セラミックインク:市場シェア分析、産業動向、成長予測(2025~2030年)

Ceramic Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641896

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

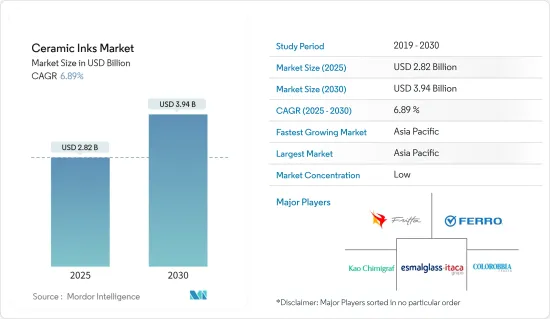

セラミックインクの市場規模は2025年に28億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.89%で、2030年には39億4,000万米ドルに達すると予測されています。

COVID-19パンデミックは市場にマイナスの影響を与えました。封鎖や制限により製造施設や工場が閉鎖されたためです。サプライチェーンと輸送の混乱はさらに市場に障害をもたらしました。しかし、2021年には業界は回復し、市場の需要は回復しました。

主なハイライト

- 短期的には、装飾ガラスとタイルの需要増が市場成長を牽引する要因です。

- 逆に、アナログからデジタル技術への移行に伴う高コストが市場成長の妨げとなる可能性が高いです。

- しかし、デジタル印刷の技術的進歩は、まもなく市場にとって好機となると予測されます。

- 予測期間中、アジア太平洋地域が世界のセラミックインク市場を独占すると予想されます。

セラミックインク市場の動向

セラミックタイルが急成長セグメント

- セラミックインク市場で最も急成長している用途はセラミックタイルです。顧客の機能的な要求に対応するために、建物の美観を向上させる必要性があります。

- セラミックタイルは、高い耐久性、耐摩耗性、色彩の永続性などの特性により、最もよく使用される素材となった。

- 過去数年間、世界中でセラミックタイルの需要が増加していることに起因する住宅建設支出の大幅な増加があります。例えば、Institution of Civil Engineers(ICE)の調査によると、世界の建設産業は主に中国、インド、米国が牽引し、2030年までに8兆米ドルに達すると予想されています。そのため、建設業界の成長によりセラミックタイルの需要が増加し、今後数年間でセラミックインク市場の需要がさらに高まると予想されます。

- インドは、アジア太平洋地域のG20経済圏の中で最も急成長している国であり続けると予想されています。インド政府は、3年間(2023~2025年)で3,765億米ドルのインフラ投資目標を発表しました。その中には、27の産業クラスター開発のための1,205億米ドル、道路・鉄道・港湾接続プロジェクトのための753億米ドルが含まれます。

- さらに、サウジアラビアは多くの商業プロジェクトに取り組んでおり、商業ビルの増加につながる可能性が高いです。5,000億米ドルの未来型メガシティ「Neom」プロジェクト、紅海プロジェクト-フェーズ1は2025年までに完成する予定で、5つの島と2つの内陸リゾートに広がる3,000室の14の高級・超高級ホテルが含まれます。リゾートには、キディヤ・エンターテインメント・シティ、超高級ウェルネス・ツーリズム・デスティネーションのアマアラ、アル・ウラにあるジャン・ヌーベルのシャラアン・リゾートなどが含まれます。そのため、商業建築への投資が増加し、セラミックインク市場の需要が上向くと予想されます。

- これらのセラミックタイルは、特に新興経済諸国において、ライフスタイルの変化や人口所得の増加に伴い、市場で大きな需要を獲得しました。その結果、消費者は他の床材や壁の装飾よりもセラミックタイルを好むようになっています。

- その結果、予測期間中にセラミックインクの需要を牽引することが期待されます。

アジア太平洋地域がセラミックインク市場をリードする見通し

- アジア太平洋地域が世界市場シェアを独占しています。インド、中国、フィリピン、ベトナム、インドネシアなどの国々で住宅や商業建設への投資が増加しており、セラミックインク市場は今後数年間で成長すると予想されます。

