|

市場調査レポート

商品コード

1641937

マイクロモバイルデータセンター:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Micro Mobile Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マイクロモバイルデータセンター:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

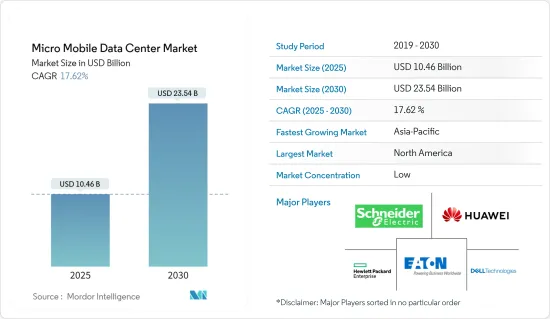

マイクロモバイルデータセンターの市場規模は2025年に104億6,000万米ドルと推定され、2030年には235億4,000万米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは17.62%です。

マイクロモバイルデータセンターは、通常のデータセンターで必要とされるストレージ、コンピュート・パワー、ネットワーキングをコンパクトにまとめた箱型のコンテナです。さらに、技術の進歩に伴い、クラウド接続が一体化され、エッジ向けのターンキーパッケージが完成しています。

主なハイライト

- マイクロモバイルデータセンターは、そのサイズ、汎用性、プラグアンドプレイ機能により、遠隔地での一時的な導入に最適です。また、洪水や地震などのリスクが高い場所での一時的な利用にも適しています。言い換えれば、マイクロデータセンターは従来のモデルの物理的フットプリントと消費エネルギーを最小限に抑えることができます。

- 世界のデジタル化の進展、インターネットの普及、スマートテクノロジーの関連性、IoT搭載デバイス、ビッグデータ、5Gネットワークの市場開拓などの要因が、マイクロモバイルデータセンターの市場動向を後押しするとみられます。エリクソンによると、5Gの契約数は2019年から2028年にかけて、世界でそれぞれ1,200万件超から45億件超へと大幅に増加すると予測されています。

- さらに、企業のオフィスではインフラを定期的に移行するため、コンテナ型データセンターのニーズが高まっています。さらに、企業はワークロードの増加に伴い、マイクロモバイルデータセンターの成長に多くの費用を費やしています。こうした要因により、今後数年間は市場拡大の大きなチャンスが生まれます。

- さらに、企業はクラウドのプレゼンスを高めており、ポータブルデータセンターの展開が必要となっています。また、低コストで低遅延であることから、中小企業向けのマイクロモバイルデータセンターの需要が高まっています。その結果、将来的な市場成長の見込みが高まっています。しかし、従来のデータセンターとの統合が市場の成長を阻害しています。

- COVID-19の発生は市場成長にプラスの影響を与え、マイクロモバイルデータセンター技術はデータストレージの大容量ニーズを満たす上で組織を支援しています。マイクロモバイルデータセンター事業者は、データストレージ需要が高まる時期に高性能のマイクロモバイルデータセンターを提供する能力と容量を保証する必要性が高まっています。パンデミック後、デジタル化技術や在宅勤務の増加により、市場は急成長しています。SaaS(Software as a Service)に対する需要の高まりは、データセンターへのトラフィックをかつてないほど増加させています。そのため、プレーヤーはこれらのソリューションに投資しています。

マイクロモバイルデータセンター市場動向

ヘルスケアエンドユーザーが大きな市場シェアを占める見込み

- マイクロモバイルデータセンターの採用は、ヘルスケア業界に柔軟性、有効性、セキュリティ、低コストモデルをもたらすのに役立ちます。世界のヘルスケア産業の成長は、マイクロモバイルデータセンターの需要をさらに促進すると推定されます。

- 電子カルテ(EHR)の増加は、ヘルスケアプロバイダーのマイクロモバイルデータセンターに対する需要をさらに高める。ファイルルームをサーバールームに置き換えるよりも、EHRベンダーが安全な施設でドキュメントをホスティングすることを選ぶ人が多いです。

- ビッグデータの増大も、データをクラウドに移行するもう一つの動機となっています。異なるデータセットをクラウドにまとめることで、業務、臨床、財務データをビッグデータ分析プロセスに集約することができます。このような要因が、ヘルスケア業界におけるマイクロモバイルデータセンターの採用拡大に寄与しています。

