|

市場調査レポート

商品コード

1851651

エッジアナリティクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Edge Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エッジアナリティクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

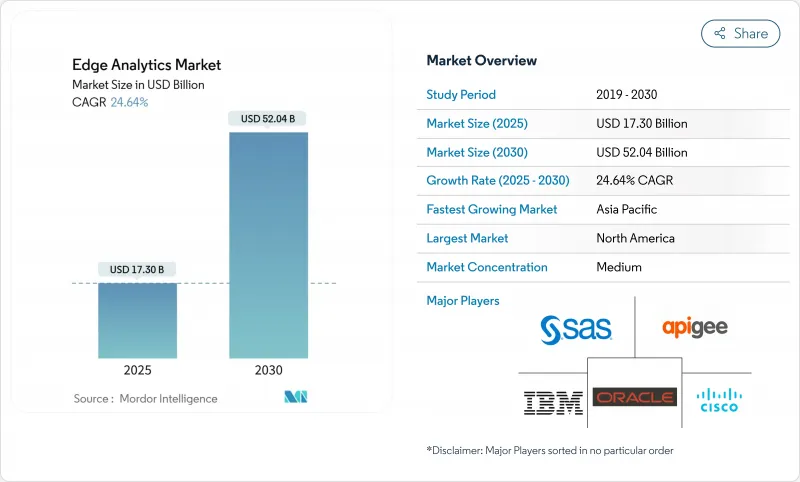

エッジアナリティクス市場規模は、2025年に173億米ドル、2030年には520億4,000万米ドルに達し、CAGR 24.64%を反映しています。

成長を後押ししているのは、IoTエンドポイントの急速な拡大、低遅延データパスをサポートする5Gカバレッジの拡大、推論エンジンをネットワークエッジに配置するAI対応シリコンの継続的な進歩です。ベンダーは、堅牢なマイクロデータセンター、液冷設計、機密データをローカルに保持しながらグローバルモデルを学習する連携学習フレームワークを優先しています。また、企業はクラウドネイティブなオーケストレーションツールを統合して、数千のエッジノードにまたがるアプリケーション配信を標準化することで、導入サイクルを短縮し、ROIの期待値を高めています。エッジアナリティクス市場は、特にリアルタイムの意思決定サポートと厳格なプライバシーの義務付けを共存させなければならないヘルスケアと金融において、データソブリンアーキテクチャに向けた規制の推進によってさらに影響を受けます。

世界のエッジアナリティクス市場の動向と洞察

IoTエンドポイントの急増

世界のデバイスベースは毎日3億2,877万TBのデータを生成しており、帯域幅を節約しリアルタイムで洞察を得られるよう、アナリティクスはローカル処理への移行を余儀なくされています。産業プラントでは現在、何百万ものセンサーから振動や温度のメトリクスがストリームされ、最適化されたモデルを実行するエッジ・アクセラレータが、10ミリ秒以下のレイテンシでこの流入を処理しています。予知保全のチェックが重機から医療用ウェアラブルまで拡大するにつれ、エッジアナリティクス市場は運用上のフットプリントを拡大し、企業のデータ戦略において不可欠なレイヤーとなります。

超低遅延アナリティクスの需要

自律型ロボット、遠隔手術装置、衝突回避システムは、5ミリ秒以内の意思決定を必要としています。エッジアナリティクスは、50~150ミリ秒のラウンドトリップを排除し、ミッションクリティカルな障害のリスクを低減します。欠陥検出アルゴリズムを地域のデータセンターからオンサイトノードに移した製造業者は、2桁の歩留まり向上を報告しており、分散インテリジェンスのビジネスケースを強化しています。

永続的なデータセキュリティと主権リスク

各エッジゲートウェイは、物理的なアクセスやパッチ未適用のファームウェアを通じて、敵が悪用できる攻撃対象領域をもたらします。また、ヘルスケア事業者は、ロケーションベースのデータ居住義務に準拠する必要があり、トラフィックをエンドツーエンドで暗号化する信頼された実行環境とゼロトラスト・オーバーレイの採用を促しています。

セグメント分析

処方的エンジンは、エッジアナリティクス市場で最も急速に成長しているレイヤであり、CAGR 25%で成長しています。このレイヤーは、基本的な記述的可視性に意思決定の自動化を追加し、異常が検出された時点で次善の策を推奨します。2024年には、記述的なモジュールが依然として売上の39%を占めているが、ユーザーの需要は、アウトプットを引き上げ、リスクを最小限に抑える、より高次の洞察へと明らかにシフトしています。エッジ・デバイスは現在、ロボット工学のパーチングをその場で最適化するコンパクトな強化学習エージェントをホストしており、この移行の背後にある商業的な牽引力を示しています。

予測アルゴリズムは、現在のダッシュボードと完全自動化の間の橋渡し役であり続けています。温度スパイクやトラフィックの急増を相関させることで、メンテナンスウィンドウや在庫ニーズの予測を可能にします。診断アナリティクスは、規模は小さいが、再発を防ぐ根本原因を明確にします。これらのスタックを組み合わせることで、ベンダーは、エントリポイントとして説明的なダッシュボードを組み込み、プレミアム加入者向けに処方的なアドオンを重ねることで、階層化されたサービスをパッケージ化することができます。その結果、エッジアナリティクス業界は成果ベースの契約に向けて成熟し続けています。

