|

市場調査レポート

商品コード

1910484

配向性ストランドボード(OSB):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Oriented Strand Board (OSB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 配向性ストランドボード(OSB):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

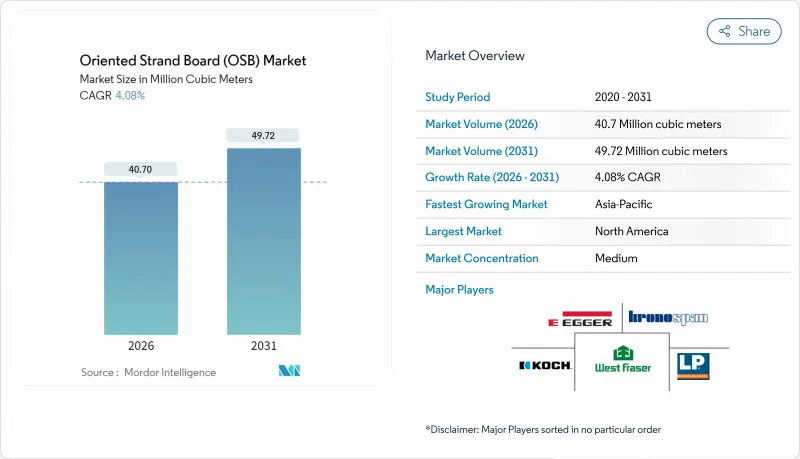

2026年の配向性ストランドボード(OSB)市場規模は4,070万立方メートルと推定され、2025年の3,910万立方メートルから成長が見込まれます。

2031年には4,972万立方メートルに達し、2026年から2031年にかけてCAGR4.08%で拡大する見通しです。

この着実な成長軌跡は、合板に対するコスト優位性、低炭素材料を後押しする規制面での追い風、プロセス自動化への投資が、OSB市場全体の需要を強化していることを浮き彫りにしています。成熟地域の建設業者は運営効率を追求し、新興経済国の政府はインフラ資金をエンジニアードウッドに振り向けており、これらが相まって健全な数量成長を支えています。競合活動は工場の自動化とグレードの革新に焦点が当てられており、ウェイアーハウザー社のAIによる乾燥機の最適化は、デジタルツールが生産量と下流工程のパネル品質を向上させている好例です。

世界の配向性ストランドボード(OSB)市場の動向と洞察

合板に対する費用対効果の高い代替材

メーカー各社は、ストランド配置ソフトウェアと精密樹脂投与技術を活用し変動費を削減することで、針葉樹合板との生産コスト差を継続的に縮小しています。ルイジアナ・パシフィック社は2025年第1四半期にOSB売上高2億6,700万米ドルを記録し、スポット価格が11%下落したにもかかわらず出荷量を維持。これは、合板生産能力の制約により需要がシフトした分をOSB市場が吸収している実態を裏付けています。特に木材価格が1立方メートルあたり100米ドル超の変動を示す状況下では、予測可能なパネル価格設定が住宅建築業者の予算確実性を支えます。その結果、配向性ストランドボード市場は、従来合板が支配していた内装仕上げ材や家具用基材分野へも進出しています。

世界の建設活動の拡大

アジア太平洋地域のインフラ整備推進は依然として最大の需要転換点であり、同地域のCAGR6.34%の見通しに反映されています。中国の丸太コストが1立方メートルあたり110米ドルで安定していることは、パネル購入者にとって利益率の見通しを裏付ける一方、インドとインドネシアの公共事業パイプラインは、長期的なエンジニアードウッドの需要拡大を後押ししています。北米における一戸建て住宅着工件数は2024年に7%増加し、建設業者がOSBの均一な釘保持能力を評価した結果、外装用合板の需要増につながりました。中東では、サウジアラビアとUAEの1,800億米ドル規模の脱炭素化計画により木材輸入量が3倍に増加し、輸出業者が新たなOSB市場の需要層を開拓する機会が生まれています。プレハブ工場ではOSBの寸法精度を活用して施工サイクルを短縮しており、建設需要の勢いとパネル消費がさらに連動しています。

ホルムアルデヒド及びVOC規制の強化

EUでは2026年8月よりホルムアルデヒド濃度0.080mg/m3未満の規制が施行され、UF樹脂に依存するメーカーは配合変更かシェア譲渡を迫られます。MDIバインダー製OSBは免除対象となる場合が多いもの、化学組成変更により変動費が15~20%増加し、コモディティグレードの利益率が圧迫されます。米国では、EPAのリスク評価草案が62の使用事例を特定し、職場曝露基準の強化を促す可能性があります。これにより換気設備や試験施設の拡充に向けた資本支出が発生します。コンプライアンス対応では、接着剤の研究開発規模を有する垂直統合型事業者が有利であり、OSB市場における技術的俊敏性の戦略的重要性がさらに高まっています。