- 中国の大規模な建設部門はセラミックインクに大きな需要を生み出しました。さらに、中国はここ数年、世界のインフラへの主要な投資国の一つであるため、大きな貢献をしています。例えば、中国国家統計局(NBS)によると、2022年の中国における建設工事の生産額は27兆6,300億人民元(4兆1,085億8,100万米ドル)に達し、2021年と比較して6.6%増加しました。

- さらに、インドの住宅部門は増加傾向にあり、政府の支援やイニシアチブが需要をさらに押し上げています。インド・ブランド・エクイティ財団(IBEF)によると、住宅都市開発省(MoHUA)は2022~2023年の予算で98億5,000万米ドルを割り当て、住宅建設と停止中のプロジェクトを完成させるための資金作りを行っています。

- インドの食品印刷分野には、食品の保存と輸送のための包装を含む大きな市場があります。セラミックインクは食品容器の印刷やガラスの印刷などに広く使われています。例えば、インド・ブランド・エクイティ財団(IBEF)によると、インドの食品加工産業は急速に成長し、過去5年間のCAGRは8.3%でした。

- さらに、2023年には、食品加工市場は9,630億米ドルの売上を生み出し、2023年から2027年のCAGRは7.23%で拡大すると予想されています。このため、セラミックインク市場には食品包装からの上向きの需要が見込まれます。

- したがって、様々なアプリケーションセグメントからの需要の増加に伴い、セラミックインク市場は予測期間中にこの地域でより成長すると予想されます。

セラミックインク産業の概要

セラミックインク市場は細分化されています。この市場の主要企業(順不同)には、Ferro Corporation、FRITTA、Colorobbia Italia SpA、Kao Chimigraf、Esmalglass-Itaca Grupoなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 装飾ガラス・タイル需要の増加

- 建設セクターの急成長

- 市場抑制要因

- アナログ技術からデジタル技術への移行に伴う高コストの発生

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- 機能性インキ

- 装飾インキ

- 印刷技術別

- デジタル印刷

- アナログ印刷

- アプリケーション別

- セラミックタイル

- 住宅

- 非住宅

- ガラス印刷

- 食品容器印刷

- その他の用途

- セラミックタイル

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Colorobbia Italia SpA

- Esmalglass-Itaca Grupo

- Ferro Corporation

- FRITTA

- INKCID

- Kao Chimigraf

- Rex-Tone Industries Ltd

- Sicer S.P.A.

- Sun Chemical

- TECGLASS

- Torrecid

- ZSCHIMMER & SCHWARZ CHEMIE GMBH

第7章 市場機会と今後の動向

- デジタル印刷方式の技術進歩

- その他の機会

目次

The Ceramic Inks Market size is estimated at USD 2.82 billion in 2025, and is expected to reach USD 3.94 billion by 2030, at a CAGR of 6.89% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. It was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing demand for decorative glass and tiles are some factors driving the studied market's growth.

- Conversely, high-cost involvement in shifting from analog to digital technology will likely hinder the market's growth.

- However, technological advancements in digital printing are projected to act as an opportunity for the market shortly.

- Asia-Pacific is expected to dominate the global ceramic ink market during the forecast period.

Ceramic Inks Market Trends

Ceramic Tiles is the Fastest Growing Segment

- The fastest-growing application of the ceramic ink market is ceramic tiles. There is a need to improve the aesthetics of buildings to address the functional requirement of the customers.

- Ceramic tiles became the most popular materials that are being used, owing to properties such as high durability, resistance to wear, color permanence, etc.

- Over the past few years, there is a significant increase in residential construction spending, owing to which there is a rise in the demand for ceramic tiles across the globe. For instance, according to a study by the Institution of Civil Engineers (ICE), the global construction industry is expected to reach USD 8 trillion by 2030, primarily driven by China, India, and the United States. Therefore, the growing construction industry is expected to include an upside demand for ceramic tiles which further will boost the demand for ceramic inks market in the coming years.

