ウッドフローリング:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Wood Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642040

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

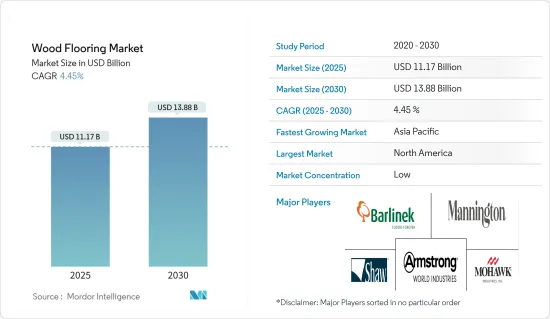

ウッドフローリング市場規模は2025年に111億7,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは4.45%で、2030年には138億8,000万米ドルに達すると予測されます。

ウッドフローリング市場は、都市化の進展、可処分所得の増加、持続可能な建材に対する意識の高まり、美観と耐久性に優れたフローリングオプションに対する消費者の嗜好の変化などを背景に、長年にわたって著しい成長と進化を遂げてきました。

ウッドフローリング市場の成長を支える主な促進要因の一つは、持続可能性と環境意識の高まりです。気候変動や森林破壊が懸念される中、環境に優しい建材を好む傾向が強まっています。特に、森林から供給されるウッドフローリングは持続可能な管理が行われており、森林管理協議会(FSC)などの団体から認証を受けているため、環境意識の高い消費者の共感を呼んでいます。こうした需要に応えるため、メーカー各社は再生木材や竹フローリングなど、持続可能なウッドフローリングの多様なソリューションを提供しています。

インテリアデザインにおけるカスタマイズやパーソナライゼーションの傾向の高まりは、ユニークなテクスチャー、仕上げ、カラーを提供するウッドフローリング製品に対する需要を後押ししています。メーカー各社はデジタル印刷や染色技術を活用して、希少な樹種を模倣したり、複雑なパターンを特徴とするウッドフローリングデザインを生み出しており、消費者は希少材やエキゾチック材に関連する高いコストや環境への影響を受けることなく、希望する美観を実現することができます。

ウッドフローリング市場の動向

エンジニアードウッドフローリングが市場の成長を後押し

無垢フローリングに比べ、エンジニアードフローリングの市場シェアは大きいです。エンジニアードウッドは無垢のハードウッドよりも寸法が安定しており、温度や湿度の変化による伸縮が少ないのが特徴です。この安定性により、地下室や床暖房設備のある部屋など、広葉樹無垢材が適さないような環境でも人工木材を設置することができます。さらに、人工木材はハードウッド無垢材よりも低価格で入手できることが多く、しかも同様の美観を備えています。

エンジニアードウッドフローリングは通常、上層に本物の木材を使用し、ハードウッドの自然な美しさと暖かさ、耐久性を高めています。ラミネートフローリングに比べ、人工木材は印刷されたイメージではなく、本物の木の単板を使用しているため、より本物の外観と感触を提供します。人工木材の多用途性、耐久性、審美的な魅力により、高品質のフローリングを求める住宅所有者に人気のある選択肢となっています。

北米はウッドフローリング市場をリードしている

北米のウッドフローリング市場は、建設活動の増加、リフォームやリノベーションプロジェクトの増加、環境に優しく持続可能な建材への嗜好の高まりといった要因によって、着実な成長を遂げています。米国とカナダでは、硬質無垢フローリングが歴史的に人気のある選択肢であり、時代を超越した魅力と耐久性が評価されてきました。しかし近年は、安定性、汎用性、耐湿性が強化された人工ウッドフローリングが大きな支持を得ており、湿度の高い地域や輻射暖房システムなど、さまざまな用途に適しています。

また、環境維持に対する消費者の意識の高まりを反映し、森林管理協議会(FSC)認証機関の認定を受けたウッドフローリング製品に対する需要も増加しています。板幅の拡大、質感のある仕上げ、再生木材の使用といった動向は、北米のウッドフローリング市場の多様性に寄与しています。製造技術の進歩により革新的なウッドフローリング製品が開発され、消費者のニーズや関心の変化に対応しています。全体として、北米のウッドフローリング市場はダイナミックで競合が激しく、都市化、デザイン動向、持続可能な慣行の進歩といった要因によって成長機会がもたらされています。

ウッドフローリング業界の概要

ウッドフローリング市場は競争が激しく、複数の主要企業が市場を独占しています。Mohawk Industries、Armstrong World Industries、Mannington Mills Inc.、Barlinek SA、Shaw Industries Groupなどの企業が著名なプレーヤーで、幅広い種類のウッドフローリング製品を提供しています。また、ニッチセグメントや特定地域に特化した地域・地元企業との競合も見られます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 建設・リフォーム活動の増加

- 持続可能で環境に優しい製品への注目の高まり

- 市場抑制要因

- 代替フローリング市場との競合

- 原材料価格の高騰

- 市場機会

- 仕上げや施工技術の向上など、ウッドフローリング技術の進歩

- カスタマイズとデザイン動向の高まり

- バリューチェーン分析

- 業界の魅力:ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 業界の技術的進歩に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- 無垢材

- エンジニアードウッド

- 流通チャネル別

- ホームセンター

- 旗艦店

- 専門店

- オンラインストア

- エンドユーザー別

- 住宅

- 商業

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Mohawk Industries

- Armstrong World Industries

- Mannington Mills Inc.