セグメント分析

OSB/3は2025年にOSB市場シェアの46.85%を占め、湿潤環境対応パネルを建築基準が推奨する追い風を受け、2031年までCAGR4.58%で市場規模を拡大し、OSB市場における役割をさらに拡大する見込みです。メーカーはフェノール・ホルムアルデヒド樹脂またはMDI樹脂を採用し、ねじ保持力を損なわずに耐水性を実現。これにより集合住宅の壁体や屋根デッキ向けの仕様設計者に支持されています。一方、OSB/4はニッチな高荷重床材市場を獲得していますが、高密度化が価格感応度の高い需要の拡大を抑制しています。OSB/2は乾燥室内用下地板としてコスト効率を維持していますが、設計者が在庫管理効率化のため単一グレードでの一括調達を採用する傾向から、改良型OSB/3へのシェア流出に直面しています。

表面処理技術の革新により、OSB/3の用途はキャビネットや装飾市場へ拡大しています。これらは従来、粗い表面仕上げのため参入が困難でした。OSBコアにパーティクルボード表面材を貼り合わせたファインOSB製品ラインは、高圧ラミネートの接着を可能にし、下流用途を拡大。これにより家具産業集積地における配向性ストランドボードの市場浸透が促進されています。規制面では、ホルムアルデヒド規制強化の懸念からOSB/1の需要が減退。これにより工場設備投資は、従来型生産ラインを高付加価値構造用グレードへ転換する方向にシフトしています。

本オリエンテッド・ストランド・ボード報告書は、グレード別(OSB/1、OSB/2、OSB/3、OSB/4)、エンドユーザー用途別(建設、家具、包装)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(立方メートル)で提供されます。

地域別分析

北米は、豊富な既存工場基盤、統合された針葉樹供給網、建設業者による製品への高い認知度により、2025年においてもOSB市場シェアの60.05%を維持しました。米国は19億米ドル規模で世界最大の輸入国であり、国内工場が稼働率向上のためAI対応乾燥機を導入して近代化を進める中でも、主にカナダおよびブラジルの工場から調達しています。カナダは輸出志向を維持していますが、高騰する繊維原料コストにより、ウェストフレイザー社のフレイザーレイク工場閉鎖に見られるように、選択的な生産調整を余儀なくされています。これにより地域供給が逼迫し、価格を支える要因となっています。

アジア太平洋地域は成長の牽引役であり、中国、インド、ASEAN諸国が都市鉄道、データセンター、中層住宅プロジェクトを加速させることで、2031年までCAGR6.23%で拡大が見込まれます。ルリ・グループによる中国初のファインOSBライン稼働は、輸入依存から国内一貫生産への転換を示し、リードタイム短縮と現地規制に合わせたグレードのカスタマイズを実現します。インドのスマートシティ計画はエンジニアードパネルの採用を促進しており、コストと施工速度の面で無垢材を上回っています。東南アジアでは観光主導の宿泊施設建設で需要が増加していますが、現地生産能力が追いつかず、北米やチリの供給業者にとって輸入ルートが開かれています。

欧州では、厳格な気候規制が木材優遇政策を定着させる一方、成熟した住宅ストックが需要拡大を抑制し、安定ながらも低成長が続いております。EU全域で2026年に施行されるホルムアルデヒド規制により、非適合サプライヤーが淘汰され、既にMDIシステムを導入している工場の機会が増加する見込みです。南欧の改修税制優遇措置と北欧のプレハブ輸出が追い風となり、OSB市場はCLTの進出に対しても防御可能な状態を維持しております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 合板に対する費用対効果の高い代替品

- 世界の建設活動の拡大

- 持続可能性を重視したエンジニアードウッドへの需要

- モジュラーおよびプレハブ住宅ブーム

- 新興の低VOC MDI接着剤使用OSBグレード

- 市場抑制要因

- ホルムアルデヒド及びVOC規制の強化

- 木材繊維価格の変動性

- CLTの採用が構造材シェアを奪う

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- グレード別

- OSB/1

- OSB/2

- OSB/3

- OSB/4

- エンドユーザー用途別

- 建設

- 床と屋根

- 壁

- ドア

- 柱と梁(型枠)

- 階段

- その他の建設

- 家具

- 住宅

- 商業

- 包装

- 食品・飲料

- 産業

- 医薬品

- 化粧品

- その他の包装

- 建設

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Arbec Forest Products Inc.

- Besgrade Plywood Sdn. Bhd.

- Coillte

- EGGER

- J.M. Huber Corporation

- Koch IP Holdings, LLC

- Koyuncuoglu Group of Companies

- Kronoplus Limited

- Louisiana-Pacific Corporation

- RoyOMartin

- Sonae Arauco

- STRANDPLYOSB

- Swiss Krono Group

- Tolko Industries Ltd.

- West Fraser

- Weyerhaeuser Company

- Yalong Wood