- India is anticipated to remain the fastest-growing G20 economy in the Asia-Pacific region. The Indian government announced a target of USD 376.5 billion in infrastructure investment over three years (2023-2025), including USD 120.5 billion for developing 27 industrial clusters and USD 75.3 billion for road, railway, and port connectivity projects.

- Furthermore, Saudi Arabia is working on many commercial projects, likely leading to more commercial buildings. The USD 500 billion futuristic mega-city "Neom" project, the Red Sea Project - Phase 1, is expected to be completed by 2025 and includes 14 luxury and hyper-luxury hotels with 3,000 rooms spread across five islands and two inland resorts. The resorts include Qiddiya Entertainment City, Amaala - the uber-luxury wellness tourism destination, and Jean Nouvel's Sharaan resort in Al-Ula. Therefore, increasing investments in commercial constructions is expected to create an upside demand for the ceramic inks market.

- These ceramic tiles gained huge demand in the market, especially in developing economies with the changing lifestyle trend and increasing population income. As a result of this, consumers are preferring ceramic tiles over other flooring and wall decoration options.

- It, in turn, is expected to drive the demand for ceramic inks over the forecast period.

The Asia-Pacific Region is Expected to Lead the Ceramic Inks Market

- The Asia-Pacific region dominated the global market share. With growing investments in residential and commercial construction in the countries such as India, China, the Philippines, Vietnam, and Indonesia, the market for ceramic inks is expected to grow in the coming years.

- China's massive construction sector generated significant demand for ceramic inks. Moreover, China is a huge contributor, as it is one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to CNY 27.63 trillion (USD 4108.581 billion), an increase of 6.6% compared with 2021.

- Moreover, the residential sector in India is on an increasing trend, with government support and initiatives further boosting the demand. According to the India Brand Equity Foundation (IBEF), the Ministry of Housing and Urban Development (MoHUA) allocated USD 9.85 billion in the 2022-2023 budget to construct houses and create funds to complete the halted projects.

- The food printing sector in India includes a large market that involves packaging for the storage and transportation of food. Ceramic inks are widely used in food container printing, glass printing, etc. For instance, according to India Brand Equity Foundation (IBEF), the Indian food processing industry grew rapidly, with an average annual growth rate of 8.3% in the past 5 years.

- Moreover, in 2023, the food-processing market will generate USD 963 billion in revenue, and the market is anticipated to expand at a CAGR of 7.23% between 2023-2027. Therefore, this is expected to create an upside demand for the Ceramic inks market from food packaging.

- Hence, with the increasing demand from the various application segments, the ceramic inks market is expected to grow more in the region during the forecast period.

Ceramic Inks Industry Overview

The Ceramic Inks Market is fragmented in nature. The major players in this market (not in a particular order) include Ferro Corporation, FRITTA, Colorobbia Italia SpA, Kao Chimigraf, and Esmalglass-Itaca Grupo.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Decorative Glass and Tiles

- 4.1.2 Rapid Growth in the Construction Sector

- 4.2 Market Restraints

- 4.2.1 High-cost Involvement in Shifting of Analog Technology to Digital Technology

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Functional Inks

- 5.1.2 Decorative Inks

- 5.2 Printing Technology

- 5.2.1 Digital Printing

- 5.2.2 Analog Printing

- 5.3 Application

- 5.3.1 Ceramic Tiles

- 5.3.1.1 Residential

- 5.3.1.2 Non-residential

- 5.3.2 Glass Printing

- 5.3.3 Food Container Printing

- 5.3.4 Other Applications

- 5.3.1 Ceramic Tiles

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Colorobbia Italia SpA

- 6.4.2 Esmalglass - Itaca Grupo

- 6.4.3 Ferro Corporation

- 6.4.4 FRITTA

- 6.4.5 INKCID

- 6.4.6 Kao Chimigraf

- 6.4.7 Rex-Tone Industries Ltd

- 6.4.8 Sicer S.P.A.

- 6.4.9 Sun Chemical

- 6.4.10 TECGLASS

- 6.4.11 Torrecid

- 6.4.12 ZSCHIMMER & SCHWARZ CHEMIE GMBH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in Digital Printing Methods

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日