|

市場調査レポート

商品コード

1851063

廃棄物管理:世界の市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Global Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 廃棄物管理:世界の市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

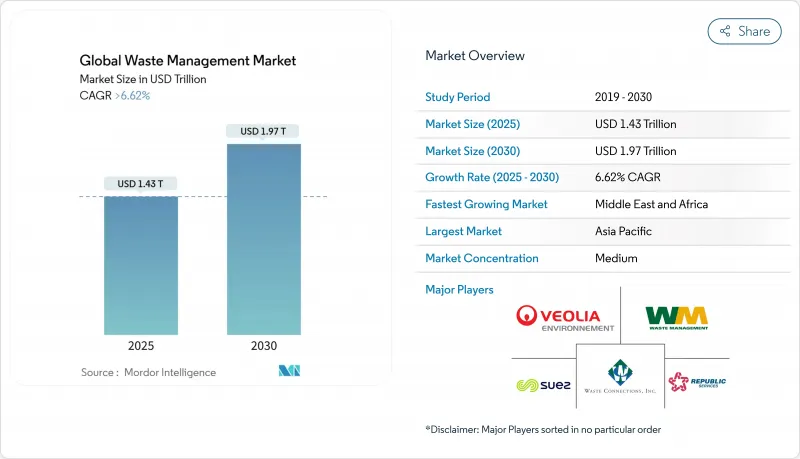

廃棄物管理市場は、2025年に1兆4,300億米ドルを生み出し、2030年には1兆9,700億米ドルに達すると予測され、2025年から2030年にかけてCAGR 6.62%で成長します。

持続的な規制圧力、企業の廃棄物ゼロ誓約の拡大、回収物の収益化により、廃棄物管理市場は埋立地中心のモデルから統合回収システムへと舵を切っています。欧州連合(EU)や米国のいくつかの州では、拡大生産者責任(EPR)法令が制定され、廃棄コストをブランド所有者に移転し、リサイクル・インフラのための専用資金プールを創設しています。同時に、米国環境保護庁(EPA)と欧州連合(EU)による強制的なデジタル追跡プラットフォームの展開は、データ主導の新たなサービス分野を生み出し、炭素捕獲技術を備えた廃棄物発電(WtE)施設への投資は、カーボン・マイナス収益の流れを解き放っています。アジア太平洋は、2024年に最大の地域となり、中東・アフリカ(MEA)は、2030年まで最も急速に成長する地域となる見込みです。電子廃棄物は、電気自動車用バッテリーの廃棄が迫っていることから、廃棄物の流れの中で最も速い速度を示しています。

世界の廃棄物管理市場動向と洞察

EUと北米における拡大生産者責任規制

義務化されたEPR制度は現在、生産者に回収とリサイクルのための資金調達を義務付け、廃棄物管理市場のコスト基盤を再構築しています。カリフォルニア州のSB 54は、2032年までにプラスチック包装を25%削減し、リサイクル率を65%にすることを義務付けており、ミネソタ州は2024年にEPR法を制定して他の米国5州に加わりました。EUは2023年にEPRを繊維製品にまで拡大し、新たなコンプライアンス市場を創出しました。この市場は、廃棄物処理事業者がEPRの資金を受けた契約を獲得するために、光学選別やポリマー識別ラインに統合し投資することを奨励しています。2024年にケニアで導入された同様の規則は、このモデルの世界的な普及を示しています。

カーボン・マイナス目標がWtE投資を促進

ネット・ゼロのコミットメントは、燃焼後の炭素回収を備えたWtEプラントに資本を誘導しています。日産720トンのごみを処理するメトロバンクーバーの施設は、年間30万トンのCO2を除去する設備に1億100万米ドルの値札を付け、排出量のバランスをプラスからマイナスに転換しました。サウジアラビアでは、300万トンの都市固形廃棄物を燃料に変換するWtEプログラムが、再生可能な電力を送電網に供給しながら、年間179万トンのCO2削減を目指しています。炭素クレジット市場へのアクセスは、事業者にとって新たな収入層となります。

南アジアとアフリカにおけるインフォーマル・セクターの断片的な優位性

広範な非正規労働力により、廃棄物管理市場への正規の浸透が制限されています。南アフリカでは、毎年367万トンの家庭廃棄物が未回収のまま放置され、不法投棄を助長し、自治体の収入を浸食しています。南アジアのインフォーマルな電子廃棄物リサイクルは、労働者を重金属にさらし、機関投資家が近代的な工場に資金を提供する意欲を削いでいます。これらの労働者を規制されたバリューチェーンに組み込むには、多くの地元事業者が資金を調達できないような訓練と資本が必要であり、回収率は低く、漏出量は多いままです。

セグメント分析

産業廃棄物は2024年に最も高い勢いを維持し、2030年までのCAGRは8.3%となる見込みである一方、一般家庭廃棄物は同年、廃棄物管理市場全体の46.54%という最大のシェアを占めました。企業の排出削減義務により、製造業者は生産くずを資源として扱うようになり、現場での梱包、溶剤回収、クローズドループ物流への需要が高まっています。年間2億5,000万ポンドの複雑なプラスチックを処理するよう設計された、イーストマンの22億5,000万米ドルの分子リサイクル事業展開は、産業機会の規模の大きさを物語っています。このシフトは、中国やASEAN諸国に集中する電子機器、自動車、消費財工場で特に顕著です。