- IoT機器、特にスマートフォンの普及は、ヘルスケア業界におけるマイクロモバイルデータセンターの需要を押し上げています。エリクソンによると、近距離モノのインターネット(IoT)デバイスの数は今年、世界で166億台に達しました。今後3年間で、この数は224億台まで増加すると予測されています。広域IoTデバイスは、今年度32億個に達し、今後3年間で52億個に達すると予測されています。患者は、自分の条件で医療機関にアクセスすることを望んでいます。ヘルスケア向けのこれらのデバイスは、充実したデータをあらゆるケアポイントを通じて安全に流すことを可能にし、患者の体験と健康アウトカムの継続的な改善を支援します。

- IoTとクラウド技術がヘルスケアに統合されるにつれて、ブロックチェーンのような概念も普及し、データストレージとマイクロモバイルデータセンターの需要が高まっています。

- ブロックチェーンを通じて生成されたデータはヘルスケアサービスにおいて極めて機密性が高いため、ブロックチェーン技術は機密記録を保護し、ユーザーの身元に関連するデータを保存・認証するために使用されており、マイクロモバイルデータセンターはヘルスケア業界で大きな可能性を秘めています。したがって、ヘルスケア業界におけるマイクロモバイルデータセンターの採用は、予測期間中に大きく成長すると予想されます。

アジア太平洋地域が急成長市場になる見込み

- アジア太平洋は、データセンターが世界で最も急速に成長している地域のひとつです。また、中小企業における自動化ツールやBIツールの採用率も高いです。したがって、この地域は調査対象市場の成長にとって大きな可能性を秘めています。

- この成長の多くは、特に中国やオーストラリアなどの国々で、過去10年間に政府機関がデータセンターを広く採用したことに起因しています。同地域のデジタル経済を活性化させることを目的としたデータセンターの進歩に対する政府の大規模な投資が、クラウドサービス、ビッグデータ、IoTの採用を後押ししています。

- 中国では、クラウドコンピューティングやその他のデータ・サービスの需要が増加の一途をたどっているが、データセンター技術の進歩は、これらの技術を近代的な製造業と統合し、中国が徐々にサービス経済へと移行していく上で重要な役割を果たすと予想されます。

- 中国におけるインターネット普及率の向上も、マイクロモバイルデータセンターの需要拡大に貢献すると思われます。中国では、企業が自社のプレゼンスを高め、品質とサイバーセキュリティを強化するために、より高速で安定したブロードバンド接続への需要が高まっています。

- コロケーション・プロバイダーやクラウドプロバイダーが大規模な建設プロジェクトに着手し、加速するデジタルの未来における役割に備えるために小規模な企業向け施設を次々と建設しているため、オーストラリアのデータセンターに対する投資見通しは引き続き明るいです。

- 加えて、ヘルスケア、小売、eコマース、業界別データセンターの普及率の高さなどが、市場のさらなる成長を促すと予想されます。さらに、BYODやIoTデバイスの職場への導入が進んでいるため、複数のソースを通じて生成されるデータが多くなっています。同地域におけるデータ拡散の急激な成長により、企業はマイクロデータセンターへの投資を余儀なくされています。

- こうした動向を背景に、アジア太平洋地域ではハイブリッドクラウドがクラウド導入の有力な手段として浮上しています。ハイブリッドクラウドは、コンプライアンスやセキュリティなどのアプリケーション要件に応じてインフラを選択できるためです。

マイクロモバイルデータセンター産業の概要

マイクロモバイルデータセンター市場は非常に断片化されており、シュナイダーエレクトリックSE、Dell EMC Inc.、Huawei Technologies、Hewlett Packard Enterprise、開発LP、Eaton Corporation PLCといった大手企業が存在します。同市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携、合併、買収などの戦略を採用しています。

- 2022年11月- ハイブリッドITインフラ管理向けに、シュナイダーエレクトリックはEcoStruxure Micro Data Center R-Series 42U Medium Densityを発売しました。この新しいマイクロデータセンター・ソリューションは、産業環境のある遠隔地のITアプリケーション向けに設計されており、セットアップが容易な完全統合型となっています。また、移動に便利な巨大な産業用キャスターも装備しています。

- 2022年4月-IBM Corporationは、インドの多国籍通信会社であるAirtelと、インドにおけるエッジクラウドサービスの提供で協業すると発表しました。両社はインドの主要20都市に広がる120のデータセンターを通じて、企業にエッジクラウドサービスを提供します。この協業により、ワークロードがエッジに移動する際に重要な主権ニーズとデータ・セキュリティを満たしながら、レイテンシーを削減することで、ユーザー・エクスペリエンスと企業業績を向上させる。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- IOTデバイス企業の普及拡大

