産業用照明:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Industrial Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641991

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

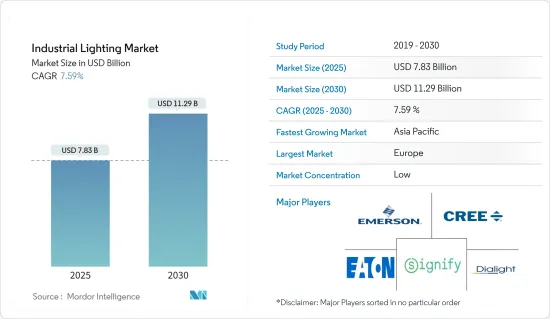

産業用照明の市場規模は2025年に78億3,000万米ドルと推計され、2030年には112億9,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは7.59%です。

幅広い照明製品が競合価格で入手可能であり、様々な産業分野でエネルギー効率の高い照明システムへの需要が高まっていることが、産業用照明市場の成長を後押ししています。

主なハイライト

- 長年にわたり、産業用照明の需要は安定した成長を遂げており、この傾向は今後数年間も続くと予想されます。産業用照明は、怪我や事故の危険性がある場所で使用されることが多く、作業員の安全性と生産性を高める上で重要な役割を果たしています。

- 産業事業者は、商業・産業現場で最も一般的な従来の照明器具、すなわち蛍光灯や高輝度放電灯(HID)の熱損失によるメンテナンスコストの高さに伴う課題に直面することが多いです。省エネと省コスト、そして低メンテナンスコストを実現するLED照明は、ここ数年で大きな需要を目の当たりにしてきました。

- 工業生産が複数の地域で急成長を続ける中、電力への依存度も高まっています。また、メーカーはしばしば多額の運用コストに課題を抱えています。これは、メーカーがエネルギー効率の高い照明ソリューションを採用せざるを得ない主な要因の一つです。加えて、世界中で多くの規制が課せられ、LEDのようなエネルギー効率の高い照明ソリューションの使用が促進されています。

- 製造工場や生産施設に既存の照明システムを統合または交換するために必要な初期費用は、特に中小産業では通常高額です。そのため、一部のエンドユーザーは、比較的低コストであるLEDよりも、コンパクト蛍光灯(CFL)、LFL、HIDを好んで使用しており、これが市場の成長を妨げています。

- COVID-19は、特に流行初期の数ヶ月間、産業部門における多くの建設活動を停止させ、市場の需要を一時的に減退させました。しかし、パンデミックに関連した多くの規制が緩和されたことで、多くの地域で建設活動が回復し始め、市場は再成長を目の当たりにしています。

産業用照明市場の動向

LED光源が大きなシェアを占める見込み

- LEDは、長寿命、エネルギー効率、運用/保守コストの低さ、投資収益率(ROI)の短期化といった特長を備えており、産業用照明市場での需要を最終的に押し上げる可能性があります。さらに、LEDは有害な紫外線や赤外線を発生しないため、冷却コストの削減、メンテナンスの簡素化、製品寿命の延長、産業環境における安全性の確保など、いくつかの利点があります。

- LEDには可動部がなく、耐久性に優れ、衝撃や腐食に強いです。さらに、火花で発火しないという利点もあります。このような特性を持つLEDは、高振動、破片、化学物質、爆発性溶液にさらされることの多い鉱業用途に非常に適しています。

- 例えば、2021年8月、産業用LED照明ソリューションを提供するDialight Groupは、EMEAおよびAPAC市場向けに新しいProSite LED投光器シリーズを発売しました。この新しい投光器は産業用途向けに設計され、鉱山現場など多様な施設の安全性とセキュリティを確保するために、鮮明でほぼ昼光に近い照明で外部の作業現場に優れた視認性を提供します。