2024年のエッジアナリティクス市場規模の56%はオンプレミスノードが占めています。オンプレミス・ノードは、個人を特定できる情報や国家安全保障情報をエクスポートできないデータ機密性の高いセクターにとって、第一の選択肢であり続けています。例えば、病院ネットワークでは、放射線技師が外部リンクを経由せずにスキャン画像にアクセスできるよう、画像サーバーを社内で管理しています。しかし、クラウド管理されたエッジは、プロバイダーが居住規則を満たす地域ゾーンを立ち上げるにつれて、2030年までのCAGRが27.5%になるなど、急速に拡大しています。

長期的にはハイブリッド・トポロジーが主流になりつつあります。機密性の高いワークロードはローカルで推論を行い、バッチの動向分析は集中型クラウドで一晩中実行されます。中央のコンソールがコンテナの更新をプッシュし、ポリシーを調和させ、経営陣のダッシュボード用に集約された洞察を収集することで、俊敏性を犠牲にすることなく制御を実現します。インフラストラクチャの重複を削減し、データオリジンの近くにコンピューティングを維持することで、予算とコンプライアンスの両方の目標に合致します。

エッジアナリティクス市場レポートは、業界を展開タイプ(オンプレミス、クラウド)、コンポーネント(ソリューション、サービス)、技術(記述分析、診断分析、予測分析、処方分析)、エンドユーザー業界(BFSI、IT・通信、製造、ヘルスケア、小売、その他)、地域別に分類しています。

地域分析

北米は、成熟したハイパースケールデータセンターのフットプリントと初期の5G収益化戦略により、2024年の売上高43%で首位を維持。通信事業者は二次的な都市圏までカバレッジを拡大し、小売業者はマイクロデータセンターを郊外の店舗の近くに設置できるようになりました。政府の優遇措置により、製造業者はスマート・ファクトリー・プログラムを採用し、AI主導のプロセス制御をラインエッジに組み込むようになりました。暗号化と監査証跡が業界標準に合致していれば、プライバシー保護に関する裁定は依然として革新に寛容です。政策の明確化は調達サイクルを短縮し、ヘルスケア、小売、エネルギーの各分野で安定した需要を支えています。

アジア太平洋地域は最も急成長しており、2025-2030年のCAGRは27%と予測されています。中国は、スマート信号機や産業用ロボットからのセンサー・フィードを取り込む地方のエッジ施設の規模を拡大しています。日本の自動車大手は手直しコストを削減する予測品質ループを導入し、インドの携帯電話事業者は新たな周波数帯を活用して物流パーク向けのプライベート5Gキャンパスを立ち上げます。国境を越えたデータの流れに関する規制の立場は多様で、多国籍企業は、ベンダーの囲い込みを避けるためにオープンソースのスタックを使用することが多く、ローカライズされた展開に向かっています。国内半導体工場への投資は、地域の自立的サプライチェーンをさらに支え、エッジプロジェクトに弾力性を組み込みます。

欧州では、GDPRとAI責任法の提案に誘導されながら、堅調ながらも慎重な取り込みが見られます。ドイツは、OPC UAゲートウェイとコンテナ化された推論で伝統的な工場を改修するIndustrie 4.0プロジェクトの先駆者であり、イノベーションとリスクガバナンスのバランスをとっています。フランスでは、スマート・トランスポート・パイロットを主導し、路側機のリアルタイム・ビデオ解析により、公共安全への対応時間を改善。北欧の事業者は、ESG指令を尊重するため、環境に優しい水素エネルギーによるエッジサイトを優先。標準化団体は、セキュアブート、リモート認証、データ交換のフレームワークで協力し、より広いエッジアナリティクス市場に利益をもたらす相互運用性の理念を育んでいます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- IoTエンドポイントの普及

- 超低遅延分析への需要

- エッジの使用事例を解き放つ急速な5G展開

- エッジ展開を簡素化するクラウドネイティブなツールチェーン

- データプライバシーを強化するオンデバイス連携学習

- 熱密度の高いAIを実現する液冷マイクロデータセンター

- 市場抑制要因

- 永続的なデータセキュリティと主権リスク

- ブラウンフィールドOTシステムとの統合の複雑さ

- 極小ML/エッジAIエンジニアリング人材の希少性

- 分散コンピューティングノードにおけるESG主導の電力上限規制

- 重要な規制枠組みの評価

- バリューチェーン分析

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要利害関係者の影響評価

- 主な使用事例とケーススタディ

- 市場のマクロ経済要因への影響

- 投資分析

第5章 市場セグメンテーション

- 展開タイプ別

- オンプレミス

- クラウド

- コンポーネント別

- ソリューション

- サービス

- エンドユーザー業界別

- BFSI

- IT・通信

- 製造業

- ヘルスケア

- 小売り

- その他

- 技術別

- 記述的分析

- 診断分析

- 予測分析

- 処方的分析

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- その他欧州地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- オーストラリア

- ニュージーランド

- その他アジア太平洋地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- Apigee Corporation

- Dell Technologies Inc.

- Intel Corporation

- Oracle Corporation

- SAS Institute Inc.

- Amazon Web Services Inc.

- Google Cloud Platform

- Hewlett Packard Enterprise

- Schneider Electric SE

- Huawei Technologies Co.

- SAP SE

- Siemens AG

- GE Digital

- Foghorn Systems

- Edge Impulse Inc.

- Greenwave Systems

- Predixion Software

- AGT International Inc.