PaaS(Payment as a Service):市場シェア分析、業界動向・統計、成長予測(2025年~2030年)

Payment as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642077

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

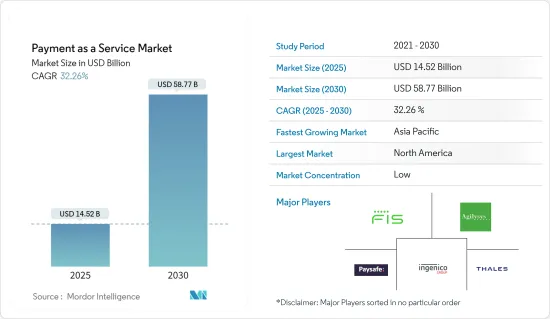

PaaS(Payment as a Service)の市場規模は2025年に145億2,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは32.26%で、2030年には587億7,000万米ドルに達すると予測されます。

現在のシナリオでは、スマートフォンの普及率が高まっており、簡単で便利なショッピング体験を提供することで顧客を支援するモバイルアプリを通じた商品やサービスの販売が拡大しています。簡単で便利な商品やサービスの購入に対する需要の高まりは、デジタル決済やキャッシュレス決済への急激なシフトをもたらしました。eコマース事業の増加は、世界の決済サービスプロバイダー市場をさらに押し上げます。

主なハイライト

- デジタルおよびオンライン取引を促進するために各国で進められている取り組みにより、ビジネスの拡大が見込まれます。PaaS市場の拡大は、Mastercard、Visa、Rupayのような決済ネットワークが世界規模で登場し、顧客の円滑な決済処理が可能になったことも後押ししています。

- スマートフォンの普及とオンライン・サービスの取り込みに対する需要の高まりは、継続的な成長を遂げています。スマートフォンの利用が重視されるようになり、世界中でインターネットが大量に普及していることから、市場での優位性は維持されると予想されます。また、銀行や金融機関がリアルタイムの決済サービスを提供することで、顧客のオンライン決済チャネルの利用頻度が高まっています。そのため、オンライン決済の需要は市場で継続的に増加しています。

- 決済業界は大きな変貌を遂げ、旧来の方法はワンクリックで新しいモジュールに置き換えられるようになった。さらに、PaaS(Payment as a Service)は、小売業者のシーンを変えているだけではないです。銀行は今、PaaS利用の増加は、顧客に信頼できる選択肢を提供する好機であることに気づいています。このように、特に小売業におけるeコマースへの依存度の高まりが、PaaS(Payment as a Service)市場を牽引しています。

- 国境を越えた取引のための世界標準が存在しないことが、市場を抑制する可能性があります。使いやすい世界の決済システム、国際基準、各国の政府規則が異なるため、銀行や企業は悪影響を受ける可能性があります。このため、データの収集と修正のために手作業が頻繁に必要となります。

- COVID-19の流行は、世界中の消費者の間でオンラインやデジタル化された支払い方法の利用や採用が増加しているため、サービスとしての支払い業界に大きな影響を与えています。さらに、消費者が市場の決済技術に慣れ親しむようになったため、PaaS(Payment as a Service)は大きな成長を遂げています。しかし、パンデミック(世界的大流行)以降、デジタル決済の採用が大幅に増加し、現金の携帯や支払いの動向が減少したことが、PaaS(Payment as a Service)市場の主な成長要因の1つとなっています。

PaaS(Payment as a Service)市場の動向

小売部門が大きく貢献する見込み

- eコマース業界の急成長により、小売企業は顧客により便利な体験を提供するため、デジタル決済技術を急速に導入しています。モバイル決済会議によると、世界中で25億人がオンラインショッピングを好んで利用しています。2025年までには、その数は40億人のデジタルバイヤーに増加すると予想されています。英国小売協会(BRC)によると、デビットカードが全取引の42.6%を占めるのに対し、現金は42.3%です。UK Financeによると、英国の小売支出全体の77%がカードで行われています。

- 加盟店は、市場での存在感と認知度を高めるため、最先端のテクノロジーを導入するケースが増えています。例えば、世界最大の小売業者であるウォルマートは最近、ペイパル・キャッシュ・マスターカードを店舗での買い物に利用できるようにすると発表しました。この企業は、顧客がペイパルのモバイルアプリを使用して、ウォルマートの店舗で現金を引き出したり、口座に入金したりできるように、決済プロバイダーのサービスを取り入れたいと考えています。

- さらに、決済サービスを提供する多くの企業が、市場での存在感を高めるために事業を拡大しています。例えば、世界で最も広範なオンライン小売業者のオンライン決済システムであるアマゾン・ペイは、地元の小売業者に「buy now pay later」機能を展開しました。アマゾンはすでに、百貨店チェーンのショッパーズ・ストップにこの決済サービスを導入しており、オンライン小売業者は5%の株式を所有し、食料品チェーンのモアに必要なインフラを設置しています。