- Barlinek SA

- Shaw Industries Group

- Beaulieu International Group

- Home Legend LLC

- Provenza Floors Inc.

- Boral Limited

- Tarkett SA*

第7章 今後の市場動向

第8章 免責事項および出版社について

目次

The Wood Flooring Market size is estimated at USD 11.17 billion in 2025, and is expected to reach USD 13.88 billion by 2030, at a CAGR of 4.45% during the forecast period (2025-2030).

The wood flooring market has witnessed significant growth and evolution over the years, driven by increasing urbanization, rising disposable income, growing awareness of sustainable construction materials, and changing consumer preferences for aesthetic and durable flooring options.

One of the key drivers behind the growth of the wood flooring market is the increasing emphasis on sustainability and environmental consciousness. With concerns about climate change and deforestation, there's a growing preference for eco-friendly building materials. Particularly, wood flooring that is sourced from forests is sustainably managed and has certification from groups like the Forest Stewardship Council (FSC), which resonates well with environmentally conscious consumers. In response to this demand, manufacturers are providing a variety of sustainable wood flooring solutions, including reclaimed wood and bamboo flooring, which are gaining popularity due to their eco-friendly attributes.

The growing trend of customization and personalization in interior design is fueling the demand for wood flooring products that offer unique textures, finishes, and colors. Manufacturers are leveraging digital printing and staining techniques to create wood flooring designs that mimic rare wood species or feature intricate patterns, allowing consumers to achieve their desired aesthetic without the high cost or environmental impact associated with rare or exotic woods.

Wood Flooring Market Trends

Engineered Wood Flooring is Boosting the Market's Growth

Engineered wood flooring holds a larger market share compared to solid wood flooring. Engineered wood is dimensionally more stable than solid hardwood, featuring less expansion and contraction with changes in temperature and humidity. This stability allows engineered wood to be installed in environments where solid hardwood may not be suitable, such as basements or rooms with underfloor heating systems. Additionally, engineered wood is often available at a lower price point than solid hardwood while still providing a similar aesthetic appeal.

Engineered wood flooring typically utilizes a top layer of real wood, offering the natural beauty and warmth of hardwood with enhanced durability. Compared to laminate flooring, engineered wood provides a more authentic look and feel, as it is constructed using genuine wood veneers rather than printed images. The versatility, durability, and aesthetic appeal of engineered wood make it a popular choice for homeowners seeking high-quality flooring solutions.

North America is Leading the Wood Flooring Market

The wood flooring market in North America is defined by steady growth, driven by factors such as increasing construction activities, rising renovation and remodeling projects, and a growing preference for eco-friendly and sustainable building materials. In the United States and Canada, solid hardwood flooring has historically been a popular choice, valued for its timeless appeal and durability. However, engineered wood flooring has gained significant traction in recent years due to its enhanced stability, versatility, and resistance to moisture, making it suitable for various applications, including areas with high humidity levels or radiant heating systems.

Additionally, the demand for wood flooring products approved by Forest Stewardship Council (FSC) certification bodies is increasing, reflecting consumers' growing awareness of environmental sustainability. Trends such as wider plank widths, textured finishes, and the use of reclaimed wood contribute to the diversity of offerings in the North American wood flooring market. Technological advancements in manufacturing techniques have led to the development of innovative wood flooring products, meeting consumers' changing needs and interests. Overall, the wood flooring market in North America is dynamic and competitive, with growth opportunities driven by factors such as urbanization, design trends, and advancements in sustainable practices.

Wood Flooring Industry Overview

The wood flooring market is highly competitive, with several key players dominating the market. Companies like Mohawk Industries, Armstrong World Industries, Mannington Mills Inc., Barlinek SA, and Shaw Industries Group are prominent players, offering a wide range of wood flooring products. Additionally, the market also sees competition from regional and local players, focusing on niche segments or specific geographical areas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Construction and Renovation Activities

- 4.2.2 Increasing Focus on Sustainable and Eco-friendly Products

- 4.3 Market Restraints

- 4.3.1 Competition from Alternative Flooring Market

- 4.3.2 High Price of Raw Materials

- 4.4 Market Opportunities

- 4.4.1 Advancements in Wood Flooring Technology, Such as Enhanced Finishes and Installation Techniques

- 4.4.2 Rising Customization and Design Trends

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness: Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Insights into Technological Advancements in the Industry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Solid Wood

- 5.1.2 Engineered Wood

- 5.2 By Distribution Channel

- 5.2.1 Home Centers

- 5.2.2 Flagship Stores

- 5.2.3 Specialty Stores

- 5.2.4 Online Stores

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Italy

- 5.4.2.6 Spain

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Mohawk Industries

- 6.2.2 Armstrong World Industries

- 6.2.3 Mannington Mills Inc.

- 6.2.4 Barlinek SA

- 6.2.5 Shaw Industries Group

- 6.2.6 Beaulieu International Group

- 6.2.7 Home Legend LLC

- 6.2.8 Provenza Floors Inc.

- 6.2.9 Boral Limited

- 6.2.10 Tarkett SA*

7 FUTURE MARKET TRENDS

8 DISCLAIMER AND ABOUT US

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日