- デジタルデータ生成のスピードと量の増加

- 市場抑制要因

- クリプトジャッキングの脅威

第6章 市場セグメンテーション

- タイプ別

- 25RU未満

- 25~40RU

- 40RU以上

- 企業タイプ別

- 中小企業(SME)

- 大企業

- エンドユーザー業界別

- 小売・eコマース

- 教育

- BFSI

- IT・通信

- ヘルスケア

- 政府・防衛

- エネルギー・公益事業

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Dell EMC Inc.

- Huawei Technologies Co. Ltd

- Hewlett Packard Enterprise Development LP

- Eaton Corporation PLC

- Panduit Corp.

- Zellabox Pty Ltd

- Hitachi Ltd

- IBM Corporation

- Vertiv Co.

- Instant Data Centers LLC

- Dataracks

- Rittal GmbH & Co. Kg

- Canovate Group

第8章 投資分析

第9章 市場の将来

The Micro Mobile Data Center Market size is estimated at USD 10.46 billion in 2025, and is expected to reach USD 23.54 billion by 2030, at a CAGR of 17.62% during the forecast period (2025-2030).

Micro mobile data centers are box-like containers filled with the same storage, compute power, and networking needed in a regular data center but delivered in a compact unit. Moreover, with technological advancements, they come with integral cloud connectivity, completing a turnkey package for the edge.

Key Highlights

- The size, versatility, and plug-and-play features of micro mobile data centers make them ideal for use in remote locations for temporary deployments. They are also well suited for temporary use by businesses in locations that are in high-risk zones for floods or earthquakes. In other words, a micro data center minimizes the traditional model's physical footprint and energy consumed.

- Factors such as increasing global digitalization, internet penetration, the relevance of smart technologies, IoT-powered devices, big data, and the development of 5G networks are likely to drive the micro-mobile data center market trends. According to Ericsson, 5G subscriptions are forecast to increase drastically worldwide from 2019 to 2028, from over 12 million to over 4.5 billion, respectively.

- Furthermore, there is a rising need for containerized data centers as corporate offices migrate their infrastructure regularly. Furthermore, corporations spend more on micro-mobile data center growth as workloads increase. Such factors create significant chances for market expansion in the next years.

- Furthermore, businesses are increasing their cloud presence, necessitating the deployment of portable data centers and rising demand for micro mobile data centers for SMEs organizations due to low cost and lower latency. As a result, there would be more prospects for market growth in the future. However, integration with traditional data centers hampers the growth of the market.

- The COVID-19 outbreak positively impacted market growth, and micro-mobile data center technologies are assisting organizations in meeting the high capacity need for data storage. There is a rising requirement to guarantee that micro-mobile data center operators have the ability and capacity to offer high-performance micro-mobile data centers during periods of elevated data storage demand. After the pandemic, the market is growing rapidly with the increased digitization technologies and permanent work from home jobs. Increased demand for software as a service (SaaS) has driven traffic to data centers like never. Hence, players are investing in these solutions.

Micro Mobile Data Center Market Trends

Healthcare End User Vertical is Expected to Hold a Significant Market Share

- Adopting a micro mobile data center helps the healthcare industry bring flexibility, effectiveness, security, and a low-cost model to the healthcare sector. The global healthcare industry's growth is estimated further to drive the demand for micro mobile data centers.

- The growth of electronic health records (EHRs) further increases healthcare providers' demand for micro mobile data centers. Rather than replacing file rooms with server rooms, many opt to have documents hosted by the EHR vendor at a secure facility.

- The growth of Big Data is another motivational factor for transferring data to the cloud. Pulling different datasets together in the cloud allows operational, clinical, and financial data to be aggregated in Big Data analytics processes. These factors contribute to the growing adoption of micro mobile data centers in the healthcare industry.

- The penetration of IoT devices, especially smartphones, boosts the demand for micro mobile data centers in the healthcare industry. According to Ericsson, the number of short-range internet of things (IoT) devices reached 16.6 billion worldwide in the current year. That number is forecast to increase to 22.4 billion by the next three years. The wide-area IoT devices amounted to 3.2 billion in the current year and are predicted to reach 5.2 billion by the next three years. Patients want access to their health organization on their terms. These devices for Healthcare enable enriched data to flow securely through every point of care to help continuously improve the patient experience and health outcomes.