- 多くの倉庫では、照明に直管蛍光灯やメタルハライドランプが使用されています。蛍光灯やメタルハライドランプは、白熱電球に比べれば改善されたとはいえ、LEDと直接比較すると、廃棄の危険性や寿命の短さ、光の効率の低さといった問題があります。そのため、これらの倉庫ではLEDへの切り替えが進んでいます。

- 世界中の政府や公共機関は、白熱灯の使用によって生じるメンテナンスの問題に対処するため、こうしたLED照明ネットワークの導入を増やしています。これらの電球や高圧ナトリウムは、周囲の反応性ガスのために化合物が発生しやすいです。また、LEDは光源として高輝度・高効率を実現し、従来の照明に比べ耐腐食性・耐蒸気性に優れた運用ソリューションを提供します。

欧州が大きな市場シェアを占める

- LEDモジュールはEU市場で急速に普及しています。この地域でLED製品の需要を牽引している重要な要因は、EUが非効率的な照明技術の販売を禁止する政策を打ち出していることです。例えば、EU全域で新しいエコデザインとラベリング規則が施行され、2021年9月から特定の蛍光灯とハロゲン電球が禁止されました。

- 2021年8月、シグニファイ社は、EUの厳しいエコデザインとエネルギー表示規制に適合するフィリップスLED Aクラス電球を初めて発売しました。新型フィリップスLED Aクラス電球は、標準的なフィリップスLED電球に比べて消費電力が60%削減され、寿命も長くなると期待されています。

- さらに、英国をはじめとする多くの欧州諸国は、2050年までに炭素排出量を正味ゼロにすることを目指しています。そのため、現地の製造企業は、このアジェンダに基づく照明技術革新に多額の投資を行っています。

- ガスと電力の卸売価格のかつてない高騰は、欧州全域の多くのセクターに負担をかけています。例えば、欧州委員会によると、欧州のガス卸売価格は2021年第3四半期に記録的な水準まで上昇し、9月末までに85ユーロ/MWhに達しました。そのため、企業は天然ガスや電力の主要ユーザーである製造、倉庫、物流全体でコスト削減を迫られています。

- Yu Energyによると、倉庫・物流業界では、照明がエネルギーの大半(通常約65%)を使用しています。この分野でのエネルギー効率は、近年、地域全体で倉庫の収容能力が急速に拡大しているため、特に重要です。例えば、ONSによると、2021年の英国における倉庫建設の新規受注額は56億ポンド(67億5,000万米ドル)で、これは1985年以降のどの年よりも多いです。このため、この分野ではエネルギー効率の高い照明ソリューションに対する需要が大きいです。

産業用照明産業の概要

産業用照明市場は非常に細分化されています。全体として、既存の競合企業間の競争は激しいです。さらに、大企業と中小企業の新たなイノベーション戦略が市場成長を促進すると期待されています。

- 2022年5月-シグニファイ社は、産業や駐車場のような厳しい環境で最適な性能を発揮するよう設計されたソリューション、最新世代のパシフィックLED gen5防水照明器具の発売を発表しました。この新しいソリューションは、幅広い重工業用途に適しています。この照明器具は、堅牢でコンパクトな製品アーキテクチャを持ち、高い防水・防塵性能と高度な機械的保護性能を備えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の産業エコシステムへの影響

第5章 市場力学

- 市場促進要因

- エンドユーザーの省エネ意識の高まり

- 多様化する産業用途におけるLED採用の増加

- 市場の課題

- 導入コストの高さ

第6章 市場セグメンテーション

- 光源別

- LED

- 高輝度放電(HID)照明

- 蛍光灯照明

- 製品タイプ別

- 高/低ベイ照明

- 洪水/エリア照明

- エンドユーザー用途別

- 石油・ガス

- 鉱業

- 製薬

- 製造業

- 倉庫

- その他のエンドユーザー用途

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Signify Holding

- Cree Inc.

- Eaton Corporation PLC

- Emerson Electric Co.

- Dialight PLC

- Legrand SA

- Zumtobel Group AG

- Acuity Brands Inc.