- デジタル決済のもうひとつの大きなメリットは、マーケティング目的で顧客データを収集できることです。これにより小売企業は、来店や購入後に顧客との関係を構築し、顧客獲得と維持にさらに努めることができます。

アジア太平洋地域が最速の成長地域に

- アジア太平洋地域は、統合決済ソリューションに対する需要の高まりと決済技術の進歩により、大幅な成長が見込まれています。さらに、同地域におけるスマートフォンの普及率とインターネットの普及率の上昇が市場を後押ししています。

- 日本、中国、オーストラリア、韓国、ニュージーランドなど、この地域の国々は成長に大きく貢献しています。例えば、アジア・ペイメント・ネットワーク(APN)は、中国、日本、シンガポール、マレーシア、タイ、韓国、ニュージーランド、ベトナム、インドネシア、フィリピン、オーストラリアを含むアジア11カ国のグループであり、同地域における国境を越えた銀行取引を促進しています。

- 多くの小規模小売業者は、以前は現金決済に依存していたが、市場競争力を維持するためにデジタル決済を急速に導入しました。例えば、インド政府が悪魔払いプログラムを開始したことで、消費者は電子決済の利用を余儀なくされました。

- さまざまな決済サービス・プロバイダーも、成長市場を開拓して事業を拡大するため、アジア太平洋地域に投資しています。例えば、Infibeam社は、年間470億米ドルの売上を誇るインドのデジタル決済ゲートウェイインフラのプロバイダーである主力ブランドCCAvenueを積極的に推進することで、デジタル決済市場における世界のプレゼンスを拡大する意向です。

PaaS(Payment as a Service)業界の概要

PaaS(Payment as a Service)市場は、多くの決済サービスプロバイダーが存在するため、競争が激しく断片化しています。市場プレーヤーは常に革新的な製品の開発に注力しています。ベンダーは市場シェアを拡大し、市場牽引力を高めるため、M&Aにますます注力しています。

- 2022年11月、主要企業に選ばれる世界金融技術プラットフォームであるAdyenは、北米の大手食料品テクノロジー企業であるInstacartが、同社を追加の決済処理パートナーとして選定したと発表しました。

- 2022年10月、決済アクセプタンスの技術的パートナーであるインジェニコと、オーストラリアの大手決済サービス・プロバイダーの1つであるライブ・ペイメンツは、シームレスで便利な決済とコマース・ソリューションを小売業者やタクシーに提供するための長期戦略的パートナーシップを締結しました。インジェニコは、ライブ・ペイメンツ向けにAXIUMシリーズのAndroidスマート決済をオーストラリア全土で展開します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- スマートフォンの普及とオンラインサービスへの需要の高まり

- eコマースプラットフォームへの依存度の増加

- 市場抑制要因

- 決済に関する世界標準の不在

- 業界バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- サービスタイプ別

- マーチャント・ファイナンス

- 規制コンプライアンス

- セキュリティと不正防止

- 決済アプリケーションとゲートウェイ

- その他のサービス

- エンドユーザー業界別

- 小売・eコマース

- BFSI

- ホスピタリティ

- メディア・エンターテイメント

- その他エンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- FIS

- Thales Group

- Ingenico Group

- Agilysys Inc.

- Paysafe Holdings UK Limited

- Total System Services Inc.

- Mastercard

- PayPal Holdings Inc.

- Verifone

- Pineapple Payments

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Payment as a Service Market size is estimated at USD 14.52 billion in 2025, and is expected to reach USD 58.77 billion by 2030, at a CAGR of 32.26% during the forecast period (2025-2030).

In the current scenario, the increasing smartphone penetration is proliferating the growth of the sale of goods and services extensively through mobile apps to assist customers by providing an easy and convenient shopping experience. The rise in demand for easy and convenient purchases of goods and services resulted in a radical shift toward digital and cashless payments. The increase in e-commerce business further boosts the global payment service provider market.

Key Highlights

- The business is anticipated to increase due to efforts being made in numerous nations to promote digital and online transactions. The expansion of the PaaS market is also expected to be aided by the advent of payment networks like Mastercard, Visa, and Rupay on a global scale for the processing of smooth payments for clients.

- The increased demand for smartphone penetration and the incorporation of online services is experiencing continuous growth. It is expected to maintain its dominance in the market with an increase in emphasis on smartphone usage and massive internet penetration across the world. In addition, customers are using online payment channels more frequently as banks and financial institutions provide real-time payment services. Therefore, demand for online payments is experiencing a continuous rise in the market.

- The payment industry has experienced a significant transformation, and the old methods are replaced with new modules with a single click. Moreover, payment as a service (PaaS) is not only changing the scene for retailers. Banks are now realizing that the rise in PaaS use is an opportunity to give their clients a reliable choice. Thus, the increasing dependence on e-commerce, especially in retail, drives the payment as a service market.