- With IoT and cloud technologies integration into Healthcare, concepts like blockchain are also gaining traction, increasing the demand for data storage and micro mobile data centers.

- Blockchain technology is being used to protect sensitive records and store and authenticate the data related to a user's identity as data generated through blockchain is extremely confidential in healthcare services, like micro mobile data centers have a great healthcare industry scope. Hence, the adoption of micro mobile data centers in the healthcare industry is expected to grow significantly over the forecast period.

Asia-Pacific is Expected to be the Fastest Growing Market

- Asia-Pacific is one of the world's fastest-growing areas for data centers. The adoption of automation and BI tools among SMEs is also high in the region. Hence, the region offers significant potential for the growth of the market studied.

- Much of this growth can be attributed to government agencies' widespread adoption of data centers during the last decade, especially in countries like China and Australia. Major government investments in data center advances, targeted at stimulating the region's digital economy, are boosting the adoption of cloud services, Big Data, and IoT.

- While the demand for cloud computing and other data services continues to increase in China, advancements in data center technology are expected to play a vital role in the integration of these technologies with modern manufacturing and China's gradual transition to a service economy.

- Increasing internet penetration in China would also help increase the demand for micro mobile data centers. Demand for faster, more stable broadband connections is growing in China as companies look to enhance their presence and provide enhanced quality and cybersecurity.

- The Australian investment outlook for data centers remains positive as colocation and cloud providers launch major construction projects and an armada of smaller enterprise facilities to prepare for a role in the accelerating digital future.

- In addition, factors, including high penetration rates in healthcare, retail, e-commerce, and BFSI verticals, are expected to drive the market's growth further. Moreover, the data generated through multiple sources is high due to the high adoption of BYOD and IoT devices in the workplace. The exponential growth of data proliferation in the region is forcing enterprises to invest in micro data centers.

- In the backdrop of current trends, hybrid cloud is emerging as a popular way forward for cloud adoption in Asia-Pacific, as it offers a choice of infrastructure depending on application requirements for compliance and security.

Micro Mobile Data Center Industry Overview

The micro mobile data center market is highly fragmented, with the presence of major players like Schneider Electric SE, Dell EMC Inc., Huawei Technologies Co. Ltd, Hewlett Packard Enterprise, Development LP, and Eaton Corporation PLC. Players in the market are adopting strategies such as partnerships, mergers, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2022 - For hybrid IT infrastructure management, Schneider Electric launched the EcoStruxure Micro Data Center R-Series 42U Medium Density. The new Micro Data Center solution is designed for IT applications in distant locations with industrial conditions, and it delivers fully integrated for easy setup. It also has a hefty weight capacity and huge industrial casters for convenient mobility.

- April 2022 - IBM Corporation announced a collaboration with Airtel, an Indian multinational telecommunications company, to provide edge cloud services in India. Together companies would supply edge cloud services to enterprises through 120 data centers spread across 20 major Indian cities. The collaboration improves the user experience and company performance by reducing latency while fulfilling sovereignty needs and data security, which is crucial as workloads travel to the edge.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Penetration of IOT Devices Enterprises

- 5.1.2 Increasing Speed and Volume of Digital Data Generation

- 5.2 Market Restraints

- 5.2.1 Cryptojacking Threats

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Up to 25 RU

- 6.1.2 25-40 RU

- 6.1.3 Above 40 RU

- 6.2 By Enterprise Type

- 6.2.1 Small and Medium Enterprise (SME)

- 6.2.2 Large Enterprise

- 6.3 By End-user Vertical

- 6.3.1 Retail and E-commerce

- 6.3.2 Education

- 6.3.3 BFSI

- 6.3.4 IT and Telecommunication

- 6.3.5 Healthcare

- 6.3.6 Government and Defense

- 6.3.7 Energy and Utilities

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Dell EMC Inc.

- 7.1.3 Huawei Technologies Co. Ltd

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Eaton Corporation PLC

- 7.1.6 Panduit Corp.

- 7.1.7 Zellabox Pty Ltd

- 7.1.8 Hitachi Ltd

- 7.1.9 IBM Corporation

- 7.1.10 Vertiv Co.

- 7.1.11 Instant Data Centers LLC

- 7.1.12 Dataracks

- 7.1.13 Rittal GmbH & Co. Kg

- 7.1.14 Canovate Group