- Osram Licht AG

- Trilux Lighting Ltd

- Hubbell Incorporated

- Larson Electronics LLC

- Hilclare Lighting

- Raytec Ltd

- Glamox UK

- Nemalux Inc.

- R.Stahl Limited

- ABB Installation Products Inc.(ABB Limited)

第8章 投資分析

第9章 市場展望

目次

The Industrial Lighting Market size is estimated at USD 7.83 billion in 2025, and is expected to reach USD 11.29 billion by 2030, at a CAGR of 7.59% during the forecast period (2025-2030).

The availability of a wide range of lighting products at competitive prices and the increasing demand for energy-efficient lighting systems across various industrial sectors drive the industrial lighting market's growth.

Key Highlights

- Over the years, the demand for industrial lighting has been experiencing steady growth, and this trend is expected to continue over the coming years as well, owing to the increasing use at warehouses and for logistics, industrial establishments, etc., across the world. Industrial lighting is often used in places that have risks of injury and accidents and play an important role in enhancing the safety and productivity of workers.

- Industrial operators often face challenges associated with high maintenance costs due to heat losses of the traditional and most common lighting fixtures in commercial and industrial settings, i.e., fluorescent and high-intensity discharge (HID) lights. LED lights that offer greater energy and cost savings, along with low maintenance costs, have witnessed a significant demand in the past few years.

- As the industrial output continues to grow rapidly across multiple regions, the reliance on electricity is also increasing. Also, the manufacturers are often challenged with substantial operational costs. This is one of the key factors compelling manufacturers to adopt energy-efficient lighting solutions. Additionally, many regulations imposed worldwide are promoting the use of energy-efficient lighting solutions, such as LED.

- The initial cost required for integrating or replacing the existing lighting systems in manufacturing plants and production facilities is usually high, especially for small and medium industries. Consequently, certain end-users still prefer compact fluorescent lamps (CFL), LFL, and HIDs over new and emerging LEDs, as they have a comparatively lower cost, which hampers the market growth.

- Covid-19 halted many construction activities in the industrial sector, especially in the initial months of the outbreak, temporarily dampening the market demand. However, with many pandemic-related restrictions easing up, construction activities have started picking up in many regions, and the market is witnessing renewed growth.

Industrial Lighting Market Trends

LED Light Source is Expected to Hold Major Share

- LEDs have features such as longevity, energy efficiency, low operational/maintenance costs, and the ability to deliver an increasingly shorter return on investment (ROI), which might ultimately drive their demand in the industrial lighting market. Moreover, LEDs do not produce any harmful ultraviolet or infrared radiation, thereby offering several benefits, such as lowered cooling costs, maintenance simplification, prolonged product life, and providing a margin of safety in an industrial environment.

- LEDs do not have any moving parts, are very durable, and can withstand shock and corrosion better. An added advantage is their inability to ignite with a spark. With such properties, LEDs are highly suitable for mining industry applications that are often subject to high vibrations, debris, chemicals, and explosive solutions.

- For instance, in August 2021, Dialight Group, a provider of industrial LED lighting solutions, launched its new ProSite LED floodlight range for the EMEA and APAC markets. The new floodlights were designed for industrial applications, providing superior visibility to external worksites with crisp, near-daylight illumination to ensure the safety and security of a diverse range of facilities, including mine sites.

- Many warehouses use linear fluorescent lamps or metal halide lamps for lighting. While fluorescents and metal halides are an improvement over incandescent bulbs, they still present issues like disposal hazards, shorter lifespan, and less efficient light when it comes to a direct comparison with LEDs. As such, these warehouses are now switching to LEDs.

- Governments and public organizations worldwide are increasingly deploying these LED Lighting networks to address the maintenance issues created by incandescent lamps' usage. These bulbs and high-pressure sodium are easily compounded due to the surrounding reactive gases. Besides, as a lighting source, LED also provides a high luminosity and high efficiency and offers operational solutions against corrosion and vapor resistance compared to traditional lighting.

