, further driving the HCI market.

- HCI is optimized for virtual workloads, similar to public cloud-based services, and offers flexible, consumption-based infrastructure economics. It enables enterprises to rapidly scale their resources by adding HCI building blocks, allowing them to respond quickly to business demands and enhance IT service agility. With essential cloud computing services such as centralized administration, computation, storage, and data security embedded into hyper-converged systems, HCI becomes a comprehensive solution.

- Automation and machine learning are widely recognized as productivity boosters for businesses, enabling improved application performance and handling large amounts of data. HCI leverages AI to handle workload demands, optimize application workloads, and optimize storage. By bridging the gaps between on-premises private cloud, public cloud, and existing data center infrastructure, HCI in a hybrid multi-cloud model allows businesses to manage end-to-end data workflows and ensure easy accessibility of data for AI applications. The increasing corporate investment in AI, as highlighted by the Artificial Intelligence Index previous year's report, also drives the HCI market forward, with last year's global investment reaching almost USD 94 billion, a significant increase from the prior year's acquisition of USD 67.85 billion.

North America is Expected to Register the Fastest Growth

- The expansion of hyper-scale cloud service providers in the region primarily drives the growth of the HCI market in North America. Colocation services have also experienced growth in both the wholesale and retail sectors. The demand for infrastructure to support virtual desktops has increased due to rising mobile data usage and the implementation of bring-your-own-device (BYOD) regulations. As a result, HCI's market share is expected to increase in North America.

- Several data center companies have made significant investments in hyperscale data centers. Equinix, for instance, has announced plans to build 32 hyperscale data centers in major global markets. With a substantial investment of over USD 6.9 billion and a total capacity of 600 megawatts, Equinix aims to expand its presence and capitalize on the growing hyper-scale data center landscape. The increasing number of regional data centers will drive the HCI market further.

- Partnerships and collaborations are also shaping the HCI market in North America. For instance, Lenovo and Kyndryl expanded their collaboration to develop and deliver scalable hybrid and advanced computing implementations and cloud solutions. Leveraging Lenovo's expertise in PCs, storage, and server performance, along with Kyndryl's IT infrastructure services, the partnership aims to provide customers with comprehensive solutions across the hybrid cloud, HCI, and advanced computing applications.

- Moreover, the surge in enterprise deployments of HCI has led to a growing demand for software-defined storage. In response to this trend, DataCore Software acquired Caringo Inc., a specialist in object storage. This acquisition enables DataCore Software to offer a unified block, file, and object storage package. Caringo's Swarm platform, designed for hyperscale data access and storage, addresses data governance needs and reduces reliance on hardware. The latest version of DataCore's data management solution expands data access capabilities across distributed storage resources.

Hyper converged Infrastructure Industry Overview

The hyper-converged infrastructure market is moderately competitive and has a few major players. Some of the players currently dominate the market in terms of market share. However, with the advancement in infrastructure services across the cloud platform, new players are increasing their market presence, expanding their business footprint across emerging economies. The Key players in the market are continuously making partnerships, mergers, and investments to retain their market position.

In February 2023, Huawei announced its plans to accelerate the digital transformation of enterprises by implementing advanced technologies such as big data, artificial intelligence, edge computing, and intelligent manufacturing. In this context, hyper-converged infrastructure is evolving rapidly, shifting from traditional data centers to the edge, from structured to unstructured data, and from single general-purpose computing power to diversified computing power. This evolution has become one of the mainstream approaches for constructing data centers.

Moreover, to support this trend, Huawei is preparing to launch its hyper-convergence strategy and new products like Kunpeng Hyperconvergence, Blue Whale Application Mall, hyper-convergence software, and supporting tools. These offerings will comprehensively upgrade ecosystem development, user experience, and business capabilities.

In April 2022, Equinix and Dell expanded their partnership to provide hyper-converged data center offerings. As part of this expansion, Equinix extended its Equinix Metal line of bare metal appliances. Moreover, the expansion includes introducing several new offerings, including Dell PowerStore on Equinix Metal, Dell VxRail on Equinix Metal, and Dell EMC PowerProtect DDVE on Equinix Metal. These new solutions aimed to deliver enhanced capabilities and performance by combining Dell's advanced hardware with Equinix's robust bare metal infrastructure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Enhanced Data Protection

- 5.1.2 Rising Demand for Integration Over Cloud Platform

- 5.2 Market Restraints

- 5.2.1 Loss of Data Privacy Over the Business Eco-system

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Professional

- 6.1.2 Managed

- 6.2 By Organization Type

- 6.2.1 Large Enterprise

- 6.2.2 Small & Medium Enterprise

- 6.3 By End-user Industry

- 6.3.1 IT & Telecommunication

- 6.3.2 BFSI

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government and Defence

- 6.3.6 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nutanix Inc.

- 7.1.2 Dell Inc.

- 7.1.3 VMware Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Cisco System Inc.

- 7.1.6 Oracle Corp.

- 7.1.7 Microsoft Corp.

- 7.1.8 NetApp Inc.

- 7.1.9 IBM Corp. (Red Hat Inc.)

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 StarWind Software Inc.

- 7.1.12 Datacore Software Corp.

- 7.1.13 Maxta Inc.

- 7.1.14 Pivot3 Inc.