- The absence of a global standard for cross-border transactions could restrain the market. Due to the lack of a worldwide payment system that is simple to use, international standards, and differing government rules in different countries, banks and businesses may be negatively impacted. This frequently necessitates manual intervention to gather and correct data.

- The COVID-19 pandemic has significantly impacted the payment as a service industry, owing to the increased usage and adoption of online and digitalized payment methods among consumers globally. Additionally, payment as a service is experiencing massive growth as consumers become familiar with the payment technology in the market. However, post-pandemic, there was a significant rise in the adoption of digital payments, reducing the trend of carrying and paying through cash which, in turn, has become one of the primary growth factors for the payment as a service market.

Payment as a Service (PAAS) Market Trends

Retail Sector Expected to be a Significant Contributor

- Retailers are rapidly adopting digital payment technology to bring more convenient experiences to their customers, owing to the massive growth in the e-commerce industry. According to the Mobile Payments Conference, 2.5 billion people worldwide prefer online shopping. By 2025, the number will grow to 4 billion digital buyers. According to the British Retail Consortium (BRC), debit cards account for 42.6% of all transactions, whereas cash is 42.3%. According to UK Finance, 77% of all UK retail spending was made by cards.

- Merchants are increasingly implementing cutting-edge technologies to boost their presence and visibility in the market. For instance, the biggest retailer in the world, Walmart, recently said that PayPal Cash Mastercard would be accepted for in-store purchases. The merchant wants to incorporate the payment provider's service so that customers can use the PayPal mobile app to withdraw cash and top up their accounts at Walmart locations.

- In addition, many companies that offer payment services are growing their operations to boost their market presence. For instance, the world's most extensive online retailer's online payment system, Amazon Pay, rolled out "buy now pay later" capabilities to local retailers. Amazon has already introduced the payments service in the department store chain Shoppers Stop, in which the online retailer owns a 5% stake and sets up the necessary infrastructure at the grocery chain More.

- Another significant benefit of digital payment is the ability to collect customer data for marketing purposes. This enables retailers to build customer relationships after their visit or purchase and further work toward customer acquisition and retention.

Asia-Pacific to be the Fastest Growing Region

- The Asia-Pacific region is expected to depict substantial growth owing to the increased demand for integrated payment solutions and advancements in payment technologies in the region. Furthermore, the rise in the penetration of smartphones and internet penetration in the region is propelling the market.

- Countries in the region, such as Japan, China, Australia, South Korea, and New Zealand, contribute significantly toward the growth. For instance, the Asian Payments Network (APN) is a group of 11 Asian countries that include China, Japan, Singapore, Malaysia, Thailand, South Korea, New Zealand, Vietnam, Indonesia, Philippines, and Australia to promote cross-border banking transactions in the region.

- Many small retailers earlier relied more on cash but rapidly deployed digital payments to remain competitive in the market. For instance, as the Indian government launched a demonetization program, consumers were forced to use electronic payments.

- Various payment service providers also invest in the Asia-Pacific region to expand their businesses by tapping the growing market. For instance, the firm Infibeam intends to expand its global presence in the digital payments market by aggressively promoting its flagship brand CCAvenue, a provider of digital payment gateway infrastructure in India with an annual run-rate of USD 47 billion.

Payment as a Service (PAAS) Industry Overview

The payment as a service market is highly competitive and fragmented, owing to the presence of many payment service providers. The market players are consistently focusing on developing innovative products. The vendors increasingly focus on mergers and acquisitions to increase market share and gain market traction.

- In November 2022, Adyen, the global financial technology platform of choice for leading businesses, announced that Instacart, the leading grocery technology company in North America, has selected the company as an additional payments processing partner.

- In October 2022, Ingenico, the technological partner in payments acceptance, and Live Payments, one of Australia's leading payment service providers, entered a long-term strategic partnership to equip retailers and taxis with seamless, convenient payment and commerce solutions. Ingenico will roll out its AXIUM range of Android Smart POS for Live Payments across Australia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Smartphone Penetration and Incorporation of Online Services

- 4.2.2 Increase Dependence on E-Commerce Platform

- 4.3 Market Restraints

- 4.3.1 Absence of Global Standards for Payments

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Force Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Types of Services

- 5.1.1 Merchant Financing

- 5.1.2 Regulatory Compliance

- 5.1.3 Security and Fraud Protection

- 5.1.4 Payment Applications and Gateways

- 5.1.5 Other Services

- 5.2 By End-user Industry

- 5.2.1 Retail and E-commerce

- 5.2.2 BFSI

- 5.2.3 Hospitality

- 5.2.4 Media and Entertainment

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 South Korea

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 FIS

- 6.1.2 Thales Group

- 6.1.3 Ingenico Group

- 6.1.4 Agilysys Inc.

- 6.1.5 Paysafe Holdings UK Limited

- 6.1.6 Total System Services Inc.

- 6.1.7 Mastercard

- 6.1.8 PayPal Holdings Inc.

- 6.1.9 Verifone

- 6.1.10 Pineapple Payments

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日