住宅向けの流れは成熟しているもの、都市化が進んでいるため、廃棄物管理市場全体の規模を拡大する上で不可欠であることに変わりはないです。各国政府は、埋立地転換目標を遵守するため、色分けされたカーブサイド・プログラムや生ごみ消化装置を設置しています。小売チェーンからの商業廃棄物は、EPR料金が店舗前の収集インフラに資金を供給するため、安定した成長を続けています。建設・解体廃棄物は政策的に注目されています。2025年4月に施行されるインドのC&D規則改正では、巨大プロジェクトにリサイクル骨材の使用が義務付けられ、破砕業者にとって予測可能なトン数になります。医療廃棄物や農業廃棄物は、ニッチではあるが拡大しつつあるカテゴリーです。パンデミック後に感染性廃棄物のプロトコルが強化され、農業バイオマスが農村地帯の嫌気性消化プラントに供給されるようになりました。

廃棄物管理市場レポートは、発生源別(住宅、商業(小売、オフィスなど)、産業、その他)、サービスタイプ別(収集、輸送、分別・選別、処分・処理)、廃棄物タイプ別(都市固形廃棄物、E-Waste、その他)、地域別(北米、欧州、その他)に分類されています。本レポートでは、上記のすべてのセグメントについて、市場規模および予測(米ドル)を提供しています。

地域別分析

アジア太平洋地域は、2024年の世界売上高の56%を占め、高度な処理を必要とする多素材廃棄物の流れを生み出す、密集した製造業クラスターと急速な都市移動が原動力となっています。中国の循環経済促進法と日本のプラスチック資源循環法は、生産者にリサイクル可能な設計を義務付けており、インドの新規則は公共インフラに再生砂と再生骨材を要求しています。深セン、東京、ベンガルールの都市当局は、家庭での分別回収を促進するため、投げ銭制を導入しています。シンガポールの新データセンターで建設廃棄物の転用率85%を達成したマイクロソフトのような多国籍企業は、廃棄物ゼロの公約を達成するため、地域ごとにリサイクル契約を結んでいます。

中東・アフリカは、2030年までのCAGR見通しが9.1%で、最も急成長している地域です。サウジアラビアの投資リサイクル会社(SIRC)は、ビジョン2030の循環型経済のマイルストーンを達成するため、ごみ固形燃料化施設とタイヤから石油への転換施設に6億2,500万米ドルを投入しています。2025年2月に署名されたGCC廃棄物ーエネルギー協力議定書は、40%の埋立地転換目標を設定し、アブダビ、マナマ、ジェッダのプラントEPCパイプラインに活力を与えています。同時に、南アフリカとケニアでは、非公式な回収業者を正式に登録するためのデジタル登録システムを試験的に導入しています。

北米と欧州は成熟した市場だが、規制の多い市場です。米国環境保護庁(EPA)は2025年、すべての有害廃棄物の輸出に電子マニフェストの通過を義務付けており、データ・コンプライアンスの収益が拡大します。2027年までに連邦政府調達から使い捨てプラスチックを段階的に廃止するというホワイトハウスの戦略は、サプライヤーとの契約に波及すると予想されます。2024年5月発効の欧州の廃棄物輸送規制は、OECD非加盟国への輸出を制限し、2026年までにエンド・ツー・エンドのデジタル追跡を義務付ける。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と力学

- 市場促進要因

- EUと北米における拡大生産者責任規制

- カーボン・マイナス目標が廃棄物エネルギーへの投資を促進する

- 企業の廃棄物ゼロ誓約がアジアの産業リサイクル契約に拍車をかける

- 米国環境保護局(EPA)と欧州連合(EU)が廃棄物フローのデジタル追跡を義務化

- 都市メガシティにおけるオンデマンドの消費者向け運搬アプリが収集量を押し上げる

- EV普及によるリチウムイオン電池廃棄物の急増が専門リサイクル需要を創出

- 市場抑制要因

- 南アジア・アフリカにおける断片化されたインフォーマル・セクターの優位性

- 西欧における新たな埋立地に対する規制モラトリアによるコンプライアンスコストの増加

- 世界的にリサイクル投資を阻害する不安定な回収商品価格

- 国境を越えた廃棄物出荷の禁止が収益性の高い貿易ルートを縮小させる

- バリュー/サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- スタートアップ・エコシステム分析

- 主要新興動向

- 地政学的ショックの影響

- 産業の魅力- ファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 排出源別

- 住宅

- 商業(小売、オフィスなど)

- インダストリアル

- 医療(健康・医薬品)

- 建設・解体

- その他(施設用、農業用など)

- サービスタイプ別

- 収集、輸送、選別、分別

- 廃棄/処理

- 埋立地

- リサイクル・資源回収

- 焼却・廃棄物発電

- その他(化学処理、堆肥化など)

- その他(コンサルティング、監査、トレーニングなど)

- 廃棄物タイプ別

- 都市固形廃棄物

- 産業有害廃棄物

- 電子廃棄物

- プラスチック廃棄物

- 医療廃棄物

- 建設・解体廃棄物

- 農業廃棄物

- その他の特殊廃棄物(放射性物質など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- ASEAN(インドネシア、タイ、フィリピン、マレーシア、ベトナム)

- オーストラリア

- その他アジア太平洋地域

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- ノルディックス(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他欧州地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- 南アフリカ

- エジプト

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Veolia Environment SA

- Waste Management Inc.

- Suez SA

- Republic Services Inc.

- Waste Connections Inc.

- Clean Harbors Inc.

- Covanta Holding Corporation

- Biffa Group

- Remondis SE & Co. KG

- Stericycle Inc.

- GFL Environmental Inc.

- FCC Environment

- Cleanaway Waste Management Ltd

- Hitachi Zosen Inova AG

- Sims Limited

- Renewi PLC

- Averda

- Daiseki Co. Ltd

- Tatweer Environmental Services

- Waste Pro USA

- Recology