Europe to Hold Significant Market Share

- LED modules have had a rapid uptake in the EU market. An important factor driving the demand for LED products in the region has been the European Union's policy measures banning the sale of inefficient lighting technologies. For instance, certain fluorescent and halogen light bulbs have been banned starting September 2021, as new Ecodesign and labeling rules came into force across the European Union.

- In August 2021, Signify introduced the first Philips LED A-class bulbs that meet the stringent EU Ecodesign and Energy labeling regulations. The New Philips LED A-class bulbs are expected to consume 60% less energy compared to standard Philips LED bulbs and have a longer lifespan.

- Further, many European countries, such as the United Kingdom, are aiming for net-zero carbon emissions by 2050. Therefore, local manufacturing companies are investing considerably in lighting innovations based on this agenda.

- The unprecedented rise in wholesale gas and electricity prices has put a strain on many sectors across Europe. For instance, wholesale gas prices in Europe rose to record levels in Q3 2021, reaching 85 EUR/MWh by the end of September, a level rarely seen in European hubs, according to the European Commission. As such, companies are under increasing pressure to cut costs across manufacturing, warehousing, and logistics, which are the major users of natural gas and electricity.

- According to Yu Energy, in the warehousing and logistics industry, lighting uses most of the energy (typically around 65%). Energy efficiency in this sector is particularly important owing to the rapid expansion in warehousing capacity in recent years across the region. For instance, as per ONS, new orders for the building of warehouses in the United Kingdom were worth GBP 5.6 billion (USD 6.75 billion) in 2021, which is more than in any year since 1985. As such, there is significant demand for energy-efficient lighting solutions from this segment.

Industrial Lighting Industry Overview

The industrial lighting market is highly fragmented. Overall, the competitive rivalry among existing competitors is high. Further, the new innovation strategies of large and small enterprise companies are expected to drive market growth.

- May 2022 - Signify announced the launch of the latest generation of the Pacific LED gen5 waterproof luminaire, a solution designed for optimal performance in the demanding environments such as industry and parking areas. The new solution is suitable for a wide range of heavy industrial applications. The luminaires have a robust and compact product architecture, with high water and dust protection, along with a high degree of mechanical protection.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Industry Ecosystem

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Awareness About Energy Savings Among End-users

- 5.1.2 Rising Adoption of LED Across Diversified Industrial Applications

- 5.2 Market Challenges

- 5.2.1 High Cost of Implementation

6 MARKET SEGMENTATION

- 6.1 By Light Source

- 6.1.1 LED

- 6.1.2 High-intensity Discharge (HID) Lighting

- 6.1.3 Fluorescent Lighting

- 6.2 By Product Type

- 6.2.1 High/Low Bay Lighting

- 6.2.2 Flood/Area Lighting

- 6.3 By End-user Application

- 6.3.1 Oil and Gas

- 6.3.2 Mining

- 6.3.3 Pharmaceutical

- 6.3.4 Manufacturing

- 6.3.5 Warehouse

- 6.3.6 Other End-user Applications

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Signify Holding

- 7.1.2 Cree Inc.

- 7.1.3 Eaton Corporation PLC

- 7.1.4 Emerson Electric Co.

- 7.1.5 Dialight PLC

- 7.1.6 Legrand SA

- 7.1.7 Zumtobel Group AG

- 7.1.8 Acuity Brands Inc.

- 7.1.9 Osram Licht AG

- 7.1.10 Trilux Lighting Ltd

- 7.1.11 Hubbell Incorporated

- 7.1.12 Larson Electronics LLC

- 7.1.13 Hilclare Lighting

- 7.1.14 Raytec Ltd

- 7.1.15 Glamox UK

- 7.1.16 Nemalux Inc.

- 7.1.17 R.Stahl Limited

- 7.1.18 ABB Installation Products Inc. (ABB Limited)

8 INVESTMENT ANALYSIS

9 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日